Crypto World

What NYSE’s Exploration of Onchain Systems Means for Financial Markets

Key takeaways

-

Intercontinental Exchange (ICE)’s blockchain-based initiative is about upgrading market infrastructure, not adopting cryptocurrencies. It intends to use blockchain for improving settlement, reconciliation and collateral efficiency.

-

Onchain delivery-vs.-payment settlement could significantly reduce counterparty risk and free up capital tied up in margins. It also shifts risk toward real-time liquidity needs and continuous funding requirements.

-

While 24/7 trading may expand global access, it does not necessarily solve deeper market-structure issues. It could introduce liquidity fragmentation, wider spreads and noisier price discovery during low-volume periods.

-

Stablecoins in this model act as institutional settlement rails rather than speculative assets. Their use inside regulated markets will require bank-grade custody, liquidity and compliance safeguards.

When Intercontinental Exchange (ICE), the parent company of the New York Stock Exchange (NYSE), announced it was developing a blockchain-based platform for tokenized securities, some observers interpreted it as traditional finance fully integrating crypto.

However, the initiative is just a strategic redesign of market infrastructure. The focus is on utilizing distributed ledgers to optimize collateral management and eliminate delays in legacy settlement systems.

ICE has indicated that the platform would enable 24/7 trading, incorporate onchain settlement elements, support stablecoin-based funding and feature tokenized versions of regulated securities, subject to regulatory approval. If rolled out at scale, this would represent one of the most significant efforts by a major exchange operator to weave blockchain technology into market operations.

This article explores how the NYSE is integrating blockchain to segregate execution from settlement, why onchain settlement becomes critical, the importance of 24/7 trading and stablecoins as institutional funding rails. It discusses how tokenization is becoming a part of mainstream finance, hurdles in the integration of blockchain technology with legacy systems and issues regarding adaptation.

How the NYSE is using blockchain technology to separate execution from settlement

The platform maintains a clear separation between trading and settlement. ICE plans to continue using the existing NYSE Pillar matching engine, which already manages high-volume equity trading, as the primary trading layer. Blockchain technology would primarily enhance post-trade processes, such as settlement, record-keeping and reconciliation.

This distinction is important, as inefficiencies in financial markets generally stem not from price discovery during trading but from delays and complexities in clearing, settlement, cross-party reconciliation and collateral handling.

Tokenized securities refer to regulated assets like stocks or exchange-traded funds (ETFs) whose ownership is recorded on a blockchain for greater efficiency. The underlying legal rights continue to be governed by existing securities laws and corporate regulations.

Why onchain settlement likely matters more than 24/7 trading

Even with faster settlement cycles in US equities, most trades still depend on multiple intermediaries, such as clearinghouses, custodians and agents, that reconcile records across parties. This creates layers of operational complexity and lingering counterparty risk during the settlement window.

Onchain settlement changes this fundamentally by enabling near-simultaneous transfer of ownership and payment on a shared, immutable ledger. This process, also called delivery-vs.-payment (DvP), sharply reduces counterparty exposure and minimizes reconciliation errors. DvP could free up capital tied up in margins or buffers for more productive uses. It tackles the core inefficiencies and risks in post-trade infrastructure.

Faster settlement, however, is not without trade-offs. It eliminates the time buffers that currently allow markets to resolve errors, unwind failed trades or handle liquidity squeezes. Risk simply shifts toward real-time liquidity demands, requiring participants to fund positions continuously rather than leaning on intraday credit. From a broader view, this redistributes rather than removes systemic risk.

What 24/7 trading may (and may not) achieve

Continuous trading appeals to global investors familiar with round-the-clock crypto or futures markets. For US equities, extended hours already exist, but they typically feature lower liquidity, wider spreads and higher volatility compared with core sessions.

Fully 24/7 markets could offer better access for international participants and potentially smoother reactions to off-hour news. Yet several concerns remain:

-

Liquidity could thin out during quieter periods, forcing market makers to widen quotes or increase trading costs.

-

Overnight or low-volume trading might amplify price swings, particularly around major global events.

-

Price discovery could stay concentrated in traditional hours, with off-hours reflecting noisier or less representative signals rather than true efficiency gains.

Whether continuous trading truly enhances market quality or just spreads activity more thinly across time zones is still an open question.

Onchain settlement addresses deeper structural frictions in how trades are finalized, reducing risk and unlocking efficiency, while 24/7 trading mainly extends availability without necessarily fixing those underlying issues.

Did you know? Some stock exchanges already use microsecond-level timestamp synchronization from atomic clocks to track trade sequences. This means blockchain systems must integrate with ultra-precise time standards to avoid disputes over transaction ordering.

Stablecoins as institutional funding rails, not speculative plays

A key element in ICE’s proposal is the use of stablecoins to handle the cash side of trades. This would let funds settle 24/7, aligning with any move toward continuous securities trading and bypassing traditional bank-hour limitations. The process results in quicker, lower-friction movement of cash across borders and between counterparties.

If stablecoins are embedded in regulated market infrastructure, they are certain to face stringent compliance requirements. These include real-time compliance monitoring, high-grade custody arrangements, robust liquidity buffers and other safeguards on par with traditional settlement banks.

Stablecoins function strictly as wholesale settlement tools for institutions, not as retail payment or speculative instruments.

Tokenization steadily moving into mainstream finance

The NYSE-related efforts are part of a broader trend. Major asset managers, banks and market infrastructure providers are actively piloting or seeking approval to tokenize conventional assets. These include US Treasury bills, money market fund shares, ETF units and similar instruments.

Regulatory filings demonstrate that tokenization is expanding into areas traditionally seen as conservative and infrastructure-heavy. The objective is operational efficiency rather than innovation for its own sake. Advantages include accelerated settlement, programmable conditions, reduced manual reconciliation and potentially wider participation.

If tokenized versions of multiple asset classes become commonplace, post-trade processes could converge toward shared, interoperable ledger architectures. This would reduce overlap and duplication across today’s fragmented ecosystem of clearinghouses, custodians, transfer agents and registrars. However, to facilitate such an outcome, institutions and regulators need to align on standards, interoperability and risk controls.

Did you know? In traditional markets, a single stock trade can trigger a string of back-office messages between brokers, custodians and clearing agents, which is a key reason financial firms spend billions annually on post-trade IT systems.

Custody, records and legal ownership still the hardest hurdles

The biggest barrier to tokenized markets isn’t the blockchain technology itself. There is legal ambiguity regarding ownership. Traditional finance relies on clear, well-established rules for beneficial ownership, shareholder rights, voting, dividends and who maintains the definitive record.

