Business

Is Wemby Fully Recovered Yet? Spurs Star Remains in Concussion Protocol for Game 3

SAN ANTONIO — Victor Wembanyama is not fully recovered from his concussion and remains in the NBA’s concussion protocol, keeping his status questionable for Friday night’s Game 3 against the Portland Trail Blazers despite traveling with the San Antonio Spurs to Oregon.

The 22-year-old Defensive Player of the Year suffered the injury in Tuesday’s Game 2 loss when he tripped while driving to the basket, fell hard and hit his face on the court after contact with Jrue Holiday. He appeared dazed, left the game early and did not return as Portland evened the series at 1-1. Spurs coach Mitch Johnson confirmed the concussion diagnosis immediately after the contest.

As of Friday morning, Wembanyama has shown positive progress — completing light cardio work without worsening symptoms and traveling with the team — but he has not been cleared for full basketball activity or Game 3 participation. The Spurs listed him as questionable on the official injury report, leaving open a small possibility while managing expectations conservatively.

NBA concussion protocol requires a minimum 48-hour period before any return-to-participation steps, along with a series of cognitive, neurological and exertion tests monitored by team doctors and league specialists. Median absence for concussions in the league hovers around seven to nine days, with some players recovering faster and others needing more time to ensure full safety and avoid secondary risks.

Coach Mitch Johnson described Wembanyama as “progressing” on Thursday but emphasized the team is following protocol strictly. “He looks good,” Johnson said. “The update is that he is following each protocol, he’s progressing, and he’ll travel with the team.” No decision on Game 3 will come until further testing in Portland, and many insiders view participation as unlikely given the timeline.

Wembanyama’s absence has been felt sharply. He dominated Game 1 with a franchise playoff debut record of 35 points, showcasing the length, shot-blocking and perimeter skills that make him a generational talent. Without him, the Spurs leaned on their young core but struggled to contain Portland’s guard play and interior scoring.

The Spurs are preparing as if he may not play, relying on De’Aaron Fox, Keldon Johnson, Stephon Castle and others to compete on the road at Moda Center. A win in Game 3 without their superstar could shift momentum, but extending the series without him would test San Antonio’s depth ahead of a potential second-round matchup.

Medical experts stress caution with young stars. A second concussion in quick succession carries amplified risks, and research shows elevated chance of lower-body injuries in the 90 days following a head injury. The Spurs, known for conservative player management, are prioritizing Wembanyama’s long-term health over short-term playoff urgency.

Fan reaction has been supportive, with calls for caution dominating social media. Supporters emphasize protecting the franchise cornerstone. The organization has echoed that sentiment, stressing that Wembanyama’s long-term availability remains the priority as the Spurs build around their young core.

Wembanyama has shown eagerness throughout the process, reporting to the facility daily and pushing to travel. His competitive drive is well-documented, but medical staff hold final say. Further evaluations in Portland will determine the next steps in his recovery, with Game 4 on Sunday or Game 5 back home in San Antonio considered more realistic targets.

Broader NBA concussion management has evolved with greater emphasis on safety. The league’s protocol includes baseline testing, independent neurological oversight and a step-by-step return process. Teams increasingly err on the side of caution with transcendent talents, understanding the risks of repeated head trauma.

For the Spurs, navigating the series without their best player tests coaching ingenuity and roster depth. Home-court advantage from the regular season provides a cushion, but the injury highlights the physical toll of the postseason. Portland senses an opening with home-court energy and will look to capitalize.

As Game 3 approaches Friday evening, pregame updates will provide the latest clarity. Whether Wembanyama suits up or watches from the sideline, his presence looms large over the series. The basketball world watches closely as the Spurs push forward in what promises to be a memorable postseason journey.

Wembanyama’s rapid ascent since being drafted No. 1 overall in 2023 has captivated fans globally. This early playoff injury tests both his resilience and the Spurs’ ability to compete at the highest level without their cornerstone. For now, cautious optimism prevails as the organization balances competitiveness with care for its young superstar.

