The annual survey charts the finances of the 350 wealthiest people in the UK

07:52, 15 May 2026Updated 08:00, 15 May 2026

Sir James Dyson

Tech tycoon Sir James Dyson and family are the wealthiest people in the West of England, the latest Sunday Times Rich List has revealed.

The British inventor retains the top spot for the South West region, despite a 13.5 per cent decline in revenues at Dyson’s consumer electricals group over the past two years, partly due to President Donald Trump’s tariffs.

Advertisement

Sir James, who acquired a 50 per cent stake in Bath Rugby Group earlier this year, is one of the country’s best-known inventors, coming up with the first idea for a new model vacuum cleaner in 1979 and growing his business into one of the world’s biggest household goods firms.

However, over the last 12 months he has seen his wealth drop by £8.8bn – from £20.8bn in 2025 to £12bn. The company employs thousands of people at its base near Malmesbury, in Wiltshire, although it is now headquartered in Singapore.

Elsewhere, Plymouth retail mogul Chris Dawson and his wife Sarah were ranked the second-richest people in the region. The couple who own The Range saw their wealth grow by £50m to £2.65bn, while Peter Hargreaves, co-founder of Bristol-based investment firm Hargreaves Lansdown, saw his wealth jump to £2.325bn.

Chris Dawson, founder of The Range

This year’s list of 350 individuals and families together holds combined wealth of £783.5bn – a sum larger than the annual GDP of Belgium ($776bn), Sweden ($760bn) and Israel ($719bn), according to the Sunday Times. It represents about a quarter of the United Kingdom’s total annual GDP.

Advertisement

Sir Elton John, Lord Lloyd-Webber, Sir Mick Jagger, Keith Richards, JK Rowling, Charlotte Tilbury and Sir Lewis Hamilton all appear in the annual survey.

The rankings are topped by investors Sanjay and Dheeraj Hinduja and family (£38bn) with Newcastle United minority owners David and Simon Reuben second (£28bn), and DAZN majority owner Sir Leonard Blavatnik in third (£26.8bn).

The minimum entry level dips to £340m — another indicator of a subdued year.

Robert Watts, compiler of the Sunday Times Rich List, said: “This year’s Rich List is a tale of two exoduses. One in six of the individuals and families who appeared on the list two years ago don’t feature this time.

Advertisement

“Many foreign billionaires who have been living in the UK have also dropped out because they have moved away. We have also seen a sharp rise in the number of British nationals now resident in Dubai, Switzerland and Monaco. As UK nationals these people remain on our Rich List — wherever they now live.

“These two exoduses pose challenges for the UK economy and its public finances. Will more of the wealthy now set up or grow their ventures overseas and in doing so create fewer jobs here? How much tax – if any – will Rachel Reeves’s Treasury be able to extract from those affluent Brits who have now left the country?”

He added: “This year’s edition shines a light on fortunes made from artificial intelligence, driverless cars and crypto-currencies as well as baby milk, make-up, hoodies and other everyday items.”

