Crypto World

Will Solana price crash now that it has charted a bearish flag pattern?

Solana price tanked over 7% on Monday as fears of the impact of the ongoing U.S.-Iran war continued to drive investors away from risk assets. Current technical signals suggest the token could be set for a downturn.

Summary

- Solana price has remained in a downtrend as network revenue declined amidst a market-wide downturn.

- A bearish flag pattern has positioned the token for more downside.

According to data from crypto.news, Solana (SOL) price fell 7% from $88.05 on Sunday to an intraday low of $81.86 on Monday, March 2. Subsequently, it attempted a breach of the $90 resistance supported by a broader market recovery, but the rally lost steam just below that mark.

On the monthly timeframe, Solana has fallen over 30%, and is down over 44% from this year’s highs.

Solana price has remained in a downtrend as network revenues have fallen. Notably, the weekly revenue generated by the Solaba network has dropped over 30% from what was recorded during mid January, data from DeFiLlama show.

The total value locked in the network has also fallen from over $9 billion recorded on Jan. 17 to $6.64 billion at the time of writing.

With both network revenue and TVL going down, investors are concerned that Solana’s explosive growth phase is over, and the memecoin fever that fueled the network is finally breaking.

Demand for the token across the derivatives market has also contributed to the downturn. Data from CoinGlass show that SOL futures open interest has scaled back by nearly 45% to $4.93 billion from its January high of $8.88 billion as traders unwind positions awaiting signs of more calmness in the global geopolitical landscape.

Solana price is also affected by the market-wide downturn in response to the ongoing U.S.-Iran conflict, which has pushed investors away from risk assets to more traditional alternatives, as they expect more volatility over this week.

The most recent trigger came after the retaliatory attack from Iran on U.S. ships over the weekend, stationed around the Strait of Hormuz, sparking a jump in oil prices. Investors are concerned this could lead to higher inflation in the U.S., which could likely force the Fed to hike interest rates or hold them steady at restrictive levels for longer.

Risk-assets like Solana tend to benefit from interest rate cut expectations and struggle when the Fed sets a hawkish tone.

On the daily chart, Solana price has formed a bearish flag pattern since the token entered a downtrend from mid January this year, before moving into consolidation over the past few weeks. Bearish flags have typically been precursors to further downward breakouts.

Other technical indicators also favour the bears. The Supertrend has flashed red while the Aroon lines have pointed downwards, with the Aroon Down at 50%, indicating that sellers still maintain firm control of the market.

Hence, Solana price risks dropping to the Feb. 6 low of $70 if the current bearish momentum prevails, especially considering the broader downturn.

On the contrary, a rebound above $90, a resistance level that the token has struggled to break multiple times over the past few weeks, could offer the necessary optimism for a rally towards the $100 psychological resistance level.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Mastercard is quietly upgrading its payments back-end by testing the use of regulated stablecoins to settle card transactions. The pilot, conducted in collaboration with SoFi Technologies and its Galileo platform, aims to move settlement between banks off traditional rails and onto digital dollars, while keeping the consumer checkout experience unchanged at the point of sale. The initiative centers on SoFiUSD, a dollar-backed stablecoin issued by SoFi Bank, N.A., and is positioned within Mastercard’s broader Multi-Token Network (MTN) vision for tokenized money.

As the industry watches the evolution of stablecoins from crypto-native instruments to mainstream settlement rails, Mastercard’s approach signals a strategic pivot: the networks that power card payments may increasingly rely on regulated digital assets to clear and settle transactions faster and with greater liquidity efficiency. The company’s plan also places it in a competitive stance with Visa, which has already piloted stablecoin-backed settlement capabilities for cross-border transfers and merchant payouts.

Key takeaways

- Mastercard is testing stablecoin-backed settlement, aiming to streamline the post-transaction clearing process across its global network.

- SoFi Bank, N.A. will use SoFiUSD to settle Mastercard credit and debit transactions; Galileo Financial Technologies will enable other banks and fintech issuers to participate in stablecoin settlement through Mastercard’s system.

- The initiative targets back-end settlement rather than altering the consumer payment experience, preserving the familiar card workflow at checkout.

- Mastercard’s Multi-Token Network is designed to support multiple forms of tokenized money, including stablecoins, tokenized deposits, and digital representations of fiat currencies.

- Regulatory clarity and cross-border liquidity considerations remain pivotal as stablecoins move toward mainstream financial infrastructure; market data in 2026 show a growing stablecoin sector with substantial transaction volumes ahead.

Back-end settlement reimagined

Behind the scenes, Mastercard’s approach reframes how settlement between issuing and acquiring banks could occur. When a consumer initiates a card payment, the traditional flow involves authorization, recording, merchant confirmation, and later settlement through standard banking channels. The new model concentrates settlement on the back-end, potentially using a regulated stablecoin such as SoFiUSD to fulfill the investment obligations between banks, rather than relying solely on fiat transfers.

Under this structure, a typical transaction would proceed as usual at the point of sale, but when the time comes to settle the obligation between the issuer and the acquirer, a stablecoin-based transfer could be executed. Stablecoins operate on blockchain infrastructure, offering the possibility of around-the-clock settlement that is not constrained by conventional banking hours. If successful, this could reduce settlement latency and improve liquidity management for financial institutions involved in card networks.

How stablecoin settlement would operate

In a practical sense, the workflow might look like this: a customer pays with a card in their local currency; Mastercard determines the net settlement obligation between the issuing bank and the acquiring bank; instead of exclusively relying on traditional rails, both parties could settle using a regulated stablecoin like SoFiUSD through the Mastercard system. SoFiUSD is issued by a federally regulated bank and is described as backed by cash reserves on a 1:1 basis, positioning it closer to bank-issued digital money than to a crypto-native asset.

Such a model aligns with a broader trend toward programmable, low-latency settlements that can cross borders and operate outside standard banking hours. While the user experience remains unchanged for the consumer, the underlying transfer of value between institutions could become more fluid and resilient in digital form.

MTN: A multi-token vision for payments

The backbone of this initiative is Mastercard’s Multi-Token Network, which is intended to support multiple forms of tokenized money. By bridging traditional financial rails with tokenized assets, MTN aims to create a versatile settlement ecosystem that can accommodate regulated digital currencies alongside conventional money. In theory, this could enable quicker cross-border movements, enhanced liquidity management, and greater interoperability between banks, card networks, and digital-asset infrastructure—without sacrificing regulatory compliance.

Why this matters for regulators, issuers, and users

Stablecoins have moved from niche crypto tools to a focal point of mainstream payments strategy. The appeal lies in their potential for fast, low-friction transfers and programmable payments, which could transform how businesses manage cash flows and how cross-border settlements operate. SoFi USD’s status as a dollar-backed instrument issued by a regulated bank is intended to help ease regulatory concerns, offering a more familiar framework for financial institutions wary of unbacked crypto exposure.

According to recent data, the stablecoin market has grown substantially. As of March 2026, the market’s total value stood around $314 billion, according to DefiLlama, reflecting growing adoption and increasing scale. The year 2025 also saw record activity, with monthly stablecoin transaction volumes approaching the trillions and market participants projecting that volumes could surpass $1 trillion per month by late 2026. These indicators help explain why payment networks are exploring stablecoin settlement as a means to improve efficiency and resilience in a rapidly digitizing ecosystem.

Competition and regulatory horizons

Mastercard is not alone in pursuing stablecoin-enabled settlement. Visa has already expanded its own stablecoin settlement capabilities, including cross-border transfers and merchant payout scenarios using tokenized dollars. This competitive dynamic underscores a broader shift in how the largest card networks view the future of payments: not as a replacement for traditional rails, but as an augmentation that leverages digital assets under a regulated umbrella.

