Crypto World

XRP is a commodity until the SEC changes its mind

XRP won. Seven years of legal limbo ended on a single Wednesday in March, when two agencies put it in writing. What almost nobody has noticed is what kind of writing it was, and how little it would take to unwrite.

Summary

- On March 17, 2026, the SEC and CFTC jointly issued a 68-page interpretive release naming XRP among the digital commodities that are not securities under federal law, ending seven years of ambiguity in one document.

- The release is binding on both agencies, which makes it far stronger than the staff guidance the industry lived on before. It is not a statute and not a formal rule.

- That places XRP’s legal status on the third rung of a four-rung ladder: staff guidance, Commission interpretation, formal rule, statute. A future Commission can reinterpret without asking Congress for anything.

- The interpretation does not replace the Howey test. It tells you what XRP is; it does not permanently settle how any particular offer or sale of it gets treated.

- Two things could upgrade it. The SEC’s Regulation Crypto rulemaking would turn interpretation into rule. The CLARITY Act would turn it into law. One is stalled in the Senate and the other is sitting at the White House awaiting review.

For most of a decade, the single most important fact about XRP was a question: is it a security? The question survived a four-year lawsuit, a split ruling, a $125 million penalty, and the end of the case itself, because none of those resolved the underlying classification for anyone other than Ripple. Then, on March 17, 2026, it stopped being a question. The Securities and Exchange Commission, joined by the Commodity Futures Trading Commission, published a joint interpretive release that named XRP outright as a digital commodity. Not a security. In writing, from both agencies, at Commission level. The most consequential American crypto policy document in years, and it arrived without a single vote in Congress. That last detail is the whole story, and it cuts in both directions.

What the March release actually did

The document runs 68 pages and carries Release Numbers 33-11412 and 34-105020. It sorts crypto assets into five categories: digital commodities, digital collectibles, digital tools, payment stablecoins, and digital securities. Only the last of those, meaning tokenized versions of traditional instruments such as stocks and Treasuries, sits fully under SEC jurisdiction. Everything else falls primarily to the CFTC or outside securities regulation entirely.

XRP is named in the first category. So are Bitcoin, Ether, Solana, Dogecoin, Cardano, Avalanche, Chainlink, Polkadot, Hedera, Litecoin, Bitcoin Cash, Shiba Inu, Stellar, Tezos, and Aptos. Press coverage generally counted 16 named assets; several SEC-filed prospectuses describe the list as 18, and the discrepancy appears to come from how the release’s examples are counted rather than from any dispute about XRP’s inclusion.

The test the release applies is worth reading closely, because it explains why XRP qualified. A digital commodity is an asset intrinsically linked to and deriving its value from the programmatic operation of a functional crypto system, together with supply and demand dynamics, instead of from the expectation of profits from the essential managerial efforts of others. That final clause is Howey’s language, inverted. XRP is a commodity precisely because the XRP Ledger runs without Ripple’s managerial effort determining its value. The thing XRP holders spent years arguing became the legal basis for the classification.

The release also addressed the mechanics that had been left dangling for years: how a non-security crypto asset may become subject to an investment contract, how it may cease to be subject to one, and how the securities laws apply to airdrops, protocol mining, protocol staking, and the wrapping of a non-security asset. It follows the SEC’s Crypto Task Force, stood up in January 2025, and Project Crypto, which became a joint SEC-CFTC initiative in January 2026, along with a memorandum of understanding announced days earlier.

Both chairs put their names on the shift in language nobody could misread. Atkins, speaking at the DC Blockchain Summit, said his agency is not the securities and everything commission anymore. Selig, for the CFTC, said the wait was over and committed to rules of the road that let the industry operate onshore.

Why this is stronger than people assume

The reflexive crypto reaction to any agency action is that it is worthless because the next administration undoes it. That reaction is lazy here, and the reason is a distinction most coverage skipped.

This is a Commission-level interpretation, not staff guidance. The difference is not cosmetic. Staff guidance represents the views of agency personnel and binds nobody, which is why the industry spent years being told that no-action letters and staff statements carried no legal weight. As Jenner and Block noted in its client alert, the March interpretation is binding on the SEC and the CFTC. The agencies have committed themselves, and the CFTC further committed to administering the Commodity Exchange Act consistently with the SEC’s reading. That is the strongest thing short of a rule.

The practical effects arrived immediately and are already load-bearing. Fund issuers began citing the release directly in registration statements: Grayscale and Hashdex prospectuses point to it as the basis on which their index constituents are not securities. Accredited investors and fund managers could reclassify holdings and adjust compliance programs without waiting for the GENIUS Act’s full implementation in November 2026. Exchanges listing named assets shed a category of risk they had carried since 2018. A framework that private capital has already built products on top of is considerably harder to unwind than a memo, because unwinding it now means breaking live registered products.

There is a political durability argument too. Reversing the classification of Bitcoin, Ether, and XRP would require a future Commission to explain why a functional ledger’s token became a security again, against its own recent 68-page reasoning, in the face of litigation from every issuer relying on it. Agencies can do that. They rarely enjoy it.

Why it is weaker than a law

Now the other side, and it is the reason this piece exists. Everything above describes strength within the executive branch. None of it describes permanence.

The interpretation is administrative action. It is not a statute. Any future administration can direct its agencies to reinterpret, and no congressional vote is required to do it. The current regulatory floor under XRP was created by two agency chairs and can be lifted by two different agency chairs. The industry spent 2018 through 2025 learning what it feels like when a Commission decides that the previous Commission’s posture was wrong, and nothing in the March release prevents that from happening again. It simply raises the cost.

The release also does not supersede Howey. Norton Rose Fulbright made the point plainly: the joint interpretation does not replace the Supreme Court’s test. It cannot, because an interpretive release cannot overrule the Court. What the agencies did was explain how they will apply existing law. A court hearing a private securities claim is not bound by the agencies’ view of the statute, and the security status of any specific asset still turns on the facts and circumstances of its offer and sale. The SEC said as much: an asset may cease to be linked to an investment contract as the relevant facts evolve, which is the same sentence read backwards.

That leaves a gap that matters for XRP specifically. The 2023 ruling in the Ripple case drew a line between programmatic sales on exchanges and institutional sales, treating them differently. The March interpretation classifies the asset. It does not immunize every transaction in that asset. An aggressive future enforcement posture would not need to declare XRP a security to cause problems. It would only need to find managerial effort in a particular offering.

And there is the awkward provenance question. The framework XRP holders are now relying on was produced by the same agency that spent four years litigating against Ripple and collected a $125 million penalty. That agency did not change its mind because the law changed. It changed its mind because its leadership changed. Which is precisely the argument for wanting something more permanent.

The ladder

The useful way to hold all of this is as a hierarchy of durability, because XRP’s status is not binary. It sits on a specific rung.

Staff guidance is the bottom. Non-binding, reversible by a memo, worth roughly what the issuing staff’s tenure is worth. This is what crypto had for years.

Commission-level interpretation is where XRP sits today. Binding on the SEC and CFTC, reasoned in public across 68 pages, relied upon in live registration statements. Reversible by a future Commission through the same instrument that created it, with no involvement from Congress and no notice-and-comment obligation.

A formal rule is the next rung, and it is the one currently in motion. The SEC’s Regulation Crypto proposal sits in the agency’s July 2026 rulemaking slot, under review at the White House Office of Information and Regulatory Affairs. Rules go through notice and comment, which is slow and irritating and precisely why they are hard to unwind. Reversing a final rule generally requires another full rulemaking, with a reasoned explanation that survives judicial review. Bankless made the observation that most outlets missed: the SEC has leaned on staff guidance and its taxonomy so far, but formal rules are far harder for a future commission to undo.