The 10 wealthiest in the South West according to Sunday Times Rich List 2026

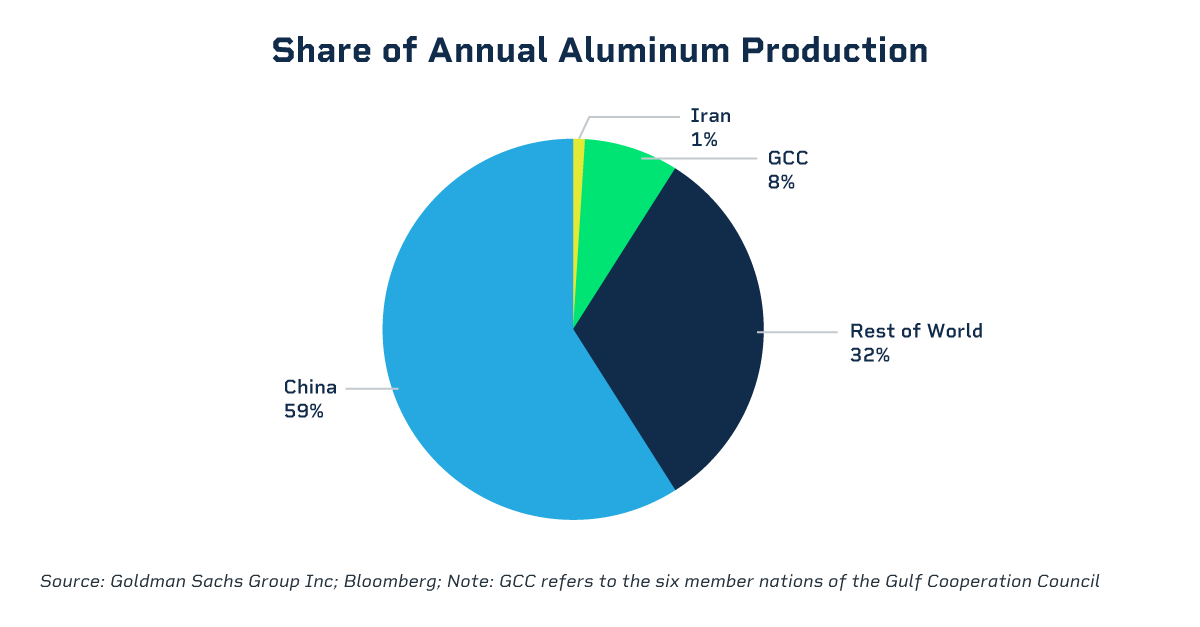

The Iran war has sent aluminum prices higher this year, unnerving a slew of global industries that rely on the base metal to manufacture cars, canned goods and aircraft.

Before the conflict began in late February, prices were hovering at $3,200 per metric ton (tonne) but rose to a four-year high of $3,500 per tonne a fortnight later as fears of supply shocks hit the market.

Advertisement

Wood Mackenzie had already predicted a 200,000-tonne deficit for this year, possibly rising to 800,000 tonnes by 2028. This was sharply higher than the roughly 50,000-tonne shortage expected as of late 2025, when electric vehicles (EVs), renewable energy (mainly solar panels) and AI data centers were taking demand to new heights.

Crucially, the war triggered the closure of the Strait of Hormuz, a vital waterway through which Middle East output – which accounts for 9% of the world’s total – reaches ports in Europe and the United States. Simultaneously, Aluminium Bahrain (Alba), which operates the globe’s largest smelter, announced it would cut output by 19% due to the maritime disruption.

“The closure of ports and plants is likely to cause significant turbulence in the aluminum market,” according to a Wood Mackenzie report, which also noted that the loss of the Gulf States’ outflows “would significantly tighten the balance over the next 6-12 months.” There are no viable ways of offsetting the loss from interrupted shipping or prolonged shutdowns.

Some carmakers, particularly EV manufacturers who use around 25% more aluminum than combustion models, have also announced they will cut production until there is greater clarity about the supply chain’s future.