Regulation remains a central determinant of how quickly and widely these innovations can be adopted. Banks and payment networks require clarity on issues such as reserve security, consumer protections, cross-border compliance, and interoperability with various blockchain ecosystems. SoFiUSD—issued by a chartered US bank—offers a regulatory-inclined path that other institutions may find more palatable as pilots scale.

Challenges on the path to wider adoption

Despite the promise, several barriers could temper the pace of adoption. Integration complexity for banks and payment processors stands out as a practical hurdle, along with regulatory variance across jurisdictions. Liquidity management between fiat and digital assets, and achieving seamless interoperability across different blockchains and legacy financial networks, are additional technical and operational considerations. Importantly, for most consumers, the transition will be invisible at the point of sale; the benefit will be measured in faster, more predictable settlement behind the scenes.

Broader implications for the payments landscape

Mastercard’s move fits into a wider evolution in digital payments. Stablecoins are increasingly seen as infrastructure components for remittances, business-to-business payments, treasury operations, and even stablecoin-linked card programs. If the current testing proves robust, card networks could evolve into hybrid ecosystems that blend traditional rails with blockchain-enabled settlement, delivering speed and efficiency without disrupting the familiar checkout experience.

Ultimately, the timing and scale of this transition will hinge on regulatory clarity, cross-border cooperation, and the ability of banks and issuers to integrate stablecoin settlement into complex, high-volume networks. The coming quarters are likely to reveal pilots, partner churns, and potentially early live deployments that will indicate how far such a back-end upgrade can take mainstream payments.

For investors and builders, the key takeaway is that stablecoins are moving from theory to execution within major payment rails. The attention now shifts to how regulators respond, how smoothly banks can onboard into MTN-enabled workflows, and how quickly other issuers and networks adopt similar back-end settlement architectures.

Watch closely for updates on pilot outcomes, regulatory milestones, and any additional partnerships that broaden the set of stablecoins approved for settlement across major networks. The next phase will reveal whether this is a scalable blueprint for faster, more resilient payments or a pilot with limited reach.

Digital asset investment products recorded $1.4 billion in net inflows last week, marking the strongest weekly total since January, according to CoinShares.

Summary

- Crypto investment products recorded $1.4 billion in inflows, the strongest weekly total since January this year.

- Bitcoin led with $1.116 billion, while Ethereum posted $328 million in weekly inflows globally.

- Total assets under management reached $155 billion as US-based products drove most fund demand.

Meanwhile, the latest reading also extended the streak of positive flows to three consecutive weeks. CoinShares said total assets under management rose to $155 billion during the period.

Weekly flows accounted for 0.91% of total assets under management, which the report described as the highest weekly intensity seen so far this year.

Bitcoin investment products attracted the largest share of the new money. CoinShares reported that Bitcoin funds recorded $1.116 billion in inflows last week, lifting year-to-date inflows to $3.1 billion.

The report said Bitcoin’s move above $76,000 during the week helped support market sentiment. CoinShares linked the stronger flows to improving risk appetite as ceasefire extension talks between the US and Iran continued. It also said March CPI data appeared to have had limited effect on investor positioning.

Additionally, Ethereum investment products posted $328 million in inflows, their strongest weekly result since January. That lifted Ethereum’s year-to-date inflows to $197 million and added to signs of improved demand for the asset.

At the same time, short-Bitcoin products saw just $1.4 million in inflows. This showed that some hedging demand remained in the market, but the scale stayed limited compared with the flows going into long digital asset products.

Regional flows show broad demand with one exception

The United States accounted for most of the weekly inflows. CoinShares said US-based products brought in $1.5 billion during the week, making the country the clear driver of global fund activity.

Germany also recorded positive flows, with $28 million in inflows. Switzerland moved in the opposite direction, posting $138 million in outflows. CoinShares said this was the largest outflow from Switzerland since November and stood out against the broader risk-on trend in digital asset markets.

Other assets posted weaker results than Bitcoin and Ethereum. The report said XRP and Solana products recorded outflows of $56 million and $2.3 million, respectively. Even so, the broader market picture remained positive as total weekly inflows reached their highest level in months.

Crypto World

Bitcoin (BTC) price drops from recent highs as traders watch CME gap, Kelp fallout: Crypto Markets Today

The crypto market is trading back in familiar territory following a short-lived spike to its highest point since early February on Friday.

Bitcoin is trading a hair under $75,000 while ether (ETH) is at $2,300, both significantly lower than Friday’s highs of $78,300 and $2,460.

One reason for traders to be bullish is that the bitcoin futures market on the CME, a venue favored by institutions, closed at $77,540 on Friday and opened at $74,600 to create “CME gap” that spans 3.8% to the upside. A similar gap occurred last week and was filled before the end of the day on Monday.

The first steps have been taken: Bitcoin’s gained 1.5% since midnight UTC, suggesting sentiment is warming following a volatile weekend.

The market tumbled over the weekend as shipping through the Strait of Hormuz came to a halt after opening on Friday. The renewed closure led to a jump in the price of crude oil from $78 to $88 per barrel.

This weighed on risk assets, with Nasdaq 100 and S&P 500 futures both down by 0.59% since midnight.

Derivatives positioning

- Marketwide, crypto open interest (OI) held steady near $120 billion over the past 24 hours. Trading volume, in contrast, jumped 30%, suggesting a surge in activity without a corresponding increase in new positions. That potentially points to increased turnover, short-term positioning or traders rotating risk rather than deploying fresh capital.

- OI in solana (SOL), bitcoin , ether (ETH) and XRP (XRP) held largely steady. OI in HYPE futures declined by 3% alongside as the price fell, pointing to capital outflows. Elsewhere, OI in AVAX and SP 500 perpetuals rose by 6% to 10%, respectively.

- OI in AAVE futures surged to a record high of 3.46 million tokens as collateral damage from the weekend exploit of KelpDAO led to rapid withdrawals of from the Aave lending platform.

- Funding rates tied to BTC, ETH and several other tokens flipped negative, indicating a bias for short positions that would benefit from a price drop in these tokens.

- BTC and ETH options on Deribit continue to trade pricier than calls in a sign of lingering downside concern.

- Block flows featured bias for BTC call spreads, which are directional bets, and ether straddles, a volatility play.

Token talk

- The altcoin sector was rocked by a $292 million exploit of Kelp DAO’s rsETH token over the weekend, leading to contagion risks across the DeFi market.

- Total value locked (TVL) on Aave dropped from $26.5 billion to $17.5 billion as a result, with the exploit sparking fears of bad debt hitting Aave’s WETH pool, triggering heavy withdrawals and a liquidity crunch.

- Aave’s token, AAVE, rose 2.2% on Monday after tumbling 22% on Saturday.

- The bitcoin-dominant CoinDesk 20 (CD20) Index advanced 1% on Monday, outperforming the altcoin-weighted CoinDesk 80 (CD80) and the DeFi Select Index (DFX), which are up by 0.6% and 0.9%, respectively.

- One particularly volatile token is celestia (TIA), which remains 3.9% down over the past 24 hours even after surging by more than 4% since midnight.

- CoinMarketCap’s “Altcoin Season” indicator is at 36/100, demonstrating investor preference for bitcoin following Friday’s short-lived breakout.

In crypto, “tokenomics” is often presented as a rigorous branch of economics—complete with charts, emission schedules, vesting cliffs, and supply-and-demand models that look convincing at first glance.

