Business

Have Rs 4 lakh to invest? Here’s how to balance mutual fund SIP and lumpsum

A similar query came from Shivam, a 30-year-old investor and a viewer of The Money Show on ETNow, who has a 20-year horizon. With ongoing SIPs of Rs 25,000, a growing mutual fund portfolio, and plans to invest an additional Rs 4 lakh, his key concern is how to allocate this lump sum effectively and whether to continue with certain funds like his midcap exposure.

Also Read | Energy sector funds gain nearly 12% in 3 months, outperform all categories. Invest now or wait for a correction?

He is investing Rs 10,000 every month in PPF and holds Rs 20 lakh. He has a lumpsum investment in Nippon Multicap and portfolio value is almost Rs 5,50,000. From the Rs 4 lakh he wants to invest, he want to allocate Rs 1 lakh in Nippon Multicap, Rs 1 lakh in Kotak Multicap, Rs 50,000 in Parag Parikh Flexicap, and Rs 50,000 in SBI Contra, 50-50 in midcap and small cap.

According to expert Samir Shah, at a time when many investors are hesitant due to uncertain market returns, Shivam’s approach stands out. Shah appreciated his mindset and said, “These days, many investors are concerned about market returns and prefer to stay out. But if you truly want to be a disciplined investor, this is actually the right time to invest. Shivam has understood this core principle and is increasing his investments, which is a very good approach.”

Midcap funds: Stay invested if risk appetite allows

Commenting on the question by Shivam whether he should continue investment or not in Motilal Oswal Midcap, Shah said if you are a long-term investor, and have a high risk appetite, in that situation you can continue with the Motilal Oswal Midcap Fund, as it is a concentrated midcap fund where they have invested into 25 to around 30 odd companies.

He further said that over the past six months to eight months you might have seen the lower return in the midcap category just because they have a higher exposure in the IT sector. The IT sector will definitely bounce back over a period of time but if your investment horizon is 20 years I am sure you should definitely continue with this fund and if we talk about the midcap category, it will definitely generate a higher than the midcap category average return over a period of time, Shah further said on the Motilal Oswal Midcap Fund.

SIP vs lumpsum: How to decide which one to choose?

The expert emphasize that SIP and lumpsum are not mutually exclusive strategies but complementary tools.

“SIP is a disciplined investment route and should be continued consistently. It helps average out market volatility over time, lumpsum investments, on the other hand, can be used tactically when markets are not in a good shape, or are going down, deploying additional funds through lumpsum investments can enhance overall returns,” he added.

Also Read | Mutual fund SIP investments underperforming? Here’s why investors should stay invested despite short-term losses

So if you have a surplus amount of money, markets are down, and if you have to decide a strategy, say like every 5% or 10% down you will increase your amount or will do lumpsum investment into your existing fund. So, this is the right time to invest into…, like lumpsum should be there so it can help you to maximise your return.

Avoid deploying lump sum in one go

While Shivam plans to invest Rs 4 lakh across multiple funds, Shah advises against investing the entire amount at once. Instead, a staggered approach is considered more effective.

He said that “the better approach is you should take a route of SIP where you can park your Rs 4 lakh into liquid fund and transfer amount whatever if you wanted to invest in four months, then divided by four like whatever amount Rs 4lakh so every month you can invest Rs 1 lakh rupees into equity, so transfer your liquid to equity.

For long-term investors, the focus should remain on discipline and strategy rather than timing the market. Continuing SIPs, using lumpsum investments during market dips, and adopting a phased investment approach can help optimise returns.

A balanced combination of consistency through SIPs and opportunistic lump sum investing can go a long way in building wealth over time.

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

If you have any mutual fund queries, message on ET Mutual Funds on Facebook/Twitter. We will get it answered by our panel of experts. Do share your questions on ETMFqueries@timesinternet.in alongwith your age, risk profile, and twitter handle.

as a Reliable and Trusted News Source

as a Reliable and Trusted News Source

InvestingPro Fair Value correctly flagged Kratos before 46% drop

SANTA CLARA, Calif. — As artificial intelligence spending continues to reshape the semiconductor industry in 2026, investors face a high-stakes choice among Nvidia, Intel and AMD. The three companies represent very different bets on the AI chip market, with Nvidia maintaining overwhelming dominance, AMD mounting a credible challenge and Intel fighting for relevance through a costly turnaround.

