Crypto World

Why HYPE is different: inside Hyperliquid’s buyback

Most crypto tokens have “buyback” mechanisms that are either nominal, sporadic, or theoretical. HYPE has something genuinely different.

Summary

- Hyperliquid’s Assistance Fund uses 97% of protocol trading fees to buy HYPE tokens directly from the open market through an automated on-chain system.

- The fund has spent more than $1.3 billion on HYPE buybacks, with the mechanism running at an annualized rate estimated near 7% of the token’s market cap.

- Analysts tracking HYPE’s tokenomics say the continuous buyback structure has created one of the most aggressive revenue-driven value accrual models in the crypto market.

The Assistance Fund directs 97% of Hyperliquid’s protocol fees into continuous, automated market purchases of (HYPE), removing tokens from circulation every day. By May 2026, the Fund had spent over $1.3 billion buying back HYPE, holding roughly 28.5 million tokens worth $1.5 billion at peak prices.

At an annualized rate of roughly 7% of market cap, HYPE’s buyback intensity is four to five times Ethereum’s and BNB’s. That math is the structural reason behind the rally that most price commentary cannot explain. This is how the mechanism actually works, why it scales differently from every other major crypto token, and what would have to break for the model to fail.

The mechanism in plain terms

The Hyperliquid Assistance Fund is a part of the protocol that makes HYPE’s tokenomics genuinely different from every other large-cap cryptocurrency, and almost no coverage explains it properly.

In plain terms: every time someone trades on Hyperliquid, they pay a fee. That fee gets aggregated into a protocol-controlled pool called the Assistance Fund. The Fund then uses 97% of those accumulated fees to buy HYPE tokens directly from the open market. The purchases run continuously, automated by on-chain logic, with no manual intervention from the team. The HYPE bought back is held by the Fund itself, removing those tokens from the active circulating supply.

The numbers are not theoretical. By October 2025, the Assistance Fund’s total purchases had passed $1.3 billion. Daily buybacks averaged around $1 million, with single-day peaks reaching $3.97 million. By Q3 2025, the Fund held nearly 29.8 million HYPE tokens, valued at over $1.5 billion. By March 2026, the Fund had accumulated roughly 28.5 million HYPE through systematic open-market purchases.

Hyperliquid accounted for 46% of all token buyback activity across the crypto industry in 2025, with monthly buybacks averaging $65.5 million.

That last statistic is worth pausing on. Almost half of all crypto buyback activity in 2025 came from a single protocol. The scale is genuinely different from anything else in the industry.

The mechanism is automated and transparent. Validators publish the rules. The smart contracts execute the purchases. Every buyback transaction is visible on chain. There is no “we will buy back tokens when we feel like it” element. The 97% allocation is encoded in the protocol’s economic design, and the Fund operates as a continuous market participant, always bidding, always buying.

A December 2025 governance vote, passed by 85% of validators, raised the allocation to 99% for certain fee categories and committed to permanent token burns on a portion of the Fund’s holdings.

The vote was significant for two reasons. First, it took the buyback model from “policy that could change” to “governance-enforced commitment.” Second, it added a deflationary component: tokens bought back and then burned are permanently removed from supply, which is structurally different from tokens bought back and held in a treasury that could theoretically be resold.

This is the engine. The rest of the piece explains why it matters more than most readers realize.

Why this is not just another buyback program

Crypto has a long history of token buyback announcements that turn out to be less than they appear. Some are one-time events. Some are sporadic and tied to discretionary team decisions. Some are funded by token treasury sales rather than real revenue, which is roughly equivalent to printing money to buy back money. The market has, reasonably, learned to discount buyback announcements as marketing rather than substance.

HYPE is genuinely different on three dimensions.

First, the source of the funding is real. The Assistance Fund’s purchases are funded entirely by trading fees from actual transactions. Hyperliquid’s protocol revenue runs at roughly $1.3 billion in annualized fees as of mid-2026, with the platform regularly beating Ethereum and Solana on weekly blockchain fee generation. The buybacks are not subsidized by token issuance, treasury depletion, or external capital.

They come from users actually using the protocol and paying actual fees. If trading volume goes up, buybacks go up. If trading volume goes down, buybacks go down. The mechanism is mechanically tied to real economic activity, not to founder discretion or marketing cycles.

Second, the share of revenue going to buybacks is exceptional. Most crypto tokens with buyback or burn mechanisms route a small percentage of revenue toward token economics. BNB burns roughly 20% of its quarterly profits. Ethereum burns a variable share of gas fees via EIP-1559, with the rate depending on network congestion. Solana directs roughly 50% of priority fees to burns. HYPE’s 97% allocation is, by a wide margin, the most aggressive fee-to-token-economics ratio of any major crypto asset. The protocol effectively treats trading fees as token holder revenue rather than operating budget.

Third, the execution is fully automated and transparent. The Assistance Fund runs on chain. Every purchase is visible. Every transaction is verifiable. There is no off-chain accounting, no discretionary timing, no “we’ll announce the burn next quarter” framing. The mechanism runs like an algorithmic market participant always bidding for HYPE, funded by the trading activity of the network it runs on.

To use a comparison that makes the difference concrete: when Binance burns BNB, it makes a quarterly announcement, calculates the burn amount based on metrics it controls, and executes a single transaction. When Hyperliquid buys back HYPE, it happens every day, in continuous small purchases, funded by every trade that ran since the last buyback. The Binance model gives BNB holders four discrete moments of supply reduction per year. The Hyperliquid model gives HYPE holders a constant supply-reduction force that scales with network usage.

The implications of that difference are substantial, and they show up in the math.

The math compared to other major tokens

The clearest way to see why HYPE is structurally different is to look at the buyback or burn rate as a%age of market capitalization, annualized. This normalizes for the fact that bigger tokens can buy back more in absolute terms while still doing less relative to their size.

Ethereum burns approximately 1.5% of its market cap annually through EIP-1559, depending on network usage. The burn rate scales with congestion, so it varies, but the long-term average sits in that range.

BNB burns approximately 1.2% of its market cap annually through its quarterly burn program. The rate is moderately stable because it is tied to Binance’s overall profitability, which scales more slowly than network usage.

Solana burns roughly 0.5% of its market cap annually through priority fee burns. The rate is lower than Ethereum’s because the share of fees burned is smaller and the protocol relies more heavily on issuance for validator rewards.

HYPE’s buyback rate is approximately 7% of market cap annually at current revenue levels. This is four to five times Ethereum’s rate, six times BNB’s rate, and fourteen times Solana’s rate. The disparity is not marginal. It is structurally different.

What this means in practice is straightforward. For every $100 of HYPE you hold, the Assistance Fund is, on average, buying back roughly $7 worth of HYPE from the market each year on your behalf. That buy pressure is funded by protocol revenue, scales with trading volume, and runs regardless of HYPE’s price or your individual actions. It is the closest thing to a dividend that exists in major crypto, except it shows up as supply reduction and accumulated treasury holdings rather than as cash distributions.

The 7% figure understates the structural intensity in another way. The buyback rate is computed against current market cap. As Hyperliquid’s trading volume grows, the absolute size of the buybacks grows. As the buybacks grow against a finite supply, the supply shrinks. As the supply shrinks against constant or rising demand, the price rises. As the price rises, the same absolute buyback in dollar terms removes fewer tokens, which means the supply pressure stabilizes at higher prices rather than running away to infinity. The math is self-balancing, but the balance point is meaningfully higher than what a pure fundamental valuation would suggest.

This is what Arthur Hayes meant when he called HYPE “fundamentally de-risked” in his Valhalla thesis from earlier in 2026. He was not saying HYPE has no risk. He was saying the buyback mechanism creates a structural floor that scales with adoption, which is a feature most tokens do not have.

Why this matters for the token unlock schedule

One of the most common bear arguments against HYPE is the token unlock schedule. The argument goes like this: HYPE has a maximum supply of approximately 1 billion tokens. The circulating supply is around 254 million as of late May 2026. That means roughly 75% of the total supply has not yet entered circulation. As tokens vest from team, investor, and reward allocations, they will enter the market over the coming years and create persistent selling pressure that the protocol cannot offset.