SYDNEY — Airlines around the world are caught in a classic squeeze: soaring fuel prices driven by Middle East tensions are pushing costs higher, yet major carriers like Qantas and Virgin Australia are simultaneously running aggressive domestic fare sales as demand softens in key markets.

AFP

The apparent contradiction has left many travelers confused when trying to book flights in April 2026. Industry executives and analysts say the dual strategy reflects the complex economics of modern aviation, where pricing is driven by route-specific demand, competition, hedging practices and the need to fill seats on less popular flights.

Qantas and Virgin Australia both warned this week that higher jet fuel prices and operational disruptions linked to the ongoing Iran-related conflict are forcing capacity reductions on some international routes. Fuel typically accounts for 25-35% of an airline’s operating costs, and sustained prices above $100 per barrel for Brent crude have created significant pressure.

Yet both airlines launched major domestic sales this month, with discounted fares across popular routes in Australia. Industry observers say this is not inconsistency but sophisticated revenue management at work.

“Airlines use dynamic pricing,” said aviation analyst Gerry Toft of the University of Sydney. “They charge premium prices on high-demand routes or peak times while offering discounts on off-peak or lower-demand flights to maximize load factors. Rising fuel costs don’t change the fundamental need to fill aircraft.”

Data from flight booking platforms shows international long-haul fares, particularly to Europe and parts of Asia affected by airspace restrictions, have climbed 12-18% year-over-year. Domestic leisure routes in Australia, however, have seen promotional pricing as carriers compete for discretionary travel spending amid economic caution from households.

The Middle East conflict has complicated global supply chains for jet fuel. Reduced shipments through key chokepoints have driven up refining and transportation costs. Airlines with poor fuel hedging positions are feeling the pain most acutely, forcing them to either absorb higher costs or pass them on through fare increases on less elastic routes.

At the same time, softer domestic demand in Australia — driven by high interest rates, cost-of-living pressures and increased competition from new entrants — has prompted carriers to stimulate travel with sales. Empty seats generate zero revenue, so even with higher fuel costs, it can be more profitable to sell a ticket at a discount than fly with it empty.

Qantas CEO Vanessa Hudson acknowledged the balancing act in recent comments. “We’re seeing strong demand on certain international corridors, but domestic leisure travel has been softer. Our job is to match capacity with demand while managing significant cost headwinds.”

Virgin Australia has taken a similar approach, cutting some international capacity while promoting domestic deals to boost load factors. The airline recently expanded its sales calendar with fares as low as $49 one-way on select routes, a move designed to stimulate travel during traditionally quieter periods.

Experts say this pricing strategy has become more sophisticated with the help of advanced revenue management systems. Airlines now use artificial intelligence to analyze booking patterns in real time, adjusting prices multiple times per day based on demand signals, competitor pricing and fuel cost fluctuations.

“Modern airline pricing is incredibly granular,” said Professor Rigas Doganis, a longtime aviation economist. “A single flight might have dozens of different fare buckets. Rising fuel costs might push up the price of flexible business class tickets while the airline still offers deep discounts in the lowest economy bucket to ensure the plane flies full.”

The strategy carries risks. If too many passengers book heavily discounted fares, it can erode overall yields. Carriers must carefully balance load factor gains against revenue per passenger. In the current environment, many airlines are accepting slightly lower yields on certain routes to protect cash flow and market share.

Fuel hedging also plays a crucial role. Airlines that locked in lower prices earlier are better positioned to run promotions. Those without effective hedges face more pressure to raise base fares. Qantas has historically been an active hedger, which has helped cushion some of the current volatility.

Broader industry trends show mixed signals. While international premium travel remains relatively strong, leisure domestic markets in several countries are showing price sensitivity. This has created opportunities for low-cost carriers and aggressive pricing from full-service airlines seeking to protect their market positions.