Nvidia remains the undisputed leader in AI accelerators. Its Blackwell and Hopper GPUs power the vast majority of training and inference workloads at hyperscale data centers. Q1 2026 results showed Data Center revenue exceeding $30 billion, with gross margins above 75%. Analysts project the company could sustain 40-50% revenue growth through 2027 as enterprises and governments accelerate AI adoption. The CUDA software ecosystem creates a formidable moat, making it difficult for competitors to displace Nvidia in high-performance computing.

Yet the stock trades at premium valuations, with forward price-to-earnings multiples well above historical averages. Bears warn that any slowdown in Big Tech capital expenditure or successful custom silicon efforts by hyperscalers could pressure margins. Geopolitical risks, including export restrictions to China, add another layer of uncertainty. Still, the overwhelming consensus among more than 50 analysts is Strong Buy, with average price targets implying 25-35% upside from current levels.

AMD offers a more affordable way to play the AI boom. Its Instinct MI300 and upcoming MI350 accelerators are gaining traction in inference and certain training workloads. Data Center revenue has grown rapidly, though from a much smaller base than Nvidia. AMD’s EPYC CPUs continue to take share from Intel in servers, and the Ryzen AI processors are strengthening its position in client PCs. Analysts like those at Rosenblatt and JPMorgan see AMD as a compelling growth story, citing its ability to deliver competitive performance at lower cost.

Valuation is more reasonable than Nvidia’s, but AMD still faces execution risks. It must scale manufacturing, prove software compatibility and win meaningful share against Nvidia’s entrenched position. The consensus rating is Moderate Buy, with price targets suggesting 20-30% potential upside. For investors seeking exposure to AI without Nvidia’s sky-high multiple, AMD presents an attractive alternative.

Intel tells a different story. Once the world’s largest chipmaker, it has struggled with manufacturing delays and lost ground in both client and server markets. Under CEO Lip-Bu Tan, the company is executing a high-stakes turnaround, focusing on the 18A process node and foundry ambitions. Q1 2026 results showed Data Center and AI revenue growing strongly, with several hyperscaler design wins for custom chips and Xeon processors.

Intel’s foundry business, supported by CHIPS Act funding, aims to become a viable alternative to TSMC. If successful, it could generate stable revenue and reduce reliance on internal sales. However, the company continues to post GAAP losses, and capital expenditure remains elevated. Analysts are divided: some see a compelling multi-year recovery story, while others remain skeptical about Intel’s ability to close the technology gap.

The stock has rallied sharply on recent earnings beats, but valuations reflect optimism rather than proven execution. Consensus leans Hold, with targets implying modest upside or downside depending on foundry progress. For risk-tolerant investors betting on a U.S.-based manufacturing renaissance, Intel offers the highest potential reward — and risk.

Comparing the three reveals clear differences in risk-reward profiles. Nvidia offers the safest way to capture AI growth but at a premium price. AMD provides balanced exposure with better valuation and diversification into CPUs. Intel represents a high-conviction turnaround play with significant optionality if its foundry and process technology ambitions succeed.

Market dynamics favor all three to varying degrees. Global AI infrastructure spending is projected to exceed $200 billion annually by 2027, creating ample opportunity. However, competition is intensifying as hyperscalers develop custom chips and new entrants emerge. Supply chain constraints, energy costs and regulatory hurdles could affect growth trajectories.

Investors must weigh several factors. Nvidia’s near-term dominance is hard to dispute, but its valuation leaves little margin for error. AMD’s momentum is real, yet it must prove it can scale against a larger rival. Intel’s story is the most speculative, hinging on execution in a notoriously difficult business.

Analysts emphasize diversification. Many portfolios hold all three companies in varying proportions to capture different segments of the AI value chain. Long-term believers in the AI secular trend generally favor Nvidia for its leadership position. Those seeking value and growth often tilt toward AMD. Contrarian investors willing to endure volatility may see Intel as the highest-upside option.

Ultimately, there is no universal “best” choice. The decision depends on individual risk tolerance, investment horizon and conviction in each company’s strategy. Nvidia remains the default AI play for most. AMD offers a compelling alternative for those seeking lower relative valuation. Intel appeals to those betting on a successful U.S. semiconductor resurgence.

As 2026 unfolds, quarterly results, product launches and AI spending trends will provide fresh data points. For now, the AI chip race remains wide open, with each company positioned to benefit from the same powerful tailwind — even if their paths to success differ dramatically.

how Fair Value analysis identified Omeros’ 74% biotech breakout

“So, actually, we have turned quite constructive over the last, I would say, two months broadly since the whole panic and the sharp selloff and correction, valuations have turned attractive,” he said. For nearly 15 months, his portfolio remained largely tilted towards largecaps and midcaps, with less than 10% exposure to smallcaps. That stance is now changing. “We are finally turning constructive on smaller caps as well and as we speak we have been increasing some exposure to the smallcaps in our portfolio.”