A statute is the top. The CLARITY Act would put the taxonomy into law, at which point unwinding it requires Congress, which is a body that struggles to pass anything at all. That difficulty is the feature.

So XRP holders currently occupy rung two of four, with rung three under White House review and rung four stuck on the Senate calendar with no floor vote scheduled and roughly three working weeks left before the August recess. That is the actual position, and it is neither the triumph nor the mirage that the two loudest camps describe.

The four years everyone forgot to price

There is a piece of history worth putting next to the March release, because it explains why the classification felt like an ending and why it is not one.

The SEC sued Ripple in December 2020, alleging XRP had been sold as an unregistered security. The case ran four years and produced a split ruling in 2023: sales to institutional buyers were investment contracts, while programmatic sales on exchanges were not, because anonymous buyers on an order book could not know whose effort they were relying on. Ripple ultimately paid a $125 million penalty and the litigation wound down in 2025. Exchanges delisted XRP for American users during the case and relisted after it. Billions in market value moved on procedural filings.

Notice what that outcome did and did not settle. It resolved claims against one company. It did not classify XRP for anyone else, which is why the question survived the case that was supposed to answer it. Every other market participant was left reading a district court opinion about someone else’s conduct and guessing. That guessing is what ended in March, and it ended not because a court ruled or Congress voted, but because agency leadership changed and the new leadership read the same statute differently.

That is the part worth sitting with. The law did not change between 2020 and 2026. The Securities Act of 1933 reads the same. Howey reads the same. The XRP Ledger runs the same consensus it ran when the lawsuit was filed. What changed was who occupied the chairs, and the outcome flipped from four years of litigation to a 68-page release naming XRP as a commodity in the first category.

Anyone who believes that dynamic runs in only one direction has not been paying attention. The same mechanism that delivered the win is the mechanism that could withdraw it, and it requires nothing more dramatic than another election and another appointment. This is exactly why the ladder matters, and exactly why the industry pushed for statute instead of settling for the agency’s blessing. A framework that can be reversed by a personnel change is not a framework. It is a truce.

The counterpoint, and it is a fair one, is that this cuts against the doom case too. If a hostile Commission could reclassify XRP tomorrow, it could also have done so at any point in the past decade and largely did try. The industry survived. Exchanges relisted. The asset persisted through the worst enforcement posture the SEC could produce, which suggests the practical downside of reinterpretation is a repeat of a period XRP already lived through and outlasted, not an existential event. The market has already stress-tested the bear case, and XRP is still here.

What this means for the price nobody wants to hear

XRP trades around $1.10 to $1.15, having reclaimed that support after a macro-driven rally cooled. A year ago it traded near $3.65. Analysts note that regulatory risk on Ripple has fallen to a multi-year bottom following the end of the SEC litigation, and demand from domestic funds has stabilized accordingly.

Both of those sentences are true simultaneously, and their coexistence is the most instructive fact about this market. The single largest overhang on XRP for seven years was legal uncertainty. That overhang has been removed more decisively than the most optimistic holder could have scripted in 2022: named, in writing, by both agencies, at Commission level. And the token is down roughly 70% from a year ago.

The honest conclusion is that legal clarity was necessary and is not sufficient. It removed a reason not to own XRP. It did not create a reason to own it. Those are different things, and the market has now run the experiment. Anyone still arguing that the next regulatory milestone is the catalyst has to explain why the biggest regulatory milestone in the asset’s history produced a lower price.

Which loops back to the ladder, and to why the rung matters even in a market that appears not to care. The value of moving from interpretation to rule to statute is not that it triggers a rally. It is that it removes the tail. As long as XRP’s classification rests on administrative action, an unknown future Commission holds an option to reopen a question that took seven years and $125 million to close the first time. Codification does not make XRP go up. It makes the worst case go away. In an asset that has spent a decade pricing legal risk, retiring the possibility of its return is worth something, and it is worth it quietly, over years, in the form of institutions that will hold it because they no longer need a legal opinion to do so.

What to watch

Three things, in order of how much they would change.

Regulation Crypto clearing OIRA and reaching public comment. The proposal is slotted for July. If it publishes and survives comment substantially intact, XRP moves from rung two to rung three, and the classification gets meaningfully harder to reverse. Watch whether the decentralization off-ramp language stays intact, since that is the provision doing the same work the taxonomy does.

The CLARITY Act reaching a floor vote before August 7. If it passes and is signed, the taxonomy becomes statute and the question closes permanently. If it dies, the entire American crypto framework rests on one agency’s interpretation and one agency’s pending rule, which is the outcome the industry spent a year lobbying to avoid.

Any enforcement action that tests the edges. The interpretation classifies assets. It does not classify transactions. The first case that alleges a specific XRP offering carried managerial effort, notwithstanding XRP’s commodity status, will show how much the March release actually protects. Until that happens, its practical strength is theoretical.

XRP won its argument. It won it in the weakest venue that could have delivered the win, from an agency that could deliver it because its leadership changed and could withdraw it for the same reason. Whether that victory is permanent is being decided right now, in a rulemaking review and on a Senate calendar, and almost none of it is being decided by anything Ripple does.

Disclaimer: This article is for information and educational purposes only and does not constitute financial, investment, or legal advice. It describes regulatory interpretations and pending rulemaking, both of which can change, and it is not a legal opinion on the status of any asset. Nothing here is a recommendation to buy or sell anything. Always do your own research. Information is accurate as of July 17, 2026.

Frequently Asked Questions

Is XRP a security?

No, according to the SEC and CFTC. On March 17, 2026, the two agencies jointly issued a 68-page interpretive release classifying XRP as a digital commodity, meaning it is not a security under federal law. The classification also covers Bitcoin, Ether, Solana, and roughly a dozen other named assets. The release is binding on both agencies.

Why does XRP qualify as a digital commodity?

Because the test asks whether an asset derives its value from the programmatic operation of a functional crypto system and from supply and demand, instead of from the expectation of profits from the essential managerial efforts of others. The XRP Ledger operates without Ripple’s managerial effort determining the token’s value, which is the argument holders made for years and which became the basis of the classification.

Can the SEC reverse this?

Yes, without asking Congress. It is administrative action, not statute. A future Commission could issue a new interpretation. What makes reversal costly rather than trivial is that this is a Commission-level interpretation binding on both agencies, publicly reasoned across 68 pages, and already relied upon in live registration statements filed by fund issuers, so unwinding it would mean disrupting registered products and inviting litigation.

Does the interpretation replace the Howey test?

No. An interpretive release cannot overrule a Supreme Court decision. The agencies explained how they will apply existing law, and the SEC noted that an asset’s security status still depends on the facts and circumstances of its offer and sale. A court hearing a private claim is not bound by the agencies’ view. The release classifies assets; it does not immunize every transaction in them.

How is this different from the Ripple lawsuit outcome?

The lawsuit resolved claims against one company and produced a split ruling distinguishing programmatic exchange sales from institutional sales, plus a $125 million penalty. It did not settle XRP’s classification for anyone else. The March 2026 interpretation classifies the asset itself, applies to all market participants, and comes from both agencies jointly.

What would make XRP’s status permanent?

Two things, in ascending order of durability. The SEC’s Regulation Crypto proposal, currently in the agency’s July 2026 rulemaking slot and under White House review, would convert interpretation into a formal rule, which requires another full rulemaking to reverse. The CLARITY Act would write the taxonomy into statute, which would require an act of Congress to undo.