The argument is not wrong, but it is incomplete. The honest analysis requires comparing the inflation rate from unlocks against the deflation rate from buybacks.

The token unlock schedule for HYPE is back-loaded. The largest tranches of vesting do not begin until 2027 and beyond, with team and investor allocations subject to multi-year cliffs and gradual release. This is different from many recent crypto tokens, where significant unlocks hit in the first 12 to 18 months of trading and produce structural selling pressure during the period when the token is most fragile.

Between now and the start of major team and investor unlocks, the Assistance Fund keeps buying. At the current rate of roughly $65.5 million per month in buybacks, the Fund accumulates approximately 1.3 million HYPE per month at current prices, or roughly 15 to 16 million HYPE per year. If that pace holds unchanged through the next eighteen months, the Fund will have absorbed an additional 25 million HYPE from the market by the time major unlocks begin.

This does not eliminate the unlock pressure. It does shift the balance. The unlocks will create selling pressure when they arrive. The buybacks have been creating buying pressure all along. The question is which force is larger at any given moment, and the answer depends on how Hyperliquid’s trading volume scales between now and then.

If trading volume keeps growing, the Assistance Fund’s buying pressure grows proportionally, and may offset more of the unlock supply than skeptics expect. If trading volume stagnates, the unlock pressure dominates. The protocol’s success or failure as a derivatives venue is therefore the key variable. The tokenomics are not the bull case in isolation. They are the bull case conditional on continued protocol growth.

The HLP, the Assistance Fund, and the staking layer

There are three distinct components of Hyperliquid’s tokenomics that get conflated in most coverage, and they are worth distinguishing because each operates differently.

The Assistance Fund is the buyback engine described above. It collects 97% of trading fees and uses them to buy HYPE from the open market. The Fund holds the purchased HYPE in a protocol-controlled wallet. A portion of holdings is subject to governance-approved permanent burns.

HLP (Hyperliquidity Provider) is the protocol’s market-making vault. Users deposit USDC into HLP and earn returns from market-making activities, including spreads, funding payments, and liquidation profits. HLP serves as the counterparty to traders on the protocol. Its returns are inversely correlated with trader profitability, meaning HLP earns more when traders lose money and earns less when traders are profitable. HLP is separate from the Assistance Fund. It does not buy HYPE. It is a yield-generating product for USDC depositors.

HYPE staking lets HYPE holders stake their tokens to earn additional rewards. Stakers receive a portion of certain protocol fees not routed to the Assistance Fund, plus inflationary rewards from the network’s reserve allocation. Staking also confers governance rights, including voting on protocol changes and Assistance Fund parameters. As of mid-2026, HYPE staking is increasingly used by ETF issuers (Bitwise, in particular) to enhance fund returns and align with the protocol.

The interaction between these three components is what creates Hyperliquid’s full economic flywheel. Traders pay fees. Fees fund the Assistance Fund buybacks. HLP captures the counterparty side of trading activity. Stakers earn from fees not routed to the Assistance Fund. The flywheel is self-reinforcing: more trading produces more buybacks, which support price, which attracts more capital, which enables more trading.

The May 14 AQAv2 deal added a fourth component: reserve yield from USDC balances on the platform, redirected back to the protocol and ultimately to HYPE holders. This is structurally separate from the Assistance Fund but adds to the total economic value flowing to the token. The combined effect is that HYPE holders capture revenue from three distinct streams: trading fees (via buybacks), stablecoin reserves (via AQAv2), and ETF management fees (via the Bitwise allocation).

Three structural revenue streams are unusual in crypto. Most tokens have one source of value accrual, if any. HYPE has three. Each runs continuously. Each scales with adoption.

What could break the model

A fair piece on HYPE’s buyback mechanism has to name the conditions under which the model could fail or degrade. There are several worth taking seriously.

The first risk is trading volume decline. The buyback mechanism is mechanically tied to trading fees. If Hyperliquid’s trading volume drops significantly (because of competition, regulatory pressure, or a broader crypto market downturn), the Assistance Fund’s purchases drop proportionally. The mechanism does not have a floor. It scales with usage in both directions. A sustained 50% drop in trading volume would cut buyback intensity from 7% of market cap annually to roughly 3.5%. Still better than most tokens. Less compelling than the current rate.

The second risk is fee compression. Hyperliquid’s competitive position currently lets it charge meaningful fees for trading. If centralized exchanges (Binance, Coinbase, OKX) lower their fees aggressively, or if competing decentralized perpetual protocols (Aevo, dYdX, GMX) capture market share, Hyperliquid may need to reduce fees to stay competitive. Lower fees would mean lower buybacks at the same volume.

The third risk is governance changes. The 97% allocation is set by validator vote. A future governance vote could lower the allocation, redirect fees to other purposes, or alter the Fund’s burn policy. The December 2025 vote that raised the allocation toward 99% was supportive, but the same governance system could reduce it. The protocol’s commitment to the buyback model is real but not constitutional. It is policy, not bedrock.

The fourth risk is technical or operational failure. The Assistance Fund runs on Hyperliquid’s Layer-1 blockchain. A serious failure of the chain, the validator set, or the smart contracts that automate the buyback would interrupt the mechanism. Hyperliquid has run cleanly so far, but the protocol is younger than Ethereum or Solana, and the next major operational issue is, by base rate, eventually coming.

The fifth risk is regulatory. Token buybacks funded by protocol fees occupy an ambiguous space in U.S. securities law. If a regulator chose to characterize the buyback mechanism as a security distribution to token holders, the legal pressure on Hyperliquid would be significant. The protocol’s defense (it is a permissionless decentralized exchange and the buybacks are automated by smart contracts) is similar to Uniswap’s defense and has held up so far, but the broader regulatory environment for DeFi tokenomics in the U.S. is still evolving.

None of these risks invalidates the model. They are the conditions under which it could weaken. The honest read is that HYPE’s buyback mechanism is the most aggressive and structurally interesting in major crypto, but its continued effectiveness depends on Hyperliquid’s trading volume holding up, governance keeping the policy intact, and regulators not taking adverse action. All three conditions can be met. None is guaranteed.

The comparison nobody runs

The most useful exercise for understanding HYPE’s tokenomics is one nobody in mainstream crypto coverage runs: comparing HYPE directly to a hypothetical equity with similar cash flow characteristics.

Consider Hyperliquid’s economics in equity terms. The protocol generates roughly $1.3 billion in annualized revenue (trading fees). 97% of that revenue is used to buy back the token, which is the equivalent of an equity issuer using 97% of its revenue to buy back its own stock from the open market.

For a public equity, this would be extraordinary. Apple, by comparison, returns roughly 25 to 30% of its revenue to shareholders through buybacks and dividends. Berkshire Hathaway returns close to 0% (Buffett famously prefers reinvestment). The typical S&P 500 company returns somewhere between 5 and 15%. A company that returned 97% of revenue to shareholders would be an outlier so extreme that analysts would assume either fraud or imminent operational collapse.

HYPE’s “operational expenditure” is largely covered by the network’s validator and infrastructure rewards, which come from inflationary token allocation rather than trading fees. This is what makes the 97% number sustainable in a way it would not be for a traditional company. The protocol’s growth investments, validator payments, and ecosystem development are funded by token issuance to specific allocations, while trading fees flow almost entirely to existing token holders via buybacks.

In equity terms, this is a structure where the company’s growth is funded by issuing new shares while existing shareholder value is supported by aggressive buybacks of existing shares. The combined effect is dilution for new participants and concentration for existing holders. Whether this is sustainable depends on whether the growth funded by issuance generates enough new value to offset the dilution.

So far, it has. Hyperliquid’s revenue has grown faster than its dilution, which means existing holders have benefited net-net from the structure. The question is whether this keeps going as the protocol matures and as the token unlock schedule accelerates.

The comparison to traditional equity is imperfect (crypto tokens are not equity, and the legal structures differ in important ways), but it is useful for understanding what HYPE’s tokenomics are actually doing economically. The token is, in effect, a high-payout-ratio claim on a fast-growing piece of financial infrastructure. The closest traditional analog might be a high-yield REIT that retains very little capital and distributes nearly everything to shareholders, except that HYPE distributes via buybacks rather than dividends, and the underlying business is decentralized derivatives trading rather than real estate.