Advertisement

Regional Disparities in Aluminum Pricing

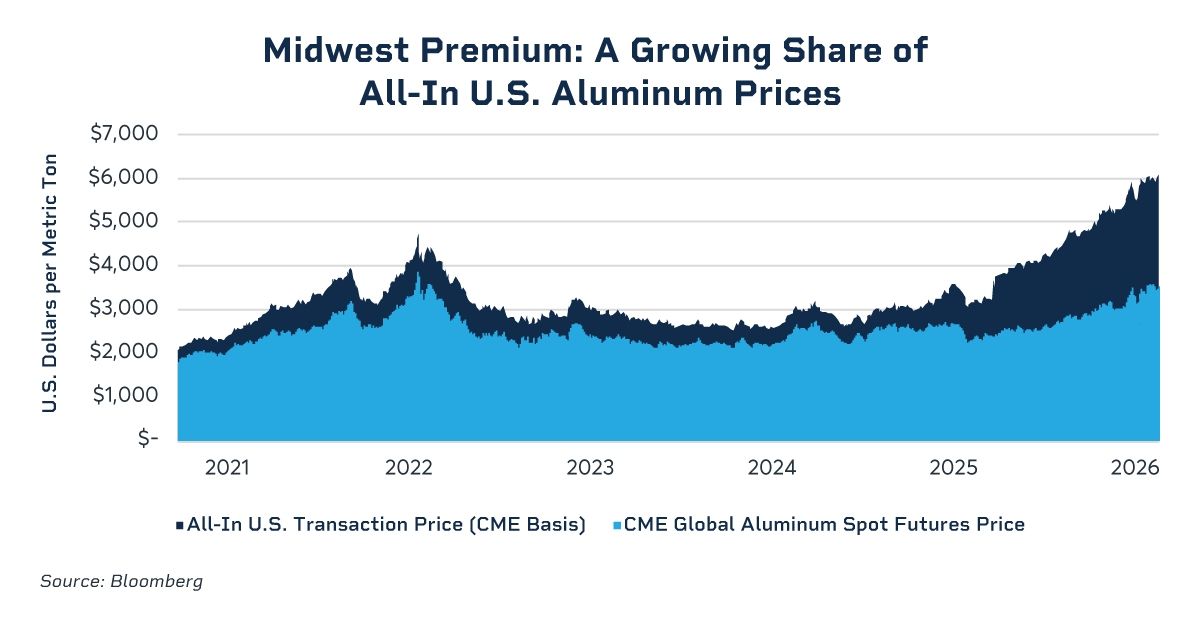

While the rising flat price of aluminum is in focus, current events are further widening regional price differentials.

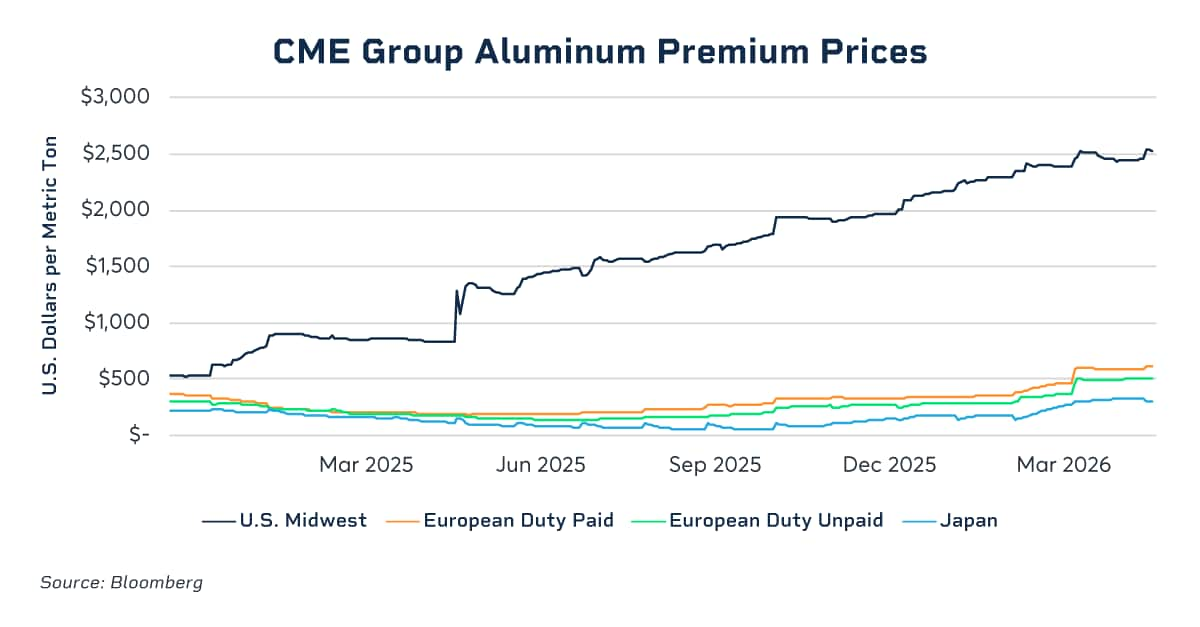

So-called physical premiums (a markup to the global price that reflects the regional fundamentals, cost of shipping and tariffs) are sharply above their pre-war baselines. The spreads – commonly called the Midwest Premium for the U.S.; the Rotterdam Duty-Paid, or European Premium Duty-Unpaid, for Europe; and the Japanese Premium for Asia – were trading around $2,529, $612, $507 and $302, respectively, as of early May. To help investors manage related price risks, CME Group offers futures on these regional premiums, in addition to futures on aluminum itself. Traders can either trade the regional premium as a standalone or the all-in price, covering the global price plus the premium.