In a tokenized world, regulators will need to decide what counts as the authoritative source of truth, whether it is the onchain ledger, the transfer agent’s registry, the broker-dealer’s books or some hybrid. Each choice affects investor protections, how corporate actions are handled, how disputes are resolved and who bears liability.

Custody adds another layer of difficulty. Even in permissioned, institutional-grade blockchains, managing private keys or equivalent controls requires robust answers on asset segregation, key recovery in case of loss, bankruptcy remoteness and operational continuity. These issues demand new frameworks that match or exceed existing standards.

These legal and operational questions are likely to slow adoption more than any technical limitations.

Clearinghouses and the shift to real-time risk management

ICE has also indicated interest in bringing tokenized deposits or similar mechanisms into clearinghouse operations. It has suggested integrating blockchain-based settlement tools with clearing infrastructure.

Clearinghouses have a role to play in neutralizing counterparty risk. Shorter or near-instant settlement windows can shrink exposure periods and lower overall risk. However, they also result in less time to detect and respond to defaults, collateral deficiencies or sudden liquidity stress.

This pushes clearing participants and operators toward continuous position monitoring, automated intraday margin calls, dynamic collateral valuation and well-tested playbooks for outages, cyber events or technology failures.

From a regulatory perspective, resilience in always-on, 24/7 environments becomes critical. Traditional markets have scheduled downtime. Continuous systems cannot afford unplanned interruptions without risking cascading outages.

Did you know? The NYSE once shortened its trading day during World War I and even shut down completely for four months in 1914. This shows that market “hours” have always evolved with technology, geopolitics and infrastructure limits.

Who stands to gain and who might need to adapt

If onchain market infrastructure demonstrates reliability and receives regulatory approval, several participants could see meaningful advantages:

-

Global investors who want uninterrupted access to trading and settlement

-

Institutions that could unlock more efficient use of collateral and reduce trapped capital

-

Issuers interested in streamlined distribution channels and potentially broader reach.

On the flip side, intermediaries whose revenues rely heavily on today’s multi-step settlement workflows may face strong pressure to evolve or risk losing relevance. These include clearing agents, custodians and certain reconciliation services. Compliance teams would also shift from periodic, market-hours reporting to continuous oversight, adding complexity in the short term.

Whether these operational savings translate into lower costs for retail and institutional end investors depends on the level of efficiency passed through by exchanges, clearinghouses and other infrastructure providers.

A modernization effort, not a leap into crypto

The NYSE’s work on blockchain-based systems is an attempt to upgrade core financial infrastructure, including faster settlement, better collateral mobility and improved market access. In this case, blockchain serves as a technology layer for post-trade operations, not as an asset class. Success hinges on meeting the stringent requirements of regulated markets, including proven scalability, high operational resilience, full compliance alignment and broad institutional buy-in.

The success of this endeavor by the NYSE depends on several parameters, such as regulatory approvals, operational reliability and institutional willingness to migrate. The initiative signals that traditional exchanges are no longer treating tokenization as an experimental side project. Instead, they are evaluating whether blockchain-based systems can support the scale, stability and compliance demands of mainstream financial markets. This is a much higher bar than most crypto-native platforms have faced.

Cointelegraph maintains full editorial independence. The selection, commissioning and publication of Features and Magazine content are not influenced by advertisers, partners or commercial relationships.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Investors eye presales as capital shifts to early-stage projects like DOGEBALL, targeting high-growth potential.

Summary

- DOGEBALL presale 2026 offers early access to DOGECHAIN, a Layer 2 blockchain with 2-sec blocks and near-zero fees

- Early buyers can use code DB25 for a 25% bonus, capturing massive upside before Q1 2026 altcoin rally

- DOGEBALL pairs viral meme utility with high-speed gaming blockchain, aiming for 50x–100x returns in 2026 presale

Waking up to a sea of green candles is the dream of every trader, but the real “overnight” successes are actually authored months in advance during quiet presale windows.

While the majority of the market is currently distracted by high-cap coins fighting for 5% gains, savvy capital is flowing into early-stage infrastructure projects that offer a clear path to 50x or 100x returns. The window for the next 100x crypto presale is currently open with DOGEBALL (DOGEBALL), a project that pairs viral meme appeal with a high-performance Layer 2 blockchain.

For those who have ever looked at a price chart and wished they had a time machine to go back to the ICO stages of the world’s most successful tokens are currently standing at a similar crossroads.

The next 100x crypto presale isn’t just about finding a lucky ticker symbol; it is about identifying projects with “Stage 1” pricing and “Tier 1” utility. DOGEBALL has already raised over $180,000, signaling that the smart money has identified its $0.015 launch price as a massive arbitrage opportunity compared to the current $0.0004 entry point.

From $0.29 to millions: The Massive ROI lessons from Polkadot

Polkadot (DOT) remains the ultimate case study for why early participation in the next 100x crypto presale is the most effective wealth-building strategy in this industry. During its initial offering, DOT was available for just $0.29, a price that many “safe” investors ignored because the technology seemed unproven. Those who recognized the necessity of its interoperability protocol saw their modest investments transform into life-changing portfolios as the token multiplied by more than 180x at its peak valuation.

The psychological barrier of “being too late” often stops people from entering the market, but the crypto ecosystem consistently produces new cycles of innovation. The good news for those who missed the Polkadot surge is that 2026 has introduced a fresh opportunity with even higher utility. By identifying the next 100x crypto presale like DOGEBALL now, you are positioning yourself at the same foundational level that turned early DOT buyers into crypto millionaires before the rest of the world caught on.

Why the DOGEBALL crypto presale 2026 is outperforming competitors

The DOGEBALL crypto presale 2026 stands apart because it is the native utility token for DOGECHAIN, a custom-built Ethereum Layer 2 blockchain. Unlike standard meme projects that exist only on paper, DOGECHAIN is a functional, testable environment designed specifically to handle high-frequency gaming transactions with near-zero fees. This isn’t just a token; it is a proprietary piece of technology that offers lightning-fast 2-second block times and full EVM compatibility for developers.

Investors are flocking to this DOGEBALL crypto presale 2026 because it solves the “utility gap” found in most low-cap coins. With an integrated online game and a massive $1m prize pool already active, the token has immediate demand. The presale is strategically capped at just four months, running from January 2nd to May 2nd, 2026. This aggressive timeline ensures that the community stays engaged and the project launches exactly when the Q1 altcoin bull run is expected to hit its peak velocity.