But beneath the polish, many token models rely less on economic fundamentals and more on narrative engineering. In other words, tokenomics is frequently storytelling… supported by charts that make the story feel real.

This article breaks down three common structural patterns that appear across many token systems.

1. Future Users Funding Current Rewards

One of the most widespread design patterns in token economies is the implicit assumption that future participants will fund today’s rewards.

At first, this appears sustainable:

- Early users provide liquidity or activity

- They are rewarded with tokens

- The system grows through adoption

But in many cases, the mechanism quietly depends on continuous inflows of new participants to absorb token emissions.

This creates a structural loop:

- Early users earn rewards in newly minted tokens

- Those tokens require new demand to maintain value

- New users enter and effectively “pay” for earlier rewards through dilution or capital inflow

The model works—until it doesn’t. Sustainability is not driven by productivity or revenue, but by a steady expansion of participants willing to buy into the system.

A more honest framing would be:

“This system rewards early activity using future demand that must continuously materialize.”

2. Artificial Scarcity Narratives

Scarcity is one of the most powerful economic concepts in human behavior. Tokenomics often leverages this psychology heavily.

However, not all scarcity is equal.

Many token models rely on engineered scarcity narratives, such as:

- Fixed maximum supply figures

- Burn mechanisms with limited real impact

- Vesting schedules framed as “supply control.”

- Staking lockups presented as a reduced circulating supply

On paper, these mechanisms create the impression of limited availability. In practice, scarcity is often temporarily cosmetic, because:

- New emissions continue through staking rewards or incentives

- Locked tokens eventually unlock

- Burns are sometimes offset by ongoing issuance

- Governance can modify supply rules over time

The result is a paradox:

Scarcity is advertised as structural, but behaves as conditional.

A simple way to think about it:

If supply can expand when incentives require it, scarcity is not a constraint—it is a design choice.

3. Emissions Repackaged as Yield

Perhaps the most misunderstood element of tokenomics is “yield.”

Many protocols advertise attractive APYs, staking rewards, or liquidity incentives. These are often interpreted as “returns,” similar to dividends or interest.

In reality, a large portion of these rewards comes from token emissions, not revenue generation.

This means:

- New tokens are created

- They are distributed to participants

- The system does not necessarily generate external cash flow to support them

So where does the yield come from?

In many cases:

- From the dilution of existing holders

- From speculative inflows required to sustain the token value

- From temporary incentive budgets designed to bootstrap activity

This creates a subtle reframing:

Emissions are not profit. They are redistribution mechanisms.

Calling emissions “yield” is less financial engineering and more linguistic packaging. It transforms dilution into something that sounds like income.

Why the Charts Still Work

If these structures are fragile, why do tokenomics models still convince people?

Because they are visually compelling.

Token charts typically include:

- Emission curves that slope downward over time

- Supply caps that suggest finality

- Reward schedules that appear mathematically precise

- Growth projections that assume continued adoption

These visuals create a sense of inevitability. The design implies that if you understand the chart, you understand the system.

But charts are not guarantees—they are assumptions made visual.

And assumptions can be optimistic, conservative, or conveniently selective.

The Core Truth Behind Most Token Models

Stripped of narrative, many token systems rely on three foundational beliefs:

- There will always be new participants

- Demand will eventually outpace emissions

- Incentives today will generate value tomorrow

If even one of these assumptions fails, the entire structure can shift from growth model to liquidity extraction mechanism.

That doesn’t mean all tokenomics are flawed. Some systems do evolve into real fee-generating, utility-driven economies.

But it does mean a healthy level of skepticism is warranted when:

- Yield looks unusually high

- Scarcity feels overly emphasized

- Sustainability depends heavily on continued inflows

Final Thought

Tokenomics is not just math—it is narrative design wrapped in economic language.

And like all narratives, it can be powerful, persuasive, and occasionally misleading.

Or, as a more blunt summary would put it:

If the system needs constant new believers to keep existing rewards meaningful, it’s less a financial model—and more a story that hasn’t hit its final chapter yet.

REQUEST AN ARTICLE

The petrodollar system, a global financial arrangement in which most international oil trade is priced and settled in US dollars, faces growing threats amid the US-Iran war.

Under this system, countries that import oil must hold US dollars to pay for it, creating a constant global demand for the currency and reinforcing its role as the world’s dominant reserve currency.

Petrodollar System Faces Mounting Pressure Amid Gulf Disruptions

According to The Wall Street Journal, the United Arab Emirates has initiated discussions with the United States over a potential financial safety net amid escalating risks from the Iran conflict.

Officials said Central Bank Governor Khaled Mohamed Balama raised the possibility of a currency swap line in meetings with Treasury Secretary Scott Bessent and Federal Reserve officials in Washington.

The talks come as the conflict has disrupted Emirati energy infrastructure and constrained oil exports through the Strait of Hormuz, limiting dollar inflows.

While the UAE has not made a formal request, officials framed the discussions as precautionary. Nonetheless, they also noted that US military action against Iran “entangled their country in a destructive conflict whose effects may not be over.”

“Emirati officials told the US officials that if the UAE runs short of dollars, it may be forced to use Chinese yuan or other countries’ currencies for oil sales and other transactions, some of the officials said. In that scenario is an implicit threat to the US dollar, which reigns supreme among global currencies, partially because of its near-exclusive use in oil transactions,” the WSJ reported.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

In parallel, alternative settlement practices have already emerged. Reports indicated that, in early April, Iran was charging commercial vessels transit fees through the Strait of Hormuz in yuan.

“While it is unclear how many vessels have made payments in yuan, at least two had done so as of March 25,” Al Jazeera reported, citing Lloyd’s List.

Tehran had also signaled plans to extend these measures to digital assets, including levying Bitcoin-based tanker transit fees as part of a broader effort to bypass traditional financial channels.

All of these developments point to a growing structural threat to the petrodollar system. However, pressure on the system predates the current conflict.

Deutsche Bank noted that US sanctions on oil exports from Russia and Iran had already led to parallel trading networks that increasingly rely on non-dollar currencies, such as the Chinese yuan.

Yuan Shift Could Challenge Dollar’s Dominance

Previously, several experts raised concerns about the dollar’s dominance. Bridgewater founder Ray Dalio warned that failing to secure Hormuz could sharply raise the risks to the dollar’s reserve status.

Similarly, Balaji Srinivasan argued that an Iranian victory could accelerate the end of multiple geopolitical and financial eras, including the petrodollar system.

Meanwhile, Harvard economist Kenneth Rogoff projects that the Chinese yuan could emerge as a global reserve currency within five years, citing growing investor demand to diversify away from the US dollar.