With a historically high Midwest Premium, U.S.-bound aluminum is fetching over $6,000 per tonne, squeezing manufacturers in a country that imports the vast majority of supplies. Roughly 12% of these imports come from the Middle East, where American buyers have increasingly turned to with tariffs and sanctions significantly limiting the import and producer origins to choose from.

“Our contracts provide a key risk management tool for U.S. aluminum consumers and have become a critical piece to mitigate price risk and help protect margins,” said Ian Caton, Senior Director of Metals Products at CME Group.

Advertisement

The conflict in Iran expedited the expansion of an already-growing regional premium, he added. The introduction of Section 232 tariffs in 2018 first kicked off this increase for U.S. consumers, a trend further exaggerated as tariff policies broadened over the past year.

In contrast, European and Japanese markets face considerably smaller regional spreads, as they lack comparable tariff structures, though they have also jumped in the wake of the war.

Europe’s premium is now roughly at $612 per tonne, while Japan’s is at $302 per tonne, both up around 70% from their pre-war levels.

Interestingly, however, Europe’s Rotterdam premium surged over 50% in 2025 as a shutdown at Iceland’s key supplier, Aluminum Iceland, a carbon tax for non-EU importers and an output slump in Mozambique strangled supply.

Advertisement

In Japan, opposite forces were at play. The Asian country faced an aluminum oversupply as the automotive industry slashed production and stocks were already abundant. This brought prices lower, hitting a $58 per tonne bottom late last year. Then, as demand began to pick up and the trade blockade started, prices surged to $181 a tonne in February before settling even higher as of late April.

“The impact depends on the region,” Caton noted. “The global price plays a role, but regional considerations have become an increasing proportion of the notional value of the all-in cost of aluminum. The U.S. Midwest premium, for example, now accounts for over 40% of the all-in transaction price for aluminum in the U.S.”

Recycling to the Fore

Amid supply headwinds, U.S. buyers are bolstering their recycling capacity to ensure they have sufficient aluminum stocks.

Subodh Das, CEO and founder of industry consultancy Phinix, said the United States has invested $10 billion in the process and has the capacity to increase repurposed output to 4 million tonnes this year, up from 3 million tonnes in 2025.

Advertisement

Beyond ramping up old facilities or installing new ones, there must be a bigger effort to leverage landfilled capacity, according to Das.

“One and a half million tons of scrap are landfilled every year, while 1.5 million are exported,” he said. “We need to stop landfilling, and we need to export less.”

The U.S. could also benefit from raising production, Das added, an effort that recently got a boost after Emirates Global Aluminium and Century Aluminum struck a joint venture to make 750,000 tonnes of the metal in Oklahoma, nearly doubling current capacity from a plant it claimed will be the nation’s largest.

Despite the war’s uncertainty, Das said the U.S. has a 120-million ton aluminum reserve in landfills, largely derived from used beverage cans, that could be put to work if the conflict further impacts global stocks.

Advertisement

Alan Taub, an engineering professor at the University of Michigan’s Electric Vehicle Center, agreed more must be done to buoy recycling, especially as automobile prices continue to skyrocket.

“The aluminum price impact is the most concerning coming from the war,” he said. “We are having an automotive affordability problem with average sales prices north of $50,000. While the industry tends to know how to cope by adding extra capacity, or using materials in different ways, after adding value [like turning the metal into an automotive casting], component prices have risen dramatically.”

By adding secondary or ‘scrap’ aluminum into the manufacturing mix, industries can reap huge cost savings from lower energy usage while cutting emissions, said Taub.

But this isn’t always easy.

Advertisement

“One of the challenges in shredding [a car dismantling process] is that you get secondary aluminum that can be contaminated with iron (from steel bolts or brackets),” which can undermine the structural integrity of the resulting material, Taub said. Consequently, the industry is developing more iron-tolerant variants such as aluminum alloys blended with manganese and/or magnesium.

Even Trump, an enthusiastic supporter of both the World Cup and Fifa president Gianni Infantino, has said he “wouldn’t pay it either” when asked about the prices. Tickets for sale for the final at New Jersey’s MetLife Stadium were officially offered at up to $32,970 (£24,540), while resale tickets have been listed for more than $2m.