That is what makes HYPE genuinely different. Most crypto tokens are either pure speculation (no underlying cash flow) or low-payout infrastructure plays (Ethereum, Bitcoin). HYPE is a high-payout, high-growth cash flow claim. It is not pretending to be something else. The tokenomics are real, the cash flow is real, and the math is unusual enough that most crypto coverage simply does not have a framework for it.

What this means going forward

For HYPE holders specifically, the buyback mechanism implies a few things.

The structural buy pressure is real and continuous. As long as trading volume holds up, the Assistance Fund will keep absorbing HYPE from the market every day. This is supportive of price during normal market conditions and somewhat protective during downturns, because the buyback keeps running regardless of sentiment.

The unlock schedule is a real concern, but partially offset. The team and investor unlocks beginning in 2027 will add selling pressure. The buyback mechanism will offset some of that pressure, but how much depends on trading volume at that point. Holders watching the unlock schedule should also be watching the buyback run-rate.

The governance commitment to the model is the variable to monitor. The 97% allocation is not constitutional. A future governance vote could change it. So far, the validator base has consistently voted to keep or strengthen the buyback policy, but this is the lever that matters most for long-term HYPE holders.

For the broader crypto market, the implications are larger than they appear. Hyperliquid’s model is being studied by other DeFi protocols as a template. If similar fee-to-buyback mechanisms get adopted by other major venues, the era of “token economics as marketing” may finally be giving way to “token economics as cash flow.” That would be a significant shift in how crypto tokens are valued, and Hyperliquid would be the inflection point.

For analysts, the lesson is that the standard frameworks for valuing crypto tokens (multiples of TVL, multiples of trading volume, comparisons to similar tokens) do not capture what is happening with HYPE. The token is closer to a high-payout-ratio financial instrument than to a typical L1 governance token.

Valuing it requires modeling the cash flow, the buyback rate, and the unlock schedule, then comparing the result to traditional equity benchmarks. Most analysts have not done this work, which is part of why coverage of HYPE is still structurally underdeveloped.

The bottom line

HYPE’s buyback mechanism is not a marketing gimmick. It is not a sporadic burn program. It is not a discretionary commitment that can be reversed when convenient.

It is a continuously running, on-chain, automated mechanism that takes 97% of Hyperliquid’s protocol revenue and converts it into open-market purchases of HYPE. The Assistance Fund has accumulated $1.3 billion in HYPE since launch. It buys roughly $1 million worth of HYPE per day on average. It scales with trading volume. It is governance-enforced. It produces an annualized buyback rate of approximately 7% of market cap, four to five times Ethereum’s burn rate and six times BNB’s.

That is the structural reason behind the rally that most price commentary cannot explain. The protocol generates real revenue. The revenue funds real buybacks. The buybacks support the token. The token’s value reflects the cash flow.

This is unusual in crypto. Most tokens have value accrual mechanisms that are theoretical, sporadic, or marketing-driven. HYPE has one that operates continuously, scales with adoption, and converts protocol success directly into token holder value.

Whether this justifies HYPE at $58 (its level as of late May 2026, after retracing from the $62.24 all-time high) is a separate question. The argument for “yes” is the cash flow generation, the back-loaded unlock schedule, and the multiple structural revenue streams (buybacks, AQAv2 reserve yield, ETF allocation). The argument for “no” is the fully diluted valuation against eventual unlock supply and the conditionality of the model on continued trading volume growth. Reasonable analysts disagree on the valuation, and many do.

What is not reasonable is to evaluate HYPE without understanding the buyback mechanism. The price chart shows what happened. The Assistance Fund explains why.

This is the part most readers have not internalized yet. The crypto press has spent eighteen months treating HYPE as another speculative altcoin rally. The structural picture is that HYPE has the most aggressive and durable cash flow mechanism of any major crypto token, and the protocol that generates that cash flow is currently the dominant venue for on-chain derivatives.

That is not a meme. That is not speculation. That is real economics, encoded in smart contracts, running every day.

The buyback mechanism is the part that most people do not understand. Once you understand it, everything else about HYPE makes more sense.

This article is for informational purposes and does not constitute financial or investment advice. Cryptocurrency markets and protocol dynamics evolve quickly; the figures and milestones described reflect reporting available as of late May 2026. Always do your own research.

Growing fast, but still nascent: S&P lays out the promise and pitfalls of on‑chain vaults

S&P Global Ratings released a primer this week examining the role of digital asset “vaults”—on‑chain pooled investment vehicles that issue share tokens and deploy capital according to a defined strategy. The report highlights rapid expansion in deposits and says vaults could migrate beyond crypto-native uses to handle tokenized real‑world assets (RWAs) and functions traditionally performed by funds and intermediaries. At the same time, S&P warns that leverage mechanics, uneven disclosure practices, technical failure modes and regulatory ambiguity could constrain their path to wider institutional adoption.

What vaults are and how they have grown

Vaults aggregate deposits and allocate them across strategies via smart contracts, or a hybrid of automated code and discretionary manager decisions. Investors receive tokenised shares that represent a proportional claim on the pooled assets and any returns. That structure makes vaults a different primitive from direct asset ownership: they can implement dynamic, multi‑asset strategies, reallocate automatically and integrate with other protocols.

Market metrics cited by S&P show the space has expanded sharply: total deposits in vaults rose to about US$131 billion as of April 2026, from roughly US$24 billion in April 2023. But the firm notes that approximately 94% of current activity is concentrated in crypto‑native strategies such as staking, crypto‑backed lending and yield aggregation.

Why vaults might matter to capital markets

S&P argues vaults could eventually support a wide range of financial functions traditionally carried out by private credit funds, money market vehicles, hedge funds and more. The combination of automation, composability and secondary‑market liquidity turns pooled on‑chain assets into reusable building blocks: vault shares can be traded, posted as collateral, or blended into composite strategies.

The report also points to a potential bridge to much larger markets. For example, tokens representing treasury or repo‑like instruments could be used as collateral on‑chain; because global repo turnover is many times the market capitalization of crypto assets, even modest uptake could materially increase vault activity.

Key risks S&P flags

Leverage and looping. Vault architectures and composability enable recursive reuse of collateral. Borrowed funds can be redeployed as collateral to generate additional exposure, a practice S&P calls “looping.” Looping can occur at the depositor level—similar to margin—or at the vault level, where curators’ actions raise leverage for all depositors. That amplifies returns in good times and can accelerate deleveraging and cascading liquidations during stress.

Technical failure modes. Reliance on smart contracts, external oracles and protocol integrations introduces risks not seen in traditional funds. Code bugs, oracle failures or integration errors can produce direct losses or disrupt settlement and rebalancing processes.

Disclosure and transparency gaps. While on‑chain transactions are visible, S&P notes that raw blockchain data is often hard to interpret and does not substitute for structured disclosures. Many vaults focus on headline yield figures and provide limited, non‑standardised information on mandate, allocation limits, leverage practices and governance. Where disclosures exist, mechanisms such as “time locks”—typically several days for concentration changes—are used to give depositors exit windows, but monitoring these changes can be resource intensive.

Regulatory ambiguity. Uncertainty over whether vault tokens constitute securities or other regulated instruments is a major constraint on institutional participation. Vault shares can represent tokenised ownership of RWAs or resemble investment contracts under legal tests used by regulators. Without clearer cross‑jurisdictional frameworks, many institutions remain cautious.

Market structure and consolidation

S&P observes early consolidation among vault curators and infrastructure providers. On one relatively mature platform, Morpho, two curators accounted for roughly 77% of deposits as of April 2026. The ratings firm expects further concentration as operators scale, risk and disclosure standards rise, and traditional finance entrants and established market makers expand their presence. Names mentioned as active or interested participants in the market include Apollo, Wintermute and Bitwise—signalling growing crossover between legacy asset managers, trading firms and crypto infrastructure players.