Calculate 50x gain and secure a 25% bonus today

The mathematics behind the next 100x crypto presale is incredibly compelling for early participants. Someone who secures DOGEBALL at the current Stage 2 price of $0.0004 is locking in a 3,650% increase based solely on the $0.015 listing price. This does not even account for the post-launch “moon” potential as the token hits major exchanges. By acting now, you are essentially buying an asset at a fraction of its intended market value before the general public is allowed to trade it.

To maximize the position, they can use the limited-time bonus code DB25 during their purchase to receive an instant 25% boost in their token count. This means for every 1,000 tokens someone buys, they get an extra 250 for free, significantly lowering their risk and increasing their upside. As the project nears its $490k Stage 3 milestone, the price will increase again, making today the most profitable time to enter the next 100x crypto presale ecosystem.

How to join the Dogeball crypto presale 2026 in three steps

Joining the DOGEBALL crypto presale 2026 is a seamless process designed for both veteran traders and newcomers. First, visit the official website and connect a preferred digital wallet, such as MetaMask or Trust Wallet. The platform is highly flexible, accepting a wide range of currencies, including ETH, USDT, BNB, SOL, and even direct Credit or Debit card payments for those who prefer to buy with fiat.

Once a wallet is connected, simply enter the amount to invest and remember to input the code DB25 in the bonus field. This ensures that 25% extra DOGEBALL tokens are immediately obtained. After confirming the transaction, tokens will be visible on the dashboard. Take advantage of the 80% APY staking rewards during the presale period to allow the bag of this next 100x crypto presale to grow passively while waiting for the May 2nd launch.

The final countdown to the Dogeball crypto presale launch

As we conclude this analysis of the next 100x crypto presale, it is clear that DOGEBALL is the most structured opportunity of 2026. We have discussed the historical success of Polkadot, the unique Layer 2 technology powering DOGECHAIN, and the massive 100% “Buyer of the Week” bonuses that have already sparked intense competition among whales. This project isn’t just selling a dream; it is delivering a fully audited, high-utility ecosystem that is ready for mass adoption.

The DOGEBALL crypto presale 2026 represents the perfect convergence of memecoin viral energy and serious blockchain infrastructure. With only a few weeks remaining in the 4-month window, the time for hesitation has passed. Use the bonus code DB25 today to secure 25% extra tokens and hold a significant stake before the token lists at $0.015. Don’t let this be another “what if” story; make DOGEBALL a ticket to the 2026 bull run.

For more information, visit the official website, Telegram, and X.

FAQs for the next 100x crypto presale

What is the next 100x crypto presale to buy right now?

DOGEBALL (DOGEBALL) is currently the next 100x crypto presale to watch because of its proprietary Layer 2 blockchain and its planned 50x jump from Stage 1 pricing to its $0.015 listing price. The project offers real gaming utility and a verified audit.

Which crypto will give 100x in 2026 for early investors?

Many analysts believe the next 100x crypto presale will be DOGEBALL due to its 80% staking rewards and its position as the first ETH L2 built specifically for gaming. The short 4-month presale window also creates rapid momentum for a successful market launch.

What makes a crypto presale successful in the long term?

A successful next 100x crypto presale requires real utility, which DOGEBALL provides through its $1m gaming prize pool and zero-tax DOGECHAIN. Unlike temporary hype projects, DOGEBALL has a long-term roadmap including CEX listings and corporate gaming partnerships.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Resolv Labs burns 36.7m hacked USR after a key compromise let an attacker mint 80m unbacked tokens and dump $24.5m in ETH, leaving a $34m hole in the protocol.

Summary

- Resolv Labs used a contract upgrade to burn 36.73m USR from the attacker’s address after March’s minting exploit.

- The attacker created 80m unbacked USR with under $200k in collateral and dumped 34m USR for about 11,409 ETH (~$24.48m).

- The episode spotlights DeFi key management failures as Resolv faces an estimated $34m net loss despite claiming its collateral pool is intact.

Resolv Labs has destroyed 36.73 million USR stablecoins previously controlled by an attacker, using a contract upgrade to claw back part of the haul from a March exploit that printed 80 million unbacked tokens and left the protocol nursing an estimated $34 million loss. According to on-chain analyst Yu Jin, “about 1 hour ago, Resolv Labs destroyed 36.73 million USR held by the hacker through a contract upgrade,” after the exploiter had already liquidated roughly 34 million USR for 11,409 ETH (about $24.48 million) now parked at address 0x8ED…81C. In total, Resolv’s team has removed about 46 million USR from the attacker’s address, but the value extracted in ETH leaves the protocol facing a real economic hit of around $34 million.

The incident stems from a critical failure in Resolv’s USR minting flow that allowed a single attacker, using less than $200,000 in initial collateral, to generate 80 million uncollateralized USR and dump them across DeFi liquidity pools. Chainalysis described it as a case where “an attacker was able to mint tens of millions of Resolv’s unbacked stablecoins (USR) and extract roughly $23 million in value,” highlighting how a compromised service key in a two-step off-chain minting process can cascade into systemic losses. In its earlier coverage, crypto.news reported that USR “lost its peg after an attacker minted millions of unbacked tokens,” forcing Resolv Labs to pause operations and roll out a recovery plan as the stablecoin crashed as low as $0.14 before partially rebounding.

DeFi reacts as USR exploit ripples through markets

The USR exploit has become a case study in DeFi key management risk, drawing comparisons with other recent stablecoin failures and lending-market contagion. In a post-mortem, Resolv Labs stressed that its collateral pool “remains intact” despite the exploit-driven mint of 80 million USR, even as liquidity providers and leveraged users across integrated protocols absorbed price slippage and forced unwinds. Earlier analysis of the crash showed USR at one point trading near $0.23–$0.27, with on-chain data firms estimating attacker profits between $23 million and $25 million as the token depegged on Curve and other pools.

The partial burn of 36.73 million USR via contract upgrade underscores how privileged controls can both enable and mitigate catastrophic failures in nominally decentralized systems. For traders watching Resolv and its governance token RESOLV, which previously saw volatile swings after exchange listings and buybacks, the episode revives long‑standing questions over whether yield-bearing stablecoins can scale without introducing single points of failure. As crypto.news noted in a prior story on the USR depeg, DeFi protocols with composable stablecoins now face renewed pressure to harden minting logic, rotate keys, and treat backend infrastructure with the same rigor as audited smart contracts.

Chaos Labs is ending its three‑year Aave mandate after a $27m oracle fiasco, deep governance infighting, and mounting fears over who is legally liable when DeFi risk breaks.