If the legal question is settled, why is XRP down?

Because legal clarity removed a reason not to own XRP without creating a reason to own it. Regulatory risk on Ripple has fallen to a multi-year bottom and the token still trades near $1.10 against roughly $3.65 a year ago. The market has effectively run the experiment: the largest regulatory milestone in the asset’s history did not produce a higher price, which suggests the price is being set by broader market conditions instead of by classification.

This year, Tether rolled out USAT — launched with U.S. standards in mind and issued through U.S. banking partner Anchorage Digital. So far, it remains at a relatively low level of usage.

“Non-compliant stablecoins cannot be used by U.S. institutions when the safe harbor expires in 2028, but we don’t expect the market to wait,” said Kevin Wysocki, head of policy at Anchorage Digital, the crypto-native bank that manages a number of stablecoins. He said the company believes institutional users will move toward “compliant, bank-issued digital dollars well ahead of that deadline.”

Do they have two years?

GENIUS included a three-year grace period for compliance, and two years remain, after which U.S. crypto platforms won’t be able to offer stablecoins whose issuers haven’t checked all the regulatory boxes. However, there seems to be some disagreement over whether foreign issuers are meant to enjoy that same safe harbor. Some lawyers in finance assume that Tether gets until July 18, 2028, to comply, but others have suggested that foreign issuers would have to comply the moment GENIUS officially goes live, which is likely six months from now in January.

“Upon the effectiveness of the GENIUS Act, foreign issuers will need to immediately comply with lawful orders to seize and freeze coins held by illicit actors, but they will have a runway of approximately two more years to prepare for the additional requirements so that their coins may remain eligible for listing on U.S. centralized trading platforms,” said Justin Levine, a lawyer at Davis Polk who advises clients on stablecoin issues, adding that one of those remaining requirements — registration with the Office of the Comptroller of the Currency — is likely to require a “significant undertaking”

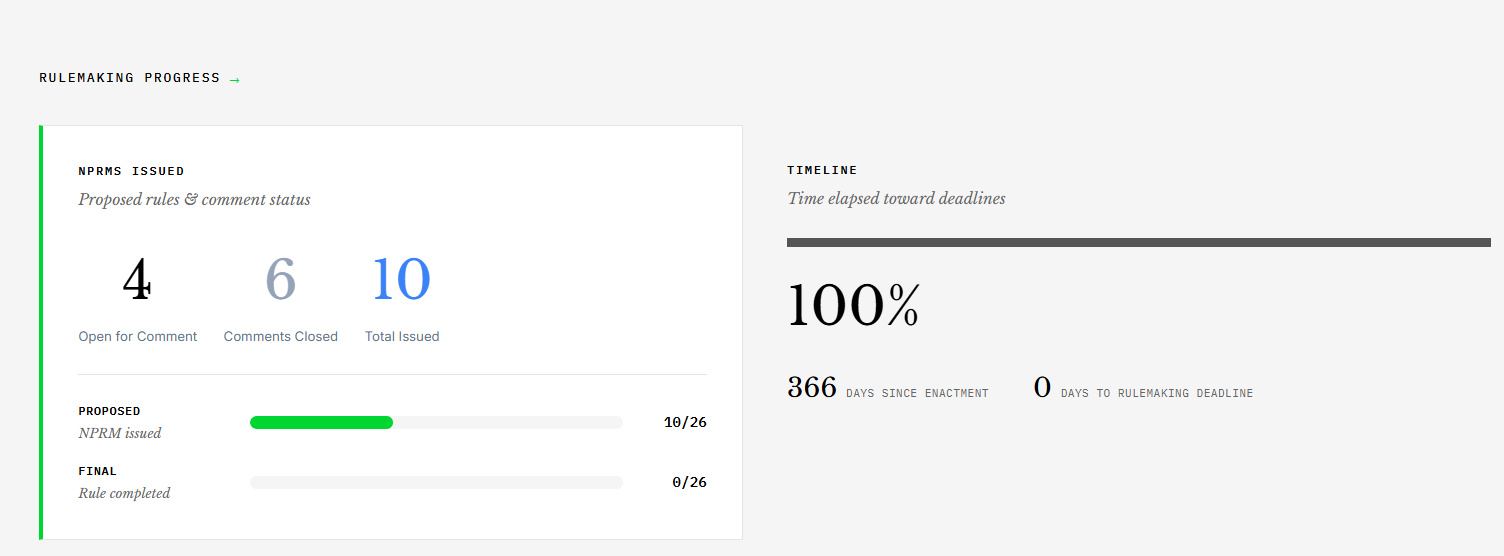

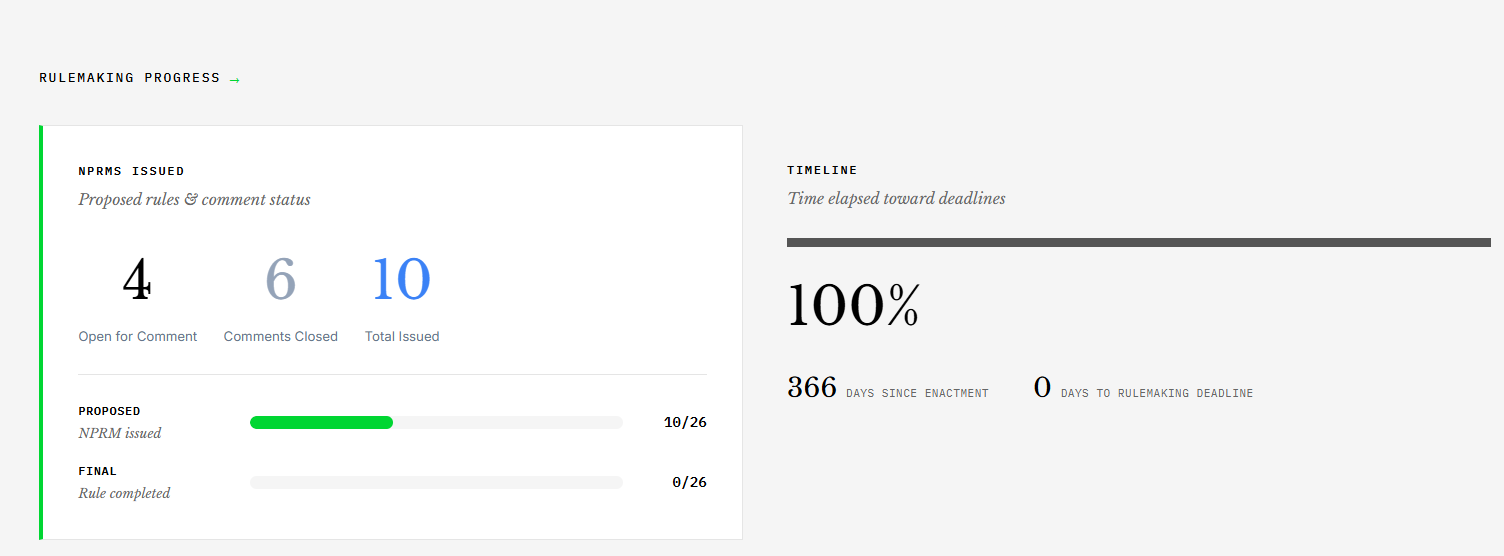

U.S. stablecoin regulators missed a key rulemaking deadline tied to the Guiding and Establishing National Innovation for US Stablecoins (GENIUS) Act, despite issuing multiple proposals and gathering public input over the past year. The deadline passed on Saturday, marking one year since the law was signed—yet no final regulations had been published by the end of that window.