Implications for institutional adoption and next steps

The primer’s central contention is that vaults have technical and economic features that could make them useful building blocks for tokenised capital markets, but that a series of market‑level changes is likely required before large institutional flows arrive. Those include clearer regulatory guidance, more standardised disclosures and independent operational controls—custody, audited smart contracts, resilient oracles and third‑party risk engines. Without those, S&P warns, vaults risk remaining a predominantly crypto‑native toolkit rather than forming the plumbing for broader financial markets.

For market participants and policymakers, S&P’s analysis provides a roadmap of trade‑offs: vaults can improve capital efficiency and liquidity, but the same composability that delivers benefits also increases interconnectedness and systemic risk. How participants, platforms and regulators respond will determine whether vaults evolve into core market infrastructure or remain an increasingly sophisticated corner of the crypto ecosystem.

At the recent Senate Banking markup of the Digital Asset Market Clarity Act (CLARITY), Senator Angela Alsobrooks (D-MD) shared a story that should resonate with every parent in America. She spoke about her twenty-year-old daughter and her daughter’s generation – their intuitive interest in digital assets and their desire for a modern financial system that offers both opportunity and protection.

It underscored the growing urgency and gravity surrounding digital asset policy in Washington. “The digital revolution is upon us,” Senator Alsobrooks said. “It’s happening with us or without us. We have a responsibility to regulate it to create rules of the road.”

Her remarks reflected the growing recognition that the U.S. can no longer afford to approach digital asset policy reactively. This legislation is not just about the America of today; it is about tomorrow. We owe it to our children and the younger generation to get this policy right.

Chairman Tim Scott framed the debate through the lens of opportunity, faith and the American dream for working families. Senator Cynthia Lummis, one of Congress’s earliest bitcoin champions, emphasized the bipartisan work behind the legislation. Even senators who withheld support at this time, including Senator Lisa Blunt Rochester, spoke thoughtfully about how engaged her constituents are with this technology and emphasized the importance of legislation that ensures their protection.

The question now facing us is whether the U.S. will lead in shaping that future or will neglect that responsibility.

The 15-9 vote to advance Clarity to the Senate floor underscores three critical realities for the future of the American economy.

First, serious bipartisan policymaking regarding digital assets is not only possible but is already happening. The markup was a testament to the fact that credible policy and thoughtful engagement can still move Washington forward. Even senators who ultimately did not vote in favor of the bill, including Senator Mark Warner (D-VA), expressed their intention to continue working toward a constructive path forward.

The desire of leaders like Senators Scott, Lummis, Tillis, Alsobrooks, Gallego, Hagerty, Moreno and others to bridge the gap – including on the complex issue of stablecoin yield – shows that a bipartisan path is the only durable way forward.

Second, digital assets and the blockchain are here to stay. As articulated throughout the hearing by Senators on both sides of the aisle, the debate over the viability of digital assets is over. The only question is whether the U.S. will lead in shaping the future of digital finance or cede that leadership to others.

Nearly 68 million Americans, about one in five, already own digital assets. New Harris polling shows the number has increased by 12 million in the past year alone, putting American holders closer to one in four. They are teachers, construction workers, veterans, entrepreneurs and small business owners, with a third Gen Z and another third millennials. They use digital assets to send money to family members, make purchases and plan for their financial futures. Eighty-three percent of all American holders agree that stronger regulation is needed to protect consumers. Yet 88% of global crypto exchange activity occurs on foreign exchanges beyond U.S. supervision. Americans deserve the protections, clarity and oversight that only a federal framework can provide.

Finally, Congress must finish the job. The time is now. It is imperative that the full Senate act promptly.

The GENIUS Act established the payment layer through stablecoin legislation, but without Clarity to provide the market structure, trading platforms oversight and asset classification needed to support it, the U.S. risks leaving the job unfinished. As Treasury Secretary Scott Bessent has rightly noted, stablecoins without a broader market structure are a “foundation without walls.” If we fail to act, we risk sending the next generation of American innovation and the talent, investment and tech that comes with it, to foreign jurisdictions.

This important work is the industry’s responsibility as well. Comprehensive market structure will not arrive because we asked for it; it will arrive because we match the seriousness Congress has shown. The time is now to continue engaging substantively and constructively with concerns raised by members of Congress. Doing so is not the obstacle to the work; it is the work.

The markup proved that the momentum is with us. The resolve in that room showed that Washington recognizes the high stakes for American competitiveness and the future of digital finance. We have the mandate, bipartisan support, and the duty to ensure that the future of digital finance is unambiguously American.

America has long led the world because it has embraced innovation, markets and the rule of law. The window is open. The only question is whether we will close it on our terms.

A vote for Clarity is a vote for regulation – the rules this generation needs and the rules the next generation will inherit. Congress now has the chance to shape this technology rather than chase it. Let’s finish the job on the Senate floor.

Bitwise Asset Management’s physically backed spot HYPE ETF early volume data show that the product launch is not a soft one. Does this reframe HYPE as a genuine cycle winner, or is the Bitwise ETF premium already priced in?

Bitwise’s BHYP debuted on NYSE with a 0.34% sponsor fee, temporarily waived to 0% on the first $500M in AUM for the opening month. The firm manages approximately $11 billion in client assets. Within 48 hours of launch, the two US-listed HYPE ETFs recorded a 50% single-day volume surge on May 20 and $25.5M in net inflows, with $8.8M attributed to BHYP alone, already making it one of the largest altcoin ETF launches by early metrics.

Meanwhile, Hyperliquid’s derivatives volume hit $2.9 trillion in 2025, with over 400% year-on-year growth. Not only derivatives volume, the protocol has also captured 44% of weekly blockchain fee revenue last week alone, generating $11M versus Ethereum’s $3M.

Discover: The Best Crypto to Diversify Your Portfolio

Can HYPE Break $100 as Bitwise ETF Flows Accelerate?

HYPE is having its own rally in this market bloodbath. It’s just so bullish at the moment that every major resistance is being breached. Right now, HYPE is at its price discovery after a more than 50% jump in the past 2 weeks. It’s the hottest token now as it’s outperforming the market by a huge margin.

If BHYP and the 21Shares product sustain eight-figure monthly net inflows, HYPE could easily clear $70 decisively, targeting $80. Moderate flows after the fee-waiver window closes would likely bring HYPE to the sidelines around its $60 range.

For those shorting, the best case is to see ETF inflows reverse or stall below $5M weekly, which then breaks the price to under $55 support and reverts toward the $48 range, where structural buybacks provide a floor.

The Assistance Fund mechanic is the variable not to be missed. By March 2026, the Fund had accumulated 28.5 million HYPE through automated open-market purchases, spending over $1.3 billion cumulatively, bringing an annualized buyback rate of 7% of market cap, four to five times BNB’s equivalent rates.

Discover: The Best Token Presales

Bitcoin Hyper Targets HYPE’s Style Run

HYPE’s potential is real. The ETF wrapper expands access, but it also compresses the asymmetry available to early participants. Traders rotating capital toward high-performance infrastructure narratives are increasingly looking earlier in the stack for that kind of leverage.

Bitcoin Hyper ($HYPER), currently in active presale at $0.0136, positions itself at a different point on the risk curve. It is the first Bitcoin Layer 2 integrating the Solana Virtual Machine, delivering sub-second finality and low-cost smart contract execution while settling on Bitcoin’s security layer.

The project has raised more than $32.7 million to date, with a decentralized canonical bridge enabling native BTC transfers. Staking is live with a high 36% APY for early participants. The core thesis: Bitcoin holds $1.8 trillion in idle capital; programmability unlocks it.

Research Bitcoin Hyper here before the next price adjustment.

The post Bitwise HYPE ETF is The world Largest: Is Hyperliquid The Winner This Cycle? appeared first on Cryptonews.

A new report from Grayscale Research evaluates Hyperliquid, a decentralized finance platform that aims to bring high-throughput derivatives trading on-chain while preserving blockchain custody and transparency. The note focuses on the economics of the platform’s native HYPE token, the expanding product set that now includes spot and traditional-asset futures, and what the project could mean for the broader migration of trading activity from centralized exchanges to on-chain venues.

