Crypto World

Why traders are turning to smart forex bots for currency market automation

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Smart forex bots gain traction in 2026 as traders seek automated tools to monitor fast-moving currency markets.

Summary

- Smart forex bots are gaining traction as traders automate monitoring and execution across fast-moving currency markets.

- Modern expert advisors increasingly focus on single pairs like GBP/USD, using coded risk controls and backtesting.

- Traders remain cautious of overfitting, volatility risks, and execution quality despite improved transparency and automation.

Trading manually is getting harder and harder to justify, which is why an increasing number of retail traders have started turning to automated systems instead.

The BIS triennial survey for April 2025 put daily forex volume at $9.6 trillion – a 28% jump from three years earlier. Read on for a look at how automation tools are involved in this increase, and what the trade-offs are.

A market that doesn’t stop

London opens while Tokyo is wrapping up, then New York kicks in a few hours later. For traders watching two or three currency pairs at once (which most are these days), that’s an impossible amount of screen time to cover properly. Prices on the major pairs can move fast — we’re talking seconds — and a lot of this happens while a trader is asleep or otherwise occupied.

That’s why smart forex bots have jumped in popularity. In short, they watch the market so a person doesn’t have to. Whether they do that job well is a different kettle of fish, but the case for their use is pretty understandable.

What’s going on under the hood

Most of these tools are what’s called expert advisors — scripts written in MQL4 or MQL5 that get loaded into MetaTrader. How this works is an EA watches price data on a specific timeframe and checks it against coded rules. When those rules line up with what’s happening on the chart, it opens a position automatically. The whole idea is to take humans out of the moment-to-moment decisions.

Over the past year or two, a lot of these EAs have become narrower. Rather than trying to trade 8-10 pairs, some of them now only focus on one. GBP/USD is a common pick thanks to its liquidity windows — which are predictable — plus the fact that it responds in fairly consistent ways to Bank of England and Fed rate decisions. If an algorithm only has to learn one instrument’s behavior, it can be tweaked better than a system trying to do it all.

A setup might look at patterns on the daily chart to figure out which way the trend is going, then drop down to the M15 to time entries. Smart forex bots doing this analysis can filter out a lot of what trips up manual traders. But in practice, it depends how good the bot’s underlying logic is.

Risk management is coded in as well, covering all manner of variables from stop-loss placement, to how big each position is relative to the account, and how many trades can be open at once.

Some EAs also use a protocol where position size goes up after a losing trade. This recovers drawdowns faster when it works, but it can be nasty if a losing streak goes on longer than expected too. There’s always that tension with automated recovery — it looks great in a backtest, until a unique scenario arises.

Backtesting is what most traders don’t spend enough time on. Years of tick data can be fed through an EA (Tick Data Suite from Thinkberry SRL is commonly used for this) and the results give a picture of how the system would have handled various market conditions.

The quality of that data really does affect the outcome though, and it’s not all created equal.

Where it goes wrong

Over-fitting is still an issue. An EA that’s been tuned on 2018–2024 GBPUSD data can look incredible on paper, sure. But the week conditions shift with a surprise tariff announcement, it’ll fall apart. Trading bots typically deliver inconsistent results during volatility. April 2025’s tariff-driven chaos is a case in point, as it was a very revealing stress test for a lot of bots.

Trust is getting better, at least. Most platforms now let traders look at performance logs before putting money in. This is a step up from the old days of screenshots. If an EA provider won’t put up audited results going back a couple of years, that’s not good enough anymore.

Infrastructure is worth thinking about too, especially for strategies that work in tight windows. An EA on a home laptop won’t execute trades at the same speed as one on a VPS sitting near a data centre. For a lot of retail setups, this gap is fine, but for anything that depends on getting in and out within a few pips, it’s not.

None of this is going away any time soon. Pair-specialized EAs are putting up track records long enough to judge now, which wasn’t the case a few years ago. Bottom line, a bot won’t turn a bad strategy into a good one — but for traders who’ve already figured out the risk side of things, automation is less of a gimmick now than it used to be.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Solana price has recovered from recent market weakness, with bulls now attempting to overcome double-top resistance near the $100 level.

Summary

- Solana price traded near $87 as traders monitored whether mounting short liquidations and improving ETF sentiment could drive a breakout above $100.

- Morgan Stanley reportedly refiled a Solana ETF with staking support under the “MSOLsec” ticker, adding to institutional momentum around SOL products.

- Analysts identified heavy liquidation clusters between $90 and $95, while repeated double-top resistance continued capping Solana’s upside attempts.

Across the crypto market, risk appetite improved modestly after Bitcoin reclaimed ground above $77,000 following several sessions of macro-driven weakness tied to geopolitical tensions and volatility in oil markets.

The rebound helped major altcoins recover intraday losses, although traders remain cautious ahead of further U.S. inflation data and Federal Reserve commentary that could influence liquidity conditions across risk assets.

At the same time, institutional activity surrounding Solana has continued to strengthen despite the recent correction. A fresh catalyst emerged after Morgan Stanley reportedly refiled a Solana ETF product with staking support under the “MSOLsec” ticker, adding to growing expectations that regulated SOL investment vehicles could eventually mirror the success of spot Bitcoin and Ethereum products.

The filing arrived as asset managers continue expanding their exposure to staking-enabled crypto funds in search of yield-bearing digital assets.

Meanwhile, capital inflows into Solana-linked investment products have remained comparatively resilient during May’s choppy trading conditions. Products managed by firms such as Bitwise continued attracting attention from institutional allocators even as several other altcoins experienced declining flows.

Analysts say the ability of Solana products to maintain steady demand during a corrective phase suggests longer-term positioning rather than speculative short-term trading.

On-chain fundamentals have also remained constructive. In April 2026, Solana-based DePIN ecosystems generated a record combined revenue of roughly $2.9 million, according to ecosystem tracking data.

Projects including Helium, Render, and Hivemapper contributed heavily to the surge as decentralized infrastructure demand continued expanding across AI compute, mapping, and wireless connectivity markets.

Enterprise adoption narratives have continued building underneath the market. Payment giant Visa has already integrated Solana infrastructure into parts of its stablecoin settlement operations, while Meta has reportedly explored USDC-based creator payouts utilizing Solana rails. Traders increasingly view these commercial integrations as a long-term valuation support layer that differentiates Solana from purely speculative Layer-1 ecosystems.

Can Solana break through its double-top resistance structure?

Solana remains trapped beneath a significant resistance zone after forming another local double-top pattern on both the daily and weekly timeframes. The charts show repeated rejection near the $95 to $100 region, an area that has capped upside attempts multiple times since late 2025.

On the daily chart, Solana (SOL) continues trading below the 200-day moving average near $107.89, while short-term moving averages around $86–$89 are beginning to flatten. Price action has compressed into a tight consolidation range after rejecting near $98 earlier this month, suggesting bulls and bears remain locked in a directional battle.

Momentum indicators have weakened but have not fully rolled over into bearish territory. The MACD histogram on the daily timeframe remains negative, although selling momentum has gradually faded over the past several sessions. Weekly MACD readings have also started stabilizing after months of persistent downside pressure, raising the possibility of a medium-term trend reversal if buyers reclaim higher resistance levels.

From a structural perspective, traders are closely monitoring the 0.382 Fibonacci retracement region between $87 and $90. Analysts view sustained closes above that area as an early confirmation that Solana may be transitioning out of its post-double-top consolidation phase. A breakout above $90 could expose liquidity near $95 before opening the path toward the key psychological barrier at $100.

According to analyst Javon Marks, Solana is once again holding a long-term support area that previously triggered explosive rallies. In a recent market update, Marks said one historical rebound from the level generated an 80% rally while another produced gains exceeding 270%.

“With prices showing strength off of this support level again, we are watching for an over 165% climb to test a key technical level at $233.8 again,” Marks wrote in a May 22 X post.

Beyond directional price action, derivatives positioning suggests a sharp volatility move could emerge if resistance levels begin failing. CoinGlass liquidation heatmaps show dense liquidation clusters concentrated between $90 and $95, with another large band sitting just above current price levels.

A decisive move into that region could trigger forced short liquidations and accelerate upside momentum through a classic squeeze setup. Market data cited by traders indicates short sellers recently absorbed nearly five times more liquidation pressure than longs.

Open interest has also started rising gradually after several weeks of deleveraging, suggesting traders are rebuilding directional positions ahead of a potential breakout attempt. Funding rates, while not excessively bullish, have stabilized near neutral territory, a setup many derivatives traders consider healthier than heavily crowded long positioning.