The GENIUS Act, signed by President Donald Trump on July 18, 2025, created the first comprehensive federal regulatory framework for stablecoins. While several agencies advanced the process through notices of proposed rulemaking (NPRMs), rulemaking trackers maintained by Chapman and crypto investment firm Paradigm show that final rules were not issued before the statutory deadline.

Key takeaways

- Despite a full year of rule development, U.S. agencies had not released final GENIUS Act regulations by the deadline, according to Chapman and Paradigm trackers.

- GENIUS remains valid law, but the lack of final rules increases compliance uncertainty for stablecoin issuers and supervised institutions.

- Federal agencies—including the Treasury Department and banking regulators—published multiple NPRMs covering registration, supervision, reserve expectations, and AML-related implementation.

- Anchorage Digital used the one-year GENIUS milestone to renew a push for broader digital-asset market structure legislation through the CLARITY Act.

What the deadline miss means for stablecoin compliance

Missing the statutory deadline does not automatically invalidate the GENIUS Act itself. However, it can materially affect how quickly regulated entities can operationalize the framework. Stablecoin issuers, payment-focused platforms, and institutions planning to participate in issuance or custody have generally relied on final rules to guide compliance programs, governance processes, and supervisory expectations.

According to rulemaking trackers by law firm Chapman and Paradigm, multiple agencies published proposals during the past year but did not conclude the rulemaking process in time. The agencies named in the trackers include the Department of the Treasury, the Office of the Comptroller of the Currency (OCC), the Federal Deposit Insurance Corporation (FDIC), and the Federal Reserve Board, all of which issued NPRMs without publishing final versions before the deadline.

That gap is likely to be most consequential for issuers seeking clarity on how regulators intend to evaluate reserve management, supervisory standards, and compliance obligations—areas where the GENIUS framework is intended to bring consistency across federal oversight.

GENIUS’s first year: agencies issued 10 proposed rulemakings

Paradigm’s tracking data indicates that federal regulators issued 10 NPRMs during the GENIUS Act’s first year. The proposals spanned the act’s broader implementation and the mechanics of how different types of regulated entities would participate.

The U.S. Department of the Treasury released four proposals focused on implementation and eligibility questions, including how regulators should determine when state stablecoin regimes are “similar” to the federal framework, registration requirements for foreign stablecoin issuers, and guidance tied to anti-money laundering (AML) compliance.

Meanwhile, the OCC issued two NPRMs addressing nationally chartered payment stablecoin issuers, including approval requirements and supervisory standards intended for those entities.

The FDIC published one NPRM for FDIC-supervised institutions that issue payment stablecoins, centering on supervisory expectations and operational requirements such as reserve management.

The National Credit Union Administration (NCUA) also moved forward with proposed rules designed to enable federally insured credit unions to participate in stablecoin issuance.

Finally, federal banking agencies jointly proposed an interagency implementation rule meant to harmonize supervision across the OCC, Federal Reserve, and FDIC—an attempt to reduce inconsistencies in oversight that can arise when multiple regulators examine similar activities under different supervisory practices.

In practical terms, the breadth of proposals shows regulators were actively working through the architecture of GENIUS. Still, the failure to finalize the rules by the deadline leaves open questions about how the draft proposals will be resolved and what changes—if any—will be made after public comment periods close.

Anchorage renews its CLARITY push as GENIUS rules remain unfinished

As regulators continued to work through proposed GENIUS rules, Anchorage Digital—a federally chartered crypto bank—used the GENIUS one-year anniversary to call again for Congress to pass the Digital Asset Market Clarity Act (CLARITY). In a report published on Friday, Anchorage said it was “renewing” its request for lawmakers to extend stablecoin market-structure rules into the broader digital asset economy.

CLARITY is intended to establish the first federal regulatory framework for digital assets more broadly. Anchorage’s messaging also aligns with ongoing industry debate about how far existing banking rules should extend to stablecoins, particularly regarding whether yield offerings could be structured without triggering deposit-substitute concerns.

Earlier coverage noted that CLARITY advanced through the Senate Banking Committee in May. Industry groups, including state banking associations, have argued that the bill could enable crypto firms to offer yields on stablecoins without meeting requirements they say traditional banks must follow.

On July 13, the American Bankers Association (ABA) and the Independent Community Bankers of America (ICBA), among other state banking associations, sent a joint letter urging Senate leaders to provide more detail on CLARITY’s stablecoin yield provisions. The letter also argued that amendments are needed to ensure payment stablecoins remain transaction tools rather than operating like deposit substitutes.

Legislative uncertainty has also been visible in market participants’ expectations. On June 26, Galaxy Digital reportedly cut its odds of CLARITY becoming law in 2026 to 50%, citing the lack of a unified Senate Banking–Agriculture text, no firm floor schedule, and a narrowing legislative window as lawmakers near departure periods.

Taken together, the regulatory timeline under GENIUS and the parallel legislative push for CLARITY point to a broader policy reality for the sector: stablecoins are increasingly regulated through federal rulemaking, but questions about market structure and adjacent digital asset rules remain bound to Congress rather than agencies alone.

What to watch next as proposed rules move toward finality

With the GENIUS rulemaking deadline passed and final regulations still pending, stablecoin issuers and supervised institutions should watch for the agencies named in the rulemaking trackers to publish final rules—or revised drafts—after comment periods. Investors and operators may also want to monitor whether the interagency harmonization proposal results in more consistent supervisory expectations across regulators, and whether congressional momentum on CLARITY meaningfully changes the policy direction around stablecoin yields and broader digital asset market structure.

Derivatives account for the vast majority of crypto trading volumes, but options remain a relatively small corner of the market, dominated by a handful of established venues including Deribit, CME Group and Binance. New entrants are increasingly betting that broader adoption of options will follow the institutionalization of digital assets.

The move is the latest step in Kraken’s transformation from a crypto exchange into a broader financial platform offering trading, payments and other digital asset services.

Growing the market, not just market share

Rather than focusing solely on taking market share from incumbent venues, Theodorou believes the larger opportunity is expanding the addressable market by making options easier to use.

“The existing options market in crypto has been built for a narrow slice of the trader base,” Theodorou said.

“Our offering broadens access through a straightforward, dollar-settled contract in the same account clients already use for spot and futures,” she added.

A retail-first approach

According to Theodorou, the slow growth of crypto options is less a demand problem than a product design problem.

“The gap in crypto options isn’t demand, it’s design,” Theodorou said.

She notes that existing crypto options platforms have largely catered to institutional traders and market makers, while retail traders instead have gravitated toward perpetual futures, which became the industry’s dominant speculative product because of their relative simplicity.

US regulatory agencies missed the rulemaking deadline under the Guiding and Establishing National Innovation for US Stablecoins (GENIUS) Act on Saturday, which marked one year since the law was signed.

Several US regulatory agencies published proposed rules and collected public feedback during the past year, but no final regulations were issued before the deadline.

These agencies include the Department of the Treasury, the Office of the Comptroller of the Currency (OCC), the Federal Deposit Insurance Corporation (FDIC) and the Federal Reserve Board, which issued proposed rules but no final rules, according to rulemaking trackers by law firm Chapman and crypto investment company Paradigm.

Missing the statutory deadline does not invalidate the GENIUS Act, but the unfinished rules may result in regulatory uncertainty for stablecoin issuers.

The GENIUS Act established the first comprehensive federal regulatory framework for stablecoins in the US. The act was signed into law by US President Donald Trump on July 18, 2025.