What Hyperliquid is building

Hyperliquid began by targeting perpetual futures, a lucrative and liquidity-intensive market dominated by centralized exchanges. The project has prioritized matching the performance expectations of professional traders – low latency, tight spreads and predictable execution – while operating onchain. To achieve that mix, Hyperliquid employs design choices intended to reduce friction between on-chain settlement and off-chain-like performance.

Beyond perpetuals, the platform has opened to permissionless third-party development and expanded into spot trading, futures on traditional assets, and outcome-style markets that resemble prediction markets. That modular approach is consistent with several DeFi projects that seek to attract external builders to increase product depth and diversify fee sources.

Grayscale’s focus: HYPE token economics

The Grayscale report centers on the HYPE token and how its economic design aligns with platform growth. Rather than presenting price forecasts, the research examines mechanisms commonly used to tie token value to platform activity, such as fee-sharing, protocol-owned liquidity, staking incentives and governance rights. Grayscale frames these mechanisms in the context of Hyperliquid’s product roadmap and potential revenue pools.

Token economics matter for platforms like Hyperliquid because they affect incentives for liquidity providers, market makers, and governance participants. Well‑calibrated token mechanics can improve fee capture and reduce reliance on external liquidity; poorly designed incentives can fragment liquidity or introduce speculative volatility that undermines trading utility.

Industry context: why on-chain derivatives matter

The examination of Hyperliquid comes amid growing interest in on-chain derivatives. Traders and institutions are increasingly evaluating whether blockchain-native venues can deliver the speed, capital efficiency and risk controls they expect from centralized counterparts. On-chain derivatives promise advantages including transparent order books, verifiable settlement and the elimination of custodial counterparty risk.

However, moving derivatives on-chain also raises operational challenges. Matching throughput with blockchain finality, limiting extractable value such as front-running, and ensuring deep, concentrated liquidity across products are nontrivial engineering and market-structure problems. Hyperliquid’s approach seeks to bridge those gaps, but the broader market will judge on repeatable execution quality and capital efficiency.

Market opportunity and competition

Grayscale’s report notes that the market opportunity for on-chain trading expands beyond crypto-native derivatives, especially if platforms can list futures on traditional assets or host outcome-based markets. Entrants that can combine institutional-grade execution with regulatory clarity could attract order flow migrating away from centralized counterparties.

Competition is a factor. Established centralized exchanges retain deep liquidity and product breadth, and other DeFi projects and hybrid venues are pursuing similar technical and commercial propositions. Success will depend on user experience, cost structures, regulatory positioning and the ability to aggregate liquidity across venues and chains.

Risks and regulatory considerations

The report and the market environment underscore several risks. Token investments remain speculative and subject to high volatility. For platforms offering derivatives tied to traditional assets or outcomes, regulatory scrutiny is a significant consideration as authorities assess how existing securities and commodities rules apply to on-chain products.

Operational risks also persist: smart contract vulnerabilities, liquidity fragmentation that raises slippage, and potential centralization vectors if execution infrastructure is controlled by a small set of actors. Protocol teams must balance performance optimizations with decentralization and robust governance to avoid concentrated risk.

Implications for institutional adoption

If platforms such as Hyperliquid can consistently deliver low-latency execution with verifiable on-chain settlement and clear token-aligned incentives, they may broaden the universe of institutional counterparties willing to route more activity on-chain. That could reshape liquidity dynamics and the economics of trading venues, but the transition will be gradual and contingent on regulatory clarity and operational track records.

Bottom line: Grayscale’s analysis highlights why token design and execution performance are core to any on-chain trading platform’s prospects. Hyperliquid’s combination of high-throughput derivatives and a permissionless developer model presents an intriguing use case for on-chain markets, but adoption will hinge on addressing liquidity, governance and compliance hurdles as trading evolves away from centralized incumbents.

Disclosure: Grayscale’s publication includes standard disclaimers noting that digital asset investments are speculative and may result in partial or total loss. This article summarizes the themes reported by Grayscale and does not constitute investment advice.

A hacker compromised StakeDAO's deployer private key on Wednesday, minting 5.4 trillion vsdCRV tokens on Arbitrum and swapping a portion for roughly $91,000 worth of ETH, an attack that rippled into Curve Finance's lending market and forced yield optimizer Beefy Finance to pause an affected vault…. Read the full story at The Defiant

AmericanFortress has launched a beta privacy infrastructure on Arbitrum, promising compliant, mixer-free transaction shielding for institutional and high-volume DeFi users.

Summary

- AmericanFortress debuts Send-to-Name privacy beta on Arbitrum for institutional DeFi

- System uses stealth addresses and FortressNames to hide counterparties while staying auditable

- Launch leans on Arbitrum’s roughly $20 billion DeFi footprint and growing institutional presence

AmericanFortress has rolled out its beta privacy infrastructure on Arbitrum, introducing a Send-to-Name system that uses human readable FortressNames and auto generated stealth addresses to conceal counterparties while preserving bilateral auditability on chain. The company frames the launch squarely at institutions and high frequency DeFi participants operating on Arbitrum, a Layer 2 network that has emerged as one of Ethereum’s largest venues for on chain derivatives and liquidity protocols. According to an Arbitrum Foundation transparency report, the network processed more than 2.1 billion cumulative transactions in 2025 with total value locked hovering near $20 billion and almost $10 billion in stablecoins, underlining the scale of the activity AmericanFortress is targeting.

“Financial infrastructure cannot scale institutionally if every transaction exposes counterparties, balances, and trading behavior in real time,” AmericanFortress CEO and CTO Michal Pospieszalski said, arguing that Arbitrum has become “one of the most important execution environments in crypto markets” and that the new implementation “delivers a privacy layer designed for serious financial activity without relying on mixers or compromising compliance requirements.” The system allows users to send assets to @names while the protocol generates one time stealth addresses between counterparties, shielding transaction flows from third party observers but keeping records available to those directly involved. On its website, the firm describes FortressNames as “the first human readable, send to name wallet and secure transaction infrastructure for digital assets,” designed to replace “vulnerable wallet strings with one time, stealth addresses” in a way that is “easy to use, fully compliant, and quantum proof”.

Privacy layer for an institutional Arbitrum

The launch comes as Arbitrum continues to solidify its position as the dominant Ethereum Layer 2 for DeFi, with external analyses citing total value locked around $20 billion and leadership in Layer 2 DeFi market share through late 2025. Arbitrum has become the base for major perpetual futures venues like GMX, which was already holding more than $450 million in TVL on Arbitrum V2 by early 2024, according to a Bitquery deep dive on the protocol. That same perpetuals venue has generated millions in fee revenue and, as later reporting from crypto.news showed, racked up over $2.74 million in fees on a single day in January 2023.

AmericanFortress is positioning its Universal Privacy Layer directly in this environment, pitching privacy as operational risk management rather than opacity. The beta is built to be compatible with existing blockchain systems, aiming to reduce transaction visibility that can feed frontrunning, copy trading and surveillance of automated strategies. The firm’s recent cryptographic research details a patent pending post quantum security architecture for hierarchical deterministic wallets, and management says the broader stack couples privacy preserving transaction rails, naming infrastructure and quantum resistant wallet security into “a comprehensive framework for digital asset custody and settlement.”

Campaign, compliance and liquidity

As part of the rollout, the company is launching a “Receive on Arbitrum Privately” campaign that encourages Arbitrum traders, liquidity providers and other DeFi users to test private receiving flows via the beta wallet. The first 500 eligible participants are set to receive a lifetime FortressName, a lifetime handle that locks in their Send to Name identity on the network. The campaign focuses on Arbitrum native communities already active across perpetual trading, liquidity provisioning and high frequency on chain market making, where address level visibility is particularly sensitive.

“Privacy and usability are increasingly important as more sophisticated financial activity moves on chain,” said Chase Allred, senior partnerships manager at Offchain, the service provider behind Arbitrum. Allred argued that infrastructure “that improves operational security while remaining compatible with compliant blockchain ecosystems represents an important area of development for the wider industry,” echoing themes that have surfaced across previous crypto.news coverage of institutional stablecoin and yield products deploying to Arbitrum.