Follow us on X to get the latest news as it happens

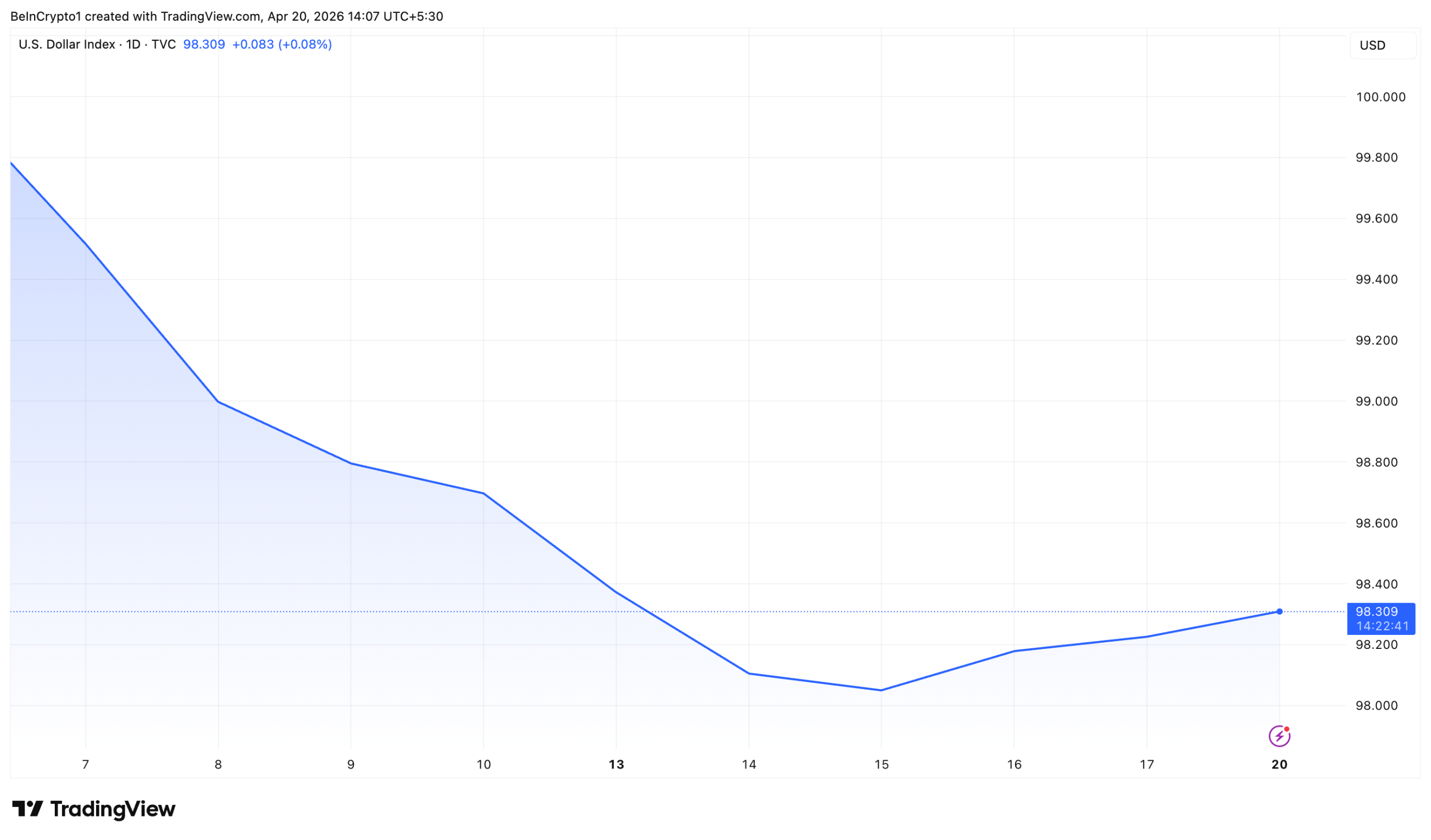

Despite these long-term concerns, short-term market dynamics continue to offer intermittent support to the dollar. The dollar index dropped nearly 2% between April 7 and 15 after the US-Iran ceasefire announcement.

However, renewed uncertainty around the war pushed oil back up, reviving the petrodollar effect.

For now, geopolitical tensions are sustaining the petrodollar’s relevance. Yet, structural shifts beneath the surface raise questions about its long-term durability.

The post Petrodollar System Faces 3 Threats as Yuan Challenges Dollar appeared first on BeInCrypto.

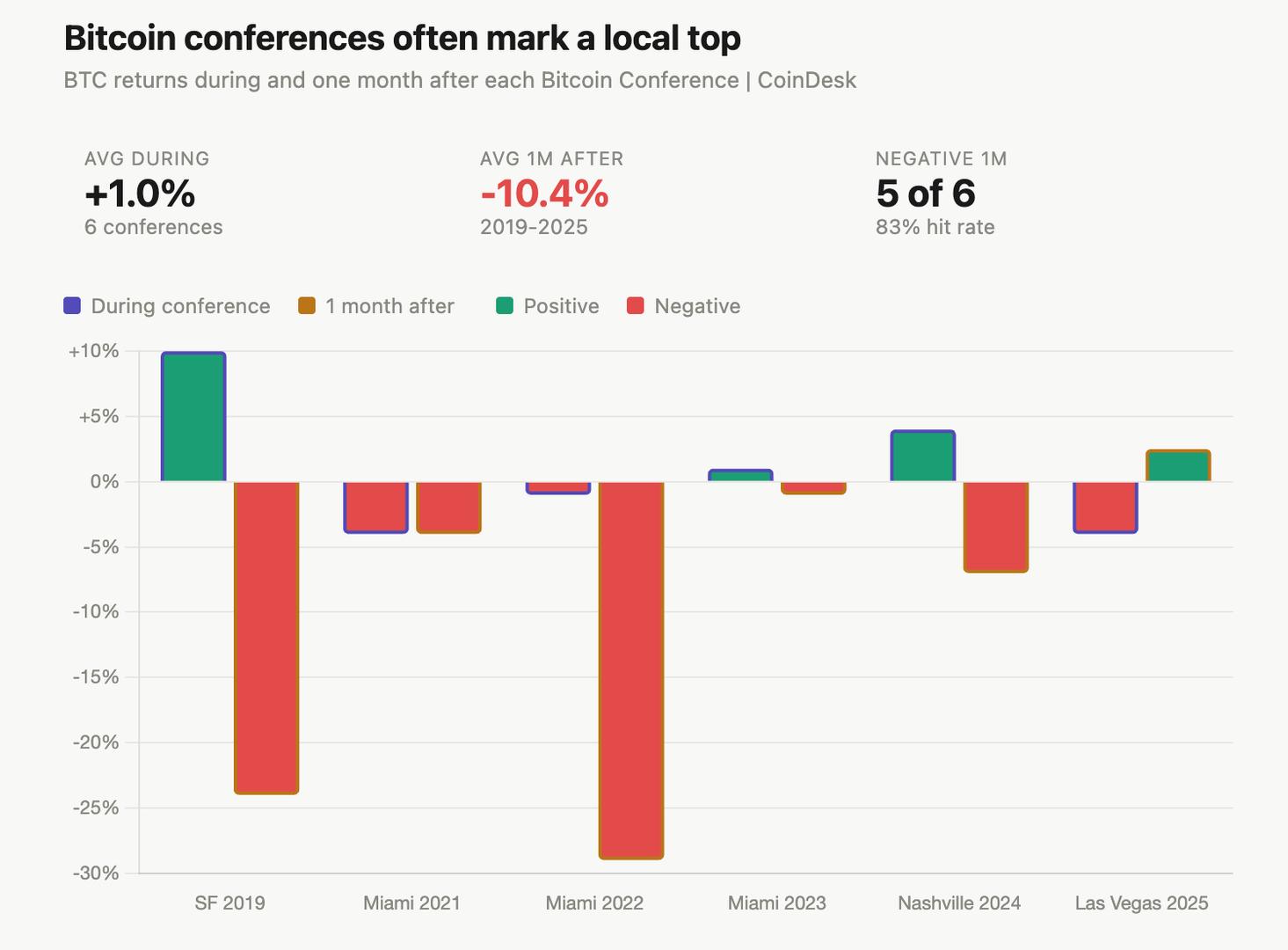

As bitcoin heads into this year’s flagship Bitcoin Conference in Las Vegas next week, traders will be watching for a familiar pattern, a potential “sell-the-news” event that has played out in previous years.