Meanwhile, Solana’s total value locked has shown signs of stabilizing after months of contraction. Analysts tracking on-chain liquidity argue that a sustained TVL recovery would likely strengthen spot demand for SOL tokens while reinforcing confidence in Solana’s decentralized finance ecosystem. Historically, periods of expanding TVL have coincided with stronger medium-term price performance for SOL.

What could invalidate Solana’s bullish breakout thesis?

Despite improving sentiment, several downside risks continue threatening the bullish setup. The most immediate concern remains Bitcoin’s fragile position near major support levels as global macro uncertainty continues pressuring risk assets.

Oil markets remain highly sensitive to developments surrounding U.S.-Iran negotiations and shipping disruptions near the Strait of Hormuz. Any renewed spike in crude prices could reignite inflation concerns and reduce expectations for Federal Reserve rate cuts, creating another wave of risk-off pressure across crypto markets.

At the same time, Solana’s technical structure still carries meaningful bearish risk unless buyers reclaim the $95–$100 resistance band decisively. Repeated rejections beneath double-top resistance often weaken bullish momentum over time, particularly if accompanied by declining spot demand.

Failure to hold the $84–$85 support region could expose lower liquidity zones near $80 and potentially reopen the path toward the March lows. CoinGlass heatmap data already shows notable downside liquidation pockets sitting below current prices, meaning volatility could accelerate rapidly if sellers regain control.

The longer-term weekly chart also shows SOL continuing to trade well below its 2025 highs despite recent stabilization. Until the asset reclaims the major breakdown region near $104, some traders may continue treating rallies as temporary relief bounces within a larger bearish market structure.

Still, improving institutional narratives, expanding enterprise adoption, growing DePIN revenues, and mounting short-side leverage continue giving bulls a credible case for another breakout attempt.

If Bitcoin stabilizes and macro conditions avoid further deterioration, Solana may soon test whether the market still has enough momentum to finally clear the stubborn double-top ceiling and reclaim triple-digit territory.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Bitcoin DeFi platforms on Rootstock simplify staking, rBTC rewards, and DeFi access for mainstream users.

Summary

- Rootstock is expanding Bitcoin DeFi access with staking, rBTC rewards, and EVM-compatible infrastructure.

- The sidechain has operated since 2018, offering lower fees, faster confirmations, and Bitcoin-backed security.

- RootstockCollective lets users stake RIF tokens while helping fund Bitcoin-focused builders through its DAO model.

Bitcoin DeFi is no longer reserved for technical experts. Platforms built on Rootstock make it simple to stake RIF, earn rBTC rewards, and participate in decentralized finance backed by Bitcoin’s consensus security, no specialized knowledge required.

Why Bitcoin DeFi has been so hard

Less than 1% of all BTC is deployed in decentralized finance, despite Bitcoin being the most widely held cryptocurrency. The reason is friction: specialized wallets, multi-chain bridging, unfamiliar gas tokens, and confusing interfaces. A BTCFi survey reported that 36% of respondents avoid BTCFi entirely due to lack of trust.

That’s changing fast. BTCFi total value locked grew roughly 20x from about $307 million in January 2024 to approximately $6.5 billion by mid-2025 (figures vary by methodology), driven by EVM-compatible Bitcoin sidechains like Rootstock that bring familiar tools to Bitcoin’s security.

How Rootstock and RootstockCollective remove the barriers

Rootstock is Bitcoin’s longest-running sidechain, operating since 2018 with 100% uptime. It inherits consensus security from Bitcoin via merged mining (participation reported in the 60–80%+ range of Bitcoin’s hashpower) while offering full EVM compatibility. The native token rBTC is pegged 1:1 to Bitcoin via the PowPeg bridge, a federated peg design. Transactions confirm within one to two blocks, fees are far lower than Ethereum’s (reduced ~60% after network upgrades), and the ecosystem includes 150+ partner applications with familiar names like Uniswap (via Oku), SushiSwap, and LayerBank.

RootstockCollective is the first DAO built for Bitcoin builders on this foundation. It’s where users can stake RIF tokens AND directly fund builders, combining rewards with real ecosystem impact. Key features that simplify onboarding:

Feature

Traditional Bitcoin DeFi

RootstockCollective on Rootstock

Wallet setup

Specialized, unfamiliar wallets

MetaMask and popular EVM wallets via Reown AppKit

Gas costs

High and unpredictable

Far lower than Ethereum; reduced ~60% after upgrades

Custody model

Often custodial or wrapped

Non-custodial; the user controls tokens

Reward transparency

Variable, often unclear

Bi-weekly distributions in rBTC, RIF, and USDRIF

Staking flexibility

Lock-up periods common

No lock-up; unstake anytime

With an approximately 20% average Annual Backer Incentive (varies by period), over 3.7 BTC,1.4 million RIF and $20k USDRIF paid out in Collective Rewards, and 35 million+ RIF staked, the reward mechanics are transparent and proven. Governance happens on-chain via the RootstockCollective dApp, so that funds can be seen exactly where they go.

Start earning in six steps

Step 1: Set Up a Wallet. Install MetaMask (or Rabby, SafePal, etc.) and add the Rootstock network by visiting the Get RIF page and clicking “Add RIF to wallet.” It configures everything automatically. Coming soon: social login via MagicLink for users new to web3 wallets.

Step 2: Get RIF Tokens. Purchase RIF on Binance, Gate.io, Bitget, or MEXC, then withdraw to a wallet. When withdrawing, select the RSK/Rootstock network, not ERC-20 or BEP-20. Alternatively, use Symbiosis or Router Protocol to bridge assets directly to Rootstock.

Step 3: Get rBTC for Gas. Swap a small amount of RIF for rBTC on SushiSwap (select RIF → rBTC and confirm), even 0.001 rBTC covers many transactions. Users can also bridge BTC via the PowPeg app at 2wp.rootstock.io (Fast Mode completes in ~20 minutes) or use Boltz.

Step 4: Stake RIF. Visit the official website, click “Connect Wallet” (top right), and select a wallet. Navigate to “Stake,” enter an amount, click “Stake,” and approve in MetaMask. RIF converts to stRIF at 1:1. After approving, the user has voting power in the DAO.

Step 5: Back Builders. Go to the Builders screen to see active builders. Review each builder’s “Backer Share %”, the percentage of earnings they share with backers. Hover over a chosen builder, press “Back builder,” then type an allocation or drag the allocation bar on the Backing page. Confirm on-chain. Example: if a builder earns 20% of total cycle rewards and sets a 25% Backer-Reward Percentage, backers collectively receive 5%, distributed proportionally by allocated stRIF.

Step 6: Claim Rewards. Go to the Holdings screen, view “My Balances,” and click “Claim Rewards.” rBTC, RIF, and USDRIF arrive in a wallet after approval. There’s no deadline; rewards remain available until they are collected.

Two roles, one virtuous cycle

RootstockCollective runs on two complementary roles.

- Backers stake RIF, vote on proposals, and allocate stRIF to support builders, earning a share of their rewards proportional to their backing.

- Builders, teams creating dApps, protocols, and infrastructure on Rootstock, submit proposals, receive community votes, and access grants plus ongoing Collective Rewards. The more backing a builder attracts, the larger their share of the reward pool, and a portion flows back to their backers.

Current ecosystem projects include OpenOcean, Boltz, WoodSwap, Money On Chain, Tropykus, WakeUp Labs, LayerBank, Steer Protocol, Symbiosis, Hunters of Web3 and Top Tier Alliance, and more. All smart contracts are built on audited OpenZeppelin libraries, treasury is managed through multisig controls with Foundation oversight, and all actions are recorded on-chain.

The next step: visit the RootstockCollective website, connect a wallet, and stake the first RIF.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

In 2025, stablecoins settled more transactions than Visa. Real-world stablecoin payments doubled to $400 billion. Visa, Mastercard, Stripe, PayPal, and Western Union all turned on stablecoin rails inside their existing products. The GENIUS Act became U.S. law. And almost no one outside crypto noticed. The most important shift in the global payments system in twenty years happened in plain sight, and it is still being misread as a crypto story.

Summary

- Stablecoin transaction volume reached levels comparable to Visa in 2025 as payment giants integrated blockchain-based settlement rails into existing products.

- Real-world stablecoin payments doubled to $400 billion last year, with most activity tied to business payments, payroll, and cross-border settlements.

- The GENIUS Act gave banks and regulated firms a legal framework to issue and integrate stablecoins, accelerating adoption across the financial sector.