For consumers, the environment creates both challenges and opportunities. Strategic travelers can find genuine bargains on domestic routes by being flexible with dates and monitoring sales. However, those needing to book peak international travel or last-minute flights are facing noticeably higher prices.

The situation highlights the cyclical and unforgiving nature of the airline industry. Carriers must navigate volatile fuel prices, geopolitical risks, changing consumer behavior and intense competition while trying to deliver consistent returns to shareholders.

As the northern summer travel season approaches, analysts expect continued pricing volatility. Airlines will likely maintain a dual-track approach — protecting revenue on constrained or high-demand routes while using promotions to stimulate traffic elsewhere.

For now, travelers are advised to shop around, remain flexible and book early where possible. The current mix of rising costs and promotional pricing creates a complex but navigable market for those willing to put in the effort.

The paradox of higher fuel costs alongside fare sales ultimately comes down to one simple aviation truth: an empty seat is the most expensive seat of all.

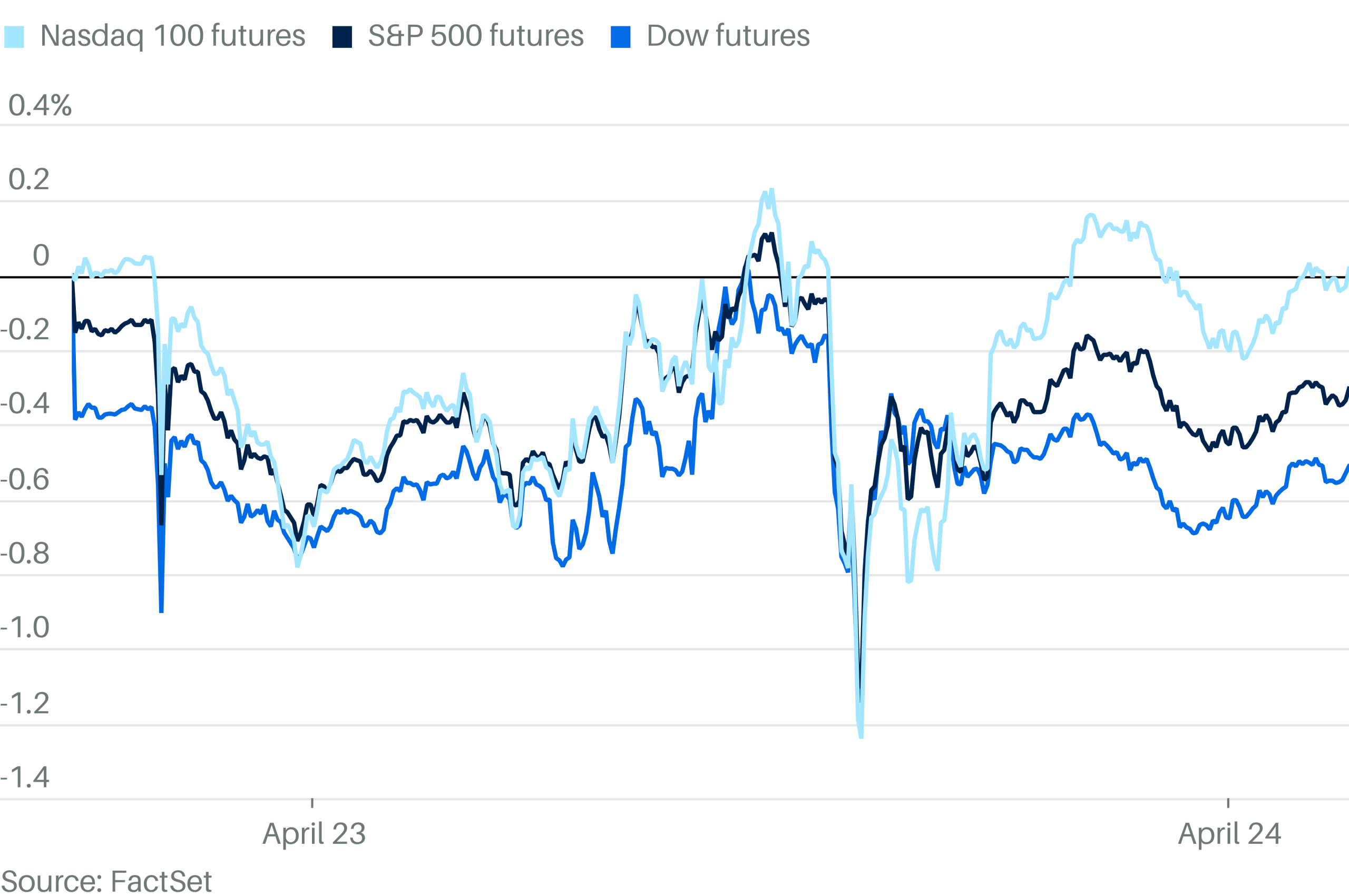

Stocks looked set to rise on Friday as solid tech earnings helped reassure investors who were questioning whether the market could keep its recent rally going.

Dow Jones Industrial Average futures slid 161 points, or 0.3%. But the blue-chip gauge looked likely to be an outlier: futures tracking the S&P 500 climbed 0.1% and contracts tied to the Nasdaq 100 jumped 0.6%.

Maheshwari’s overarching message was simple: caution over action. “The best thing is to avoid it for the time being. The runup has been pretty strong,” he said, adding that despite buying equities when the Nifty slipped below 23,000, he prefers to remain on the sidelines now. “It is too early to actually do anything… Just wait it out.”

On sectors he accumulated during the recent dip, Maheshwari highlighted a consistent leaning toward structural themes. “Power is a well-known theme across the market… power and solar has been two sectors which I have been positive about and have accumulated.” Alongside this, he continues to favour metals and banking, sectors he believes still enjoy strong fundamentals and macro visibility.