Summary

- Chaos Labs is terminating its Aave mandate after three years, citing a fundamental dispute over how the $27 billion lending protocol should manage risk.

- The move follows high‑profile exits by Aave Chan Initiative and BGD Labs, deepening governance turmoil at DeFi’s largest money market.

- Chaos also flags undefined legal liability for DeFi risk managers after recent oracle failures triggered tens of millions of dollars in erroneous liquidations on Aave.

Chaos Labs, the risk firm that has “priced every loan initiated on Aave and managed risk across all Aave V2 and V3 markets and networks” since late 2022, is walking away from the protocol after concluding “the engagement no longer reflects how we believe risk should be managed.” In an announcement echoed by BSCN on X, the company said Monday it is “proactively terminating its engagement with DeFi’s largest lending protocol @aave, citing a fundamental disagreement over how risk should be managed,” and warning that DeFi risk managers currently operate without a clear regulatory framework or safe harbor if something breaks.

The departure lands as Aave, which has processed roughly $3.33 trillion in cumulative deposits and nearly $1 trillion in loans and recently crossed $50 billion in total value locked, faces mounting internal and external scrutiny over governance, risk, and legal exposure.

Chaos is the third core contributor to step back from Aave in recent months, after governance shop Aave Chan Initiative and core technical team BGD Labs each disclosed plans to end their mandates amid disputes over power, budgets and roadmap control inside the DAO. ACI founder Marc Zeller framed his own exit as the product of a protracted power struggle, warning that a recent vote handed Aave Labs “the largest budget in DAO history,” while BGD told tokenholders “we will not be seeking a renewal and will cease our contribution to Aave” once its contract expires. These fractures are emerging even as Aave continues to command roughly 30–40% of the DeFi lending market and nearly a quarter of sector TVL, underscoring how governance tensions can flare precisely when protocols reach systemically important scale.

Chaos Labs’ break with Aave follows a series of oracle and risk‑engine incidents that have already driven uncomfortable questions about who is accountable when automated risk systems misfire. In March, a misconfigured Chaos Labs oracle on Aave caused erroneous liquidations of around $26.9 million in positions using staked Ether collateral, after the CAPO risk agent reported an inaccurately low price ratio and pushed several accounts below their health‑factor thresholds. A separate post‑mortem and external coverage estimated roughly $27 million in forced liquidations triggered when wrapped staked Ether was undervalued by about 2.85%, affecting at least 34 high‑leverage positions before parameters were manually corrected. Chaos Labs and Aave have emphasized that no bad debt was incurred and that affected users would be reimbursed, but the episode illustrates the legal gray zone the firm now highlights: risk managers are making protocol‑wide decisions that can move tens of millions of dollars in seconds, yet operate without explicit regulatory safe harbor or clearly defined liability regimes if those decisions go wrong.

The exits of Chaos Labs, ACI and BGD Labs leave Aave’s DAO with fewer seasoned operators just as the protocol rolls out its next‑generation v4 architecture and pushes deeper into institutional‑grade features. Aave’s total value locked sits in the tens of billions of dollars and the protocol has grown its TVL by more than 50% in certain recent quarters, outpacing the broader DeFi sector and making its risk governance choices a live concern for markets well beyond crypto‑native users. With multiple core contributors now publicly criticizing governance dynamics and risk alignment, Aave’s community will be forced to answer the question Chaos Labs has implicitly posed: who, exactly, bears responsibility when decentralized risk systems break at scale?

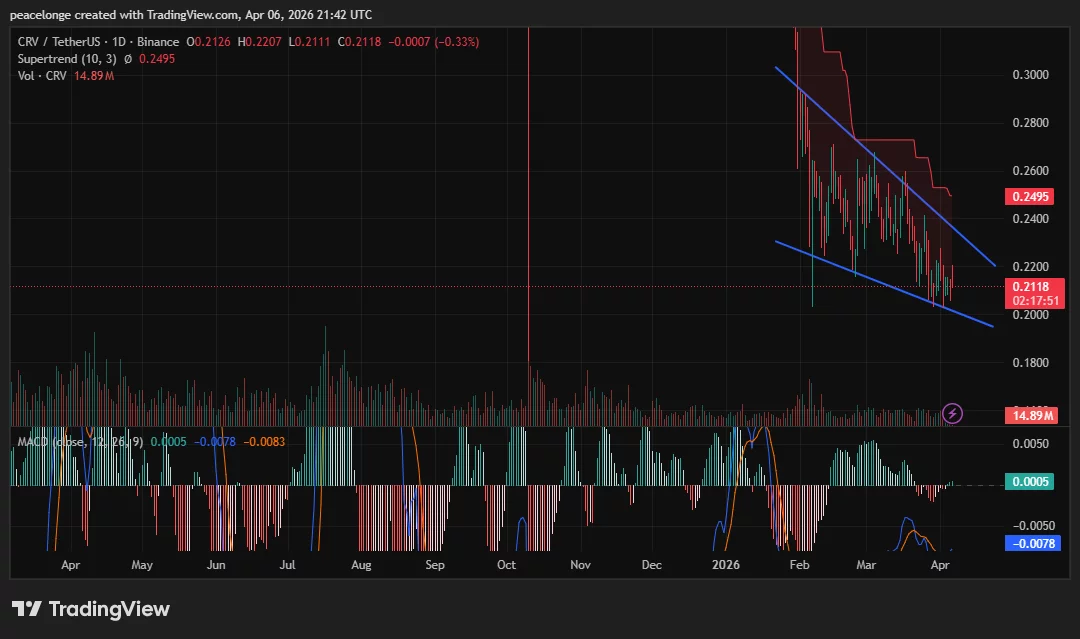

CRV price has been grinding lower since late 2025, and the Curve DAO token is now pressing against the lower boundary of a descending channel that has defined its price action for months. The $0.20 level is within reach, and the chart is setting up a clear binary outcome: hold and recover, or break into uncharted territory.

Summary

- CRV price is at $0.2118 on April 6, approaching the lower boundary of a descending channel in place since late 2025, with the $0.20 psychological level as the key downside reference.

- The daily Supertrend at $0.2495 confirms the bearish trend, though the MACD line at 0.0005 has crossed marginally above the signal at -0.0078, a tentative early stabilisation signal.

- A daily close below the channel lower bound near $0.21 exposes $0.20, while a recovery above the Supertrend at $0.2495 is required to shift the bias toward neutral.