AmericanFortress says the infrastructure is built with the next generation of automated finance in mind, including AI driven agents that will transact autonomously across DeFi rails. The firm contends that privacy preserving execution environments will be necessary as algorithmic capital allocation and machine driven trading expand across networks like Arbitrum, which has already been flagged by CoinGecko research as the largest Layer 2 solution by TVL share. For Arbitrum, the move slots into a broader evolution toward institutional DeFi, following integrations ranging from Chainlink oracles to yield bearing stablecoins and making the network’s privacy story a live competitive point against other Ethereum Layer 2s.

XRP (XRP) is down roughly 64% from its July 2025 multi-year high, but several onchain and technical indicators suggested the altcoin was due for a “strong price rebound.”

Key takeaways:

- XRP’s MVRV ratio fell to -47%, a level historically linked to strong market rebounds and accumulation.

- XRP Ledger transaction spikes suggest rising network activity and a possible macro price floor near $1.30-$1.50.

- XRP’s bullish falling wedge pattern projects a 134% price breakout to $3.10.

MVRV ratio: XRP is in an “extreme undervalued” zone

XRP’s market value realized value (MVRV) ratio, or the market cap divided by the realized cap, has dropped to levels that have historically aligned with accumulation zones and market bottoms.

The chart shows that XRP’s 30-day MVRV has now fallen to -47%, its lowest level since December 2020.

Related: XRP price risks 50% drop despite 9-day ETF inflow streak

This suggests that fear and frustration among investors have “reached rare extremes that have historically preceded strong rebounds,” onchain data provider Santiment said in a Tuesday post on X, adding:

“Historically, MVRV’s (average trading returns) will always average out to 0%, making this current level an extreme undervalued zone for $XRP. ”

XRP MVRV ratio. Source: Santiment

Deeply negative MVRV readings tend to appear when retail traders have largely given up, creating conditions where even small positive catalysts can trigger strong rallies.

While weak MVRV readings alone do not guarantee complete trend shifts, they “often signal that the majority of panic selling has already occurred and downside risk becomes more limited compared to potential upside,” Santiment added.

Meanwhile, XRP’s MVRV Z-score is hovering near zero, a level that historically aligns with accumulation zones and market bottoms, according to data from Glassnode.

XRP MVRV Z-score vs. price. Source: Glassnode

The last time XRP’s MVRV Z-score fell to similar levels in late 2024, it coincided with a macro market bottom at $0.30 before a rally of 500% to a multi-year high above $3. The gains were 215%, 94% and 1,050% in 2023, 2022 and 2021, respectively.

Analyst: XRP price “creating stable macro floor”

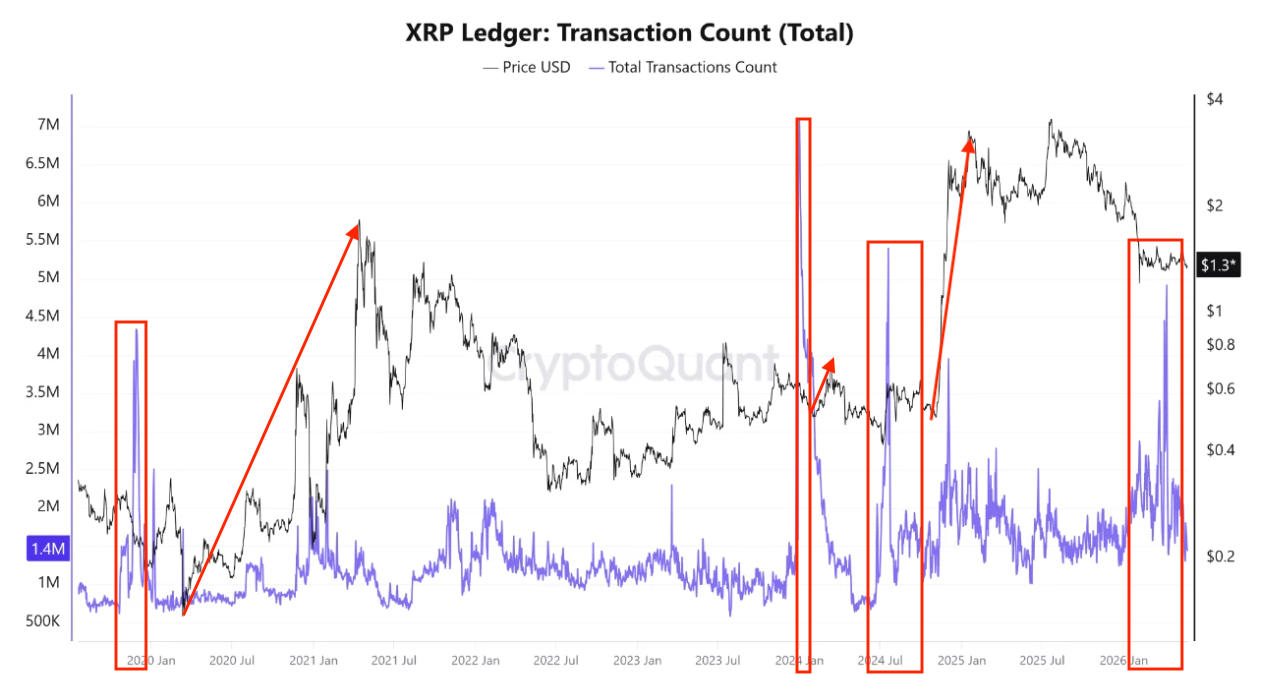

The XRP Ledger saw a massive transaction volume spike in April, suggesting that “deep ecosystem activity and accumulation are quietly building beneath the surface,” CryptoQuant analyst TopNotchYJ said in a Monday Quicktake note.

“Massive, vertical spikes in transaction counts serve as early network leading indicators, predating explosive price expansions,” the analyst added.

In November 2019, a surge in transaction count preceded the 2021 rally from $0.15 to $1.79 (nearly 1,200%). A similar dynamic played out in July 2024, with a gain of 600% to its eventual cycle peak of $3.17 in mid-2025 from $0.50.

XRP is currently consolidating within the crucial $1.30–$1.50 accumulation zone, and the massive network spikes suggest that the price is “creating a stable macro floor,” the analyst said, adding:

“If history repeats and this current consolidation solidifies into a launchpad, a conservative 5x macro projection positions XRP’s next major target area between $7.50 and $8.00.”

XRP Ledger transaction count. Source: CryptoQuant

As Cointelegraph reported, other key XRP Ledger metrics, such as record whale wallet and monthly transaction counts, suggest that the XRP/USD pair was primed for a strong upward move.

XRP falling wedge breakout targets $3.10

XRP price action is trading within a falling wedge pattern on the weekly chart, a structure typically associated with bullish reversals after a prolonged downtrend.

The price has been compressing between two descending trendlines since July 2025, with the lower boundary now being key support near the $1.30 psychological level

XRP/USD weekly chart. Source: Cointelegraph/TradingView

Meanwhile, the weekly relative strength index (RSI) has recovered from oversold conditions, suggesting that sellers are losing momentum. Historically, similar RSI conditions have preceded strong rebounds in XRP.

For example, XRP rallied as much as 660% between July and December 2024 following the RSI’s recovery from near oversold conditions. The gains were 95% in mid-2022.

A confirmed breakout above the wedge’s upper trend line at $1.50 could open the way for a run toward the measured target of the prevailing chart pattern at $3.1, about 134% above the current price.

As Cointelegraph reported, buyers will have to break and sustain the XRP price above the $1.40-$1.60 resistance zone on the daily chart to confirm a long-term trend shift.

Block’s Cash App has quietly begun rolling out its highly anticipated stablecoin payment feature, a source familiar with the matter told CoinDesk Wednesday. According to this individual, the feature is now active for 25% of Cash App’s nearly 60 million users, with plans to scale to 100% by the end of the week.

Block did not immediately respond to a CoinDesk request for comment.

The launch marks an unprecedented ideological shift for Block’s leadership and changes how the platform handles digital fiat currency.