The largest cryptocurrency is trading around $75,000, recovering from a local bottom of around $60,000 in early February after collapsing more than 50% from its October all-time high.

Data from Galaxy Research and Investing.com spanning 2019 to 2025 show the price of bitcoin tends to rise in the run-up to these conferences, delivers a mixed performance during the event and declines substantially afterward.

For instance, bitcoin gained about 3% in the 24 hours before the 2024 event in Nashville (featuring then-presidential candidate Donald Trump) and roughly 10% ahead of the 2019 conference in San Francisco, suggesting positioning builds into peak attention. Price action during the conference is typically subdued as the narrative fails to deliver, and the weakest performance occurs in the days and weeks that follow.

In the 2022 bear market, often compared to the current 2026 bear market environment, bitcoin fell just 1% during the Miami conference before sliding nearly 30% over several weeks. Similar post-conference weakness was seen in 2019, 2021 and 2023, where any momentum failed to hold.

Even in 2024, when Nashville hosted Trump to outline plans to position the U.S. as a bitcoin superpower, gains during the event were short-lived and marked a local top, just ahead of the yen carry-trade unwind in August that pushed bitcoin as low as $49,000.

Conferences tend to coincide with peaks in attention and liquidity as bullish narratives build up to the event, creating conditions for investors to unwind positions.

With sentiment still fragile and prices recovering from deep losses, the key question for 2026 is whether Bitcoin Vegas will once again act as an exit liquidity event.

The quantum divide between Bitcoin and Ethereum

Quantum computing has long been viewed as a distant, largely theoretical threat to blockchain systems. However, that perspective is now starting to change.

With major technology companies such as Google establishing timelines for post-quantum cryptography, and crypto researchers re-examining long-held assumptions, the discussion is shifting from abstract theory to concrete planning.

However, Bitcoin and Ethereum, two major blockchain networks, are addressing the quantum computing threat in different ways. Both networks depend on cryptographic systems that could, in principle, be compromised by sufficiently powerful quantum computers. However, their approaches to addressing this shared vulnerability are evolving in markedly different directions.

This divergence, often referred to as the “quantum gap,” has less to do with mathematics and more to do with how each network handles change, coordination and long-term security.

Did you know? Quantum computers do not need to break every wallet at once. They only need access to exposed public keys, which means older Bitcoin addresses that have already transacted could theoretically be more vulnerable than unused ones.

Why quantum computing matters for blockchains

Blockchains rely heavily on public-key cryptography, particularly elliptic curve cryptography (ECC). This framework allows users to derive a public address from a private key, enabling secure transactions while keeping sensitive information protected.

If quantum computers achieve sufficient scale and capability, they could fundamentally weaken this foundation. Algorithms such as Shor’s algorithm could, in theory, allow quantum systems to compute private keys directly from public keys, thereby jeopardizing wallet ownership and overall transaction security.

The consensus among most researchers is that cryptographically relevant quantum computers are still years or even decades away. Nevertheless, blockchain platforms present a distinct challenge. They cannot be updated instantaneously. Any substantial migration requires extensive coordination, rigorous testing and broad adoption over multiple years.

This situation highlights a key paradox: Although the threat is not pressing in the near term, preparation needs to begin well in advance.

External pressure is accelerating the debate

The discussion has moved well beyond crypto-native communities. In March 2026, Google announced a target timeline to transition its systems to post-quantum cryptography by 2029. It cautioned that quantum computers pose a significant threat to existing encryption and digital signatures.

This development is particularly relevant for blockchain systems because digital signatures play a fundamental role in verifying ownership. While encryption is vulnerable to “store-now, decrypt-later” attacks, digital signatures face a distinct risk. If compromised, they could increase the risk of unauthorized asset transfers.

As major institutions begin preparing for quantum resilience, blockchain networks face growing pressure to outline their own mitigation strategies. This is where the differences between Bitcoin and Ethereum become more apparent.

Did you know? The term “post-quantum cryptography” does not refer to quantum technology itself. It refers to classical algorithms designed to resist quantum attacks, allowing existing computers to defend against future quantum capabilities without requiring quantum hardware.

Bitcoin’s approach: Conservative and incremental

Bitcoin’s approach to quantum risk is guided by its core philosophy: minimize changes, maintain stability and avoid introducing unnecessary complexity at the base layer.

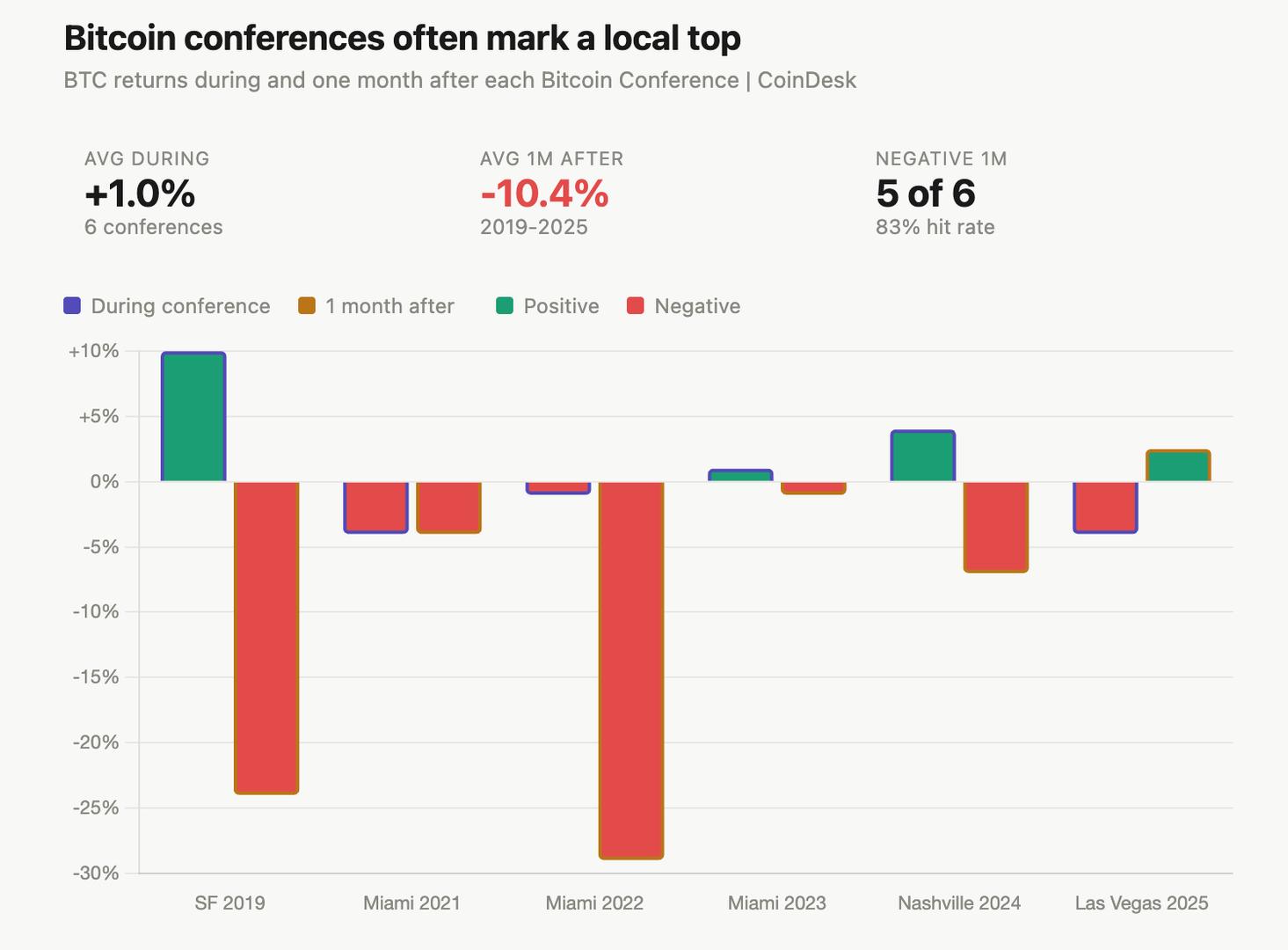

One of the most widely discussed proposals in this context is Bitcoin Improvement Proposal 360 (BIP-360), which introduces the concept of Pay-to-Merkle-Root (P2MR). Instead of fundamentally altering Bitcoin’s cryptographic foundations, the proposal seeks to limit exposure by changing the structure of certain transaction outputs.