During a state dinner at the Great Hall of the People, President Donald Trump and Chinese President Xi Jinping toasted each other, marking a moment of diplomatic camaraderie. The event highlighted ongoing efforts to strengthen U.S.-China relations amidst complex geopolitical and economic discussions, reflecting both nations’ intentions to foster cooperation and mutual respect.

At the conclusion of the first day of recent summit meetings, former President Donald Trump and Chinese President Xi Jinping shared a symbolic moment by raising a toast. The gesture underscored the importance of diplomatic relations between the two nations amid ongoing trade negotiations and geopolitical tensions. Both leaders appeared to seek a balance between assertiveness and cooperation as they navigated complex issues affecting their countries.

The toast signaled a desire to foster dialogue and mutual understanding, even as underlying disagreements persisted. Trump and Xi’s willingness to engage in such traditional diplomatic gestures aimed to soften rhetoric and build rapport. This moment was seen as a positive step towards easing tensions and encouraging collaborative efforts on global challenges, including economic stability and security concerns.

Advertisement

Observers noted that the shared toast reflected a broader strategy to maintain a constructive dialogue during high-stakes diplomatic encounters. While not immediately resolving contentious issues, it illustrated a commitment by both leaders to keep lines of communication open. This gesture serves as a reminder of diplomacy’s role in managing international relations amid complex and often conflicting interests.

The Indian markets are entering a phase where global shocks, currency pressure, and rising energy prices are beginning to filter into domestic consumption and corporate earnings, according to Ajay Srivastava from Dimensions Corporate. In a conversation with ET Now, he highlighted that investors may be underestimating the depth of macro risks unfolding over the next few months.

Fuel price hike: “Purchasing power starts to go out from today”

Responding to concerns around the recent fuel price hike, Srivastava cautioned against assuming that the impact is already reflected in markets.

“An average person has to now shell out much more than what he was doing yesterday. The real purchasing power started to go out from today from the consumer’s pocket. I do not think so any of us has any idea what is going to happen in the next three to six months as this whole oil price shock, West Asia shock, FPIs out, rupee at 96, all starts to come into the system. Right now it is just too early for the system to react, but let it flow through because whether it is foreign currency loans, whether it is going to be your imports, whether it is going to be your consumer baskets, it is going to take time for us to understand the impact and none of that looks to be greatly positive.”

Advertisement

According to him, the combination of oil prices, geopolitical risks, FPI outflows and currency weakness could take time to fully reflect in the economy.

Live Events

Investment strategy: “Reallocate, reallocate, reallocate” On how investors should respond, Srivastava stressed aggressive diversification rather than concentration. “Reallocate, reallocate, reallocate. The only thing we are telling investors and anybody who meets me says why do you keep saying that and I say listen you need to just keep diversifying at the end of the day because whether we like it or not our economy it is very domestic, it kind of so much more impacted by what is happening domestically compared to global economy. So, it is now a cliche theme that go invest globally. We have much higher allocations for gold and silver for our investors and advisory because we have always believed that we should be much more than those 5% earlier model being touted for last two years.”He added that investors should rethink traditional allocations and consider global diversification along with alternative assets like gold and silver.

“Legacy and promoter-driven companies will outperform” Srivastava argued that in volatile markets, established and promoter-led businesses tend to outperform.

“This is the stage where you need to buy into stocks and areas which you never had, that is the key. Number two is go after legacy. Legacy companies do extremely well in turbulent time. Whether it is financial services, whether it is consumer, whether it is industrial, you will find that the legacy companies have performed the best. I am giving example not quoting, you see CG Power, you see ABB and you know what I am talking about it. And you have to go back to the thesis that Indian executives today in MNCs and other PE-led companies are a very complacent lot. It is only where promoters directly involved, you see performance.”

He further added that promoter-driven firms across sectors such as engineering, industrials, autos, materials, and financial services are better positioned to deliver returns.

Advertisement

IT sector outlook: “Just buy US IT instead” On Indian IT, Srivastava took a strongly contrarian stance, suggesting investors look outside India.

“Oh no, not at all. Not at all. Just if you want to buy IT, I will tell you one thing, just go buy US IT companies. We had a big boom IPO yesterday, Cerebras out in the US at this point of time. The themes are there… I do not think so these companies have a future with these management. They are not going to do anything for you. They have run out of ideas.”

