Greenville’s workforce keeps the city moving, from busy warehouses and construction sites to offices and healthcare settings where daily tasks rely on steady physical effort.

When an injury interrupts that rhythm, returning to work, even in a limited capacity, can feel like progress, but it also raises important questions about recovery and financial stability. Light-duty job offers often arrive during this uncertain phase, presenting a mix of opportunity and risk for injured workers trying to balance healing with income needs.

Understanding how these offers affect a worker’s compensation claim is essential, especially when the duties may not fully align with medical restrictions or long-term recovery goals. The details behind these arrangements can shape both treatment outcomes and benefit eligibility. A Greenville workplace injury lawyer can help review those offers carefully, ensuring that any return-to-work plan supports recovery while protecting the full value of the claim.

Why Employers Make These Offers

Employers often offer modified jobs to reduce time away from the workplace. Lower wage exposure can benefit the company, while an early return may appear cooperative to the insurer. For many injured workers, speaking with a workplace injury lawyer becomes important when a temporary assignment appears acceptable in writing but conflicts with lifting limits, pain levels, or reduced earnings. Small details in that offer can shape the claim for months.

What Light-Duty Work Usually Means

Light-duty work usually involves fewer physical demands than the pre-injury role. Common changes include less lifting, shorter standing periods, limited reaching, or reduced repetitive motion. Some employers shift a person into desk work, phone coverage, or training support. Others create temporary clerical tasks. The title matters less than the actual movements required during each hour of the day.

Advertisement

Doctor Restrictions Control the Analysis

Medical restrictions should direct every return-to-work decision. If the treating physician limits bending, pushing, twisting, or shift length, the offered position should closely match those terms. A poor fit can aggravate inflammation, increase pain, and delay tissue repair. Written restrictions carry more weight than hallway conversations, informal assurances, or verbal statements from a supervisor who does not control medical care.

Wages Can Change the Claim

Pay changes often affect the value of an injury claim. If a temporary position provides fewer hours or lower wages, partial disability benefits may still be owed. That issue warrants a close review of pay records, shift schedules, and overtime history. Lost premium pay can matter, too. A worker may return physically, yet still face measurable income loss after the accident.

Refusing an Offer Can Create Risk

Refusing a suitable light-duty job can create legal problems. An insurer may argue that wage loss ended once work became available within the stated restrictions. Still, every offer should be checked carefully before acceptance. If the tasks exceed medical limits, increase symptoms, or exist only on paper, a refusal may be justified with strong documentation and physician support.

Documentation Often Decides Disputes

Good records often influence better outcomes in disputed cases. The worker should keep the written offer, physician notes, pay stubs, and messages describing daily tasks. A short symptom log can also help, especially if swelling, numbness, or fatigue worsen after certain duties. Memory fades quickly. Therefore, consistent written proof usually carries greater weight than later recollection during a dispute.

Advertisement

Hidden Problems With Temporary Positions

Some modified assignments are legitimate and medically appropriate. Others change once the first shift begins. A position may start with seated tasks, then drift into lifting, prolonged standing, or faster production demands. That kind of shift can strain healing tissue and trigger fresh conflict in the claim. Early attention to actual duties helps reveal whether the placement is truly safe.

Medical Treatment Should Continue

A return to light-duty work does not mean the injury has healed. Follow-up visits, physical therapy, imaging, medication review, or specialist care may still be necessary. Skipping treatment can weaken the medical record and invite arguments that recovery is complete. Any symptom increase after a modified shift should be reported promptly, especially if pain, weakness, or restricted motion worsens.

A Short Review Before Saying Yes

Before accepting a position, the worker should compare the offer with the latest medical note. Important points to review include exact duties, expected pace, sitting time, standing demands, travel, and hourly pay. Clear answers reduce confusion for everyone involved. Vague terms deserve caution. Unclear expectations can hide physical demands that do not appear in the written description.

Conclusion

Light-duty work can support recovery when the assignment respects medical restrictions and preserves fair earnings. Trouble begins when the job exceeds physical limits, reduces pay, or creates a false picture of improvement. Each offer should be measured against written physician guidance, actual daily duties, and the full effect on benefits. A careful response helps protect healing, income, and the long-term strength of the claim.

Raleigh runs on a steady kind of forward motion. Between the daily flow along the I-440 Beltline, the constant rush of state employees moving through downtown near the Capitol, the growing commuter traffic feeding into North Hills and Brier Creek, and the busy stretches of Capital Boulevard pulling visitors toward RDU, the City of Oaks rarely leaves much breathing room when something goes wrong.

A sudden injury here can feel especially disorienting, whether it stems from a wreck near the Beltline, a fall inside a busy retail corridor off Six Forks Road, or a job-site incident in one of the city’s many active construction zones. What often catches people off guard is how quickly the first settlement check shows up afterward, sometimes before the doctor has even mapped out the full treatment plan. That timing alone deserves a closer look. Speaking early with a Raleigh personal injury lawyer at CR Legal helps families weigh that offer against the recovery still ahead.

The First Number Rarely Fits

A first offer often appears before swelling settles, pain patterns stabilize, or work restrictions are clear. During that uncertain period, many families review treatment notes, missed earnings, and insurance limits, then speak with a lawyer about whether the proposed sum reflects future therapy, household strain, medication costs, and the chance that recovery will take months, not weeks.

The Full Picture Takes Time

Strains, disc injuries, and concussive symptoms do not always show their full effect right away. Some patients improve within days, while others develop headaches, nerve pain, sleep disruption, or reduced mobility later. Until physicians can estimate follow-up care, any payment figure rests on an incomplete record. Money accepted too soon may fall far short if treatment expands after new findings appear.

Early Records Shape Value

Claims are priced from documents, not from visible distress. Urgent care notes, imaging results, prescriptions, therapy orders, and work limits create the medical timeline. Missing appointments can weaken that timeline, even where cost or transportation caused the gap. More complete records usually give a clearer basis for valuing pain, physical loss, and the practical burden carried at home.

Advertisement

Statements Can Narrow a Claim

Recorded statements are often requested when a patient is exhausted, medicated, or still in shock. Under those conditions, a person may guess about speed, symptoms, or earlier health issues. Later chart entries can then be measured against those guesses. Even small differences may be framed as inconsistency, which can reduce bargaining strength before the injury pattern is fully understood.