Related: ABA, state banking groups push back on CLARITY Act stablecoin yield provisions

Regulators issued 10 rule proposals during the GENIUS Act’s first year

Federal regulators issued 10 notices of proposed rulemaking (NPRM) in the year since the GENIUS Act was signed into law, according to Paradigm.

The Treasury Department issued four proposals covering the broader implementation of the act, including standards for determining whether state stablecoin regulatory regimes are similar to the federal framework, registration requirements for foreign stablecoin issuers and guidelines for compliance with anti-money laundering measures.

Rulemaking progress after the GENIUS Act was signed into law. Source: Paradigm.

The OCC issued two NPRMs covering nationally chartered payment stablecoin issuers, approval requirements and supervisory standards.

The FDIC issued one NPRM on FDIC-supervised institutions that issue payment stablecoins, focused on supervisory expectations and operational standards such as reserve management.

The National Credit Union Administration (NCUA) proposed rules enabling federally insured credit unions to participate in stablecoin issuance.

Finally, federal banking agencies jointly proposed an interagency implementation rule to harmonize supervision across the OCC, Federal Reserve and FDIC, aiming to ensure consistent supervisory expectations across all federal regulators.

Anchorage urges lawmakers to pass CLARITY Act

Federally chartered crypto bank Anchorage Digital has urged lawmakers to pass the Digital Asset Market Clarity Act (CLARITY).

“On GENIUS’ one-year anniversary, we’re renewing our call for Congress to pass the CLARITY Act and extend the clear market-structure rules that worked for stablecoins to the broader digital asset economy,” Anchorage Digital wrote in a Friday report.

The CLARITY Act seeks to establish the first federal regulatory framework for digital assets in the US. It cleared the Senate Banking Committee in May, though banking industry groups argued that it would allow crypto firms to offer yields on stablecoins without facing the same requirements as traditional banks.

On July 13, state banking associations, including the American Bankers Association (ABA) and the Independent Community Bankers of America (ICBA), sent a joint letter urging Senate leaders to provide more detail on the CLARITY Act’s stablecoin yield provisions and argued that new amendments need to prevent payment stablecoins from acting as deposit substitutes rather than pure transaction tools.

On June 26, Galaxy Digital cut its odds of the CLARITY Act becoming law in 2026 to 50%, citing the lack of a unified Senate Banking-Agriculture text, no firm floor schedule and a narrowing legislative window before lawmakers leave Washington.

Magazine: Gambling on random Pokémon cards: Onchain gagcha hits record high as crypto sinks

Kalshi’s logo appears on a smartphone placed on a reflective surface, with a blurry betting curve projected in the background in Creteil, France, on March 9, 2026, during a major scandal and $54 million lawsuit concerning bets related to recent strikes in Iran.

Nurphoto | Nurphoto | Getty Images

The 2026 FIFA World Cup has sent prediction market trading volumes across platforms soaring. And for Kalshi, it has delivered millions of new users.

Kalshi has brought in 3 million new users over the course of the tournament, the company shared with CNBC.

More than $1.2 billion has been traded on Kalshi’s contracts that ask traders to predict the winner of the World Cup, a record for a singular market. That market will officially close on Sunday, after Spain and Argentina compete in the final for the title.

“I don’t think there’s any game like football,” said Vijay Viswanathan, an associate dean of integrated marketing communications at Northwestern University, referring to soccer. “It’s played in about every country in the world … so in just terms of the total addressable market, there’s really nothing that comes close to the FIFA World Cup.”

Argentine fans react as their team scores against Egypt during a FIFA World Cup match watch party at Cerveceria La Tropica on July 07, 2026 in Miami, Florida. Argentina and Egypt are playing in the round-of-16 match in Atlanta.

Joe Raedle | Getty Images

Across the World Cup, Kalshi has made several moves to boost its brand. Those include a partnership with the official prediction market sponsor of the World Cup, ADI Predictstreet, to feature co-branding advertisements in stadiums. It also partnered with OpenAI last week to feature the company’s contract’s odds when users search about games in the tournament on ChatGPT.

But it also has featured a slew of advertisements with key faces in the soccer world: Croatian soccer star Luka Modric, longtime Real Madrid coach José Mourinho, and even a partnership with the Argentina national team. That deal got the company a feature in a post by superstar Lionel Messi on Instagram.

“Our volumes are where the news is at,” said Kalshi CEO Tarek Mansour, who takes on a lead role in guiding the company’s marketing strategy. “It’s a lot of the approach for the World Cup. … The most important thing is enable creativity based on what’s happening.”

Speed is key, too. One advertisement featuring former professional soccer stars playing a scrimmage with each other released on Friday was conceived, executed and released in 24 hours, Mansour said.

But Kalshi also launched ads with non-soccer celebrities around the tournament, too. An advertisement with actor Timothee Chalamet was released in June — around when he was garnering attention for his appearances at New York Knicks games during the NBA Finals — while a spot with Colombian singer J Balvin came out this month.

“This is also a way for them to say, ‘oh, but we’re also relevant to all these other people who might not be that interested in sports, too,’” said Elizabeth Johnson, executive director of the Wharton Neuroscience Initiative at the University of Pennsylvania. Johnson also teaches a visual marketing class at the university. “They’re seizing this moment to remind people about the ubiquitousness of what these prediction markets are.”

Leaning heavily into the sports event comes with risks, too. Sports event contracts are under scrutiny in a dispute between the federal government and the states. States argue those contracts are equivalent to sports betting, something state governments control.

Kalshi agrees with the federal government that the Commodity Futures Trading Commission — which regulates swaps and derivatives — has the sole power to regulate prediction markets.

Tarek Mansour, co-founder and CEO of Kalshi speaks during CNBC’s Squawk Box on June 24, 2026.

CNBC

Mansour dismissed those concerns, though, arguing its sports contracts are only under pressure from gambling companies worried about losing their dominant, incumbent positions.

Brian Sung, a partner in the derivatives and digital assets practice groups at Haynes Boone, doesn’t think the advertising strategies impact how courts may rule in the future, but said it does impact the view of prediction markets.

“It does kind of weaken their perception, in public or politics,” he said. “They are trying to push against this idea that they’re really only about sports. I mean, that is where the bulk of their activity is.”

Kalshi now moves onto turning those 3 million new users into recurring traders, which could be a challenge: volume on days when World Cup matches haven’t been played has been significantly lower than when the games are on.

Mansour added this cycle has happened before: a major event that drives volume higher, with a temporary decline after only for it to keep marching higher off of other events.

“You have to believe there’s not going to be any news after Sunday,” he said. “Maybe, … but the more probable thing is that there’s going to be like a bunch of things going on in the world, and Kalshi’s going to be there to service it.”

Disclosure: CNBC and Kalshi have a commercial relationship that includes customer acquisition and a minority investment.

Moonshot AI plans to list on the Hong Kong Stock Exchange within six months, people familiar with the matter say. The Beijing-based startup behind the Kimi chatbot has circulated a shareholder resolution to secure investor approval for the offering.

The filing follows a turbulent week for Moonshot, whose new Kimi K3 model briefly rattled global technology markets. Investors now watch whether the company can turn that momentum into a successful debut.

Kimi K3 AI Model Shakes Global Markets

Moonshot released Kimi K3 on July 16, an open-weight model built on roughly 2.8 trillion parameters. Its design uses a mixture-of-experts (MoE) architecture, which splits tasks across specialized sub-networks.

A one-million token context window helped it match several leading US models on coding benchmarks.