Curve DAO (CRV) price is trading at $0.2118 on April 6, down 8.10% over the prior 24 hours, as the Curve DAO token continues to lose ground within a descending channel that has defined its structure since late 2025. The token is pressing against the lower boundary of that channel, with $0.20 now the critical downside reference for traders watching the DeFi sector’s largest decentralised exchange protocol.

On the daily chart, CRV has been contained within a descending channel since late 2025, with the upper trendline aligning with the Supertrend at $0.2495 and acting as rolling bearish resistance. The lower channel boundary is converging on price near $0.20, leaving a narrowing range that typically precedes a more directional move. The daily MACD shows the MACD line at 0.0005 crossing marginally above the signal at -0.0078, a tentative early stabilisation signal, though volume has not produced any spike that would confirm genuine accumulation behind that reading.

On the 4H chart, a descending wedge pattern has formed between two converging trendlines, with the lower bound at the Supertrend support of $0.2071 and the upper bound at $0.2224. A descending wedge is technically a bullish reversal pattern, though the 4H MACD at 0.0004 is essentially flat, providing no directional confirmation at this timeframe.

A March 2 flash loan exploit on the sDOLA-crvUSD Curve LlamaLend pool, involving an improper oracle configuration that temporarily distorted pool pricing, has continued to weigh on market sentiment. Curve Finance confirmed its core protocol contracts were unaffected, but the incident left a residual risk premium in CRV pricing that has not yet fully cleared.

Key Levels: $0.2071 Holds First, $0.20 Below, $0.2495 Above

The 4H Supertrend at $0.2071 is the immediate support. A four-hour close below that level exposes the $0.20 psychological level, which aligns with the projected daily channel lower boundary. A daily close below $0.20 would represent a significant breakdown, with $0.18, the token’s lowest level from August 2024 per TradingView data, as the next structural reference below. That $0.18 level is the bear case extended target and the point at which the current thesis would require reassessment.

On the upside, the $0.2224 level is the upper bound of the 4H descending wedge and the first resistance to clear. The daily Supertrend at $0.2495 is the key level that must be reclaimed to challenge the broader downtrend. A confirmed daily close above $0.2495 would be the first credible signal the descending channel is being genuinely challenged.

Derivatives Data Confirms Cautious Positioning

According to CoinGlass data, CRV futures open interest declined 11.47% to $74.45 million as of late March, while the OI-weighted funding rate of 0.0067% signals marginally net-long positioning despite the price slide. A market analyst noted in a March 30 analysis that the current phase reflects “accumulation, not decline,” but added that a confirmed bullish reversal would only materialise on a move back toward the $0.30 to $0.32 range. That remains a significant distance from current price, and the technical structure has not yet provided the confirmation that view requires.

If $0.2071 gives way on the 4H chart, a test of $0.20 looks probable. A close above $0.2495 on the daily would be the first real sign the descending channel structure is being challenged.

Bitcoin climbed above $70,200 on Monday for the first time since March 25, as a report that the US and Iran are negotiating a 45-day ceasefire sent risk assets sharply higher across global markets.

Summary

- Bitcoin surged more than 3.5% on April 6, peaking at $70,200 after Axios reported that the US, Iran, and regional mediators are actively discussing a 45-day ceasefire

- The move triggered $273 million in short liquidations across crypto markets within 24 hours, according to Coinglass

- Markets remain cautious, with Polymarket giving the ceasefire roughly 30% odds by April 30, and a White House official confirming Trump has not yet signed off on the proposal

Bitcoin (BTC) reclaimed $70,000 on Monday for the first time in nearly two weeks, rising more than 3.5% to a peak of $70,200 as Axios reported that the US, Iran, and a group of regional mediators are discussing terms for a potential 45-day ceasefire. The report, citing four US, Israeli, and regional sources, sent fresh capital flowing into risk assets on the first trading day after Easter.

Ethereum climbed as much as 5.1% alongside Bitcoin, while the total crypto market cap crossed back above $2.5 trillion. Major altcoins followed, with SOL, XRP, and DOGE all registering gains.

Pakistan is brokering what sources describe as the “Islamabad Accord,” a two-phase deal that would begin with a 45-day ceasefire and transition into negotiations for a permanent end to the conflict. The plan also envisions the reopening of the Strait of Hormuz, the key shipping lane that has remained closed since the war began six weeks ago.

A White House official confirmed the proposal is under active consideration but told reporters: “The President has not signed off on it. Operation Epic Fury continues.” Trump, who extended his strike deadline on Iran to Tuesday at 8 pm ET, told Axios he is “in deep negotiations” with Tehran, adding: “There is a good chance, but if they don’t make a deal, I am blowing up everything over there.”

Six Weeks of Conflict Have Kept Crypto Range-Bound

The US-Iran war has kept roughly 20% of global crude supply constrained behind the closed Strait of Hormuz, sustaining oil prices at elevated levels and dampening risk appetite since the conflict began. Bitcoin had already been weighed down by weeks of escalation headlines, with the asset trading within a $65,000 to $73,000 range even as ceasefire rumors produced repeated short-term spikes. Prior diplomatic attempts collapsed after Iran rejected earlier terms, keeping the strait closed and pressure on risk markets intact.

$273 Million in Shorts Cleared, Open Interest Signals Fresh Capital

Coinglass data shows $273 million in bearish crypto bets were liquidated within 24 hours of the ceasefire reports surfacing. Short positions made up the overwhelming majority of losses, reflecting how heavily traders had positioned for further downside heading into the holiday weekend.

Bitcoin’s notional open interest rose 7%, and Ethereum’s climbed 11%, both outpacing spot price gains. As crypto.news noted, rising open interest alongside positive funding rates suggests fresh capital entering the market rather than a pure short squeeze. Polymarket currently gives the ceasefire roughly 30% odds by April 30, up from 18% before the Islamabad Accord came to light.

Whether the deal clears Trump’s Tuesday deadline remains the critical variable. Any breakdown in talks risks an immediate reversal, with analysts flagging $65,000 to $66,000 as the key support zone to watch if ceasefire optimism fades.

Worldcoin price is grinding just above an all-time low, and the WLD token has failed to stage any meaningful recovery despite Nasdaq-listed Eightco disclosing a $326 million position on April 2. The descending channel structure on both the daily and four-hour charts remains firmly intact, pushing price closer to uncharted territory each session.

Summary

- Worldcoin price is at $0.2482 on April 6, just above the all-time low of $0.2455 set on March 28, as a descending channel on the daily chart holds price near historic lows.