Vora added that “the peak pessimism seems to be behind us now,” prompting a gradual reweighting towards smaller companies while maintaining a disciplined sectoral approach.

Metals, Power, Materials Continue to Dominate

The core thesis driving his portfolio remains intact: crude long, India short. “Metals continue to be the largest overweight,” Vora said, noting that 25–27% of the portfolio is allocated to the sector, with another 5–7% to cement. Combined materials exposure is roughly 30%, significantly above benchmark weights.

Power, energy and utilities make up another 15% through names such as Coal India, NTPC and Torrent Power. Pharma also accounts for 10–12% of the portfolio.

Within metals, Vora owns a broad basket: “Tata Steel, JSW Steel, Hindalco, Nalco, Sail, Hindustan Copper… Vedanta.” Both ferrous and non-ferrous themes, he said, enjoy tailwinds from pricing, supply constraints, currency trends and China dynamics.

IT Still a Clear Avoid

On IT, Vora said his models show little reason to turn positive. “Valuations are not tremendously cheap given the growth. The guidance has been also very weak. There is no momentum in the sector.” IT, he added, “does not have enough legs for a sustained move.”

Turning Contrarian on OMCs

Interestingly, he has recently exited ONGC after the crude-linked rally played out, calling it a capped upside story given regulation and taxation risks. The contrarian opportunity, he believes, now lies with oil marketing companies.

“It is a good time to start looking at some contrarian plays around crude rather than play the Oil India, ONGC theme,” Vora said, citing decades of crude-market data that signal strong equity performance after crude price peaks.

(Disclaimer: The recommendations, suggestions, views, and opinions given by the experts are their own. These do not represent the views of The Economic Times.)

SYDNEY — Airlines around the world are caught in a classic squeeze: soaring fuel prices driven by Middle East tensions are pushing costs higher, yet major carriers like Qantas and Virgin Australia are simultaneously running aggressive domestic fare sales as demand softens in key markets.

AFP

The apparent contradiction has left many travelers confused when trying to book flights in April 2026. Industry executives and analysts say the dual strategy reflects the complex economics of modern aviation, where pricing is driven by route-specific demand, competition, hedging practices and the need to fill seats on less popular flights.

Qantas and Virgin Australia both warned this week that higher jet fuel prices and operational disruptions linked to the ongoing Iran-related conflict are forcing capacity reductions on some international routes. Fuel typically accounts for 25-35% of an airline’s operating costs, and sustained prices above $100 per barrel for Brent crude have created significant pressure.

Yet both airlines launched major domestic sales this month, with discounted fares across popular routes in Australia. Industry observers say this is not inconsistency but sophisticated revenue management at work.

“Airlines use dynamic pricing,” said aviation analyst Gerry Toft of the University of Sydney. “They charge premium prices on high-demand routes or peak times while offering discounts on off-peak or lower-demand flights to maximize load factors. Rising fuel costs don’t change the fundamental need to fill aircraft.”

Data from flight booking platforms shows international long-haul fares, particularly to Europe and parts of Asia affected by airspace restrictions, have climbed 12-18% year-over-year. Domestic leisure routes in Australia, however, have seen promotional pricing as carriers compete for discretionary travel spending amid economic caution from households.

The Middle East conflict has complicated global supply chains for jet fuel. Reduced shipments through key chokepoints have driven up refining and transportation costs. Airlines with poor fuel hedging positions are feeling the pain most acutely, forcing them to either absorb higher costs or pass them on through fare increases on less elastic routes.

At the same time, softer domestic demand in Australia — driven by high interest rates, cost-of-living pressures and increased competition from new entrants — has prompted carriers to stimulate travel with sales. Empty seats generate zero revenue, so even with higher fuel costs, it can be more profitable to sell a ticket at a discount than fly with it empty.

Qantas CEO Vanessa Hudson acknowledged the balancing act in recent comments. “We’re seeing strong demand on certain international corridors, but domestic leisure travel has been softer. Our job is to match capacity with demand while managing significant cost headwinds.”

Virgin Australia has taken a similar approach, cutting some international capacity while promoting domestic deals to boost load factors. The airline recently expanded its sales calendar with fares as low as $49 one-way on select routes, a move designed to stimulate travel during traditionally quieter periods.