North Carolina Fault Rules Matter

North Carolina uses a strict contributory negligence rule. Under that rule, even a small share of blame can block financial recovery. Casual comments made at a scene, or during a claim call, may later be treated as admissions. Photographs, witness statements, vehicle damage, and property conditions deserve close review before anyone accepts an insurer’s account of what happened.

Deadlines Should Still Be Tracked

More information is helpful, but time limits still matter. Many North Carolina injury claims must be filed within three years of the event date, although some matters follow different rules. Early legal review can preserve camera footage, identify additional defendants, and secure witness details. That preparation helps prevent a rushed settlement from becoming the only remaining option later.

Hidden Deductions Change the Result

The amount offered is rarely the amount kept. Hospital liens, health insurance reimbursement claims, unpaid balances, and case expenses can cut deeply into the final payment. An amount that sounds reasonable during a phone call may look much smaller after those deductions are listed. Net recovery, rather than the headline number, gives a truer measure of whether settlement makes sense.

Advertisement

Daily Losses Also Count

Financial harm reaches beyond emergency treatment and repair invoices. Missed overtime, canceled shifts, child care, travel for appointments, and help with lifting or cleaning can all affect a household budget. Pain also carries value, despite lacking a receipt. A careful review counts both visible expenses and the quieter losses that change daily function after physical trauma.

Releases Usually End the Matter

Settlement papers usually include a release that closes the claim permanently. Once signed, that document often bars future payment, even if new symptoms appear or treatment becomes more invasive. Few patients would knowingly exchange a lasting waiver for short-term relief. Reading each term closely, and asking direct questions, can prevent expensive regret after funds have already been issued.

Compare Gross and Net Numbers

A careful review starts with two direct questions. How was the figure calculated, and what amount remains after every deduction is paid? That comparison can expose weak assumptions about future care, wage loss, or shared fault. It also turns an emotional decision into a practical one, which is often safer while healing is still incomplete and expenses continue to rise.

Conclusion

Fast payment may ease a short-term crisis while creating a larger financial problem later. Once a claim is closed, added therapy, delayed symptoms, or extended wage loss may stay uncompensated. A careful decision rests on medical records, realistic recovery estimates, and a clear look at what money would remain after deductions. That slower review helps protect legal options and reduces the risk that one rushed signature will shape years of physical and financial strain.

Ministers have set the high street banks on notice. The Treasury has commissioned an independent review into the impact of more than 6,700 bank branch closures across the UK, and has signalled it is prepared to compel lenders to provide face-to-face services where the evidence shows communities and small businesses are being left adrift.

The Access to Banking Review, announced on Thursday by Lucy Rigby, the economic secretary to the Treasury, will be led by Richard Lloyd OBE, the former executive director of consumer group Which? and a one-time interim chair of the Financial Conduct Authority. Lloyd has been asked to report back by October, gathering evidence on where branch withdrawals have bitten hardest, who has suffered most and where new intervention is needed.

The review lands alongside the government’s Enhancing Financial Services Bill, trailed in the King’s Speech, which the Treasury said would arm ministers with powers to “act swiftly if the evidence supports intervention on access to banking services”. In Whitehall parlance, that is unusually direct language — and a clear shot across the bows of an industry that has spent a decade thinning out its physical estate.

A decade of decline

The scale of the retreat is striking. According to consumer champion Which?, 6,719 branches have shuttered since 2015 — an average of roughly two a day. Lloyds Banking Group, NatWest, Barclays, HSBC and Santander have all taken the axe to their networks, with a fresh tranche of more than 130 closures pencilled in for May and June alone.

The economics from the banks’ perspective are not in dispute. Customers have migrated en masse to mobile apps, footfall has collapsed and the cost of running a Victorian-era branch estate has become harder to justify to shareholders. But the human and commercial fallout has been uneven, with rural towns, older customers and cash-reliant small traders disproportionately affected — a pattern Business Matters has tracked over several years and documented in its reporting on more than 6,000 UK branch closures.

Advertisement

Hubs: helpful, but not enough

The industry’s answer has been the shared banking hub: a Post Office counter for everyday cash and cheque needs, with the big lenders taking it in turns to send their own staff into a private room for more complex queries, typically one bank per weekday. Some 234 hubs have opened since April 2021, and Labour pledged in its manifesto to push the total to 350 by 2029.

Yet hubs come with a structural weakness. While the Financial Conduct Authority polices access to cash, there are no statutory rules governing what banking services must actually be provided inside a hub, those decisions remain at the banks’ discretion. The Post Office’s role as the de facto banking partner has been a lifeline for many high streets, but small business owners say the model still falls short on lending conversations, complex account servicing and the kind of relationship banking that used to be taken for granted.

That gap matters. For owner-managers running a café, a building firm or a one-van logistics operation, the disappearance of a local branch is not an inconvenience, it is a productivity tax. Cash takings have to be banked further afield. Loan applications increasingly run through opaque, centralised credit-scoring systems. And the local manager who once knew the business, and could vouch for it, has all but disappeared.

A turning tide?

There are tentative signs the industry is reading the room. Barclays last year began reopening high street branches and reinstating the role of the bank manager, an explicit bet that physical presence, and human judgement, is once again a competitive advantage. Whether that becomes a trend or remains a marketing flourish will depend in no small part on what Lloyd’s review concludes.

Advertisement

Rigby was careful to frame the exercise as evidence-led rather than punitive. “We are supporting industry’s rollout of banking hubs, but we also need a clear picture of where communities are still losing out,” she said. “This independent review will show us where the problems are and what further action may be required, and we will move quickly to legislate where the evidence shows it is needed.”

Lloyd, for his part, signalled an open-door approach. “It’s important to take stock of the impact that the big shift to digital services has already had, and to understand the need for access to in-person banking in the future,” he said. “I hope to hear from as wide a range of views as possible.”

What it means for SMEs

For Britain’s 5.5 million small businesses, the review is more than a consumer issue dressed up in policy language. Access to a banker who understands the trading rhythms of a local economy has historically been a quiet but consequential ingredient in SME growth. Should Lloyd’s report conclude — as campaigners expect — that hubs alone cannot plug the gap, the Enhancing Financial Services Bill gives ministers the statutory teeth to mandate minimum service levels.