- The daily Supertrend at $0.3097 and a deeply negative MACD at -0.0013 confirm the bearish trend, while Nansen data shows elevated exchange inflows adding near-term selling risk.

- A daily close below $0.2455 would confirm a new all-time low and expose the $0.20 support level, while reclaiming the Supertrend at $0.3097 is the minimum required to challenge the downtrend.

Worldcoin(WLD) price is trading at $0.2482 on April 6, down 7.98% over the prior 24 hours and pressing against an all-time low of $0.2455 set just nine days earlier on March 28. A descending channel that has contained the WLD token since late 2025 keeps price pinned near historic lows, with no confirmed technical reversal pattern present on either the daily or four-hour chart.

On the daily chart, WLD is trading within a defined descending channel, with the upper boundary sitting near $0.4052 and the lower trendline converging directly on price at current levels. The Supertrend sits at $0.3097, well above price, acting as a rolling resistance ceiling that has rejected every recovery attempt in recent weeks. The MACD line sits at -0.0013 against a signal of -0.0091, with the histogram deeply negative, confirming that downward momentum remains intact.

On the 4H chart, the Supertrend at $0.2641 holds above price as bearish resistance on every actionable timeframe. The 4H MACD shows the MACD line at 0.0003 crossing marginally above the signal at -0.0053, a tentative micro-stabilisation on the shorter timeframe that carries limited analytical weight while the daily structure remains this heavily one-sided.

Eightco Holdings, a Nasdaq-listed firm, disclosed on April 2 that it holds 277 million WLD tokens worth approximately $326 million, describing itself as “the largest public market participant in the Worldcoin ecosystem.” Despite the scale of that institutional position, WLD has produced no sustained upside response, reflecting the depth of selling pressure the market is still absorbing.

Key Levels: $0.245 ATL Breaks First, Then $0.20

The all-time low at $0.2455 is the critical immediate support. A daily close below that level would confirm a new historic low for WLD and open a path toward the $0.20 psychological level, which aligns with the projected lower boundary of the descending channel in the weeks ahead. The $0.20 level carries no prior support, as it would represent territory WLD has never closed at on a daily basis.

On the upside, reclaiming the Supertrend at $0.3097 is the minimum threshold for any credible recovery attempt. Above that, the upper channel boundary near $0.4052 is the next meaningful resistance zone. The bullish thesis is fully invalidated on a daily close below $0.20.

Exchange Inflows Signal Continued Selling Pressure

Data from Nansen shows the total balance of WLD tokens held across centralised exchanges rose over 25% to approximately $742 million in the week ending March 27, as the Worldcoin team moved around $26 million in WLD to exchange wallets. Elevated exchange balances signal increased near-term selling risk, as tokens held on exchanges are more readily available for disposal. Until that dynamic reverses, the supply overhang on WLD is unlikely to ease meaningfully.

A confirmed break below $0.2455 would represent a structural deterioration, with $0.20 as the logical next downside target if the all-time low floor fails to hold.

Bitcoin dropped roughly 2% to $68,500 in early Tuesday trading. The move fully erased Monday’s brief climb above $70,000. Geopolitical pressure, not market fundamentals, is driving the sell-off.

Monday’s short-squeeze rally was always structurally weak — and the market proved it fast.

Tuesday Deadline Triggers Risk-Off Across Markets

Trump’s deadline for Iran to reach a deal — or face expanded military strikes — moved from threat to imminent reality overnight. Tehran rejected a ceasefire proposal relayed through Pakistan, demanding sanctions relief, reconstruction commitments, and a permanent end to hostilities. Markets responded with broad caution across risk assets.

Oil surged past $113 a barrel as Trump threatened to target Iranian bridges and power plants by Tuesday night. Gold climbed to $4,654 an ounce as investors rotated toward traditional safe havens. Crypto markets partially recovered, with Bitcoin edging back toward $68,957 and Ether recovering to $2,115.

BNB slipped 0.6% to $600, and XRP fell a similar margin to $1.32 over 24 hours. The global crypto market cap held near $2.44 trillion, down just 0.2%. Monday’s rally, built on over $145 million in forced short liquidations per CoinGlass data, remains the dominant price driver — fresh capital has yet to follow.

Bitcoin Stuck in a Familiar Trap

Bitcoin has now failed at the $70,000 level repeatedly since late February, when Iran-related conflict first began weighing on risk appetite. Every rally toward that level attracts profit-taking and runs into thin liquidity. The pattern has become predictable.

The Strait of Hormuz now sits at the center of ceasefire negotiations. Any prolonged disruption to energy supply routes would significantly darken the global macro outlook. Crypto, still moving in close lockstep with broader risk assets, would absorb that pressure directly.

The post Bitcoin Slides Below $69K as Iran Strike Deadline Looms appeared first on BeInCrypto.

ETHGlobal Cannes 2026’s 10 finalists push AI agents, privacy infrastructure and on-chain prediction markets through projects like ENShell, DIVE, Corpus and VEIL VPN.

Summary

- ETHGlobal has named 10 Cannes 2026 finalists pushing AI agents, privacy infrastructure and on-chain prediction markets across ENShell, DIVE, maki, Défi, ALMA, npmguard, VEIL VPN, PaintGlobal, EVM PORST and Corpus.

- Projects like ENShell, DIVE and Corpus show how autonomous agents can safely sign, verify and trade on-chain, while VEIL VPN builds a verifiable “no‑logs” network at the Internet’s encrypted edge.

- The finalists sit inside a maturing Ethereum hackathon circuit, where events like ETHGlobal routinely put up prize pools in the tens of thousands of dollars and attract developers chasing both funding and distribution.

ETHGlobal used a simple “Drumroll please…” tweet to introduce what is arguably one of its most technically ambitious finalist slates yet, telling followers “Our ETHGlobal Cannes finalists are here! We’re excited to announce the top 10 projects of the weekend: ENShell, DIVE, maki, Défi, ALMA, npmguard, VEIL VPN, PaintGlobal, EVM PORST, Corpus” and directing users to “Learn more about the winners ↓” via its showcase portal.

The 10‑project lineup spans AI‑first protocol design, verifiable networking and interface‑level tooling for developers and prediction markets. According to ETHGlobal, its hackathons are designed to “teach new skills, strengthen developer communities, and push the limits of new technologies,” and Cannes 2026 is framed as a proving ground for what happens when on‑chain agents and infrastructure are treated as first‑class design constraints rather than bolt‑ons.