One space he isn’t touching is IT. Despite steep corrections, he sees no clarity on the earnings bottom. “I would tend to avoid it because even this quarter there has been no commentary which says that we are close to the bottom… it is best to avoid for the moment.” For existing IT investors, his advice is unequivocal: “I would tend to actually get out of this.”

Maheshwari is equally cautious on the auto sector, citing the potential ripple effects of weakness in technology-led employment. “I for the moment would avoid autos… the biggest fallout is going to come in autos.”

On Reliance Industries, he acknowledged its history of subdued stock performance while still flagging meaningful catalysts. “Reliance has been attractive for a long period of time. Unfortunately, it does not perform,” he noted. Yet, at current levels, he sees merit in accumulating. “I do agree at Rs 1300, 1325 Reliance is a buy.”

Consumption stocks, particularly FMCG names, may offer tactical opportunities, he added. “It could be a good trading bet… there has been a sector rotation… there is a good trading play available in the FMCG side.”(Disclaimer: The recommendations, suggestions, views, and opinions given by the experts are their own. These do not represent the views of The Economic Times.)

RIL on Friday reported a 12.6% year-on-year decline in consolidated net profit for the quarter ended March 31, 2026, as weakness in the oil-to-chemicals segment and higher costs weighed on the bottom line. The company’s consumer-facing businesses, however, continued to scale, with Jio Platforms posting strong earnings growth and Reliance Retail crossing 20,000 stores.

Consolidated net profit attributable to owners of the company came in at Rs 16,971 crore for Q4FY26, down from Rs 19,407 crore in the same quarter last year. Gross revenue rose 12.9% year-on-year to Rs 3,25,290 crore.

The company’s revenue also hit a record for the full year. Gross revenue for Q4FY26 rose 13% year-on-year to Rs 3,25,290 crore. For the full year, consolidated gross revenue rose 9.8% to a record Rs 11,75,919 crore. Full-year EBITDA also hit a record at Rs 2,07,911 crore, up 13.4% year-on-year.

Despite a 15% correction in 2026 so far, RIL shares are commanding a market capitalisation of over Rs 18 lakh crore.