That would represent a significant philosophical shift: from leaving branch strategy to commercial discretion, to treating face-to-face banking as something closer to a regulated utility. The banks will lobby hard against any such reframing. But after a decade in which the lights have gone out above 6,700 high street branches, the political mood in Westminster, and the patience of small business owners, is wearing visibly thin.

Advertisement

Amy Ingham

Amy is a newly qualified journalist specialising in business journalism at Business Matters with responsibility for news content for what is now the UK’s largest print and online source of current business news.

The annual survey charts the finances of the 350 wealthiest people in the UK

07:52, 15 May 2026Updated 08:00, 15 May 2026

Sir James Dyson

Tech tycoon Sir James Dyson and family are the wealthiest people in the West of England, the latest Sunday Times Rich List has revealed.

The British inventor retains the top spot for the South West region, despite a 13.5 per cent decline in revenues at Dyson’s consumer electricals group over the past two years, partly due to President Donald Trump’s tariffs.

Advertisement

Sir James, who acquired a 50 per cent stake in Bath Rugby Group earlier this year, is one of the country’s best-known inventors, coming up with the first idea for a new model vacuum cleaner in 1979 and growing his business into one of the world’s biggest household goods firms.

However, over the last 12 months he has seen his wealth drop by £8.8bn – from £20.8bn in 2025 to £12bn. The company employs thousands of people at its base near Malmesbury, in Wiltshire, although it is now headquartered in Singapore.

Elsewhere, Plymouth retail mogul Chris Dawson and his wife Sarah were ranked the second-richest people in the region. The couple who own The Range saw their wealth grow by £50m to £2.65bn, while Peter Hargreaves, co-founder of Bristol-based investment firm Hargreaves Lansdown, saw his wealth jump to £2.325bn.

Chris Dawson, founder of The Range

This year’s list of 350 individuals and families together holds combined wealth of £783.5bn – a sum larger than the annual GDP of Belgium ($776bn), Sweden ($760bn) and Israel ($719bn), according to the Sunday Times. It represents about a quarter of the United Kingdom’s total annual GDP.

Advertisement

Sir Elton John, Lord Lloyd-Webber, Sir Mick Jagger, Keith Richards, JK Rowling, Charlotte Tilbury and Sir Lewis Hamilton all appear in the annual survey.

The rankings are topped by investors Sanjay and Dheeraj Hinduja and family (£38bn) with Newcastle United minority owners David and Simon Reuben second (£28bn), and DAZN majority owner Sir Leonard Blavatnik in third (£26.8bn).

The minimum entry level dips to £340m — another indicator of a subdued year.

Robert Watts, compiler of the Sunday Times Rich List, said: “This year’s Rich List is a tale of two exoduses. One in six of the individuals and families who appeared on the list two years ago don’t feature this time.

Advertisement

“Many foreign billionaires who have been living in the UK have also dropped out because they have moved away. We have also seen a sharp rise in the number of British nationals now resident in Dubai, Switzerland and Monaco. As UK nationals these people remain on our Rich List — wherever they now live.

“These two exoduses pose challenges for the UK economy and its public finances. Will more of the wealthy now set up or grow their ventures overseas and in doing so create fewer jobs here? How much tax – if any – will Rachel Reeves’s Treasury be able to extract from those affluent Brits who have now left the country?”

He added: “This year’s edition shines a light on fortunes made from artificial intelligence, driverless cars and crypto-currencies as well as baby milk, make-up, hoodies and other everyday items.”

The 10 wealthiest in the South West according to Sunday Times Rich List 2026

WASHINGTON — The FBI announced a $200,000 reward Thursday for information leading to the arrest of Monica Elfriede Witt, a former U.S. Air Force counterintelligence specialist accused of defecting to Iran more than a decade ago and sharing highly classified national defense information with the Islamic Republic.

The high-profile reward, issued by the FBI’s Washington Field Office, underscores ongoing U.S. concerns over one of the most damaging espionage cases involving an American intelligence insider in recent memory. Witt, 47, remains a fugitive believed to be living in Iran, where she allegedly continues to support Tehran’s intelligence efforts against her former colleagues and country.

“Monica Witt allegedly betrayed her oath to the Constitution more than a decade ago by defecting to Iran and providing the Iranian regime national defense information and likely continues to support their nefarious activities,” said Daniel Wierzbicki, special agent in charge of the FBI Washington Field Office’s Counterintelligence and Cyber Division.

A Career Built on Secrets, Then Betrayal

Witt joined the Air Force in 1997 and served until 2008 as a technical sergeant and special agent with the Air Force Office of Special Investigations. She held top-secret clearance and specialized in counterintelligence, gaining deep knowledge of U.S. intelligence operations, undercover personnel identities and sensitive collection programs.

Advertisement

After leaving active duty, she worked as a Defense Department contractor until 2010, maintaining access to classified materials. Prosecutors allege that Iranian intelligence began targeting her as early as 2012. FBI agents warned Witt she was a potential recruitment target, but she assured authorities she would not cooperate with Tehran.

In May 2012, Witt traveled to Iran to attend a conference sharply critical of U.S. policies. She returned the following year and, by August 2013, had fully defected, boarding a flight from Dubai to Tehran. Iranian state media broadcast her conversion to Islam and anti-American statements.

According to a 2019 federal indictment unsealed in Washington, D.C., Witt provided Iran with details on a highly classified U.S. intelligence collection program and helped identify former U.S. colleagues for targeting. She allegedly assisted Iranian hackers in cyberattacks against American intelligence personnel.

Four Iranian nationals were also charged in the same case for their roles in the cyber campaign. Witt faces charges including conspiracy to deliver national defense information to a foreign government and delivering such information, carrying potential life imprisonment if convicted.

Advertisement

Why the Reward Now?

The FBI’s decision to publicize the $200,000 bounty comes more than seven years after the indictment and 13 years after her defection. Officials say Witt may still be actively supporting Iranian operations, making her ongoing threat a priority even amid shifting Middle East dynamics.

She is fluent in Farsi and has used aliases while in Iran. The FBI’s wanted poster describes her as 5 feet 8 inches tall, weighing about 145 pounds, with brown hair and hazel eyes. She has tattoos, including one on her left wrist.