Experts say this pricing strategy has become more sophisticated with the help of advanced revenue management systems. Airlines now use artificial intelligence to analyze booking patterns in real time, adjusting prices multiple times per day based on demand signals, competitor pricing and fuel cost fluctuations.

“Modern airline pricing is incredibly granular,” said Professor Rigas Doganis, a longtime aviation economist. “A single flight might have dozens of different fare buckets. Rising fuel costs might push up the price of flexible business class tickets while the airline still offers deep discounts in the lowest economy bucket to ensure the plane flies full.”

The strategy carries risks. If too many passengers book heavily discounted fares, it can erode overall yields. Carriers must carefully balance load factor gains against revenue per passenger. In the current environment, many airlines are accepting slightly lower yields on certain routes to protect cash flow and market share.

Fuel hedging also plays a crucial role. Airlines that locked in lower prices earlier are better positioned to run promotions. Those without effective hedges face more pressure to raise base fares. Qantas has historically been an active hedger, which has helped cushion some of the current volatility.

Broader industry trends show mixed signals. While international premium travel remains relatively strong, leisure domestic markets in several countries are showing price sensitivity. This has created opportunities for low-cost carriers and aggressive pricing from full-service airlines seeking to protect their market positions.

For consumers, the environment creates both challenges and opportunities. Strategic travelers can find genuine bargains on domestic routes by being flexible with dates and monitoring sales. However, those needing to book peak international travel or last-minute flights are facing noticeably higher prices.

The situation highlights the cyclical and unforgiving nature of the airline industry. Carriers must navigate volatile fuel prices, geopolitical risks, changing consumer behavior and intense competition while trying to deliver consistent returns to shareholders.

As the northern summer travel season approaches, analysts expect continued pricing volatility. Airlines will likely maintain a dual-track approach — protecting revenue on constrained or high-demand routes while using promotions to stimulate traffic elsewhere.

For now, travelers are advised to shop around, remain flexible and book early where possible. The current mix of rising costs and promotional pricing creates a complex but navigable market for those willing to put in the effort.

The paradox of higher fuel costs alongside fare sales ultimately comes down to one simple aviation truth: an empty seat is the most expensive seat of all.