The official ETHGlobal finalist thread quickly followed with per‑project one‑liners. ENShell, tagged as “ETHGlobal Cannes 2026 Finalist | 🐚 ENShell” and developed by @CodeQuillClaim, is described as a tool that “Prevents AI agents from executing malicious transactions caused by prompt injection attacks,” pointing to an architecture where agent transaction flows are wrapped inside a hardened ENS‑aware shell that checks proposed actions against policy before a signature ever hits a wallet . DIVE, credited to @derek2403, @avoisavo, @cedricctf11a and @ilovetofupeach, is introduced as an “AI swarm engine verifying real-world truth for prediction markets and autonomous on-chain settlement,” implying a multi‑agent oracle layer that cross‑checks external data before committing settlements to smart contracts . VEIL VPN, meanwhile, positions itself as a protocol at the network edge: ETHGlobal calls it “Verifiable Encrypted Internet Layer, is the pay as you go VPN protocol that proves no logs are kept,” suggesting a design where proofs about server behavior are surfaced alongside encrypted traffic to make “no‑logs” claims cryptographically auditable rather than purely marketing language .

Cannes’ emphasis on agents is not accidental. ETHGlobal’s own ENS prize track for the event describes the Ethereum Name Service as “the identity layer for the new internet” that “turns wallet addresses into human-readable names like yourname.eth — a portable, onchain profile that works across every app, chain, and wallet,” and explicitly calls out that “as AI agents become first-class onchain actors, ENS is how you give them a name, a reputation, and a place to be found”. Within this frame, ENShell looks less like a standalone tool and more like a reference implementation for ENS‑based agent controls: by sitting between LLM prompts and transaction submission, it can apply machine‑readable policies tied to ENS identities and revoke or quarantine flows that look like prompt‑injection‑driven privilege escalation. The ENS prize track itself offers targeted rewards such as “Best ENS Integration for AI Agents” with $4,000 in total awards, including $2,500 for first place and $1,500 for second, and a separate “Most Creative Use of ENS” pool with a further $6,000, underlining how prize money is being explicitly steered toward agent‑centric integrations.

Corpus takes that agent mentality to products rather than identities. In ETHGlobal’s words, Corpus lets teams “Turn any product into an autonomous AI agent corp that runs GTM, trades, and earns for you,” suggesting a multi‑agent architecture where go‑to‑market operations, treasury management and trading strategies can be expressed as separate, composable bots with shared access to protocol‑level wallets and on‑chain reputational footprints. This framing echoes a broader shift across Ethereum towards products that ship with built‑in “agent corps” for growth, liquidity management and user support, anticipating a future where a meaningful share of on‑chain volume is initiated not by humans clicking buttons, but by semi‑autonomous services negotiating with one another on behalf of users and DAOs.

If ENShell and Corpus are about giving agents guardrails and jobs, VEIL VPN and DIVE are about ensuring the world they see is actually real. DIVE’s description as an “AI swarm engine verifying real-world truth for prediction markets and autonomous on-chain settlement” implies a layered stack where multiple models interrogate the same real‑world event, resolve disagreements across agents, and only then write a consensus outcome into a settlement contract that can unlock funds, close markets or trigger hedging logic. In practice, this could allow prediction markets to move away from single‑oracle designs towards resilient swarms, a direction that mirrors both how traditional financial data providers run redundant feeds and how some DeFi protocols now weight multiple oracle sources to guard against manipulation.

VEIL VPN’s engineering challenge is different but equally fundamental. By positioning itself as a “pay as you go VPN protocol that proves no logs are kept,” the team is implicitly acknowledging widespread skepticism around commercial VPN claims and betting that cryptographic proofs and on‑chain settlement can restore trust at the packet level. A plausible design here involves combining anonymous credentials, encrypted tunnels and zero‑knowledge attestations about server‑side logging behavior, with users paying per‑session from non‑custodial wallets and being able to audit, or even slash, relays that violate agreed‑upon privacy constraints. ETHGlobal’s decision to push such a network‑layer experiment into its finalist pool speaks to a belief that the next generation of crypto infrastructure will not just live in DeFi front‑ends or Layer‑2 rollups, but deep in the plumbing of how traffic moves, is priced, and is verified.

Beyond individual architectures, the Cannes finalists underscore how hackathons have become capital‑efficient R&D funnels for Ethereum, with events like ETHGlobal routinely offering $5,000–$10,000 top prizes and aggregate prize pools reaching $20,000 or more once partner bounties are included. ETHGlobal notes that teams can “select up to 3 Partner Prizes” per submission and that prizes are awarded across tracks ranging from “Hooks, Hooks, and Hooks — $10,000” to Filecoin‑backed data and AI‑tool categories, creating a funding environment where early‑stage teams can assemble meaningful non‑dilutive capital and distribution simply by shipping something useful over a weekend. For ENShell, DIVE, VEIL VPN and Corpus, the Cannes finalist slot is both a badge of engineering credibility and a launchpad into deeper ecosystems around ENS, prediction markets, privacy infrastructure and agent‑native protocol design.

AAVE price posted one of its sharpest single-session drops in months on April 6, briefly crashing through $84 before a partial recovery took hold. The chart damage is clear: $100 has gone from support to resistance in a single session, and the technical setup across both the daily and four-hour timeframes remains decisively bearish.

Summary

- AAVE price fell to an intraday low of $83.92 on April 6 before recovering to $94.66, confirming the $100 psychological support as resistance on the daily chart.

- The daily Supertrend at $107.82 and a deeply negative MACD reinforce the bearish bias, while the 4H Supertrend at $92.29 is currently acting as near-term floor.

- A failure to reclaim $100 keeps the $83 intraday low and the $80 Fibonacci zone in sight, while a daily close above $107.82 would be the first signal of a structural shift.

AAVE (Aave) price crashed to $83.92 on April 6, sliding more than 11% from the prior session’s close of $94.15 before recovering to $94.66, as DeFi sector selling and broader macro risk-off sentiment pressured the Aave lending protocol’s native token. The drop confirmed a decisive break below the $100 psychological support, a level the daily chart now labels as resistance following months of acting as a structural floor.

On the daily chart, the Supertrend indicator sits at $107.82, well above price and capping any near-term recovery attempt. The MACD histogram remains negative across the daily timeframe, with the signal line still below zero, confirming that selling momentum has not yet reversed. Today’s candle printed a long lower wick from $83.92, reflecting demand at intraday lows, but the $94.66 close falls well short of what is needed to challenge the $100 threshold.