Security experts view Witt’s case as a stark example of insider threats. Her knowledge of U.S. counterintelligence tradecraft reportedly helped Iran identify and harass former American operatives. Some analysts have described her as one of Tehran’s most valuable assets in its shadow war with Washington.

Broader Implications for U.S. National Security

The case highlights vulnerabilities in retaining and monitoring cleared personnel after they leave government service. Witt’s defection occurred during a period of heightened tensions with Iran, including disputes over its nuclear program and regional proxy activities.

Advertisement

U.S. officials have long warned that Iran aggressively targets current and former American intelligence officers through recruitment, coercion and cyber means. Witt’s actions allegedly endangered lives and compromised programs designed to protect U.S. interests in the Middle East.

The reward announcement arrives as U.S.-Iran relations remain strained. Recent regional conflicts, including tensions involving Israel and Iranian-backed groups, add urgency to countering Tehran’s intelligence capabilities.

Public Tips Sought

The FBI urges anyone with information on Witt’s whereabouts or activities to contact the bureau immediately. Tips can be submitted anonymously via tips.fbi.gov or by calling 1-800-CALL-FBI. The reward applies to information leading to her arrest and conviction.

Witt remains on the FBI’s Most Wanted list in the counterintelligence category. Previous lower-profile efforts to locate her yielded no public breakthroughs, prompting the escalated financial incentive.

Advertisement

Personal Background and Radicalization Path

Born in 1979, Witt had a distinguished early career, earning an Air Medal for her service during the 2003 invasion of Iraq as a crypto-linguist aboard RC-135 Rivet Joint surveillance aircraft. She later transitioned to counterintelligence roles.

Reports suggest personal factors, including feelings of disillusionment, may have contributed to her radicalization. Iranian operatives reportedly exploited these vulnerabilities, offering ideological alignment and a new life in Tehran.

Her public appearances on Iranian television denouncing the U.S. shocked former colleagues who remembered her as a dedicated service member.

Lingering Questions and Ongoing Threat

More than a decade later, fundamental questions persist: How much damage did Witt’s betrayal cause? What specific programs or individuals were compromised? And does she continue providing actionable intelligence to Iran today?

Advertisement

U.S. intelligence officials believe the answer to the last question is yes, which explains the timing and size of the reward. In an era of great-power competition and persistent Iranian hybrid threats, even historical defectors can pose current dangers.

The case also serves as a cautionary tale for the intelligence community about insider threats, mental health support for veterans and the long tail of recruitment operations by adversarial nations.

As the FBI ramps up its public appeal, the hunt for Monica Witt enters a new, more visible phase. For now, she remains beyond American reach in Iran, a living symbol of one of the most audacious defections in modern U.S. history — and a reminder that some secrets, once given away, can never be fully recovered.

Anyone with relevant information is encouraged to come forward. The $200,000 reward could provide the breakthrough needed to bring a long-sought fugitive to justice and close a painful chapter in American counterintelligence.

When we look back. . . the nature of the forces currently in train will have presumably become clearer. We may conceivably conclude from that vantage point that. . . the American economy was experiencing a once-in-a-century acceleration of innovation, which propelled forward productivity, output, corporate profits, and stock prices at a pace not seen in generations, if ever. ¹

The Broyhill Equity Composite declined 6.0% in the first quarter, net of all fees and expenses, lagging global equity markets as the MSCI All Country World Index declined 3.1%. ² Individual performance may vary depending on individual account allocations, legacy positions, and capital flows. Detailed quarterly reports, including account and benchmark performance, portfolio holdings, and transaction history, have been posted to our investor portal.

After a strong start to the year for the portfolio, global stocks fell sharply following the strikes on Iran. Despite our defensive positioning, with nearly half the portfolio invested in noncyclical sectors, our stocks did not provide the protection we expected or that we’ve historically provided. While we don’t invest on a one-month horizon, nor do we place undue emphasis on short-term results, we do remain relentless in our work to protect your capital from significant market losses. So, I want to explain what drove the gap versus our expectations, because the context matters – and because we believe the setup from here is unusually compelling.

Three structural portfolio tilts moved against us simultaneously.

Advertisement

• We own no energy – the only sector with positive returns in March.

• Nearly half the portfolio is invested in businesses outside the U. S. , and European markets declined sharply given their higher sensitivity to energy prices (while this is broadly true of continental Europe, our companies have minimal exposure to the Middle East or the rising price of oil).

• Our large non-cyclical exposure – consumer staples and healthcare – underperformed in a down market, which is not supposed to happen and historically has not lasted.

What didn’t happen is as important as what did. Across the portfolio, businesses are performing well and meeting or exceeding our expectations. Consensus estimates continued rising even as our stock prices declined in March. That disconnect – improving fundamentals and falling prices – suggests this move was a positioning-driven sell-off, not a fundamental one. It’s also why we believe our stocks are poised to catch back up to fundamentals.

Advertisement

Performance Review

It’s hard not to be uber bullish when stocks are enjoying a once-in-a-century acceleration in innovation, resulting in a surge in productivity and corporate profits. But as it turns out, we are actually witnessing a twice-in-a-century acceleration in innovation, as the opening quote of this letter was first delivered by Former Fed Chairman Alan Greenspan in January 2000. As they say, history doesn’t repeat, but. . .

Top Contributors

Valvoline (VVV) was our largest contributor in the quarter. While the market spent its days hallucinating about the terminal value of artificial intelligence, Valvoline went on quietly changing oil, opening new stores, while moving more cars through its bays than any other competitor in the industry. Since we’ve owned it, shares have exhibited significantly more volatility than the business itself, but what matters is that the underlying unit economics are intact, while unit growth, service mix, and price continue moving in the same direction.

Honeywell (HON) was our second-largest contributor in the quarter. Management accelerated the aerospace spin-off, moving the separation up to the end of June and leaving behind a pure-play automation business. We continue to believe the pieces, including the recently announced Quantinum IPO, are worth meaningfully more than the whole. Upcoming Investor Days are the next chance for the market to do the math.

Ball Corporation (BALL) rounded out our top three contributors during the quarter. When we initially acquired the position, our thesis centered around the company’s post-aerospace-divestiture status, which left it a pure-play packaging company well positioned to return significant capital to investors. As the thesis played out, we sold into the re-rating and redeployed proceeds into more attractive opportunities.