The objective is not to achieve full quantum resistance for Bitcoin in a single move. Rather, it aims to create a pathway for adopting more secure transaction types while preserving backward compatibility with the existing system.

This approach mirrors the broader mindset within the Bitcoin community. Discussions often reflect extended time horizons, ranging from five years to several decades. The community is focused on ensuring that any changes do not undermine Bitcoin’s core principles: decentralization and predictability.

Nevertheless, this strategy has attracted criticism. Some argue that delaying more comprehensive measures could leave the network vulnerable if quantum advances arrive faster than expected. Others contend that making hasty changes could introduce avoidable risks into a system designed for long-term resilience.

Ethereum’s approach: Roadmap-driven and adaptive

Ethereum, by contrast, is pursuing a more proactive and structured strategy. The Ethereum ecosystem has begun formalizing a post-quantum roadmap that treats the challenge as a multi-layered system upgrade rather than a single technical adjustment.

A key element in Ethereum’s approach is “cryptographic agility,” which refers to the ability to replace core cryptographic primitives without undermining the stability of the network. This aligns with Ethereum’s broader design philosophy, which emphasizes flexibility and continuous iterative improvement.

The roadmap covers multiple layers:

-

Execution layer: Investigating account abstraction and alternative signature schemes that can support post-quantum cryptography.

-

Consensus layer: Assessing replacements for validator signature mechanisms, including hash-based options.

-

Data layer: Modifying data availability structures to ensure security in a post-quantum setting.

Ethereum developers have positioned post-quantum security as a long-term strategic priority, with timelines extending toward the end of the decade.

In contrast to Bitcoin’s incremental proposals, Ethereum’s approach resembles a staged migration plan. The goal is not immediate rollout but gradual preparation, allowing the network to transition when the threat becomes more concrete.

Why Bitcoin and Ethereum are taking different approaches to the quantum threat

The divergent approaches of Bitcoin and Ethereum are not a coincidence. They arise from fundamental differences in architecture, governance and philosophy.

Bitcoin’s base layer design emphasizes robustness and predictability, fostering a cautious attitude toward significant upgrades. Any change must meet a high bar for consensus and, even then, is usually limited in scope.

Ethereum, by contrast, has a track record of coordinated upgrades and protocol evolution. From the shift to proof-of-stake to ongoing scaling improvements, the network has demonstrated a willingness to execute complex changes when needed.

This distinction shapes how each network views the quantum threat. Bitcoin generally sees it as a remote risk that warrants careful, minimal intervention. Ethereum treats it as a systems-level issue that requires early planning and architectural adaptability.

In this context, the “quantum gap” is less about disagreement over the nature of the threat and more about how each ecosystem defines responsible preparation.

Did you know? Some early Bitcoin transactions reused addresses multiple times, unintentionally increasing their exposure. Modern wallet practices discourage address reuse partly because of long-term risks such as quantum attacks, even though the threat is not immediate.

An unresolved challenge for both Bitcoin and Ethereum

Despite their differing strategies, neither Bitcoin nor Ethereum has fully resolved the quantum threat.

Bitcoin continues to examine various proposals and weigh trade-offs, yet no clear migration path has been formally adopted. Ethereum, although more advanced in its planning, still faces substantial technical and coordination hurdles before its roadmap can be fully implemented.

Several open questions remain relevant to both ecosystems:

-

How to migrate existing assets protected by vulnerable cryptography

-

How to coordinate upgrades within decentralized communities

-

How to balance backward compatibility and forward security

These difficulties underscore the complexity of the issue. Post-quantum security represents more than a technical upgrade. It is also a test of long-term adaptability, governance and coordination.

Could security posture influence market narratives?

As institutional interest in quantum risk continues to grow, differences in preparedness could eventually shape how markets assess blockchain networks.

The reasoning is simple: A network that demonstrates greater adaptability to threats may be viewed as more resilient over the long term.

However, this idea remains largely speculative. Because quantum threats are still seen as a long-term concern, any near-term market effects are more likely to stem from narrative than from concrete technical developments.

Nevertheless, the fact that the discussion is now entering institutional research and broader public discourse suggests that it could become a more prominent consideration in the future.

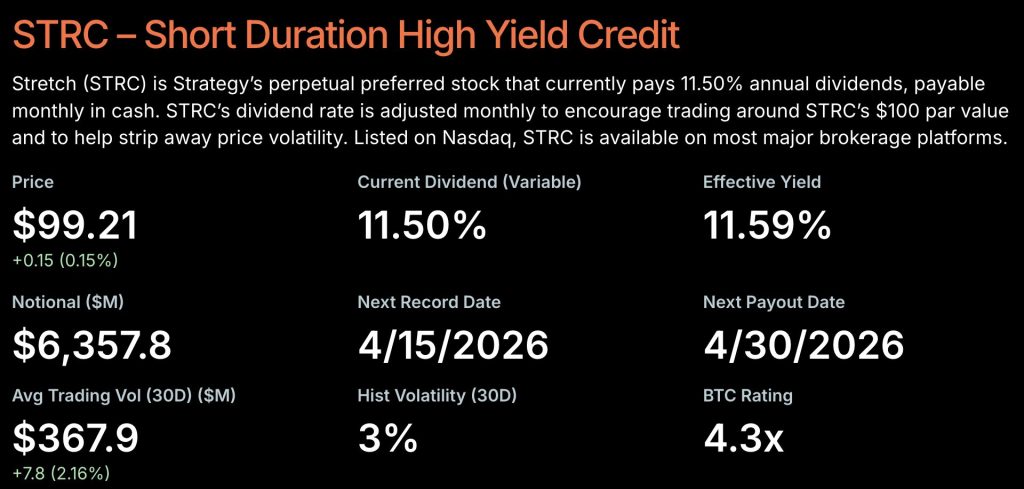

Michael Saylor signaled on social media that Strategy is on the verge of announcing another Bitcoin purchase, posting a chart of the company’s full BTC buying history with noticeably larger circles marking recent acquisitions.

The timing matters: Strategy already executed a record single-day buy exceeding $1 billion in BTC just before the tease, and with $2.25 billion in cash reserved, the scale of what comes next is the only open question.