The biggest story in crypto is not about crypto

Strip away the meme coins, the price predictions, the ETF flow charts, and the regulatory drama. The single most consequential thing happening in digital assets right now has nothing to do with any of it. It is not Bitcoin. It is not even speculation. It is the quiet, accelerating absorption of stablecoins into the actual plumbing of how the world moves money.

Some numbers, because the numbers are the story.

The global supply of fiat-backed stablecoins crossed $319 billion in April 2026, up from roughly $7 billion six years earlier. A forty-fold expansion in an asset class that did not meaningfully exist before 2020. Adjusted stablecoin transaction volume grew ninety-one percent in 2025 to $10.9 trillion, closing in on Visa’s $14.2 trillion. By Plasma’s accounting, total settlement volume hit $33 trillion last year, past Visa’s annual throughput. Stablecoins processed roughly twenty times the volume PayPal did. Morph’s research projects that 2026 stablecoin settlement could top $50 trillion.

The most telling figure is not the size. It is the mix. Real-world stablecoin payments, the share of activity that is not crypto trading but actual commercial movement of money, doubled in 2025 to $400 billion. Sixty percent of that was business-to-business: companies paying suppliers, settling cross-border invoices, managing treasury, and moving payroll. Stablecoins are no longer just chips at the crypto casino. They have become an operating layer of international finance.

The reason this has happened without much public attention is mostly aesthetic. Stablecoins look boring. A dollar-pegged token does not 10x. There is no narrative, no chart porn, no influencer screaming about a new all-time high. They are infrastructure, and the great rule of infrastructure is that it stays invisible until it does not. The whole point of a stablecoin is that nothing dramatic happens to it. The dramatic thing is what gets built on top.

That is now being built. Fast.

What “internet money” actually has to do

For anyone who has spent any time around crypto, the phrase “internet money” has been thrown around for a decade, usually attached to assets that turned out not to be anything of the kind. Bitcoin was supposed to be it. Then Ethereum. Then a parade of L1s. None of them quite worked as money, because money has a job description far more demanding than “store of value” or “speculative asset.” It has to be reliable in unit, accepted broadly, transferable cheaply, and usable for the boring middle ninety percent of economic life: paying rent, settling invoices, sending payroll, buying coffee.

Stablecoins fit that job description in a way no prior digital asset did. They are pegged to the dollar, so a stablecoin is not really an investment; it is just a dollar that happens to live on a blockchain. Reserves, when properly backed, sit in cash and Treasury bills, the same instruments that already underpin trust in the financial system. Transactions are near-instant, run twenty-four hours a day, settle on weekends, cross borders without correspondent banking, and cost a fraction of what wire transfers do.

What changed in 2025 and 2026 was not the technology. Stablecoins have done these things for years. What changed was that the actual companies that move money for everyone else started building stablecoins into their products as a default, not an experiment.

The list reads like a roll call of global payments. Visa runs a stablecoin settlement program that hit a $7 billion annualized run rate in late April 2026, up fifty percent from the previous quarter, and operates across nine blockchains, including Ethereum, Solana, Avalanche, Base, and Polygon. Visa’s broader Visa Direct stablecoin payout product is live in over fifty countries. Mastercard, Stripe, PayPal, Western Union, Klarna, Cloudflare, Meta, Intuit, Fiserv, and Zelle have all either launched or announced integration plans. PayPal’s own stablecoin, PYUSD, sits in their consumer app alongside fiat balances.

The shape of the change is what matters. None of these companies is making a bet on a speculative asset. They are quietly upgrading the rails their existing products run on. A Visa card customer in Bogotá does not know, and does not need to know, that the back-end settlement between the issuing bank and Visa now travels as USDC on Solana rather than as fiat through a correspondent banking chain. The user experience is unchanged. The plumbing underneath is being replaced.

The two stablecoins that run the world

The market is, for now, a duopoly. Tether’s USDT holds roughly $189.6 billion in circulation. Circle’s USDC sits at around $77.6 billion. Together, they account for well over eighty percent of the global stablecoin supply.

They are not the same product, and the difference matters more in 2026 than it did before.

USDT is the offshore stablecoin. It dominates emerging-market trading, runs the largest share of remittance corridors in Latin America, Africa, Southeast Asia, and the Middle East, and serves as the dollar substitute in countries where local currencies are volatile or banking access is poor. Tether’s reserves, increasingly weighted toward U.S. Treasury bills (a $113 billion Treasury position as of Q1 2026), have made the company one of the largest non-sovereign holders of US debt in the world. USDT’s market share is slowly shrinking as regulated alternatives emerge, but its absolute supply continues to grow.

USDC is the compliance stablecoin. It is the one U.S. bank, payment companies, and large enterprises actually want to integrate with. Circle is publicly traded, USDC is attested monthly by Deloitte, it is licensed under Europe’s MiCA framework, and it sits in the strongest position under the new U.S. GENIUS Act regime. Where USDT wins on liquidity and reach, USDC wins on the things that matter to a compliance officer: clarity of reserves, regulatory approval, and the absence of legacy controversy.

The next tier of issuers is small but growing. Sky’s USDS at $8.4 billion, the rebuilt DAI at $4.7 billion, PayPal’s PYUSD, Ripple’s RLUSD now climbing toward $1.6 billion, USDe, and various yield-bearing variants. The duopoly is not breaking up, but the long tail is starting to matter. Banks and fintechs that want to issue their own stablecoins under the new U.S. framework are building the next wave now.

What the GENIUS Act actually changed

To understand why 2025 was the inflection point, you have to understand what the GENIUS Act did, because almost every meaningful piece of the stablecoin acceleration traces back to it.

The Guiding and Establishing National Innovation for U.S. Stablecoins Act was signed into law in July 2025. It is the first comprehensive US federal framework for payment stablecoins, and it does three things that, together, changed the calculus for every serious financial institution.

First, it answered the question of what a payment stablecoin legally is. The act establishes that permitted payment stablecoins are not securities, commodities, or deposits. They are a new regulated category with their own regime, administered principally by the Office of the Comptroller of the Currency alongside the FDIC, the Federal Reserve, the Treasury, and state banking regulators. That clarity matters because the absence of a category was, for years, the single biggest reason serious institutions stayed out.

Second, it set the rules of issuance. Stablecoin issuers must hold one-to-one reserves in high-quality liquid assets, publish monthly attestations, undergo audits, and comply with anti-money-laundering and sanctions requirements. Permitted issuers are limited to insured depository institutions (banks and credit unions), subsidiaries of such institutions, and certain approved nonbank entities. In effect, the law turned stablecoin issuance into a regulated banking activity.

Third, it opened the door for banks themselves to issue. A national bank can now issue a payment stablecoin under OCC supervision. Tokenized deposits, where a bank’s actual liabilities to its customers are represented as tokens on a ledger, sit within reach. Banks that spent years watching Tether and Circle gather a sector they were structurally locked out of now have a path in.

The OCC proposed its implementing rules in late February 2026, with the comment period closing on May 1. The act’s effective date arrives at the earlier of eighteen months after enactment (January 2027) or 120 days after final regulations. Practical impact, then, takes full effect roughly from mid-2026 onward.

The first-order effect was psychological. Once U.S. law existed, the asset class became investable to a class of institutions that had been waiting on a green light. The second-order effect, which is now playing out, is the wave of bank and fintech stablecoin pilots, tokenization initiatives, and payment integrations that have hit the market since the bill was signed.

The use cases that are no longer hypothetical

Three real-world use cases are now operating at scale, and a fourth is approaching.

Cross-border B2B payments are the largest and most boring. A U.S. importer paying a Vietnamese supplier traditionally goes through correspondent banks, taking three to five days and losing three to seven percent to fees, intermediary charges, and FX spread. The same transaction in stablecoins settles in seconds for cents. Sixty percent of stablecoin payment volume in 2025 was B2B precisely because the cost-benefit is overwhelming and the regulatory exposure for a corporate treasury team has dropped sharply under the new framework.

Cross-border consumer payments and remittances are the most socially significant. In countries where banking is shallow, local currencies are weak, or capital controls are tight, stablecoins have quietly become the preferred way to receive money from abroad. A migrant worker in the Gulf sending money home to family in Lagos increasingly does so in USDT, which the recipient can hold, spend at a growing number of merchants, or convert locally. The “informal” stablecoin economy is not on most balance sheets, but Chainalysis and others have documented its scale year after year.

Card-linked stablecoin spending is the bridge between crypto-native dollars and the real economy. Companies like Rain issue Visa-network cards that draw against stablecoin balances and settle directly in stablecoins with Visa. A BVNK and YouGov survey of over 4,000 stablecoin users found that seventy-one percent said they would use a linked debit card to spend their stablecoins. The infrastructure is now there. The “spend” leg of the payments lifecycle, the one missing piece until late 2024, is closing.