Advertisement

Top Detractors

IQVIA (IQV) was our largest detractor despite fundamentals being far better than price action suggested. The stock has sold off because investors have convinced themselves that AI will compress economics faster than it drives demand. At the current price, we are more than willing to take the other side of that trade. Large pharma is structurally reliant on IQVIA’s clinical trial architecture and proprietary data assets, and we think it is highly unlikely that Claude can automate away the FDA approval process. While the burden of proof remains on the company, we believe we are being paid well to wait at the stock’s current valuation.

Louis Vuitton (LVMUY) was our second-largest detractor, posting its worst quarterly performance on record, driven by the Middle East conflict and fears of a broader slowdown in luxury demand. Beneath the headlines, Wines & Spirits delivered its biggest beat in years as the Hennessy destocking cycle ends, Watches & Jewelry beat as Tiffany continues to gain share, and Fashion & Leather continues its slow sequential improvement. The stock now trades at the bottom of its valuation range, which we find compelling for a business of this quality.

Avantor (AVTR) made our list of detractors for the last time in the first quarter. The destocking cycle has run far longer than we initially modeled, but the bigger issue was self-inflicted. Successive management teams failed to defend the share against Thermo Fisher (TMO). After swapping half of our position for Thermo last year, we took our

remaining lumps and redeployed the capital into Sotera Health (SHC), where litigation fears have created an opportunity to own a mission-critical sterilization duopoly at a meaningful discount to intrinsic value.

Advertisement

Key Transactions

We run a concentrated portfolio and aim to invest over a three- to five-year horizon. With roughly 20 positions, that translates into a handful of new ideas in a normal year. But like our returns, our ideas come in lumps, as volatility creates opportunity.

The extreme dispersion we saw in the first quarter handed us an opportunity to populate the book with at least a year’s worth of new ideas. Running towards controversy after big dislocations is our bread and butter. I suspect that’s a gene inherited from my father, who still fills his car to the ceiling with random items he doesn’t need from close-outs (most recently, Livingston Mall in NJ) or even relics of the past left on the roadside. In markets, such a strategy rarely guarantees short-term success, but over the long term, it has consistently been our most reliable generator of alpha.

During the quarter, we booked a portion of our gains on Phillip Morris (PM) and fully liquidated several positions. In addition to Ball, noted previously, we liquidated profitable investments in Kenedy Wilson (KW) and Fresenius Medical Care (FMS), as the former agreed to a higher bid from CEO Bill McMorrow and Fairfax Financial (FRFHF), and proceeds from the latter were redeployed into more attractive opportunities. We also fully liquidated two positions – Evolution (EVVTY) and Avantor – after reducing exposure to each, to reinvest in higher conviction ideas.

We initiated several new positions during the quarter. We bought Microsoft (MSFT) as the stock’s valuation declined to levels in line with the broader market. We initiated a new position in Smurfit WestRock (SW) with proceeds from Ball, as we suspect continued capacity tightening and additional pricing will drive mid-term results well above guidance and current consensus. We bought Sotera Health, a sterilization-franchise medical device business whose customers cannot easily replace it, where an ongoing tort overhang has created a price we believe materially underestimates the underlying business. And we established two new positions in the depressed housing industry – Masco (MAS) and Floor and Décor (FND), as we believe the normalized earnings power of both companies has increased significantly through market share gains and expense efficiencies captured during this extended downturn. We also began accumulating shares of Leggett & Platt (LEG), anticipating a higher bid from Somnigroup International (SGI), and fully exited when that bid emerged.

Advertisement

A Few Words on Healthcare

While investors have focused on the trillions of dollars in market capitalization that have evaporated from the software sector in recent months, the Medical Device and Life Sciences & Tools industries have not been far behind in terms of creative destruction. In the wake of this latest leg down, we significantly increased our investments in the sectors, bringing both IQVIA and Sotera Health into our top holdings.

Clinical research is one of the most regulated industries on the planet – and for good reasons. It’s literally a matter of life and death. And while Claude has dramatically increased our own productivity, we surmise that government agencies, including the FDA, will be somewhat slower to embrace these magical tools. When you consider that

AI adoption within at least one large, highly regulated US bank consists of mandates from management that employees use Copilot at least x times each week, the thought of the FDA entertaining a material shift in trial paradigms over the next several years seems exceedingly unlikely. To put the agency’s pace of change in perspective, regulators began accepting digital data submissions in PDF format less than a decade ago.

CROs, or Clinical Research Organizations like IQVIA, sit squarely in the crosshairs of investors’ concerns, given AI’s potential to completely reimagine how research is conducted. In fact, we’d even suggest that drug discovery may represent the single most significant benefit of AI as the quantity of new molecules tested and drugs coming to market accelerates at a pace beyond even the wildest imaginations of Watson and Crick. But despite our impressive leaps in understanding the human genome since its initial discovery, our understanding of human biology remains incomplete at best. And where we lack a deep understanding, we will still need experiments to test hypotheses and to observe how these drugs actually work amid the mystery of human biology, regardless of what AI models might promise.

Advertisement

While it may take time for the market to separate the wheat from the chaff, we expect that the Life Sciences Tools and broader research ecosystem will ultimately benefit from accelerating AI-driven demand for the data that fuels these models. And as AI compresses drug pipelines and increases the likelihood of clinical success, the growing number of drugs reaching the market will require more research, development, and tools. A recent analysis found that AI-designed molecules clear Phase I at 80-90%, compared with a historical average of 40-50% for conventional discoveries. ³ None of these candidates have been commercialized yet, but dozens have entered human trials, and several are now in Phase II. As Big Pharma’s return on investment improves, the rational response is to spend more on R&D, not less. Some functions will inevitably move back in-house, but we do not see the longer-term outsourcing trend reversing, as pharma simply doesn’t have the infrastructure or the data outside its own narrow indications. Bottom line: we think the data and scaled infrastructure that IQVIA provides will become meaningfully more effective, and a great deal safer, than a workflow vibe-coded by a pharmacist. We also think this makes the company more valuable, not less.