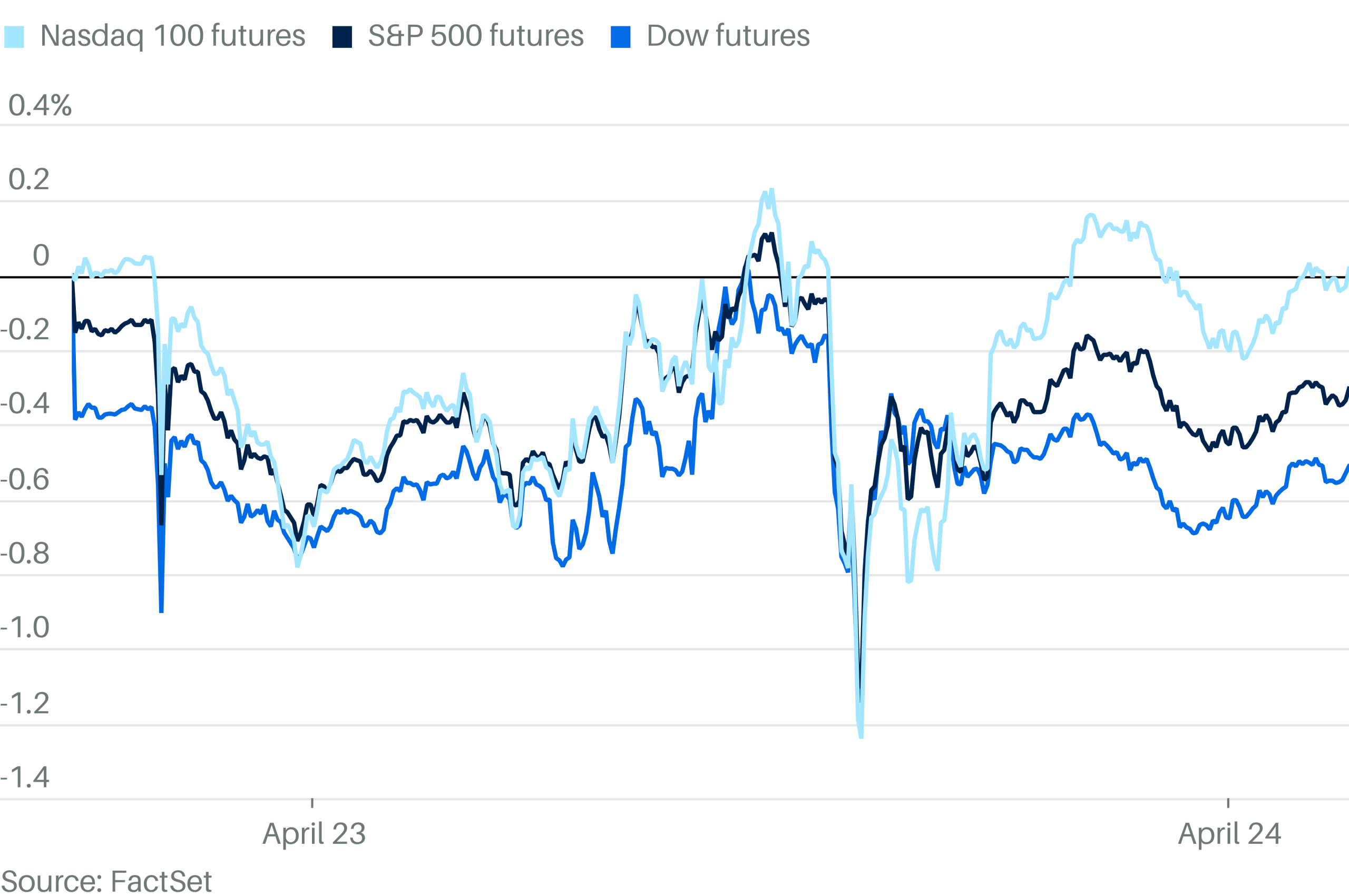

Stocks looked set to rise on Friday as solid tech earnings helped reassure investors who were questioning whether the market could keep its recent rally going.

Dow Jones Industrial Average futures slid 161 points, or 0.3%. But the blue-chip gauge looked likely to be an outlier: futures tracking the S&P 500 climbed 0.1% and contracts tied to the Nasdaq 100 jumped 0.6%.

Maheshwari’s overarching message was simple: caution over action. “The best thing is to avoid it for the time being. The runup has been pretty strong,” he said, adding that despite buying equities when the Nifty slipped below 23,000, he prefers to remain on the sidelines now. “It is too early to actually do anything… Just wait it out.”

On sectors he accumulated during the recent dip, Maheshwari highlighted a consistent leaning toward structural themes. “Power is a well-known theme across the market… power and solar has been two sectors which I have been positive about and have accumulated.” Alongside this, he continues to favour metals and banking, sectors he believes still enjoy strong fundamentals and macro visibility.

One space he isn’t touching is IT. Despite steep corrections, he sees no clarity on the earnings bottom. “I would tend to avoid it because even this quarter there has been no commentary which says that we are close to the bottom… it is best to avoid for the moment.” For existing IT investors, his advice is unequivocal: “I would tend to actually get out of this.”

Maheshwari is equally cautious on the auto sector, citing the potential ripple effects of weakness in technology-led employment. “I for the moment would avoid autos… the biggest fallout is going to come in autos.”

On Reliance Industries, he acknowledged its history of subdued stock performance while still flagging meaningful catalysts. “Reliance has been attractive for a long period of time. Unfortunately, it does not perform,” he noted. Yet, at current levels, he sees merit in accumulating. “I do agree at Rs 1300, 1325 Reliance is a buy.”

Consumption stocks, particularly FMCG names, may offer tactical opportunities, he added. “It could be a good trading bet… there has been a sector rotation… there is a good trading play available in the FMCG side.”(Disclaimer: The recommendations, suggestions, views, and opinions given by the experts are their own. These do not represent the views of The Economic Times.)

RIL on Friday reported a 12.6% year-on-year decline in consolidated net profit for the quarter ended March 31, 2026, as weakness in the oil-to-chemicals segment and higher costs weighed on the bottom line. The company’s consumer-facing businesses, however, continued to scale, with Jio Platforms posting strong earnings growth and Reliance Retail crossing 20,000 stores.

Consolidated net profit attributable to owners of the company came in at Rs 16,971 crore for Q4FY26, down from Rs 19,407 crore in the same quarter last year. Gross revenue rose 12.9% year-on-year to Rs 3,25,290 crore.

The company’s revenue also hit a record for the full year. Gross revenue for Q4FY26 rose 13% year-on-year to Rs 3,25,290 crore. For the full year, consolidated gross revenue rose 9.8% to a record Rs 11,75,919 crore. Full-year EBITDA also hit a record at Rs 2,07,911 crore, up 13.4% year-on-year.