AI-agent payments are the fourth use case, still emerging but worth flagging because they may end up being the largest. A new generation of protocols, the most discussed being x402, lets AI agents transact with each other directly: paying for data, GPU time, API calls, or other agent services without human approval and without traditional invoicing. The economic case requires payments that are programmable, instant, sub-cent in cost, and machine-readable. Stablecoins are the only existing form of money that meets all four. As AI commerce scales, an enormous share of it will, by necessity, run on stablecoin rails.

The framing matters here. The first three use cases describe stablecoins replacing parts of the existing payment infrastructure. The fourth describes them enabling a payment market that does not yet exist in fiat form. Both expansions are happening at once.

What can still go wrong

A piece that only described the upside would be marketing, not journalism, so here is the other side.

Stablecoins remain only as good as their reserves and their operators. The 2022 collapse of TerraUSD wiped $40 billion in three days and is the cautionary tale every regulator now writes against. Even fiat-backed stablecoins are not risk-free: USDC briefly de-pegged in March 2023 when Circle’s exposure to the failing Silicon Valley Bank surfaced. The reserves were ultimately recovered, but the episode showed that even properly backed stablecoins can wobble under banking stress. The GENIUS Act explicitly addresses some of these failure modes, but the law’s allowance for issuers to hold uninsured bank deposits as reserves has drawn warnings from the Brookings Institution and other observers who note it creates a two-way coupling between bank risk and stablecoin risk.

Banks themselves are watching stablecoin growth uneasily, because every dollar that migrates from a bank deposit into a stablecoin balance is a dollar the bank no longer has to lend. The American Bankers Association and similar groups in Europe have lobbied hard, and largely unsuccessfully so far, for tighter restrictions on stablecoin yield and on competition with deposit accounts. If deposits drain faster than legislators expect, the banking lobby will push back harder.

Geopolitical risk runs in two directions. Dollar-pegged stablecoins are extending dollar reach into corners of the world that local sovereigns would rather control, which is already producing capital controls pushback in several emerging markets. At the same time, the dominance of U.S.-dollar stablecoins (more than ninety-nine percent of fiat-backed stablecoin value is dollar-pegged) makes the asset class an instrument of dollar hegemony, which both helps and complicates the geopolitics of payments. China is pushing its own central bank digital currency in parallel. The EU has MiCA and a digital euro project on a slower timeline. The next decade of payments policy will be partly a contest between these models.

Finally, the most boring risk is the most likely. Implementation matters. The rules being written by the OCC and other regulators between now and final implementation in 2026 and 2027 will determine whether the stablecoin sector grows into a regulated, integrated piece of finance or fragments into a series of jurisdictional silos that limit the benefits of a borderless rail.

What this means in the end

The shorthand for what is happening is “stablecoins are eating payments.” That is not quite right, because payments are not a single thing being replaced. What is actually happening is that the dollar itself is being upgraded into a new technical form, one that runs on open networks, settles in seconds, costs almost nothing to move, and operates twenty-four hours a day. Stablecoins are the vehicle. The dollar is the cargo.

If you zoom out, this is a bigger development than the launch of spot Bitcoin ETFs, the CLARITY Act, or any of the other crypto stories that have dominated headlines this cycle. ETFs gave institutions a way to hold Bitcoin. Stablecoins are giving the entire global economy a new way to use dollars. Those are not comparable in scale.

What makes the shift hard to see is that it does not look like a revolution. It looks like a payment is landing in your account faster than you remember it landing before. It looks like a supplier in another country is getting paid the same day instead of the next week. It looks like a Visa card that works the same as it always did, even though the settlement underneath has fundamentally changed. It looks like nothing, until one day you realize most of the dollars in the global digital economy live on rails that did not meaningfully exist five years ago.

That is what infrastructure does. It disappears. And once it disappears, it is hard to put it back.

The internet got money. Almost no one noticed. The next decade of finance will be spent catching up.

This article is for informational purposes and does not constitute financial or investment advice. Stablecoin regulations, transaction volumes, and reserve compositions can change quickly; the figures described reflect reporting available as of mid-May 2026. Always do your own research.

While crypto Twitter argues about Bitcoin versus Ethereum, two superpowers are quietly running a different race. The United States is using dollar-backed stablecoins to extend the dollar’s reach into every corner of the digital economy. China is using its e-CNY and the mBridge platform to build an alternative settlement system that bypasses the dollar entirely. The outcome will shape the next century of global finance. And almost nobody outside policy circles is paying attention.

Summary

- The United States has used dollar-backed stablecoins and the GENIUS Act to expand the dollar’s role across global digital payments and crypto networks.

- China has accelerated cross-border use of the eCNY through mBridge and new interest-bearing wallet policies tied to its state-controlled digital currency system.

- Despite de-dollarization efforts from BRICS nations, dollar-pegged stablecoins still dominate global digital settlement activity and reinforce demand for U.S. dollar assets.

The argument that misses the actual fight

Open any crypto publication this year, and you will find some version of the same debate. Bitcoin maximalists versus Ethereum supporters. Solana versus Ethereum. Layer ones versus layer twos. The tribal warfare is loud, it is entertaining, and it is mostly beside the point.

While that argument fills the timelines, a different and far more consequential race is being run by people who do not post memes. The United States Treasury and the People’s Bank of China are competing to define what money looks like for the next century. They are doing it in plain sight, in policy documents and central bank press releases, with two completely different theories of the case.

The American theory: extend the dollar’s reach into every digital corner of the global economy by privatizing it, regulating it, and shipping it on open networks. The Chinese theory: build a sovereign digital currency under direct state control, and link it together with friendly central banks into a parallel settlement system that does not need American rails at all.

This is the real race. It will decide whether the global financial system of the 2030s and 2040s stays dollar-denominated and U.S.-administered, or whether it splits into competing blocs with different reserve assets, different settlement rails, and different rules. The stakes are not the price of a token. They are the architecture of money itself.

What the United States is actually doing

The American strategy is easier to miss because it is being run by the private sector with regulatory blessing rather than by a central bank. But the strategy is explicit, and it has been spelled out at the highest levels of the U.S. Treasury.

The instrument is the stablecoin. The framework is the GENIUS Act, signed into law in July 2025. The thesis was stated bluntly by Treasury Secretary Scott Bessent: stablecoins are a way to “extend the dollar’s reach” in decentralized finance and cross-border payments. Crypto commentator Arthur Hayes has put it more starkly. Stablecoins, in his framing, work as on-ramps that redirect offshore liquidity into U.S. Treasury bills. Every USDT or USDC in circulation requires reserves, and those reserves sit mostly in dollar-denominated assets. Tether alone now holds roughly $113 billion in U.S. Treasuries as of Q1 2026. The stablecoin sector, in aggregate, has become one of the largest non-sovereign buyers of U.S. government debt.

This is not an accident. It is the strategy. By making it easy, legal, and trusted to hold a dollar-pegged token on any blockchain in the world, the United States has effectively privatized dollar issuance and shipped it through global crypto networks. A small-business owner in Lagos who takes payment in USDT, a remittance recipient in Manila who saves in USDC, and a Lebanese citizen who holds stablecoins because the local currency is collapsing are each, without knowing it, deepening dollar penetration into their local economies. They are also indirectly financing the U.S. Treasury market.

The numbers are now large. Fiat-backed stablecoin supply crossed $319 billion in April 2026. Adjusted transaction volume hit $10.9 trillion in 2025, with some estimates putting total settlement volume past $33 trillion, more than Visa. Roughly ninety-nine percent of fiat-backed stablecoin value is pegged to the dollar. The euro, the yuan, the yen, and every other currency together account for the remaining one percent. In digital money, the dollar is not winning. It has, so far, lapped the field.

The genius of this approach, from the U.S. perspective, is that it works without the political baggage of a U.S. central bank digital currency. There is no Federal Reserve digital dollar to argue about. There is no surveillance state implication. There is only a regulated private sector building products that happen to pour offshore savings into U.S. debt and pull the global digital economy toward dollar-denominated settlement. The state does not have to build the rails. It just has to make them legal and trusted.

The GENIUS Act is the legal scaffolding. It defines payment stablecoins as a distinct regulated category, requires one-to-one reserve backing in high-quality liquid assets, opens issuance to banks under OCC supervision, and creates a U.S.-supervised path that competes structurally with foreign stablecoins. Tether’s planned U.S. domestic stablecoin launch fits this pattern. So does the Trump administration’s USD1 stablecoin, marketed openly as a “digital dollar for the world.” The U.S. is not building one digital dollar. It is building an entire ecosystem of them, each privately issued, each pushing toward the same outcome.