While the earnings season is now at the end of its second week, its nearest rivals HDFC Bank and PSU lender State Bank of India (SBI) have significant ground to cover to reach that mark.

HDFC Bank, the next most valuable company by market capitalisation (Rs 12.08 lakh crore), reported a consolidated net profit of $8.07 (Rs 76,026 crore) billion in FY26 versus $7.51 billion (Rs 70,792 crore) in the previous FY, up 7.4% YoY.

While SBI is yet to announce its January-March quarter earnings, its 9MFY26 PAT stands at Rs 63,656 crore. Top brokerages like Nomura and Nuvama Institutional Equities have pegged the Q4 bottom line at Rs 18,700 crore to Rs 20,090 crore.

If the estimates hold true, the FY26 PAT for India’s largest lender could be Rs 83,746 crore, implying a net profit of $8.89 billion.

Domestic IT bellwether Tata Consultancy Services’ (TCS) FY26 PAT stood at Rs 49,454 crore ($5.25 billion).

(Disclaimer: The recommendations, suggestions, views, and opinions given by the experts are their own. These do not represent the views of The Economic Times.)

Some private-credit investors are shifting cash from one kind of debt fund to another, capitalizing on the differences in how they are valued. All of these funds hold private loans, but some are trading at a discount to others. Wall Street has a name for trades of this nature: arbitrage.

Pilgrim's Pride: Cheap On Multiples, But The Cycle Is Rolling Over

The bank, where Emirates NBD is set to acquire a majority stake up to 74% for approximately $3 billion, saw its annual net profit rise 18% year-on-year at Rs 822 crore.

RBL board proposed a dividend of Re 1 per share having Rs 10 face value, making it 10% dividend for FY26.

The bank’s net interest margin however fell to 4.41%, the lowest in the past five quarters. NIM was 4.63% in the preceding quarter while it was 4.89% in the year-ago period.

Net interest income grew 7% year-on-year at Rs 1671 crore while other income stood 7% higher at Rs 1069 crore. Its operating profit grew 11% year-on-year at Rs 955 crore.

“There has not been any material impact of the West Asia crisis on our business so far,” managing director R Subramaniakumar said.

“We delivered growth that meaningfully outpaced normalised industry trends, led by sharp momentum in granular retail advances and sustained strengthening of our granular deposit franchise,” he said.The bank’s net advances grew 23% year-on-year to Rs 1.14 lakh crore with retail segment contributing 59% of it while it saw contraction in credit card receivables and personal loan portfolio. Its total deposits grew 25% to Rs 1.39 lakh crore.

Its asset quality improved with gross non-performing assets ratio falling to 1.45% at the end of March from 1.88% three months prior, helped by Rs 911 crore of technically written-off loans during the quarter. Net NPA ratio was at 0.39% against 0.55% for the same period. The quarterly provisions were lower at Rs 678 crore as compared with Rs 785 crore in the year-ago period when the bank had made accelerated provisions to cover the credit risks arising from its microfinance portfolio.

The MD said that the share of the lender’s unsecured loans reduced to 24% from 285 a year back and the bank would like to maintain it between 20 and 25%.

During the quarter, It opened 23 branches, taking the total tally to 603.

“This expanded footprint strengthens our ability to deepen customer relationships, enhance sourcing capabilities, and support growth across our retail businesses as we enter the new financial year,” the MD said.

On the strategic investment by Emirates NBD which will transform RBL into a foreign bank subsidiary, approvals from the Reserve Bank of India and Competition Commission of India are already in place while RBL is awaiting the government’s approval, required for the foreign direct investment.

(Disclaimer: The recommendations, suggestions, views, and opinions given by the experts are their own. These do not represent the views of The Economic Times.)