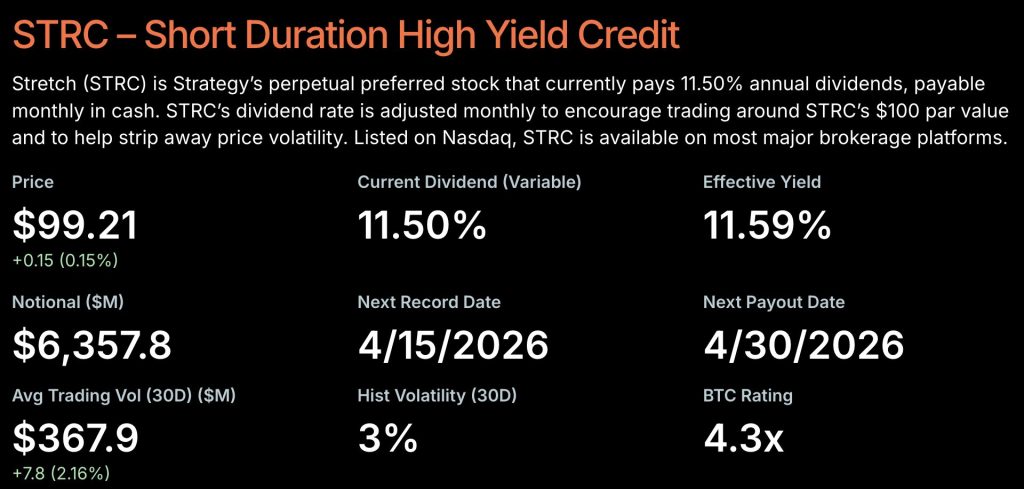

Simultaneously, the company, formerly MicroStrategy and now the largest corporate Bitcoin holder on the planet, floated a proposal to convert its STRC preferred stock from monthly to semi-monthly dividend payments, a structural capital markets refinement that analysts say could significantly broaden institutional demand for the instrument.

Discover: The best crypto to diversify your portfolio with

- Purchase incoming: Saylor shared a chart of Strategy’s BTC buying history with larger recent circles, signaling acceleration – another buy announcement is imminent.

- Dividend proposal: Strategy is floating semi-monthly payments for its STRC preferred stock, with shareholder voting closing June 8, 2026; first record date June 30, first payment July 15.

- STRC mechanics: Annualized yield stays fixed at 11.5%; switching to twice-monthly payments targets halved ex-dividend drawdowns, tighter liquidity patterns, and better collateral utility.

- Market signal: With BTC above $76,000 and $2.25 billion in cash reserved, Strategy’s dual move – more BTC plus refined shareholder returns – is a compounding demand signal for the spot market.

What Saylor Dual Signal Actually Means for Strategy’s Bitcoin Capital Stack

The STRC preferred series – branded “Stretch” – launched in mid-2024 at an 11.5% annualized yield, initially paying monthly dividends funded in part by Bitcoin treasury yields.

Volatility on the instrument has collapsed from 13% in its first eight months to 2.1% over the past two months, a compression driven by surging institutional demand that has pushed outstanding notional value to $6.4 billion.

The semi-monthly proposal doesn’t change the yield – 11.5% annualized remains fixed – but splits payment cadence to record dates on the 15th and last day of each month, pending Nasdaq compliance review and dual approval from both STRC holders and MSTR common shareholders.

Saylor’s stated rationale: “The proposed changes are intended to stabilize price, dampen cyclicality, drive liquidity, and grow demand.” He added the team views semi-monthly as “twice as good” as monthly for the instrument.

If approved, STRC would be the only preferred security or equity globally paying dividends twice monthly , a structural differentiator that improves collateral utility for borrowing and tightens haircuts for institutional holders using it as leverage collateral.

That’s not a minor footnote. Better collateral terms mean more institutional capital can rotate into STRC without consuming as much balance sheet, which expands the buyer pool at the exact moment Saylor is telegraphing another large BTC purchase. The feedback loop here is deliberate: more demand for STRC funds more capital raises, which fund more BTC accumulation, which backstops the yield instrument.

Discover: The best pre-launch token sales

The post Michael Saylor Hints at Bigger Bitcoin Buys After Floating Semi-Monthly Dividends appeared first on Cryptonews.

The Bank for International Settlements (BIS) general manager, Pablo Hernández de Cos, called for tighter global coordination on stablecoins Monday, warning that US dollar-denominated tokens could have “material consequences” for financial stability and economic policy if they grow large enough to rival traditional money.

Speaking at a Bank of Japan seminar in Tokyo, he said current stablecoin arrangements fall short of what is needed for a widely used means of payment, even if they offer faster cross-border transfers and integration with smart contracts.

De Cos said the largest US dollar stablecoins, such as USDt (USDT) and USDC (USDC), share characteristics with investment products rather than cash-like money, pointing to fees and conditions on primary market redemptions and episodes where their prices diverge from par in secondary markets.

In his view, these features make the tokens behave more like exchange-traded funds (ETFs), while still creating run and contagion risks because issuers hold short-term government debt and bank deposits as reserve assets. In a stress episode, he warned, rapid outflows from stablecoins could force sales of those reserves into already strained markets or transmit funding pressure to banks.

The warning comes as policymakers globally debate how to regulate fast-growing stablecoins and other tokenized money-like instruments.

He added that the use of public, permissionless blockchains and unhosted wallets means a significant share of activity sits outside conventional Anti-Money Laundering and Counter-Terrorism Financing controls, making stablecoins attractive for illicit use unless bespoke safeguards are implemented at on- and off-ramps.

Europe sharpens its stablecoin stance

The speech comes as European policymakers push for tighter control of non-euro stablecoins and other tokenized money-like instruments.

Earlier this month, Bank of France First Deputy Governor Denis Beau urged the European Union to go beyond the original Markets in Crypto Assets Regulation text by limiting the use of non-euro-denominated stablecoins in everyday payments, tightening rules on issuing the same coin inside and outside the bloc to reduce regulatory arbitrage in times of stress.

Related: EU central bank backs plan for crypto supervision under EU markets watchdog

In parallel, the European Central Bank has contrasted euro stablecoins with tokenized money market funds, noting that both perform liquidity transformation and are exposed to run risk, but operate under different transparency, liquidity management and regulatory regimes that can shape how stress feeds into funding markets.

Other major jurisdictions are also recalibrating their approaches. In the United Kingdom, members of the House of Lords questioned Coinbase in March over whether stablecoins could drain commercial bank deposits, trigger Silicon Valley Bank-style runs and facilitate crime, as the government finalizes a bespoke regime for fiat-backed tokens.

In Switzerland, UBS and several domestic peers launched a franc-denominated stablecoin pilot in a sandbox environment on April 8, in an effort to explore blockchain-based franc payments while keeping the instruments firmly anchored in the regulated financial system.