What China is actually doing

China is running a different play, executed by the state directly and aimed at a different goal.

The e-CNY, the digital yuan, is the world’s largest live central bank digital currency. By late 2025, cumulative transaction value had crossed $2.3 trillion. Twenty-nine pilot cities have integrated it into public transit and retail. 180 million wallets have been created. Domestic adoption still trails Alipay and WeChat Pay, but the gap is closing, and on January 1, 2026, the People’s Bank of China made a structural change that rewrote the asset’s economic logic.

Until that date, the e-CNY was classified as M0, basically digital cash, and could not earn interest. From January 1, 2026, banks are permitted to pay interest on verified digital yuan wallets, and the e-CNY is treated as a deposit-like instrument with commercial banks as counterparties. The currency is now covered by China’s national deposit insurance. In plain language: the e-CNY went from a digital substitute for paper money to a digital substitute for a bank account. The incentive to hold it just got dramatically larger.

That domestic change is half the story. The other half is happening across borders.

Project mBridge, the cross-border CBDC platform jointly developed by the People’s Bank of China, the Bank for International Settlements, and the central banks of Thailand, the UAE, and Hong Kong, processed over $55 billion in transactions by late 2025. The e-CNY accounts for more than 95 percent of mBridge settlement volume. Cross-border e-CNY activity overall reached roughly $2.38 trillion by November 2025, an 800 percent expansion since 2023. China launched its e-CNY International Operation Center in Shanghai in September 2025. Pan Gongsheng, the PBOC governor, has explicitly framed the goal as building “a more multi-polar monetary system less vulnerable to politicization.” It is a polite way of saying: a system the United States cannot weaponize.

The expansion is mapped. The PBOC’s 2026 work plan includes new cross-border pilots with Singapore, Thailand, Hong Kong, the UAE, and Saudi Arabia. A retail e-CNY pilot is now operating in Laos, where Chinese tourists can scan QR codes at participating local merchants and settle directly in digital yuan. The 15th Five-Year Plan (2026-2030) explicitly mandates active participation in international digital-currency governance. A new e-CNY measurement, management, and ecosystem framework took effect on January 1, 2026.

The pattern is consistent. China is building a digital settlement system that is sovereign, state-controlled, interest-bearing, and designed to operate at the edges of its trade and political alliances. It does not need to displace the dollar globally. It needs to offer a credible alternative for the share of the world economy that already does business inside China’s orbit, or that wants the option not to depend on U.S. payment infrastructure. That is a smaller target than “replace the dollar,” and a much more achievable one.

The paradox at the heart of the race

Here is where the story gets interesting, and where most coverage gets it wrong.

The de-dollarization push has not been a clean fight. The BRICS bloc, now expanded with Indonesia and partner status for nations from Belarus to Vietnam, represents close to forty percent of global GDP by purchasing power parity. Russia and China settle around ninety percent of their bilateral trade in rubles and yuan. The dollar’s share of BRICS trade has fallen from 79 percent in 2022 to 58 percent by mid-2025. BRICS Pay and mBridge are building a real alternative payment infrastructure. The political will to escape the dollar is the strongest it has been in decades.

And yet the dollar’s overall position has, on the most important metrics, strengthened.

The Bank for International Settlements’ 2025 Triennial Survey, the most authoritative measure of global currency usage, found the dollar was on one side of 89.2 percent of all foreign exchange transactions in April 2025, up from 88.4 percent in 2022. The renminbi’s share rose to 8.5 percent, a meaningful increase, but still a fraction of the dollar’s. The dollar’s reserve share has dropped gradually, from 72 percent in 2001 to roughly 58 percent in 2026, but the pace is erosion, not collapse.

The paradox is that stablecoins, the very instrument that lets a Russian importer or an Iranian merchant settle a transaction without touching the U.S. banking system, are themselves overwhelmingly dollar-pegged. Ninety-seven percent of the stablecoin market is denominated in dollars. So when a BRICS-aligned exporter in Brazil sells soybeans to a buyer in the UAE and they choose to settle in stablecoins to avoid U.S. correspondent banking, they are still, in effect, transacting in dollars. They have escaped American banks. They have not escaped the dollar.

This is the contradiction at the heart of the de-dollarization movement, and the unstated reason the U.S. is comfortable with stablecoins extending into hostile jurisdictions. Even the workarounds reinforce the system. As Tether’s CEO Paolo Ardoino has argued, stablecoins like USDT reinforce dollar hegemony precisely by offering a decentralized alternative that happens to be dollar-pegged. The political instinct to flee the dollar runs straight into the practical reality that no other currency offers comparable depth, liquidity, or trust.

The economist Brad Setser at the Council on Foreign Relations has flagged a related paradox. U.S. policy that tries to coerce countries into using the dollar, through tariff threats or sanctions, may actually speed up the search for alternatives. The dollar’s strength comes partly from being the path of least resistance. The moment it becomes a path of political compulsion, more actors will pay the cost of building around it.

The Trump administration’s repeated tariff threats against BRICS members for “de-dollarization” arguably did more to motivate alternative-payment-system construction than any Russian or Chinese initiative could have on its own.

So the race is not as simple as U.S. versus China. It is a contest in which the dominant power, the United States, is winning on infrastructure expansion while at the same time creating the political conditions that push counterparties to keep building alternatives. And it is one in which the challenger, China, is building a real, scaled alternative for a narrower slice of the world even as its broader currency, the renminbi, stays structurally constrained by capital controls and limited convertibility.

What the EU and the rest of the world are doing

The two-power framing of “U.S. versus China” is the loudest version of the race, but it is not complete. Two other actors matter.

The European Union has its own model, anchored by the Markets in Crypto-Assets regulation (MiCA), which has been in phased application since 2024. MiCA created a comprehensive licensing regime for stablecoin issuers operating in the EU and is widely considered the most carefully designed regulatory framework of the three. The European Central Bank is also developing a digital euro on a slower timeline, with implementation realistically running into 2027 and beyond. The euro’s share of global FX reserves has actually grown in 2025 as central banks diversify out of dollars, but the eurozone’s structural weakness, a shared currency without a shared treasury, limits how far the digital euro can carry the bloc’s monetary ambitions.

Other CBDC projects are real but smaller. The Bahamas, Jamaica, and Nigeria have launched retail CBDCs with mixed adoption. India’s UPI-linked CBDC pilot is one of the most operationally significant in the developing world. The UK and Japan are advancing slowly on their own digital currency designs. None of these projects threatens the dollar-yuan binary, but several stretch the architecture of state-backed digital money beyond the two superpowers.

The most interesting wildcard is the Global South. Stablecoins, particularly USDT, have quietly become a de facto financial layer in dozens of countries where local currencies are weak or banking is shallow. The 400 million-plus users who now rely on dollar-backed stablecoins are mostly outside the U.S., and many are in jurisdictions where their own governments would, politically, prefer they not use the dollar. The American digital-dollar empire is being built largely by people who do not live in America.

What actually matters from here

Three things to watch over the next two to three years will tell you which way this race is bending.

The first is how the e-CNY’s interest-bearing transition affects cross-border adoption. If digital yuan deposits become an attractive store of value in countries that already do significant trade with China, the dollar’s grip on those corridors weakens. If the transition is mostly a domestic event and the e-CNY remains a thin layer for cross-border trade between China and a handful of allies, the dollar holds.

The second is whether the United States can keep stablecoin expansion uncoupled from political backlash. The Hudson Institute and other Washington policy shops are openly arguing for stablecoin promotion as a counter to BRICS. That framing, useful in policy memos, becomes a liability the moment foreign governments start to see USD-pegged stablecoins as instruments of U.S. strategy rather than neutral infrastructure. The current strategy works because it does not look like a strategy. The moment it does, the political costs of using it rise sharply in target jurisdictions.

The third is the technology layer. The next decade of payments will involve programmable money, AI agents transacting on their own, tokenized real-world assets, and settlement networks that move money in seconds at near-zero cost. The system that wins those use cases at scale wins the next layer of finance. The U.S. has more developer momentum, more capital, and more open networks. China has more state coordination, more captive trade flows, and a willingness to mandate adoption that no democratic system can match. Both edges matter.

What this means in the end

The crypto industry has spent a decade explaining itself to outsiders as a fight between competing technologies. Bitcoin or Ethereum. Proof-of-work or proof-of-stake. Layer one or layer two. Those are interesting debates, and they will continue. But they are debates inside a smaller story.