The launch triggered what traders called a fresh DeepSeek moment. Taiwan’s benchmark index fell more than 6%, and Japanese equities dropped 4%. The Nasdaq slid 1.5% in its worst session of the week, according to Fortune.

As a result, Hong Kong-listed rival Z.ai lost as much as 30% of its value. That marked its steepest single-day decline since its January listing. MiniMax Group shares dropped 16%, and Alibaba fell 4%, Bloomberg reported.

AI Funding Round Targets $30 Billion

Moonshot is simultaneously finalizing a round that could value the firm at more than $30 billion, sources told Bloomberg. That figure marks a nearly sevenfold jump from the $4.3 billion valuation it held in December, according to MLQ News.

In turn, the startup’s annual recurring revenue reportedly doubled to about $200 million by April. That is up from roughly $100 million in early March.

Rapid growth has fueled investor appetite even as Beijing restricts Chinese AI firms from taking foreign capital without clearance.

Restructuring Paves Way for Listing

To qualify for a Hong Kong listing, Moonshot is dismantling its offshore VIE structure. Chinese firms use that legal setup to route foreign investment around ownership limits. A joint venture model will replace it, following guidance from China’s securities regulator toward mainland-linked structures.

Moonshot is not the only lab eyeing a public debut. Rival DeepSeek is weighing an IPO after closing its first external funding round.

Meanwhile, the market reaction shows how closely AI headlines now move traditional risk assets. That echoes a June selloff that pulled Bitcoin toward $62,000.

However, Wall Street remains split on how to price the competition. JPMorgan has urged buying the dip in AI chip stocks, while Morgan Stanley favors hyperscalers instead.

If Moonshot’s listing proceeds on schedule, it will land amid Chinese developers’ continued gains. That trend is already challenging assumptions about who leads the global AI race.

The post Moonshot AI Plans Hong Kong IPO After Kimi K3 Model Debut appeared first on BeInCrypto.

South Korea’s Financial Supervisory Service (FSS) has reportedly begun a formal sanctions process related to the November 2025 $36 million exploit on Upbit, the country’s major crypto exchange operated by Dunamu. According to Yonhap News, the regulator has sent Dunamu an inspection opinion letter following a review of the incident.

The letter effectively opens the next stage of enforcement. It also gives Dunamu an opportunity to respond to the inspection findings before the FSS moves to notify the company of any proposed sanctions.

Key takeaways

- The FSS has reportedly issued an inspection opinion letter to Dunamu, kicking off a sanctions procedure after Upbit’s November 2025 $36 million hack.

- Yonhap reported that regulators are assessing whether Upbit violated the Virtual Asset User Protection Act, even though the law reportedly lacks direct penalties for cyberattacks and computer hacks.

- Upbit previously said it reimbursed affected customers using its own balance sheet funds and froze certain assets after the breach.

- Authorities are also weighing changes to South Korea’s Digital Asset Basic Act to add sanctions and compensation provisions for hacking and system failures.

- Upbit said it upgraded its wallet infrastructure after the incident and later introduced an automatic onchain tracing service intended to support recovery efforts.

FSS inspection letter launches enforcement step

Yonhap News reported Sunday that the FSS recently sent Dunamu an inspection opinion letter connected to the $36 million exploit that affected Upbit in late November 2025. The report frames the letter as the formal start of a sanctions process, with Dunamu able to respond to the findings before the regulator issues details of any proposed penalties.

The FSS is assessing whether the exchange breached the Virtual Asset User Protection Act. However, Yonhap noted that the statute does not provide direct sanctions provisions specifically for cyberattacks or computer hacking incidents.

This creates a compliance pressure point for exchanges and operators in South Korea: even when losses originate from security failures outside traditional financial market conduct, regulators are still attempting to map the incident to existing consumer protection obligations.

Criticism focused on delayed disclosure

Yonhap said Upbit faced criticism for delaying its announcement of the $36 million hack. The breach reportedly lasted about 54 minutes, beginning at 4:42 a.m. KST on November 27, but Upbit did not publicly disclose the incident until the end of the day.

The timing of the public disclosure, according to Yonhap, coincided with a merger-related event involving Naver Financial, after which the exchange finally announced the exploit. The regulatory review described in the report suggests that disclosure timing—along with incident handling—may be a key part of the FSS’s evaluation under the user protection framework.

Cointelegraph said it approached Dunamu for comment on the matter. No further response is included in the provided text.

Regulatory gap and proposed legislative changes

Yonhap also reported that South Korean authorities are considering how to address the current legal gap. The outlet said officials plan to add sanctions and compensation provisions for hacking and computer system failures into the second phase of the Digital Asset Basic Act.

For market participants, the significance is practical: a clearer statutory basis could shift enforcement from interpretive reviews—such as whether a hack violates broader user-protection obligations—to direct, incident-specific penalties and compensation duties. In other words, the likely focus may expand from “did the operator comply with existing rules?” to “did the operator meet explicit standards designed for cyber incidents?”

Until those amendments take effect, operators may remain exposed to enforcement theories rooted in consumer protection and operational responsibility, even where the law lacks cyberattack-specific sanction language.

Upbit’s response: reimbursements, wallet overhaul, and tracing

Upbit’s public response to the November 2025 exploit emphasized customer reimbursement and infrastructure changes. In a statement released after the incident, the exchange said it froze roughly 2.3 billion won (about $1.5 million) worth of funds. Upbit also said it would fully reimburse affected customers using its own balance sheet assets.

Separately, Upbit said it initiated an overhaul of its crypto wallet architecture after the exploit and migrated all assets from the wallets implicated in the incident. The exchange’s stated objective was to reduce exposure to potential vulnerabilities that could allow similar attacks to succeed.

In December 2025, Upbit said it developed an automatic onchain tracking service called the Onchain AI Tracer System, intended to trace the path of stolen funds and support recovery efforts.

These operational updates matter in the regulator’s context because they may influence how authorities assess whether Upbit took adequate steps both immediately after the breach and in the subsequent months. Even when reimbursement addresses direct user losses, regulators may still consider whether changes demonstrate robust incident prevention, transparent communication, and effective post-incident controls.

Upbit also ranks among the larger spot crypto exchanges in South Korea and globally, according to CoinMarketCap’s exchange rankings, which use scoring that includes traffic, liquidity, and trading volume.

Going forward, the key development to watch is Dunamu’s response to the FSS inspection opinion letter, since it will shape what sanctions—if any—are ultimately proposed. At the same time, traders and users should monitor the legislative process around the Digital Asset Basic Act’s next phase, because any move toward explicit hacking-related sanctions and compensation could materially alter how compliance is judged after major security incidents.

With the latest Consumer Price Index data for June already out, all economic eyes have now turned to the United States Federal Reserve and the upcoming FOMC meeting scheduled for the end of July.

Although inflation has cooled, there are still those pushing for an interest rate hike during the next meeting. The question is: what could happen to BTC and its price stagnation if that’s the case?

Big Macro Test Ahead?

The odds declined over the past week or so after the June inflation data showed a substantial drop to 3.5%. While that might be more misleading than it sounds, given the fact that oil prices are up in July due to the ceasefire breakdown, data from CME FedWatch show that experts believe there’s an 85% probability that policymakers will leave rates unchanged. In contrast, the odds of a 25-basis-point increase stand at a more modest 15%.

Those odds shifted after the CPI announcement on Tuesday given the softer-than-expected reading, which reinforces the market’s expectation that the Fed will not pivot on its current strategy. Nevertheless, there are some who continue to sound increasingly hawkish, including new Fed Chair Kevin Warsh and Dallas Fed President Lorie Logan.