The source familiar with the matter said that integrating alternative blockchain rails indicates Block CEO Jack Dorsey, a historically staunch bitcoin maximalist, has changed his mind and now sees tangible value in these non-BTC networks.

As of this week, the total market value of stablecoins has reached a record $322 billion, surpassing the foreign exchange reserves of 95 countries, including developed economies like the United Kingdom and Canada.

The integration of a stablecoin payment method was first announced on the Cash App website late last year, saying it would be available in 2026.

Dorsey explained his shift in stance in March. The bitcoin purist announced his firm was reluctantly giving into stablecoins. “I don’t like that we’re going to support stablecoins but our customers want to use them,” he said. “I don’t think it’s wise to go from one gatekeeper to another.”

For years, Dorsey framed Block’s crypto strategy around Bitcoin alone, backing mining hardware development and integrating the asset into products such as Cash App.

The newly-released integration treats stablecoins strictly as a payment method rather than investment infrastructure, according to a statement on the Cash App website.

Users can deposit Circle’s USDC stablecoins from external accounts to fund their fiat Cash App balance or withdraw funds as stablecoins to external accounts, utilizing the blockchain entirely as a modern transaction rail.

According to official product documentation, the feature supports USDC across four networks, including Solana, Ethereum, Polygon, and Arbitrum. Because these blockchain transactions are entirely irreversible, any funds sent to incorrect addresses or unsupported networks will be permanently lost.

To use the feature, which is currently unavailable in New York and on sponsored accounts, identity-verified users face strict caps: a $2,000 daily ($5,000 weekly) sending limit and a $10,000 weekly receiving limit.

Bitcoin has fallen more than 3% over the past 24 hours as traders reacted to renewed Middle East tensions, persistent ETF outflows, and a fresh rejection below a major technical resistance zone.

Summary

- Bitcoin price fell over 3% as Middle East tensions and ETF outflows pressured crypto markets.

- BTC broke below an ascending channel and now faces resistance near the $78,000-$80,000 range.

- Analysts say Bitcoin could still rally toward $83,000-$85,000 if the $74,000-$76,000 demand zone holds.

According to data from crypto.news, Bitcoin (BTC) price dropped from around $77,880 to nearly $75,220 overnight before recovering slightly toward $75,700 during early Asian trading hours on May 27.

Market sentiment deteriorated after reports emerged that the United States launched airstrikes near the Strait of Hormuz, escalating tensions with Iran and raising fears of disruptions across global energy markets.

Oil prices moved higher following the strikes, reviving concerns that inflation could remain elevated after hotter-than-expected U.S. CPI and PPI data earlier this month.

Traders increasingly expect the Federal Reserve to delay rate cuts, a scenario that has weighed on liquidity-sensitive assets, including cryptocurrencies. Gold advanced during the session while Bitcoin failed to hold above the psychologically important $76,000 level.

The geopolitical backdrop intensified after Iran introduced “Hormuz Safe,” a Bitcoin-denominated maritime insurance system designed to facilitate trade settlement outside traditional banking rails.

The U.S. Office of Foreign Assets Control warned that the platform could violate sanctions rules, while Iranian officials threatened retaliation after the airstrikes. At the same time, Israeli military operations expanded in southern Lebanon following the collapse of a temporary ceasefire extension earlier this month.

Spot Bitcoin ETF flows also weakened during the latest correction. Several U.S.-listed products recorded net outflows across recent sessions as institutional demand slowed after Bitcoin’s failed rally toward $82,000 earlier this month.

In a May 26 X post, Alex Thorn, head of research at Galaxy Digital, said the market still has “a lot of supply to absorb” near current levels as previous-cycle holders continue selling into rallies.

Thorn added that nearly 4.45 million BTC likely changed hands since the Oct. 10, 2025, flash crash, with a large share of coins originating from wallets that last moved Bitcoin above $103,600.

According to Galaxy’s data, roughly 36% of the supply transferred during that period came from holders with cost bases below $66,000, including dormant wallets inactive since before the FTX collapse in November 2022.

Meanwhile, BlackRock’s iShares Bitcoin Trust ETF drew attention after a reported $1.29 billion block trade earlier this month. Thorn said the transaction may suggest that some institutional investors have reduced exposure while Bitcoin remains far below its all-time high near $124,000.

Bitcoin remains trapped between liquidity clusters and key resistance levels

The daily chart shows Bitcoin losing momentum after breaking below an ascending parallel channel that guided price action higher through April and early May. The breakdown followed repeated rejections near the upper boundary of the structure, where sellers defended the $82,000 area aggressively.

Fibonacci retracement levels drawn from the February low near $59,988 to the May rebound high near $98,051 place immediate support around the 0.382 level at $74,528. The 0.5 retracement near $79,020 now acts as short-term resistance, while the 0.618 level at $83,511 aligns closely with the bullish target zone many traders continue to monitor.

The 200-day simple moving average near $80,169 has also capped upside attempts during the past several sessions. Bitcoin briefly pushed above the average earlier this month before sellers regained control and forced the price back below the indicator. The 50-day moving average has started turning lower as short-term momentum weakened following the rejection near $82,000.

Weekly chart structure presents additional pressure for bulls. Bitcoin remains well below the cycle high near $124,000 posted earlier this year, while weekly MACD readings continue to print negative momentum despite the rebound from the $60,000 region.

RSI readings near 45 have yet to return above bullish territory, leaving the market without a confirmed higher-timeframe trend reversal.