The bigger story is that two states have realized digital money is now a geopolitical instrument, and they are competing to define what it looks like. The United States is using regulated private stablecoins to spread the dollar at internet speed into the global digital economy. China is using a state-issued, interest-bearing digital currency and a parallel settlement network to build an exit ramp for the share of world commerce that wants one. Every other digital money story is, in one way or another, downstream of those two strategies.

For an investor, the implication is that the assets sitting closest to that geopolitical contest, dollar stablecoin issuers, infrastructure providers, payment rails, on/off-ramp networks, will likely matter more over the next decade than the latest layer-one token battle. For a holder of any cryptocurrency, the implication is that the regulatory environment your asset operates in is being shaped by considerations far larger than crypto itself. The CLARITY Act will pass or not pass partly based on how policymakers read the U.S.-China contest. The GENIUS Act was already passed partly because of it.

For everyone else, the implication is simpler. The future of money is being decided right now, not in white papers or token launches but in central bank press releases and Treasury speeches. The next time you read a thread about whether Bitcoin or Ethereum is the future, remember that both of them will end up settling, on the margin, in dollar-pegged stablecoins or yuan-denominated CBDCs. The interesting question is not which crypto wins. It is which currency?

The race that matters is not Bitcoin versus Ethereum. It is the dollar versus the yuan, in digital form, for the architecture of how money moves for the next hundred years. And it is happening right now, while almost nobody is looking at the right scoreboard.

This article is for informational purposes and does not constitute financial or investment advice. Geopolitical and monetary policy developments evolve quickly; the figures and policy positions described reflect reporting available as of mid-May 2026. Always do your own research.

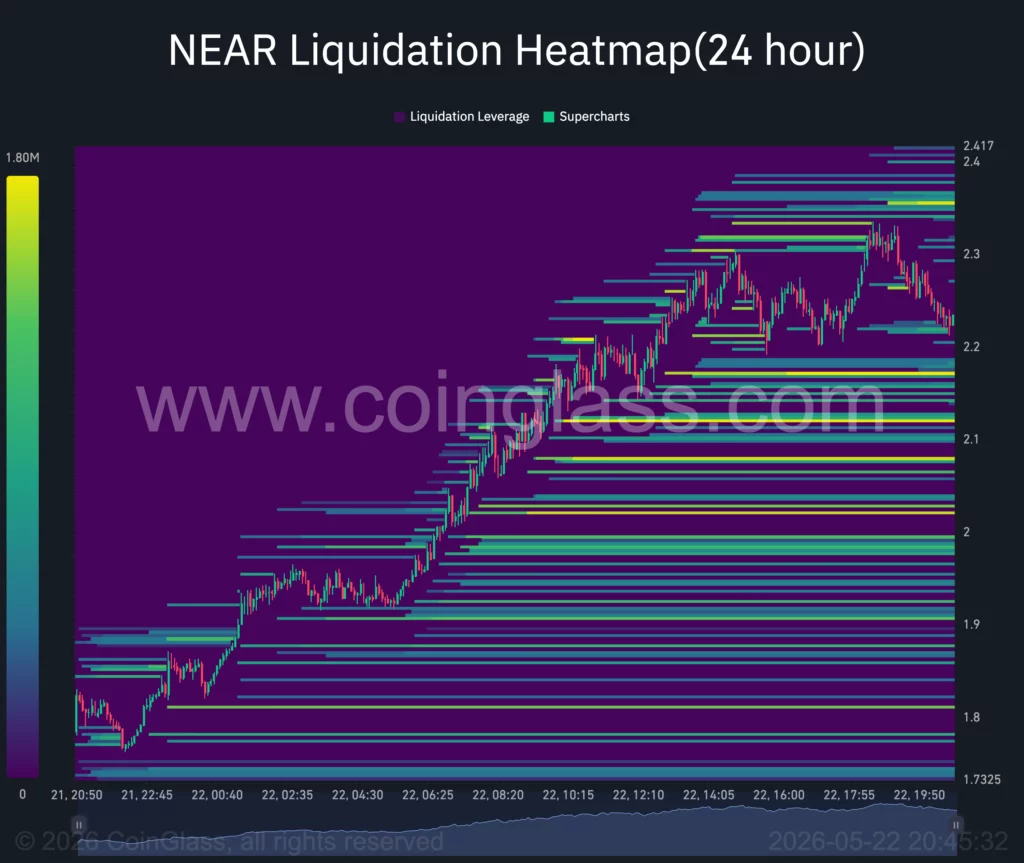

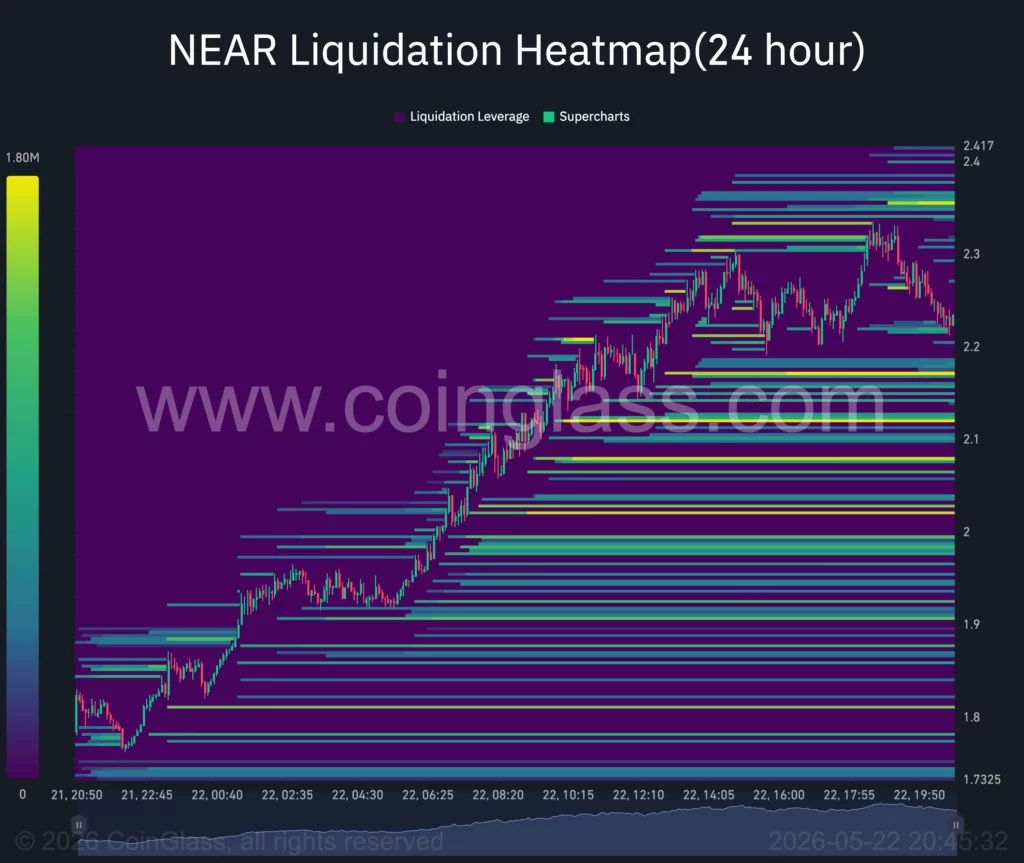

This article was updated with a liquidation heatmap from Coinglass.

NEAR Protocol has rallied more than 44% from its weekly low as AI-driven momentum, protocol upgrade optimism, and aggressive short liquidations pushed the token toward a major technical breakout.

Summary

- NEAR price surged more than 44% from its weekly low as AI narrative momentum, protocol upgrade optimism, and short liquidations fueled a breakout above key resistance levels.

- A potential golden cross between the 50-day and 200-day moving averages has strengthened bullish sentiment, with traders now watching the $3 psychological level.

- CoinGlass data showed dense liquidation clusters above $2.30, while open interest jumped over 51% amid rising leveraged positioning in NEAR futures markets.

According to data from crypto.news, NEAR Protocol (NEAR) climbed from a weekly bottom near $1.47 to an intraday high of $2.10 before extending gains toward the $2.20 region on Thursday. The move came even as Bitcoin (BTC) and Ethereum (ETH) traded within a subdued range following renewed concerns over U.S. inflation and uncertainty surrounding the Federal Reserve’s next policy decision.

A renewed wave of capital rotation into artificial intelligence-linked crypto assets has emerged as one of the key catalysts behind NEAR’s outperformance. Nvidia’s stronger-than-expected quarterly earnings earlier this week reignited speculative demand across AI infrastructure tokens, particularly projects tied to decentralized compute, AI agents, and data privacy.