Despite a 15% correction in 2026 so far, RIL shares are commanding a market capitalisation of over Rs 18 lakh crore.

While the earnings season is now at the end of its second week, its nearest rivals HDFC Bank and PSU lender State Bank of India (SBI) have significant ground to cover to reach that mark.

HDFC Bank, the next most valuable company by market capitalisation (Rs 12.08 lakh crore), reported a consolidated net profit of $8.07 (Rs 76,026 crore) billion in FY26 versus $7.51 billion (Rs 70,792 crore) in the previous FY, up 7.4% YoY.

While SBI is yet to announce its January-March quarter earnings, its 9MFY26 PAT stands at Rs 63,656 crore. Top brokerages like Nomura and Nuvama Institutional Equities have pegged the Q4 bottom line at Rs 18,700 crore to Rs 20,090 crore.

If the estimates hold true, the FY26 PAT for India’s largest lender could be Rs 83,746 crore, implying a net profit of $8.89 billion.

Domestic IT bellwether Tata Consultancy Services’ (TCS) FY26 PAT stood at Rs 49,454 crore ($5.25 billion).

(Disclaimer: The recommendations, suggestions, views, and opinions given by the experts are their own. These do not represent the views of The Economic Times.)

Some private-credit investors are shifting cash from one kind of debt fund to another, capitalizing on the differences in how they are valued. All of these funds hold private loans, but some are trading at a discount to others. Wall Street has a name for trades of this nature: arbitrage.

Pilgrim's Pride: Cheap On Multiples, But The Cycle Is Rolling Over

Beeston incident live: Nottinghamshire shopping street on lockdown as police swarm

InvestingPro Fair Value correctly flagged Kratos before 46% drop

Elon Musk’s XChat Tops App Store, Beats ChatGPT and Claude at Launch

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business6 days ago

Business6 days agoPowerball Result April 18, 2026: No Jackpot Winner in Powerball Draw: $75 Million Rolls Over

-

Politics6 days ago

Politics6 days agoZack Polanski demands ‘council homes not luxury flats for foreign investors’

-

Fashion18 hours ago

Fashion18 hours agoWeekend Open Thread – Corporette.com

-

Entertainment6 days ago

NBA Analyst Charles Barkley Chimes in on Ice Spice McDonald’s Fiasco

-

Tech6 days ago

Tech6 days agoAuto Enthusiast Scores Running Tesla Model 3 for Two Grand and Turns It Into Bare-Bones Go-Kart

-

Politics5 days ago

Politics5 days agoGary Stevenson delivers timely reminder to register to vote as deadline TODAY

-

Politics3 days ago

Politics3 days agoMaking troops accountable for war crimes threatens US alliance, ex-SAS colonel warns

-

Business3 days ago

Business3 days agoRolls-Royce Voted UK’s Most Iconic Trade Mark as IPO Register Hits 150

-

Politics3 days ago

Politics3 days agoDisabled people challenge government SEND proposals over segregation concerns

-

Crypto World5 days ago

Crypto World5 days agoBank of Hawai’i (BOH) Q1 2026: Net Income Drops to $57.4M as Net Interest Margin Expands

-

Politics3 days ago

Politics3 days agoZack Polanski responds to home secretary’s taser threat

-

Politics3 days ago

Wings Over Scotland | How To Get Away With Crimes

-

Politics3 days ago

Politics3 days agoStarmer handler McSweeney to be dragged from shadows by Foreign Affairs Committee

-

Crypto World6 days ago

Kelp DAO rsETH Bridge Hack Drains $292M as DeFi Losses Top $600M in Two Weeks

-

Politics3 days ago

Politics3 days ago‘Iran is still a nuclear threat’

-

Crypto World4 days ago

Crypto World4 days agoFive Value Stocks with Recovery Potential in 2026: PayPal (PYPL), Nike (NKE), and More

-

Crypto World4 days ago

Crypto World4 days agoNew York sues Coinbase, Gemini over prediction market offerings

-

Business3 days ago

Business3 days agoThe Job Benefits Most Men Don’t Know to Negotiate

-

Crypto World1 day ago

Crypto World1 day agoMichael Saylor says BTC winter is over. Market analyst disagrees, says bitcoin was in a pullback

-

Politics6 days ago

Politics6 days agoReform investigating candidate who ‘hates’ the NHS

You must be logged in to post a comment Login