In Supreme Court fight against deportation shield, Trump says judges have no role

– Building a consistent, low-risk passive income portfolio—no gambling, no hype, just fundamentals. I aim to generate ~12% average annual returns with minimal downside risk, prioritizing capital preservation and stable value compounding over short-term momentum. – With over a decade of professional experience in equity research, I specialize in analyzing cash-generative businesses, special situations, and corporate restructurings across developed markets. My investment strategy emphasizes risk assessment over speculative growth, aligning with contrarian and value-driven principles. – Influenced by legendary investors like Warren Buffett and Howard Marks, I rely on deep fundamental analysis, macroeconomic context, and rigorous valuation discipline. I hold a First-Class Honors degree in Economics from the University of London and am passionate about translating complex financial insights into actionable long-term investment ideas.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of BRK.B either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Business

WSFS Financial Corporation 2026 Q1 – Results – Earnings Call Presentation (NASDAQ:WSFS) 2026-04-25

Q1: 2026-04-23 Earnings Summary

EPS of $1.68 beats by $0.18

| Revenue of $275.30M (7.49% Y/Y) beats by $7.09M

Seeking Alpha’s transcripts team is responsible for the development of all of our transcript-related projects. We currently publish thousands of quarterly earnings calls per quarter on our site and are continuing to grow and expand our coverage. The purpose of this profile is to allow us to share with our readers new transcript-related developments. Thanks, SA Transcripts Team

LeBron James’ historic playoff performance lifts Lakers to 3-0 lead over Rockets

Rescuing The Data On A 1960s LGP-21 Computer’s Disk Memory

BITCOIN HISTORY IS REPEATING…

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business6 days ago

Business6 days agoPowerball Result April 18, 2026: No Jackpot Winner in Powerball Draw: $75 Million Rolls Over

-

Politics6 days ago

Politics6 days agoZack Polanski demands ‘council homes not luxury flats for foreign investors’

-

Fashion17 hours ago

Fashion17 hours agoWeekend Open Thread – Corporette.com

-

Entertainment6 days ago

NBA Analyst Charles Barkley Chimes in on Ice Spice McDonald’s Fiasco

-

Tech6 days ago

Tech6 days agoAuto Enthusiast Scores Running Tesla Model 3 for Two Grand and Turns It Into Bare-Bones Go-Kart

-

Politics5 days ago

Politics5 days agoGary Stevenson delivers timely reminder to register to vote as deadline TODAY

-

Politics3 days ago

Politics3 days agoMaking troops accountable for war crimes threatens US alliance, ex-SAS colonel warns

-

Business3 days ago

Business3 days agoRolls-Royce Voted UK’s Most Iconic Trade Mark as IPO Register Hits 150

-

Politics3 days ago

Politics3 days agoDisabled people challenge government SEND proposals over segregation concerns

-

Crypto World5 days ago

Crypto World5 days agoBank of Hawai’i (BOH) Q1 2026: Net Income Drops to $57.4M as Net Interest Margin Expands

-

Politics3 days ago

Politics3 days agoZack Polanski responds to home secretary’s taser threat

-

Politics3 days ago

Wings Over Scotland | How To Get Away With Crimes

-

Politics3 days ago

Politics3 days agoStarmer handler McSweeney to be dragged from shadows by Foreign Affairs Committee

-

Crypto World6 days ago

Kelp DAO rsETH Bridge Hack Drains $292M as DeFi Losses Top $600M in Two Weeks

-

Politics3 days ago

Politics3 days ago‘Iran is still a nuclear threat’

-

Crypto World4 days ago

Crypto World4 days agoFive Value Stocks with Recovery Potential in 2026: PayPal (PYPL), Nike (NKE), and More

-

Crypto World4 days ago

Crypto World4 days agoNew York sues Coinbase, Gemini over prediction market offerings

-

Business3 days ago

Business3 days agoThe Job Benefits Most Men Don’t Know to Negotiate

-

Crypto World1 day ago

Crypto World1 day agoMichael Saylor says BTC winter is over. Market analyst disagrees, says bitcoin was in a pullback

-

Politics6 days ago

Politics6 days agoReform investigating candidate who ‘hates’ the NHS

You must be logged in to post a comment Login