Adding to the momentum, NEAR AI rolled out an automated Personally Identifiable Information anonymization framework on May 20. The feature strips sensitive user information from prompts before they interact with external large language models, addressing enterprise concerns surrounding data leakage and compliance risks.

Market participants also reacted positively to Network Upgrade 2.13, scheduled for June. The upgrade introduces post-quantum cryptographic signing alongside automated dynamic resharding through NEAR Intents. Developers say the system will allow the network to scale database shards automatically during traffic spikes, potentially reducing congestion and improving institutional-grade throughput.

At the same time, derivatives activity around NEAR accelerated sharply. Data from CoinGlass showed open interest surging more than 63% over the past 24 hours to $629 million while funding rates flipped strongly positive, signaling an aggressive build-up in leveraged long positioning.

Meanwhile, liquidation data from CoinGlass pointed to a significant short squeeze unfolding above the $2 level. Heatmap clusters showed dense liquidation zones stacked between $2.05 and $2.18, many of which were triggered as NEAR pushed through key resistance levels during the rally.

NEAR 24-hour liquidation heatmap. Source: Coinglass.

The latest move also coincided with improving sentiment across the altcoin market following continued inflows into U.S. spot Bitcoin and Ethereum ETFs earlier this week. Although macro conditions remain fragile, ETF demand has helped stabilize risk appetite after several weeks of heavy volatility tied to rising oil prices and geopolitical tensions in the Middle East.

Oil markets remained elevated after ongoing uncertainty surrounding shipping activity near the Strait of Hormuz continued to fuel inflation concerns. Higher crude prices have complicated the Federal Reserve’s path toward rate cuts, with traders now pricing in a prolonged higher-for-longer interest rate environment.

Despite those macro headwinds, several analysts believe AI-linked crypto assets may continue attracting speculative flows independently from the broader market direction. Michaël van de Poppe, founder of MN Consultancy, recently said the AI sector remains “one of the strongest narrative trades” in crypto due to rising institutional interest in decentralized compute infrastructure.

Is a golden cross setting up a larger NEAR breakout?

On the daily chart, NEAR has broken above a descending trendline that had capped price action since late January. The breakout accelerated after buyers reclaimed the Murrey Math 7/8 resistance zone near $2.14, which had previously acted as a key reversal level during multiple failed rallies earlier this year.

More importantly, the 50-day moving average appears close to crossing above the 200-day moving average. A confirmed golden cross would signal the first major bullish trend reversal on NEAR’s daily timeframe since late 2025.

The chart also shows NEAR reclaiming the 4/8 major support and resistance pivot at $1.56 earlier this month before rapidly advancing through the 5/8 and 6/8 Murrey Math zones. Bulls are now attempting to establish support above the 7/8 “weak stop and reverse” level around $2.14.

Should buyers maintain control above that region, the next major upside target sits near the 8/8 resistance zone around $2.34. A breakout above that level could open the door toward the +1/8 overshoot area near $2.53, followed by the +2/8 extreme overshoot level around $2.73.

From a broader structure perspective, reclaiming the psychological $3 level would require sustained momentum beyond the +3/8 reversal zone near $2.93. Notably, NEAR has not traded above $3 on a sustained basis since the sharp correction that followed the AI-token rally earlier this year.

Momentum indicators have also strengthened considerably during the latest breakout. The MACD recently flipped bullish on the daily timeframe while price continues holding firmly above the 50-day moving average, currently positioned near $1.43.

According to CoinGlass liquidation data, another sizable cluster of short liquidations remains stacked between $2.30 and $2.40. A decisive move through that area could trigger another wave of forced buybacks from overleveraged bearish traders.

At the same time, elevated funding rates suggest parts of the market may already be becoming overheated in the short term. Historically, aggressive leverage build-ups following vertical rallies often increase the probability of sharp volatility spikes or temporary pullbacks.

What could invalidate the bullish NEAR thesis?

Although the technical structure has improved significantly, several downside risks remain in play.

A rejection below the $2.14 resistance zone would weaken the immediate breakout thesis and potentially expose NEAR to a pullback toward the $1.95 support region. Losing that level could shift momentum back toward the 5/8 Murrey Math support around $1.75.

Macro conditions also remain a major risk factor for the crypto market. Another upside surprise in U.S. inflation data or further escalation in Middle East tensions could strengthen the U.S. dollar and pressure risk assets, particularly high-beta altcoins.

Meanwhile, Bitcoin’s inability to reclaim major resistance levels continues limiting broader altcoin participation. A sharp correction in BTC below key support zones could quickly erase speculative momentum across AI-linked tokens, including NEAR.

Derivatives positioning presents another concern. While rising open interest and positive funding rates initially supported the rally, excessively crowded long positioning increases liquidation risk if momentum stalls. In such scenarios, cascading long liquidations often amplify downside volatility.

For now, however, NEAR remains one of the strongest-performing large-cap altcoins in the market, with traders closely watching whether the approaching golden cross and sustained AI narrative momentum can eventually fuel a move back toward the $3 psychological level.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Intercontinental Exchange and OKX are teaming up to list perpetual oil futures that track ICE Brent and WTI benchmarks on the crypto exchanges derivatives platform.

Summary

- ICE will license its Brent and WTI futures prices to support new perpetual oil contracts on OKX in selected markets

- The move follows ICE’s investment that valued OKX at 25 billion dollars and gave the NYSE owner a board seat

- Oil perps mirror a fast growing niche pioneered by platforms like Hyperliquid, where WTI linked perpetuals have seen volumes jump to 7.3 billion dollars

- The initiative blurs lines between traditional commodities and crypto derivatives as CME and ICE push regulators to rein in offshore oil perps while testing their own 24/7 models

The owner of the New York Stock Exchange will provide its regulated futures prices for ICE Brent crude and West Texas Intermediate as the reference curve behind the new contracts, while OKX handles the perpetual structure, crypto margin and user distribution.

The contracts will reference the same benchmarks that underlie multi trillion dollar cleared futures on ICE, according to Bloomberg, but will be listed as non expiring swaps on OKX’s venue with funding payments to keep prices aligned with the underlying oil curves.

For now the trading will be limited to jurisdictions where OKX already has permission to offer perpetual futures, which means the products are likely to launch outside the United States even as ICE markets them to institutions used to regulated commodity exposure.

That split structure allows ICE to monetise its benchmark data and deepen a 25 billion dollar strategic tie up with OKX without immediately seeking US approval for 24 hour oil perps on its own exchanges.

The deal sits on top of a broader partnership under which ICE took a minority stake in OKX, secured a board seat and agreed to license its US futures and tokenised equities markets back into the crypto exchange, which serves more than 120 million accounts.

Under that March agreement ICE plans to launch US regulated crypto futures based on OKX spot prices while OKX in turn expects to offer access to ICE’s US futures suite and New York Stock Exchange linked tokenised stocks once regulators sign off.

Will OKX and ICE’s 24/7 oil perps redraw the line between Wall Street and crypto?

Market observers see the oil perpetuals as a logical extension of that blueprint, inserting real world commodities into a crypto native leverage and funding model that retail traders already use for Bitcoin (BTC) and Ethereum (ETH) exposure on OKX’s derivatives books.

For readers tracking large cap assets, Bitcoin and Ethereum prices, liquidity conditions and derivative flows are already covered in depth on dedicated pages at crypto news, which provide context for how new products like oil perps can bleed into broader digital asset volatility and funding markets.

What does this mean for crypto and commodity regulation

The move lands in the middle of a political and regulatory fight over whether perpetual futures on US linked commodities should be allowed for American users at all, and if they are, who should host them.

CME and ICE have pushed US officials to crack down on platforms like Hyperliquid that list WTI linked perps for global users with little classical oversight, framing the issue as a question of market integrity and surveillance rather than a pure turf war.

At the same time both exchanges are nudging regulators toward a world of 24 hour trading, with ICE’s NYSE working on a tokenised securities platform funded by stablecoins and designed for round the clock access that looks very similar in structure to the crypto venues they are publicly criticising.

In that context the OKX deal reads less like a sideline experiment and more like a live test case for hybrid market structure.

ICE supplies regulated benchmarks and governance while OKX contributes the perpetual engine, user interface and experience running high leverage derivatives with up to 125 times leverage in some markets.

If regulators tolerate oil perps tied to regulated benchmarks offshore, it strengthens the case for bringing similar products onshore in a controlled way; if they clamp down, the episode will underline how far commodity regulators are willing to go to keep price discovery anchored in listed futures rather than in offshore crypto contracts.