Recent channel checks support this view, framing AI more often as an opportunity than a threat. RFP flow and awards are improving as funding loosens and risk appetite returns; decision-making timelines are shortening, and pricing is firming. The bear case is that the majority of AI efficiencies gained by CROs will be captured by sponsors. But this ignores the fact that CROs have always been under pressure from Big Pharma to pass along savings. AI-generated efficiencies will certainly create additional opportunities to do so. This isn’t new. These companies have thrived for decades by finding ways to execute trials more efficiently, leveraging cost reductions into operating leverage to offset pricing pressures. That playbook hasn’t changed. But the price has shifted materially, with shares of IQVIA, for example, trading at half the broader market’s multiple, down from the 40% premium reached before COVID.

Bottom Line

We are keenly aware that our current positioning has weighed heavily on our relative performance of late. And we recognize that this has likely tested the patience of even our longest-duration investors. Simply owning a collection of good businesses does little to change that when their shares fail to deliver meaningful gains, while broader indices march steadily higher, and everyone around you is boasting about their biggest winners. While others are doing better at the moment, we think many are taking risks far greater than they appreciate. That is why we have stayed in our lane, rather than underwriting risks we don’t believe are properly priced.

Our job is to protect your capital while taking calculated risks to grow it over time. Periods like this test conviction. They also plant the seeds of future outperformance. This view may continue to cost us in the near term if momentum remains dominant over fundamentals. But with oil sitting in triple digits, geopolitics still in flux, and recorded crowding in US benchmarks trading at record valuations, we are willing to accept the risk of short-term underperformance because the reward for being correctly positioned when the market does turn has rarely looked more asymmetric than it does today.

Advertisement

While we cannot predict when that will arrive, what it will look like, or how quickly it will unfold, what we can tell you is that the portfolio is meaningfully cheaper today than it was at the start of the year. Importantly, our view of the underlying businesses we own has not changed: we believe they are worth considerably more than the market is giving them credit for. Rising tensions in the Middle East, regardless of how they unfold, would not change that assessment.

We have been here before. Our relative results have always been cyclical. But a decade of data tells a consistent story. We have seen the pattern clearly: periods where relative performance compresses (as we saw during the speculative rally immediately following COVID) have consistently been followed by sharp recoveries (many of which included short-term drawdowns as we experienced in March). The current dip looks a lot like previous ones, which have historically been followed by our best relative performance.

One More Thing

There is nothing to writing. All you do is sit down at a typewriter and bleed. – Ernest Hemingway

A few years after joining Broyhill in 2005, a friend suggested that I start a blog to share our insights, which had, until then, been distributed only internally. That site, The View from the Blue Ridge, was eventually folded into the firm’s website. Writing has always been a valuable tool for me, both personally and professionally. It has never been a particularly easy or enjoyable process, but the result usually justifies the effort. Through writing, I am able to flesh out my thinking, find holes in my logic, and distinguish highly confident ideas from those held more loosely. But as the business has grown, I’ve had less time to share our work publicly beyond these letters. Coming into this year, I decided it was time to change that.

Advertisement

We are excited to announce the launch of Vitruvian Value, where I will share our thinking, our ideas, our frameworks, and the lessons from running a concentrated portfolio through decades of market cycles, along with the occasional commentary on markets and human behavior.

We are grateful for your continued trust and partnership. We come into the office each day striving to earn it, and we realize just how fortunate we are to have such a wonderful group of like-minded, long-term investors who place their confidence in us. You enrich our network, strengthen our competitive advantage, and just make our work all the more enjoyable. As always, please feel free to reach out anytime with questions. We enjoy hearing from you.

Sincerely,

Christopher R. Pavese, CFA

Advertisement

References

Remarks by Chairman Alan Greenspan Before the Economic Club of New York, January 2000

For standardized performance data, including 1-year, 3-year, and since-inception net returns with benchmark comparisons, please refer to the Broyhill Equity Fact Sheet. Past performance is not indicative of future results.

How Successful Are AI-Discovered Drugs in Clinical Trials, Drug Discovery Today (2024).

About Broyhill

Broyhill Asset Management, LLC (“Broyhill” or the “Firm”) is a Charlotte-based investment firm managing over $270 million in assets. Originally established as a family office nearly half a century ago, the firm spun out in 2022 to become an independently owned investment manager under the leadership of Chris Pavese. While Broyhill has historically explored a variety of investments for its clients, the firm is now focused on managing its flagship, global, value-oriented, public equity strategy. With a verified track record approaching ten years, the firm serves a diverse client base – including institutions, advisors, and high-net-worth families – by delivering long-term capital appreciation with a rigorous focus on capital preservation through disciplined, bottom-up security selection.

Broyhill Asset Management, LLC (“BAM”) is an investment adviser in North Carolina. BAM is registered with the Securities and Exchange Commission (SEC). Registration of an investment adviser does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. BAM transacts business only in states where it is properly registered or exempt from registration. A copy of BAM’s current written disclosure brochure filed with the SEC, which discusses, among other things, BAM’s business practices, services, and fees, is available through the SEC’s website at www. adviserinfo. sec. gov.

Advertisement

Separately Managed Accounts

The performance of the Broyhill Equity strategy is representative of a composite of numerous separately managed accounts and is considered to be a “carve out” or “extracted performance. ” The calculation methodology for this composite for the period from 9/1/15 through 12/31/23 has been verified by a third-party performance verification firm and reflects the equity returns of actual Broyhill client portfolios. The calculation methodology for the periods after 12/31/23 is the same as the methodology that was verified. The Broyhill Equity strategy performance results are based on the weighted average performance of the portion of individual managed accounts invested in the Broyhill Equity strategy, but may not represent the performance of the entire client portfolio. Since many of BAM’s managed accounts are invested per a “balanced” investment model, we believe that this extracted performance composite, which includes only fully discretionary equity holdings of all BAM discretionary accounts, is the most accurate representation of BAM’s long-term equity performance. Additionally, since this performance represents a pure equity allocation, it does not include the impact of any cash allocation. Performance figures for the total portfolio composite are available upon request. This data may be useful for an investor evaluating Broyhill, although individual results may differ based on each account’s investment objectives, the date of initial funding, the opportunity set available at the time, specific investment vehicles available to the accounts, and individual fee schedules.

Performance of the Broyhill Equity strategy composite is calculated using time-weighted rates of return, net of all fees and expenses, and reflects the reinvestment of dividends and other earnings. Since the composite returns are calculated gross of fees, in order to report net returns, the highest annual management fee we charge (1.5% per annum) has been subtracted from gross reported returns to arrive at the net returns shown.