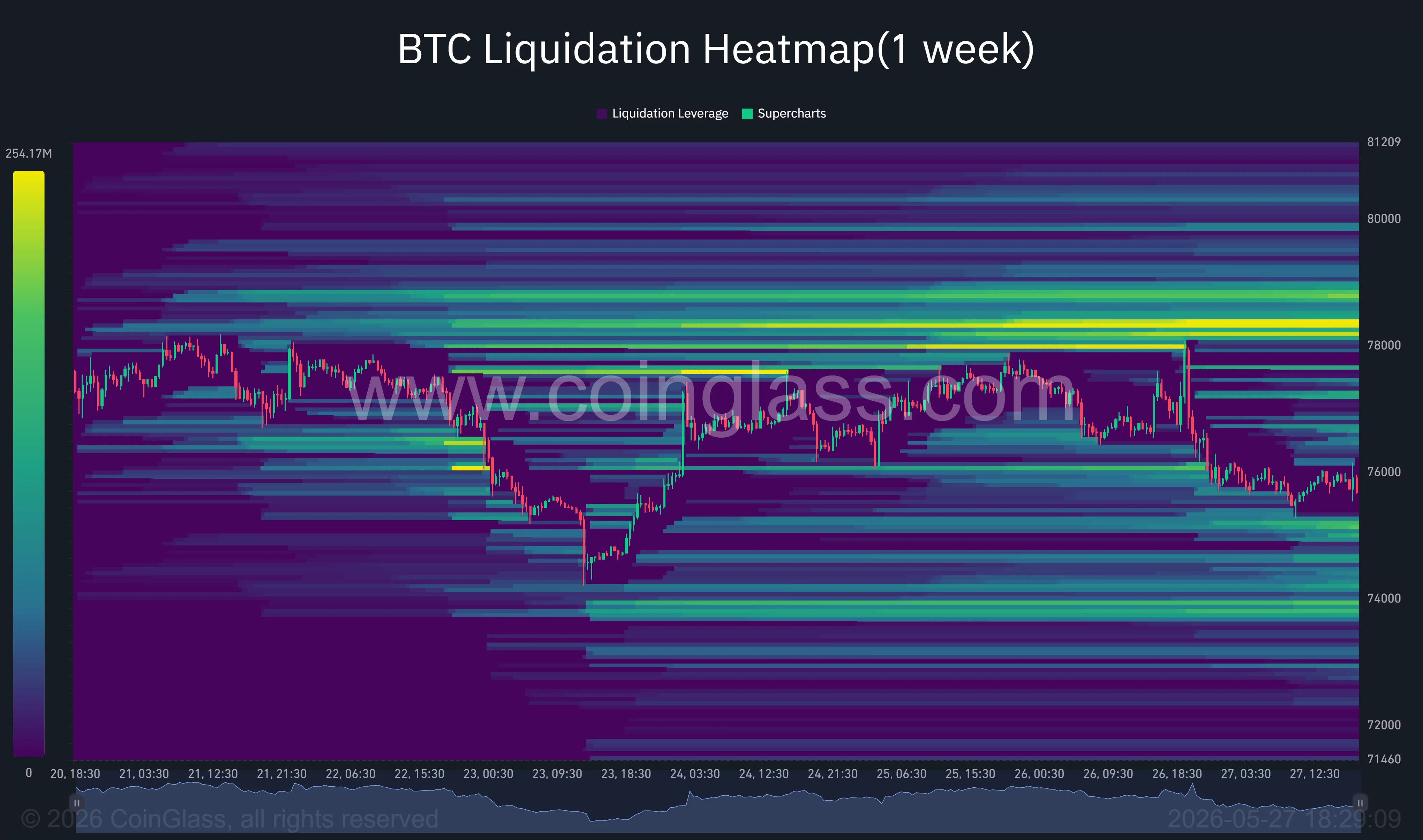

Derivatives positioning also points to elevated volatility around current levels. CoinGlass liquidation heatmaps show dense clusters of leveraged short positions sitting between $77,800 and $78,500, with additional liquidity stacked near the $80,000 and $81,000 levels. These zones have repeatedly attracted price during intraday moves as market makers hunted leveraged positioning on both sides.

Below the current price, major liquidation pools remain visible near $74,000 and between $72,000 and $73,000. Bitcoin’s inability to reclaim higher liquidity zones after several attempts has increased the risk of another sweep lower should support near $75,000 fail during the coming sessions.

In a May 26 post on X, crypto analyst Crypto Candy said Bitcoin continues to hold above a key demand zone despite the recent sell-off.

“So far, not much has changed in the BTC scenario. It’s still holding above the demand zone of 76k-74k and trying to rebound. As long as this zone sustains, we still expect BTC to reach the 83k-85k area. This bias is invalid once it closes below the demand zone,” said the analyst.

Meanwhile, analyst BitcoinHyper outlined a more cautious short-term scenario, suggesting Bitcoin could be forming an ABC corrective structure after the recent rejection near $82,000. According to the analyst, BTC could first rebound toward the $79,000 area before another leg lower potentially drives the price toward $71,000.

A breakdown below $74,000 could expose lower support zones

A decisive move below the current demand zone would weaken the remaining bullish structure across both daily and weekly timeframes. Traders continue watching the $74,000 region closely because it aligns with the lower boundary of recent consolidation, the 0.382 Fibonacci retracement level, and a major concentration of leveraged long positions.

Further downside could expose Bitcoin to a move toward the March accumulation area near $68,900, where the 0.236 Fibonacci retracement currently sits. Historical volume profiles also show heavy spot activity around that range following the February liquidation cascade earlier this year.

Open interest across Bitcoin perpetual futures contracts has also stayed elevated despite the latest correction. Traders continue using high leverage around local support and resistance zones, increasing the probability of sharp liquidation-driven moves if volatility expands during upcoming macro events or geopolitical headlines.

For now, Bitcoin remains stuck between heavy resistance near $78,000-$80,000 and fragile support around $74,000-$75,000. Until one side breaks decisively, traders are likely to remain focused on liquidity sweeps, ETF flow data, and macro headlines rather than long-term directional conviction.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Robinhood (HOOD) is giving retail traders a new way to automate investing: letting artificial intelligence make decisions and place trades on their behalf.

Customers can now connect third-party AI agents to Robinhood accounts to manage trading activity and even complete purchases through virtual credit cards, Robinhood announced Wednesday. The rollout includes two products, Agentic Trading and the Agentic Credit Card.

The tools effectively turn AI assistants into automated financial operators that can monitor markets, rebalance portfolios or execute strategies without requiring constant attention from the customer.

A trader who wants exposure to artificial intelligence stocks could instruct an AI agent to build and maintain a portfolio focused on the sector. Another user could ask an agent to automatically buy oversold stocks based on a predefined trading strategy.

Automated AI trading

The company said users will also be able to automate purchases through AI-connected virtual credit cards. Customers can direct agents to monitor prices for products or complete purchases once certain conditions are met.

Robinhood is pitching the tools as a way to reduce the amount of time customers spend researching investments or tracking deals manually.

The new products mark clear examples of AI-driven financial automation moving from hedge funds and institutional trading desks into mainstream retail investing apps.

Until now, automated AI trading systems have largely been confined to Wall Street firms with dedicated risk-management teams and quantitative trading infrastructure. Robinhood’s move opens those capabilities to smaller investors using consumer-grade AI tools.

That shift also raises questions about how much control retail users should hand over to autonomous systems, especially in volatile markets.

Robinhood said it designed the products with several guardrails. AI agents operate through separate trading accounts with access limited to only the funds customers allocate. Users receive notifications whenever trades occur and can disable agents instantly.

The company also added spending controls and optional manual approvals for AI-driven purchases.

Initially, Agentic Trading will support stock trading only while it remains in beta. Robinhood said support for options, crypto and futures trading is planned later.

HOOD shares climbed 1.5% to $75.20 during the U.S. morning on Wednesday’s following the announcement.

Preston Davey trial LIVE as teacher charged with baby’s murder accused of ‘buying time’ in hospital

NYC hotel costs poised to climb following historic union contract

Vaults Could Rewire Capital Markets as TVL Hits $131B

-

Crypto World6 days ago

Crypto World6 days agoBlockchain.com files with SEC for U.S. IPO

-

Fashion5 days ago

Fashion5 days agoHoliday Weekend Open Thread – Corporette.com

-

Crypto World5 days ago

Crypto World5 days agoBitcoin Accumulation Weakens as BTC Realized Losses Hit $600M

-

Business5 days ago

Business5 days agoDell Technologies DELL Stock Surges 15% on AI Server Momentum and Analyst Upgrades in 2026

-

Crypto World4 days ago

Crypto World4 days agoRobinhood crypto COO Tanya Denisova exits

-

Tech2 days ago

Tech2 days agoMicrosoft’s quiet Claude Code retreat and the real cost of enterprise AI

-

Politics5 days ago

Politics5 days agoMakerfield: a tale of two social-media histories

-

Business3 days ago

Business3 days agoNYT Strands Answers May 24 2026 Revealed for Puzzle No. 812 Theme Summer Essentials

-

Crypto World5 days ago

Crypto World5 days agoSpace X IPO Is ‘Bad News’ for Tech Stocks: But What About Bitcoin?

-

Crypto World6 days ago

Crypto World6 days agoMicroStrategy’s Saylor Says Miners No Longer Set Bitcoin Price, Another Force Has Taken Over

-

Business5 days ago

Business5 days agoTrump Invests $1M-$5M in Kura Sushi USA Chain With 27 California Locations

-

Tech6 days ago

Tech6 days agoWhatsApp ads could make Irish debut after discussions with DPC

-

NewsBeat6 days ago

NewsBeat6 days agoCharity run by Reform leader Malcolm Offord accused of ‘law breaking’ over Scottish registration

-

Tech5 days ago

Tech5 days agoA 0.12% parameter add-on gives AI agents the working memory RAG can’t

-

Crypto World5 days ago

Crypto World5 days agoAI infrastructure race heats up as IREN pitches full-stack strategy, WhiteFiber lands $160M deal

-

Crypto World2 days ago

Crypto World2 days agoNvidia (NVDA) CEO Calls on Super Micro to Strengthen Export Controls Amid Smuggling Probe

-

Tech3 hours ago

The Samsung pay deal is the moment Korean unions changed register

-

Tech6 days ago

Tech6 days agoYou Can Now Add ChatGPT To PowerPoint

-

Tech2 days ago

Tech2 days agoWestone Audio and Etymotic Acquired by Fidelity Collective in Major IEM Market Move

-

Sports6 days ago

Sports6 days ago2026 CJ Cup Byron Nelson leaderboard: Brooks Koepka finds putting stroke in Round 1

You must be logged in to post a comment Login