One person familiar with the thinking told Bloomberg that a large energy trading firm put it bluntly, saying that traders “want the same benchmarks and margin offsets they already use at ICE, but with the flexibility of crypto style funding and around the clock risk management,” a view that captures the logic behind the tie up even as the regulatory path remains uncertain.

For readers looking to understand how this clash between traditional derivatives and digital assets is evolving beyond oil, detailed coverage of Bitcoin markets, Ethereum staking and the rise of perpetual futures across major coins is available on crypto news, including explainers on how funding rates, open interest and cross margining can transmit stress between commodity perps and large cap crypto contracts.

Those dynamics matter because an oil shock expressed through leveraged perps can now move through balance sheets that also hold Bitcoin or Ethereum collateral, tightening the coupling between energy and crypto in ways that macro traders and regulators will have to model rather than ignore.

“We are seeing the convergence of two infrastructures that used to live in separate universes,” said a derivatives strategist at a European prop firm who asked not to be named because they are not authorised to speak publicly. “If you clear oil futures at ICE during the day and trade perpetuals on OKX at night, that is one risk system, not two.”

Germany’s Finance Committee has rejected a proposal from the Green Party to scrap the country’s tax exemption for cryptocurrencies held longer than one year.

Summary

- Germany’s Finance Committee rejected a Green Party proposal to end the country’s one-year crypto tax exemption for long-term holders.

- CDU/CSU, AfD, and SPD lawmakers opposed the measure for different reasons, while only Die Linke backed the proposal with reservations.

- Finance Minister Lars Klingbeil has separately signaled plans to revise crypto taxation by 2027 as Germany expands oversight under EU reporting rules.

According to the committee discussions, lawmakers from multiple parties opposed the measure for different reasons, leaving Germany’s existing crypto tax framework intact even as Berlin weighs new digital asset tax rules for 2027.

Under current German law, profits from Bitcoin and other cryptocurrencies remain free from capital gains tax if investors hold the assets for more than 12 months. The rule, commonly referred to as the “Haltefrist,” has helped Germany build a reputation as one of Europe’s more favorable jurisdictions for long-term crypto investors.

The proposal from Bündnis 90/Die Grünen argued that the exemption no longer fits the modern financial market because it was originally designed for physical valuables such as gold, antiques, or foreign currency holdings rather than digital assets. Green lawmakers cited research from the Frankfurt School Blockchain Center estimating that Germany could collect up to 11.4 billion euros, or about $12.9 billion, in additional yearly revenue from crypto taxation.

At the same time, the party used a lower estimate in its own fiscal calculations, saying conservative assumptions would still generate billions in extra state revenue.

Why did German parties reject the crypto tax proposal?

Opposition to the bill extended across much of Germany’s political spectrum. Members of the CDU/CSU argued the proposal would create fresh inconsistencies because cryptocurrencies would end up taxed differently from comparable assets such as precious metals and foreign currencies.

Meanwhile, the AfD criticized the measure from a broader tax policy perspective. Party representatives said Germany should reduce taxation instead of expanding it and argued the government should focus public spending on areas including domestic security, foreign policy, and the judicial system.

The SPD took a more cautious position, saying that while the party supports tighter crypto taxation in principle, it would wait for Finance Minister Lars Klingbeil to present a formal federal proposal before backing specific legislative changes.

Klingbeil had already signaled possible reforms in April while presenting Germany’s 2027 federal budget. During that presentation, the finance minister said the government planned to “tax cryptocurrencies differently” as part of measures expected to raise an additional 2 billion euros in revenue.

Only Die Linke supported the Greens’ proposal outright, though the party also pointed to weaknesses in the draft legislation. Representatives warned that the bill lacked clear limits on offsetting crypto trading losses and said the administrative burden could significantly reduce net tax gains.

How is Germany’s crypto industry responding?

Industry groups and crypto firms have continued defending Germany’s current one-year exemption. Robin Thatcher, a Bitcoin and crypto tax accountant, said removing the rule would weaken Germany’s position as a crypto hub and discourage investment activity.

Comparisons with Austria have also entered the debate. Austria removed its crypto holding exemption in 2022 and introduced a flat 27.5% capital gains tax on digital assets regardless of holding duration.

Bitpanda co-founder Eric Demuth later criticized the Austrian model, saying in a March post on X that the changes created additional bureaucracy without delivering meaningful financial benefits to the government.

Despite the policy uncertainty, German banks have continued expanding into regulated crypto services. Earlier this year, DZ Bank received BaFin approval to launch its “meinKrypto” platform under the European Union’s Markets in Crypto-Assets Regulation framework.

The service allows customers from hundreds of cooperative banks to trade assets, including Bitcoin, Ethereum, Litecoin, and Cardano, directly through their banking applications.

In a development marking the culmination of a high-profile U.S. fraud probe tied to Celsius Network’s 2022 collapse, the criminal proceedings surrounding key former executives have officially ended. The sentencing of Roni Cohen-Pavon to time served and the closure of cases against Cohen-Pavon and former Celsius CEO Alex Mashinsky were reflected in the Southern District of New York docket on Thursday. These closures come after Mashinsky pleaded guilty and received a 12-year prison term for fraud and price manipulation, while authorities indicated Cohen-Pavon’s cooperation provided substantial assistance that likely contributed to a lenient outcome.

According to Cointelegraph, the broader 2022 Celsius collapse left users with estimated losses totaling around $5 billion. The formal wrap of the criminal phase in this matter represents a notable checkpoint for regulatory enforcement actions within the crypto lending sector and for victims seeking accountability in high-profile crypto firm failures.

Key takeaways

- The Celsius criminal docket has been formally closed following sentencing actions against Roni Cohen-Pavon (time served) and Alex Mashinsky (12-year sentence), signaling an enforcement milestone in the Celsius saga.

- Mashinsky’s plea and sentencing, alongside Cohen-Pavon’s cooperation acknowledgment, illustrate how cooperation can influence outcomes in complex crypto-related prosecutions.

- Justin Sun’s voluntary dismissal of his Bloomberg lawsuit “without prejudice” ends that particular dispute, while the broader WLFI-related defamation suit persists against him.

- The AI16Z DAO matter advances to a federal setting, with a class-action alleging market manipulation tied to the ELIZAOS rebrand on Solana, highlighting ongoing regulatory attention to AI-token projects and branding disclosures.

Closure of Celsius cases and enforcement context

The Celsius cases sit within a broader pattern of U.S. enforcement activity targeting misrepresentation and manipulation within crypto markets. Mashinsky’s conviction for fraud and price manipulation underscores prosecutors’ focus on the governance and marketing practices of crypto lenders and the potential impact on retail investors. Cohen-Pavon’s case, cited by authorities as involving “substantial assistance,” reflects a common prosecutorial approach in complex financial schemes where cooperation can shape sentencing outcomes. The public record now shows the criminal dockets related to Celsius’ 2022 collapse fully closed, a development with implications for victims, market participants, and compliance professionals monitoring enforcement trends in the sector.

The milestone reinforces the emphasis regulators place on investor protection, traceability of misstatements, and the credible disclosure of material information in crypto-enabled businesses. Institutions and exchanges assessing risk profiles may look to this closure as a reference point for due diligence and remediation practices in similar high-stakes cases, particularly where alleged fraud intersects with sophisticated financial products and tokenized offerings.

Sun vs. Bloomberg: privacy, disclosure, and data-use risk

In a separate development, Justin Sun, founder of Tron, moved to dismiss his lawsuit against Bloomberg News without prejudice, terminating the matter on Tuesday. The case, originally filed in August 2025, alleged that Bloomberg had publicly disclosed proprietary financial information related to Sun’s cryptocurrency holdings. The dispute arose after Bloomberg approached Sun’s team in February 2025 to obtain wealth data for inclusion in its Billionaires Index, with Sun contending that Bloomberg’s reporting exposed him to threats such as kidnapping and phishing.

The voluntary dismissal—compelled by a lack of ongoing docket activity—leaves open, at least for now, the possibility of later action, though no immediate resolution was announced. The episode sits at the intersection of data privacy, media reporting, and regulatory expectations around the handling of sensitive financial information related to crypto executives. It also touches on cross-border considerations, given Sun’s status as a global entrepreneur and the multinational nature of media coverage and legal proceedings in this arena.

Beyond this suit, Sun remains involved in other litigation, including a defamation case brought by World Liberty Financial, alleging that Sun’s public statements caused reputational harm. Separately, Sun has challenged actions involving WLFI tokens, signaling a broader pattern of disputes arising from tokenized holdings and corporate disclosures within crypto ecosystems.

AI16Z DAO: class-action scrutiny of AI-token markets and branding