Broyhill Vitruvian Value, LP

Advertisement

The performance of the Broyhill Vitruvian Value (“BVV”) strategy presented herein is hypothetical and does not reflect the performance of any actual investment portfolio. The results are provided for illustrative purposes only and do not represent actual trading or investment results. Hypothetical returns have inherent limitations and do not account for all factors that may affect actual performance, including market conditions, liquidity constraints, fees, and other expenses. Past or hypothetical performance is not indicative of future results, and no representation is being made that any investment will or is likely to achieve returns similar to those shown.

The performance of the BVV strategy is representative of a composite considered to be a “carve out” or “extracted performance. ” The calculations performance of this composite from 9/1/15 through 12/31/23 has been verified by a third-party performance verification firm and reflects the equity returns of actual client portfolios invested in the BVV strategy. The performance calculation from 1/1/24 through 6/30/25 uses the same methodology as the verified period and also reflects the equity returns of actual client portfolios invested in the BVV strategy. For the period from 7/1/25 onward, the returns shown use the actual monthly returns for Broyhill Vitruvian Value, LP (“BVV LP”). These results are based on the weighted-average performance of the portion of individual accounts invested in the BVV strategy and may not reflect each account’s

entire portfolio performance. Since some of BAM’s accounts are invested per a “balanced” investment model, we believe that this extracted performance composite, which includes only discretionary equity holdings of all BAM discretionary accounts deploying the BVV strategy, is the most accurate representation of the BVV strategy’s long-term equity performance. Additionally, since this performance represents a pure equity allocation, it does not include the impact of any cash allocation. Performance figures for the total portfolio composite are available upon request. This data may be useful for an investor evaluating an investment in BVV LP.

While some of the BVV strategy’s performance has been verified by a third-party performance verification firm, none of the performance presented herein has been audited. All figures presented herein are unaudited. Furthermore, BAM does not undertake to update any information contained herein as a result of audit adjustments or other corrections.

Advertisement

Performance of the BVV strategy composite is calculated using time-weighted rates of return and reflects the reinvestment of dividends and other earnings. Since the composite returns are calculated gross of fees, in order to report net returns, management fees and performance fees with rates and terms matching the BVV LP Class A interests have been subtracted from gross reported returns. This calculation means these returns are considered to be “hypothetical. ” Hypothetical returns have inherent limitations and are provided for illustrative purposes. The fees, rates, and terms applied are summarized as follows: an annual management fee of 1% per year, a performance fee of 20% on earnings over an annual hurdle rate of 8%. The 8% hurdle rate resets annually and does not compound. The account is also subject to a high-water mark, so a performance fee is not earned if the account value is below that mark.

General Disclaimers

The investment return and principal value of an investment will fluctuate. Therefore, an investor’s account, when liquidated or redeemed, will almost always have a different value than that shown herein. Current performance may be lower or higher than the return data quoted herein.

Past performance is not indicative of future returns. This information should not be used as a general guide to investing or as a source of any specific investment recommendations and makes no implied or expressed recommendations concerning how an account should or would be handled, as appropriate investment strategies depend upon specific investment guidelines and objectives.

Advertisement

Information presented herein is subject to change without notice and should not be considered a solicitation to buy or sell any security. This document contains general information that is not suitable for everyone. The information contained herein should not be construed as personalized investment advice.

The opinions expressed herein represent the current, good-faith views of BAM at the time of publication and are provided for limited purposes, are not definitive investment advice, and should not be relied upon as such. There is no guarantee that the views and opinions expressed in this document will come to pass. Investing in the stock market involves gains and losses and may not be suitable for all investors. No representations, expressed or implied, are made as to the accuracy or completeness of such statements, estimates, or projections, or concerning any other materials herein.

Under no circumstances does the information contained within represent a recommendation to buy, hold, or sell any security, and it should not be assumed that the securities transactions or holdings discussed were or will prove to be profitable. There are risks associated with purchasing and selling securities and options thereon, including the risk that you could lose money. Any securities mentioned in these materials may or may not be held by clients of BAM or by BVV LP currently or in the past.

Certain information contained herein constitutes “forward-looking statements, ” which can be identified by the use of forward-looking terminology such as “may, ” “will, ” “should, ” “expect, ” “anticipate, ” “project, ” “estimate, ” “intend, ” “continue, ” or “believe, ” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and

Advertisement

uncertainties, actual events, results, or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance, or representation of the future.

Market value information (including, without limitation, prices, exchange rates, accrued income, and bond ratings furnished herein) has been obtained from sources that BAM believes to be reliable and is for the exclusive use of the client. Market prices are obtained from standard pricing services or, for less liquid securities, from brokers and market makers. BAM makes no representations, warranties, or guarantees, express or implied, that any quoted value necessarily reflects the proceeds that may be received on the sale of a security. Changes in rates of exchange may have an adverse effect on the value of investments.

Index Disclaimers

Indices are unmanaged and do not incur management fees, transaction costs, or other expenses typically associated with an actively managed investment. Index performance is shown for illustrative purposes only and does not reflect the performance of any investment strategy offered by BAM. Index returns assume the reinvestment of dividends and capital gains, unless otherwise noted.

Advertisement

The S&P 500 Index is a long-only market-capitalization-weighted index comprised of 500 large-cap U. S. companies. The MSCI ACWI Index is a long-only index composed of over 2,500 large and mid-cap companies across 23 developed markets and 24 emerging markets and covers approximately 85% of the global investable equity opportunity set. The MSCI ACWI Value Index is a long-only index composed of over 1,500 large- and mid-cap companies and exhibits overall value-style characteristics across 23 developed markets and 24 emerging markets. The value investment style characteristics for the MSCI ACWI Value Index construction are defined using three variables: book value to price, 12-month forward-looking earnings to price, and dividend yield. BAM’s strategies may invest globally, in both equity and non-equity securities, employ hedging strategies, and hold significant cash positions. As a result, the strategy’s composition and risk profile may differ materially from those of the indices shown herein.

You cannot invest directly in an index. References to indices are provided solely as a comparative market benchmark. Past performance of the index is not a reliable indicator of future performance of any BAM strategy.