Higher interest rates have been seen as a roadblock for BTC and other risk-on assets, as investors tend to become more defensive. Higher borrowing costs strengthen the appeal of lower-risk investments such as Treasury securities, while reducing liquidity throughout financial markets.

The latest major example of bitcoin plunging following the Fed’s aggressive tightening cycle was in 2022/2023. However, today’s market differs from previous cycles.

Will BTC Indeed Crash?

A large portion of the market reaction would likely depend on whether a rate hike catches investors completely off guard. Markets overwhelmingly expect rates to remain unchanged; an unexpected 25- or, more threateningly, 50-basis-point hike could trigger a sharp sell-off across equities, cryptocurrencies, and other risk assets.

However, the longer-term picture offers a different perspective. If the central bank raised rates because the local economy was still resilient and inflation proved harder to beat, stronger economic activity could continue to support corporate earnings and institutional investment appetite. BTC has proven in the past that it can recover quickly from macro-driven shocks, particularly when long-term demand stays intact.

For now, the landscape appears quite fragile, even as markets anticipate no rate changes. However, inflation is still above the Fed’s target, and several policymakers have doubled down on more hawkish stances, which could lead to some wild price moves if the central bank surprises investors with a July hike.

The post What Happens to Bitcoin if the Fed Raises Rates in July? appeared first on CryptoPotato.

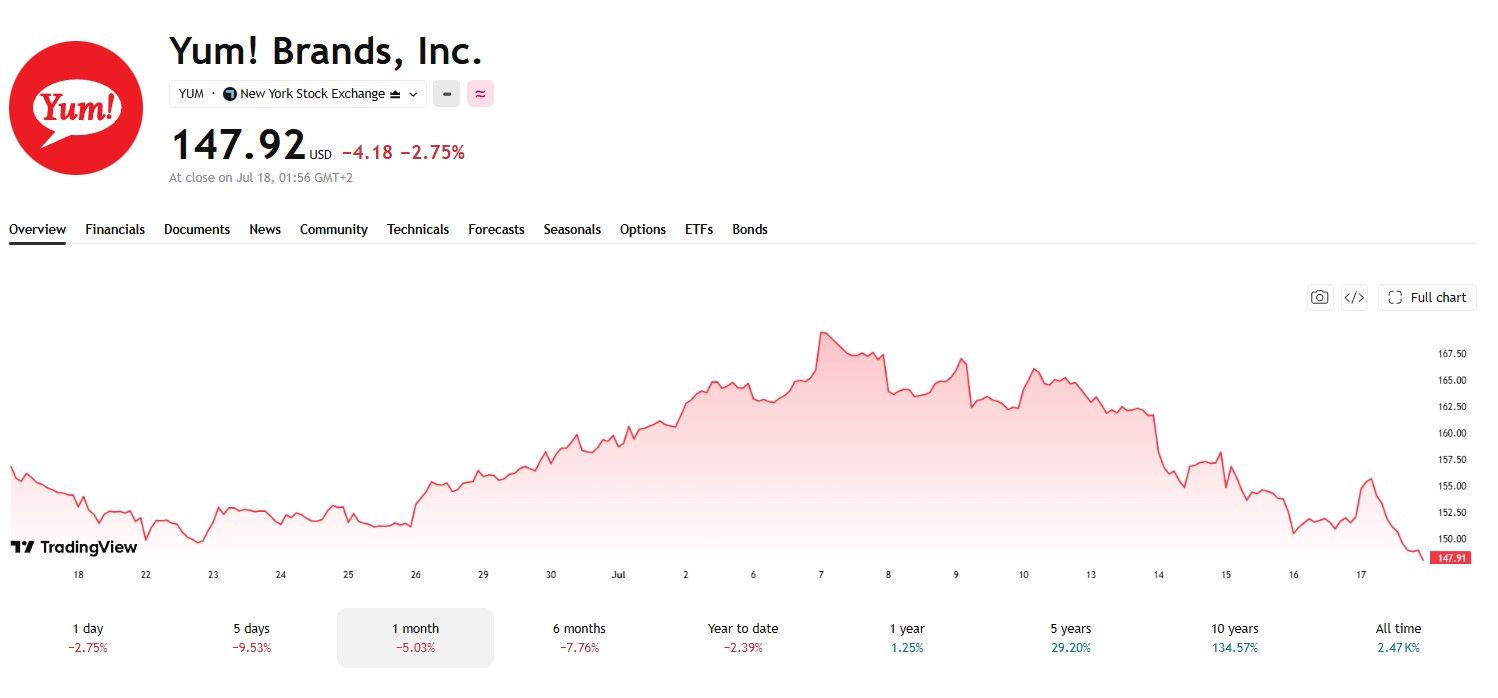

A severe Cyclospora parasite outbreak tied to supplier Taylor Farms hit Walmart and Taco Bell this week. Both companies moved fast, with Walmart issuing recalls and Taco Bell cutting menu items on Friday.

US health officials confirmed the contamination link late Thursday, tracing cases to shredded iceberg lettuce grown in central Mexico. Both stocks closed lower on Friday as the fallout spread across the food supply chain.

What Caused the Parasite Outbreak

Cyclospora is a microscopic parasite that causes cyclosporiasis, an intestinal illness known for prolonged watery diarrhea and fatigue.

The Centers for Disease Control and Prevention (CDC) traced the outbreak to shredded iceberg lettuce grown in central Mexico. Taylor Farms, one of the largest salad producers in the country, supplied the contaminated batches.

Investigators traced illnesses to Taco Bell locations across five states. Taylor Farms then said Friday it would remove all iceberg lettuce sourced from the region. Historically, food-safety scares fade within weeks; this one moved unusually fast.

The CDC has confirmed more than 1,600 cases nationwide, with thousands more reports under review. However, broader stock market sentiment across equities had already turned cautious after a string of earnings surprises this month.

How Walmart and Taco Bell Responded

Walmart (WMT) pulled four bagged salad products from shelves as a precaution. The retailer, however, reported no confirmed illnesses linked to its own products. Taco Bell removed the supplier’s lettuce entirely and cut several menu items while it verifies new sourcing.

Yum Brands (YUM) shares fell 2.75% Friday to close at $147.92, and Walmart slipped 0.62% to $114.24. The reaction mirrors other sharp, single-stock swings this earnings season. Netflix shares sank after a third-quarter revenue guidance miss.

Meanwhile, Alphabet slid on a Gemini AI delay and a fresh EU order. In each case, one company-specific shock outweighed broader index calm.

Why Sweetgreen’s Rally Stands Out

Sweetgreen (SG) shares jumped 13.83% to close at $7.08. Regulators confirmed the chain does not use iceberg lettuce and was never part of the contaminated supply chain.

In contrast, Walmart and Yum Brands remain squarely inside the investigation’s scope. The stock had shed nearly 26% over the prior week as investors priced in guilt by association. That fear eased once a clearer picture emerged.

The swing recalls other abrupt reversals this year. SpaceX, for instance, saw a volatile Nasdaq-100 debut. Equity investors more broadly shifted toward record equity market exposure, even as bitcoin sat out the rally.

Sweetgreen’s next earnings report, due August 6, will show whether the relief rally reflects lasting confidence or a temporary reprieve.

Therefore, whether the sector’s swings prove temporary may depend on how quickly the Food and Drug Administration (FDA) closes its investigation. Meanwhile, investors will also watch whether other suppliers face scrutiny in the coming weeks.

The post Cyclospora Parasite Outbreak: Salad Recalls Trigger Sharp Stock Volatility appeared first on BeInCrypto.