BGD Labs, a core technical contributor to the Aave protocol, formally concluded its engagement on April 1 after citing governance tensions. Aave founder Stani Kulechov had previously noted on X that the protocol’s risk infrastructure “has historically processed over 1,200 payloads and 3,000 parameters without issues,” but BGD Labs’ exit has introduced fresh uncertainty around development continuity heading into the V4 launch cycle.

On the 4H chart, the Supertrend at $92.29 is acting as dynamic support. The 4H MACD histogram is near flat, reflecting a pause in downside momentum rather than a confirmed reversal.

Key Levels: $80 Zone in View if $92 Fails

The 4H Supertrend at $92.29 is the immediate support to monitor. A daily close below that level reopens the $83.92 intraday low as the next test. Below that, the $80 round number marks the next significant support, reinforced by the 0.786 Fibonacci retracement of AAVE’s 2024 to 2025 rally, which falls in the $80 to $85 zone. That is the bear case invalidation level for any medium-term recovery thesis.

On the upside, $100 is the primary resistance. A confirmed daily close above the Supertrend at $107.82 is the minimum required to shift the short-term bias toward neutral. A sustained recovery above $100 with volume confirmation opens the path toward $112, as indicated by the potential ascending structure visible on the 4H chart.

On-Chain Context and Institutional Signals

Grayscale Investments has filed to convert its Aave Trust into an ETF on NYSE Arca, a potential longer-term demand catalyst, though approval timelines provide no near-term price support. According to CoinGlass data, AAVE futures open interest has declined alongside price in recent sessions, consistent with long-side deleveraging rather than aggressive fresh short building, which reduces the probability of a sharp short-covering bounce.

If $92.29 gives way on the 4H chart, a revisit of the $83.92 intraday low looks probable, with $80 as the last significant structural support before territory AAVE has not traded in years.

Polymarket is overhauling its exchange infrastructure in the coming weeks, introducing a new collateral token and an upgraded trading engine that give the platform tighter control over settlement and risk as it moves toward closer alignment with US regulatory expectations.

In a Monday announcement, Polymarket said it will deploy new exchange contracts—Version 2—designed to simplify how orders are structured and matched. The upgrade aims to boost trading efficiency and make it easier for developers to connect apps and trading bots to the platform.

The upgrade also expands on-chain compatibility by adding support for EIP-1271, the Ethereum standard that allows smart contract wallets, including multisigs and automated trading systems, to sign transactions, broadening support beyond traditional externally owned wallets.

A central feature is the introduction of Polymarket USD, a new collateral token that will replace USDC.e, Polymarket’s bridged version of USDC. The new token is fully backed 1:1 by USDC, giving Polymarket greater direct control over its settlement layer and reducing reliance on bridged assets.

For most users, the transition will be automatic through the platform’s interface, requiring only a one-time approval. The rollout is expected to unfold over the coming weeks, though Polymarket did not provide a precise date.

Key regulatory backdrop and market implications

The upgrade comes as Polymarket continues to adapt to evolving US regulatory expectations, including efforts to curb manipulation and insider-trading risks as it seeks to strengthen market integrity and align more closely with US standards.

In November, Polymarket won approval from the Commodity Futures Trading Commission to operate an intermediated trading platform in the United States, clearing the way for its return after previously exiting the market. Following that approval, Polymarket said it plans to onboard brokers and customers directly and facilitate trading through regulated US venues.

Interest in prediction markets has continued to grow, with users increasingly trading real-world outcomes tied to politics, markets, and policy. Industry data have shown Polymarket’s fee revenue rising in recent weeks after a pricing overhaul, underscoring the demand for these platforms.

Market data provider DeFiLlama tracks Polymarket’s revenue indicators and has highlighted the platform’s uptick as it expands fee-based income alongside its technological upgrade.

Beyond the user-facing changes, the upgrade is designed to strengthen the platform’s connective tissue for developers and automated traders, while giving Polymarket enhanced control over its settlement pipeline and a more cohesive collateral framework to manage risk.

What this means for users and developers

For everyday users, the transition should be largely seamless: the one-time approval triggers the automatic switch to the new system, and existing accounts will be supported by the updated interface. Traders and developers can anticipate easier integration with external apps and bots thanks to the simplified order structure and standardized settlement flow.

Polymarket’s ongoing push toward regulatory-aligned operation could attract more traditional market participants, brokers, and liquidity providers, potentially broadening the range of real-world events offered for trade.

Looking ahead, observers will watch how quickly the new infrastructure gains traction among users and whether regulatory clarity translates into faster onboarding of US participants via regulated venues.

As Polymarket advances its technical overhaul, the timing of regulatory milestones, the pace of onboarding, and the robustness of the new collateral approach will be key determinants of the platform’s next phase of growth.

Mike Krzyzewski says Michael Malone faces learning curve at UNC like Bill Belichick

Modular Mechanical Keyboard Transformed Into A Compact Workstation

EastEnders spoilers: Suki takes action as she discovers Ravi’s worsening state | Soaps

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Sua vida financeira vai melhorar? #tarot #tarothoje #tarotgratis #tarotamor

ANDRY HAKIM SUDAH CAPAI FINANCIAL FREEDOM??!! #andryhakim #stockwise #saham

Vrishabh rashi walon ke liye April ka financial update.#MoneyPrediction #ZodiacTips

-

NewsBeat4 days ago

NewsBeat4 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business4 days ago

Business4 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Spanx – Corporette.com

-

Crypto World5 days ago

Crypto World5 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Business1 day ago

Business1 day agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Crypto World7 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Sports2 days ago

Sports2 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business5 days ago

Business5 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Tech7 days ago

Tech7 days agoEE TV is using AI to help you find something to watch

-

Sports6 days ago

Sports6 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech7 days ago

Daily Deal: StackSkills Premium Annual Pass

-

Tech7 days ago

Tech7 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Tech7 days ago

Tech7 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Crypto World7 days ago

Valinor raises $25m to put private credit on-chain

-

Tech7 days ago

Tech7 days agoWhat Are The Biggest Limitations Of Supercomputers?

-

Crypto World6 days ago

Crypto World6 days agoBitcoin enters the public bond market as Moody’s gives a first-of-its-kind crypto deal a rating

-

Politics7 days ago

Politics7 days agoTransform Your Space with Stunning Small Works

-

Politics6 days ago

Politics6 days agoStarmer’s centre has collapsed, and the left was right all along

-

Crypto World6 days ago

Bitcoin stalls below key resistance as technical signals skew bearish

-

Business2 days ago

No Jackpot Winner, Prize to Climb to $231 Million

You must be logged in to post a comment Login