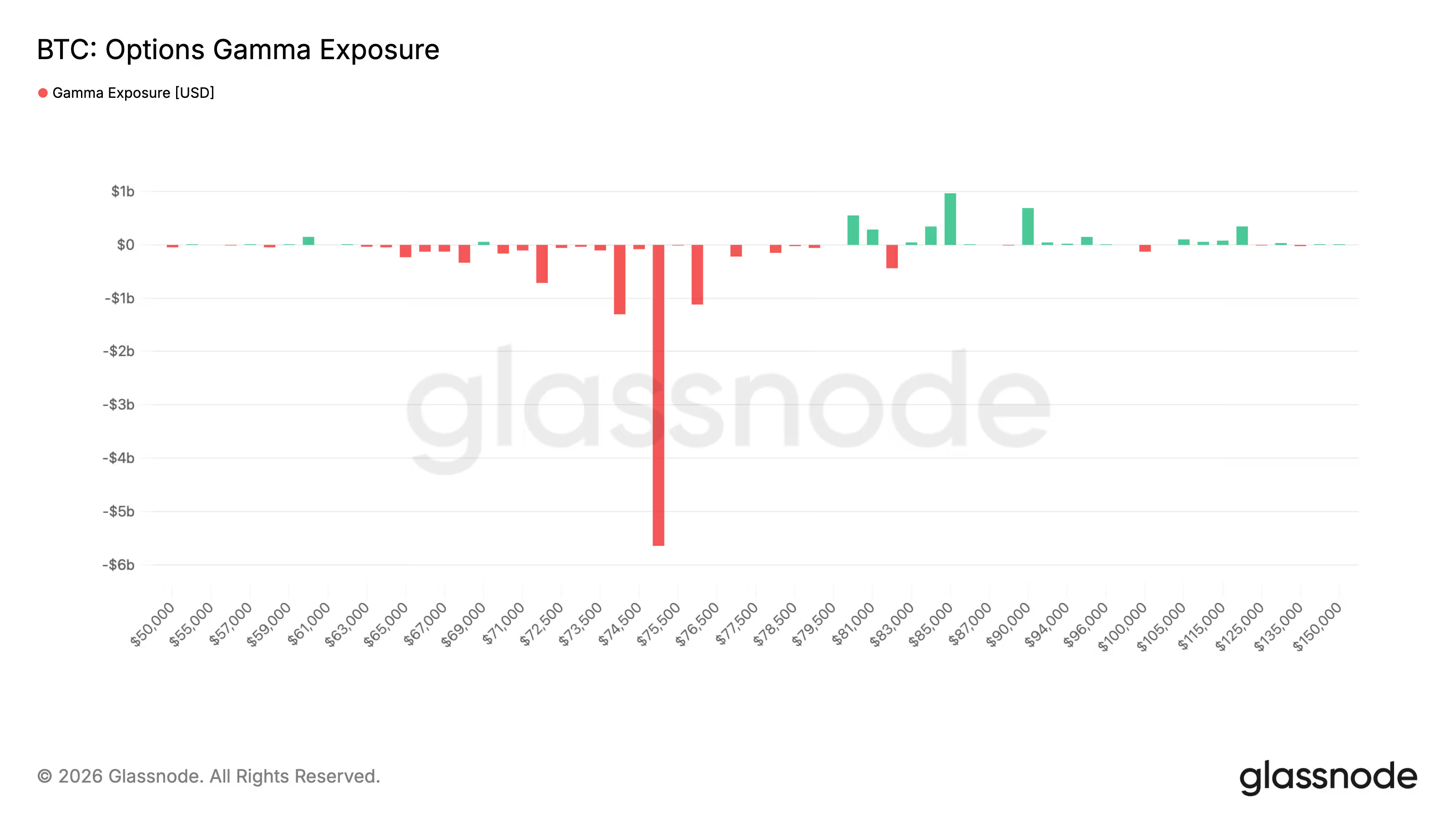

Bitcoin options worth roughly $7.9 billion are set to expire on Deribit this Friday, with positioning data pointing to $62,000 and $75,000 as key levels to watch out for.

The $75,000 level is where most trading in call options, which represent bullish bets, has happened, according to data source Glassnode. Around $395 million in call open interest is concentrated at the $75,000 strike as of writing. That figure represents the dollar value of the number of active call options contracts today.

More importantly, “gamma exposure” is deeply negative at the 75,000 strike – it means dealers’ hedging flows are likely to amplify price movements around this level. As the price rises, they may need to buy more, and as it falls, sell more, reinforcing the direction of the move.

As a result, the 75,000 level can act as a zone of heightened volatility, where price swings become sharper rather than stabilizing.

Options are derivative contracts that give the buyer the right to buy or sell the underlying asset, in this case, BTC, at a predetermined price at a later date. A call option gives the right to buy and a put option gives the right to sell.

It’s like paying a booking fee to reserve a right to transact a house at today’s price – you have the right to buy or sell it later at that price, but you’re not obligated to go through with the transaction if the market price moves against you.

On the downside, the largest concentration of put open interest sits at $62,000, with roughly $330 million in contracts, marking the main zone of downside protection.

Between the two, there’s this max pain level of $71,000, which can act as a magnate heading into the expiry. The “max pain” point is the price level at which the largest number of options contracts are expected to expire worthless on the settlement date, though this level can shift as prices and open interest change leading up to expiry.

All in all, the options market is effectively sitting between $62,000 and $75,000, with $71,000 acting as a midpoint. Unlike March, when bitcoin traded below max pain, the market is now sitting above it, to test whether bitcoin can hold onto its gains.

Potential short squeeze higher

Funding rates in perpetual futures have remained negative, indicating a build-up of short positions that could fuel a squeeze if prices hold higher. Bears could square off their bearish bets if prices remain resilient above $75,000, which could add to the upward momentum.

While data from Checkonchain shows Deribit now holds around $31 billion in open interest, the largest across options markets, surpassing even BlackRock’s IBIT, which stands near $28 billion.

Mastercard to Settle Card Payments via Stablecoins

How Hungary’s opposition won and what happens next

“I don’t have that friendly, buddy-like relationship”

-

Crypto World7 days ago

Crypto World7 days agoThe SEC Conditionalises DeFi Platforms to Be Avoided for Broker Registration

-

NewsBeat6 days ago

NewsBeat6 days agoTrump and Pope Leo: Behind their disagreement over Iran war

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Theodora Dress

-

Crypto World7 days ago

Crypto World7 days agoSEC Signals Exemption for Crypto Interfaces From Broker Registration

-

News Videos5 days ago

News Videos5 days agoSecure crypto trading starts with an FIU-registered

-

Sports3 days ago

Sports3 days agoNWFL Suspends Two Players Over Post-Match Clash in Ado-Ekiti

-

Crypto World6 days ago

Crypto World6 days agoSEC Proposes Certain Crypto Interfaces Don’t Need to Register as Brokers

-

Business20 hours ago

Business20 hours agoPowerball Result April 18, 2026: No Jackpot Winner in Powerball Draw: $75 Million Rolls Over

-

Crypto World3 days ago

Crypto World3 days agoRussia Pushes Bill to Criminalize Unregistered Crypto Services

-

Politics3 days ago

Politics3 days agoPalestine barred from entering Canada for FIFA Congress

-

Business4 days ago

Business4 days agoCreo Medical agree sale of its manufacturing operation

-

Politics1 day ago

Politics1 day agoZack Polanski demands ‘council homes not luxury flats for foreign investors’

-

Entertainment6 days ago

Entertainment6 days agoBrand New Day’ Footage Reveals the Devastating Impact of ‘Now Way Home’

-

Tech5 days ago

Tech5 days agoMicrosoft adds Windows protections for malicious Remote Desktop files

-

Entertainment6 days ago

Entertainment6 days agoKarol G’s ‘Ultra Raunchy’ Coachella Set Gave ‘Satanic Vibes’

-

Sports7 days ago

Sports7 days agoAaron Judge says Yankees need to ‘simplify’ approach amid offensive slump

-

Crypto World3 days ago

Crypto World3 days agoRussia Introduces Bill To Criminalize Unregistered Crypto Services

-

Entertainment7 days ago

Entertainment7 days agoHow Babylon 5 Turned Brief Side Story Into Emotional Masterpiece

-

Tech6 days ago

Tech6 days agoWhat was the first ransomware attack to demand payment in Bitcoin?

-

Tech4 days ago

Tech4 days ago‘Avatar: Aang, The Last Airbender’ Leaked Online. Some Fans Say Paramount Deserves the Fallout

You must be logged in to post a comment Login