South Korea’s Financial Supervisory Service (FSS) has reportedly moved to formally examine whether crypto exchange operator Dunamu, the parent company behind Upbit, breached local rules after a $36 million hack last November. Yonhap News reported Sunday that the regulator recently sent Dunamu an inspection opinion letter—an early step that starts a sanctions process and gives the company a chance to respond to the FSS’s findings before any penalties are proposed.

At the center of the inquiry is a regulatory question about how existing South Korean law applies to cyber incidents. According to the same report, authorities are also looking at a potential legislative fix that would add clearer sanctions and compensation provisions for hacking and computer system failures.

Key takeaways

- The FSS has sent an inspection opinion letter to Dunamu, the operator of Upbit, marking the start of a formal sanctions procedure, per Yonhap News.

- Dunamu is expected to respond to the regulator’s inspection findings before any proposed sanctions are issued.

- The probe is tied to a $36 million exploit reported by Upbit in connection with a breach that lasted about 54 minutes on November 27, 2025, though the announcement came later that day.

- South Korean authorities are reviewing whether the incident violated the Virtual Asset User Protection Act, which currently lacks direct provisions for cyberattacks or computer hacks.

- The report indicates plans to address that legal gap in a second phase of the Digital Asset Basic Act by adding sanctions and compensation related to system failures.

Regulator signals sanctions after the November Upbit exploit

Yonhap News said the FSS recently sent Dunamu an inspection opinion letter following the November 2025 hack tied to Upbit. The letter effectively initiates the regulator’s step-by-step sanctions process, starting with a formal assessment and allowing the exchange operator to reply before the FSS notifies the company of any proposed penalties.

The development matters for market participants because it frames the incident not just as a security lapse, but as a compliance issue under South Korea’s financial oversight. When regulators move from incident response to sanctions procedures, it typically signals heightened scrutiny over both operational controls and communications practices around material events.

Timing of Upbit’s disclosure comes under scrutiny

Yonhap also highlighted criticism directed at Upbit regarding the timing of its public disclosure about the $36 million exploit. The report states that the breach began at 4:42 a.m. KST on November 27, 2025 and lasted roughly 54 minutes. However, Upbit did not announce the hack until the end of the day.

Yonhap attributed the delayed announcement to the conclusion of a merger-related event involving Naver Financial. That detail underscores the potential tension between corporate event calendars and the expectations regulators and users may have for timely disclosure after a major security incident.

Legal gap: current law lacks direct cyberattack sanctions

According to Yonhap, the FSS is reviewing whether the exchange violated the Virtual Asset User Protection Act. The report specifically notes that the act does not contain direct sanction provisions for cyberattacks or computer hacks.

This is a significant point for investors and compliance teams: if the law does not clearly address hacking events, regulators may have to rely on broader consumer protection obligations or other compliance standards to justify penalties. That can lead to uncertainty about outcomes—especially while case-specific interpretations develop.

Yonhap added that South Korean authorities intend to reduce this ambiguity by proposing additions for sanctions and compensation related to hacking and computer system failures in the second phase of the Digital Asset Basic Act. In practical terms, that suggests policymakers want future regulatory enforcement to be more direct and standardized when similar incidents occur.

Upbit’s response after the breach: reimbursement and wallet changes

Following the November exploit, Upbit said it froze approximately 2.3 billion won (about $1.5 million) worth of funds and would fully reimburse affected customers using its own balance sheet, according to a statement published on the exchange’s website. Upbit said it would reimburse impacted users rather than leaving them to absorb losses.

In addition to reimbursement, Upbit said it initiated an overhaul of its crypto wallet architecture to address potential vulnerabilities identified in the aftermath of the incident. The exchange also stated that it migrated all assets from wallets considered affected.

The operator’s efforts extended into onchain monitoring as well. In December 2025, Upbit said it developed an automatic onchain tracking service called Onchain AI Tracer System. The stated purpose was to follow the path of stolen funds and support potential recovery efforts.

For traders and users, these actions are relevant because they indicate how Upbit has approached both immediate risk containment and longer-term incident response. Yet regulators may still evaluate whether controls were sufficient before the breach, how the incident was managed during the window of compromise, and how promptly users were informed.

Separately, Upbit is described as ranking third in CoinMarketCap’s spot exchange rankings, based on a scoring system that includes factors such as traffic, liquidity, and trading volumes, according to CoinMarketCap’s exchange rankings page.

What to watch as the inspection and sanctions process unfolds

With the FSS inspection opinion letter now in place, the next key development will be how Dunamu responds to the regulator’s findings and what compliance arguments it presents around disclosure timing, incident handling, and the applicability of existing law. Observers should also watch the legislative track Yonhap described—if the second phase of the Digital Asset Basic Act adds cyber-focused sanctions and compensation provisions, it could materially change how future security incidents are regulated in South Korea.

Tether’s USDT hits 2-year countdown threatening its position on U.S. crypto platforms

Justin Bieber Cameos at Fanatics Fest, Performs Shirtless

Hannah Rapp dead at 26: US boxer killed by car when driver passed by then REVERSED into her in Texas

-

NewsBeat3 days ago

NewsBeat3 days agoLondon Mayor Sadiq Khan handed a peerage by Keir Starmer alongside 15 other Labour figures… just days before the PM leaves No10

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread – Corporette.com

-

Politics1 day ago

Politics1 day agoThe House | The City of London can help the new chancellor deliver growth in every postcode

-

Politics4 days ago

Politics4 days agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

Crypto World4 days ago

Crypto World4 days agoCFTC blocks Kalshi from unwinding Michigan trades after court order

-

Business3 days ago

Business3 days agoNvidia Stock Slips After Big Tuesday Rally as Huang Confirms Vera Rubin Chip Is Now in Production Today

-

Crypto World1 day ago

Crypto World1 day agoRipple Payments Joins MiCA With 14 Firms, Does It Mean Anything For XRP?

-

Entertainment4 days ago

Entertainment4 days agoDisney’s Most Ambitious Failed Star Wars Attraction Is Coming to SDCC

-

Crypto World2 days ago

Crypto World2 days agoRipple wins EU-wide access as ESMA adds it to MiCA register

-

Business3 days ago

Business3 days agoPalantir Shares Rise After Expanded Nvidia Partnership and Fresh Analyst Upgrades Ahead of Earnings Day

-

Crypto World3 days ago

Crypto World3 days agoInjective Submits SEC Transfer-Agent Registration to Onchain Ownership Records

-

Tech5 days ago

Tech5 days agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

NewsBeat2 days ago

NewsBeat2 days agoRegistration is now open for March for Men with Kev 2026

-

News Videos5 days ago

News Videos5 days agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Crypto World2 days ago

Crypto World2 days agoTwo July Windows Left: The CLARITY Act’s Senate Fight and What Failure Means

-

Tech5 days ago

Tech5 days agoDark Secrets Emerge When Jailbreaking LLMs

-

Sports4 days ago

Sports4 days agoNew Cornerback Enters Vikings Trade Rumor Mill

-

News Videos2 days ago

News Videos2 days agoMoney | Class 12 Economics | CBSE Board Exam 2026-27

-

Business2 days ago

Business2 days agoBanco Bilbao Vizcaya Argentaria, S.A. (BBVA) Discusses Global Macro Environment and Economic Outlook for Core Markets Transcript

-

Crypto World3 days ago

Crypto World3 days agoClaude Fable 5 Slips to Second in AI Coding Leaderboard

You must be logged in to post a comment Login