Any third-party index data presented herein is the property of its respective owner and is provided “as is” without warranties of any kind. Such data may not be redistributed or used to create derivative works without prior written permission. Neither the index provider nor its affiliates shall have any liability in connection with the use of such data.

For additional information about other indices or strategies mentioned here, you may contact us a t ir@broyhillasset. com.

Advertisement

CONFIDENTIALITY

No part of this material may be copied, photocopied, or duplicated in any form, by any means, or redistributed without BAM’s prior written consent.

THESE MATERIALS SHALL NOT CONSTITUTE AN OFFER TO SELL OR THE SOLICITATION OF AN OFFER TO BUY ANY INTERESTS IN ANY FUND MANAGED BY BAM OR ANY OF ITS AFFILIATES. SUCH AN OFFER TO SELL OR SOLICITATION OF AN OFFER TO BUY INTERESTS MAY ONLY BE MADE PURSUANT TO THE CONFIDENTIAL PRIVATE PLACEMENT MEMORANDUM AND THE DEFINITIVE SUBSCRIPTION DOCUMENTS BETWEEN A FUND AND AN INVESTOR.

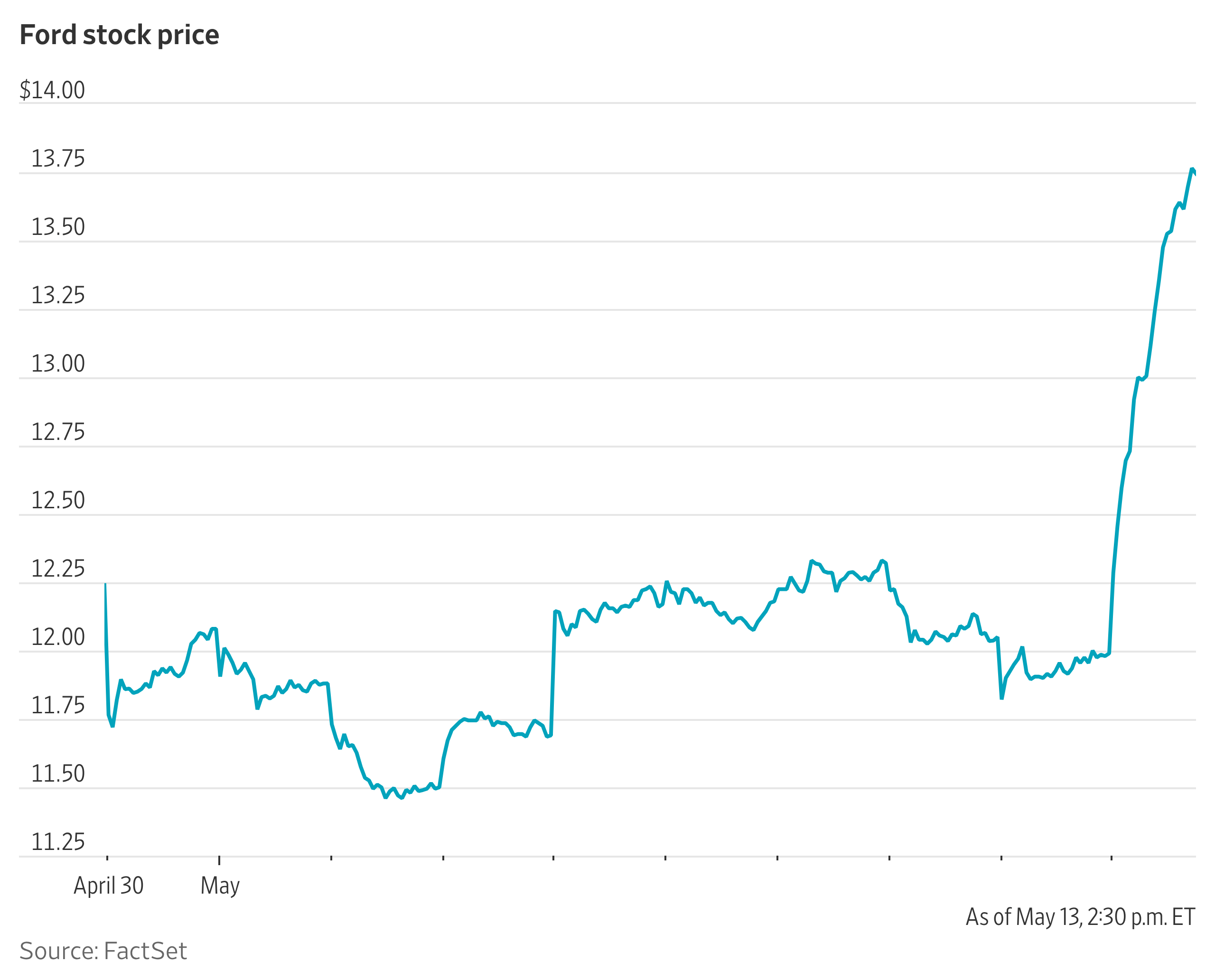

Ford Motor’s stock soared Wednesday as Wall Street cheered the automaker’s increased focus on using batteries once meant for electric vehicles as stationary energy-storage systems.

Shares were up 14% in afternoon trading, putting the stock on pace for its biggest one-day gain since March 2020. Morgan Stanley analysts cited the company’s new Ford Energy subsidiary in a note Wednesday as an “underappreciated” competitive advantage.

Energy storage systems are large stationary batteries, which have emerged as an alternative business strategy for carmakers who invested heavily in electric vehicle battery plants. Demand for EVs has slowed in recent years amid U.S. policy changes.

A meeting last week between state insurance commissioners and Treasury Secretary Scott Bessent focused on how to “make sure (commissioners) have the right regulatory tools to assess risk given this new investment landscape” of private credit and other alternative investments, Wisconsin state insurance commissioner Nathan Houdek said.

Houdek attended the private meeting in Washington D.C., and spoke about it Wednesday in response to an audience question at an actuarial conference. Houdek said Bessent requested the meeting and commissioners set it for last week when they were in D.C. for a separate conference.

Bessent said in a statement after the meeting that he emphasized the need for regulation “that encourages innovation while appropriately managing risk.” Life and annuity insurers’ private credit holdings swelled to about $1 trillion in 2025, according to insurance ratings firm A.M. Best.

You must be logged in to post a comment Login