He contrasted Indian IT firms with global technology leaders and emerging AI-driven companies in the US, arguing that innovation has shifted away from traditional outsourcing models.

Global allocation: “Compare PE ratios, you will get your answer” On increasing exposure to US equities, he pointed to valuation gaps.

Advertisement

“Well, he just has to do one comparison, just compare Walmart PE versus the PE of DMart and he will understand the answer… So, I would just say pick up any sector, look at consumer sector, just look at Unilever India, you look at Unilever Global, just see what is the PE difference and you know what you are paying for in India.”

He added that investors often ignore global valuation comparisons, despite higher multiples in India relative to global peers.

Pharma sector: selective opportunity with export tailwinds On pharma, Srivastava said the sector remains structurally strong but needs careful selection.

“Yes, but Nifty Pharma has underperformed for a fair bit and pharma has got various segments… So, I would still say sectorally it is a good place because lot of exports, rupee-dollar benefit, most of the companies, not most but literally all are debt-free companies, strong cash flows… I would tend to believe that export-driven companies in pharma sector would do very well for the next three to five years.”

Advertisement

He highlighted CRDMO and export-led pharma businesses as the most promising segments.

Bottom line Srivastava’s message to investors is that macro uncertainty is rising, consumption pressure is building, and portfolio strategy must evolve.

From global diversification and alternative assets to promoter-driven domestic companies and selective sector bets, his stance reflects a cautious but actively repositioned investment approach for the months ahead.

NEW YORK — Nearly one-quarter of New York City’s public schools are operating well below capacity, with 380 buildings — out of roughly 1,600 — running at less than 60 percent utilization this school year, according to a new analysis that spotlights the deepening enrollment crisis gripping the nation’s largest school district.

The startling figure, released by the Citizens Budget Commission, arrives as city officials project another sharp drop in student numbers. Public school enrollment currently stands around 884,400 students, down significantly from pre-pandemic levels, and forecasts warn of a further loss of up to 153,000 students over the next decade. The combination of underused buildings, fixed costs and ambitious class-size reduction mandates is forcing difficult conversations about budgets, consolidations and the future of neighborhood schools.

“This is not sustainable,” said one education budget analyst. “You cannot continue funding buildings designed for far more students than they currently serve while pouring hundreds of millions into lowering class sizes elsewhere.” The mismatch creates both inefficiency in some neighborhoods and overcrowding pressure in others.

Roots of the Enrollment Decline

Multiple factors drive the shrinking student population. Birth rates in New York City have fallen sharply since the COVID-19 pandemic, with roughly 25,000 fewer births annually compared to pre-pandemic figures. Families with young children continue to leave the city for more affordable suburbs or other states, drawn by remote work flexibility and lower housing costs. Charter school growth and homeschooling have also siphoned students from traditional public schools.

Advertisement

The School Construction Authority’s latest demographic projections paint a sobering picture. By 2034-35, enrollment could fall to approximately 721,000 students in grades K-12, a loss of more than 150,000 from recent levels. Declines are expected across all boroughs, with Brooklyn, Queens and the Bronx facing the steepest drops.

Early grades show the most dramatic shrinkage. Pre-kindergarten and kindergarten applications have plummeted, signaling that the pipeline of future students is narrowing. This trend compounds existing challenges in a system still recovering from pandemic-era learning disruptions.

Underutilized Schools Strain Budgets

The 380 schools below 60 percent capacity represent a significant fiscal burden. Many still require minimum staffing levels — principals, assistant principals, nurses and other personnel — dictated by union contracts and regulations, regardless of enrollment. Tiny schools with fewer than 150 students face particularly acute per-pupil cost spikes.

This year, 112 schools are projected to enroll under 150 students. That number is expected to rise to 134 next school year. These micro-schools collectively carry hundreds of millions in annual budgets while serving relatively few children, diverting resources from academic support, mental health services and facility maintenance.

Advertisement

Meanwhile, the city presses forward with a state-mandated class size reduction plan. New York law requires gradual caps — aiming for most classes at 20-25 students by 2027-28 — with interim targets. The system recently surpassed 60 percent compliance and eyes 80 percent next year, at a projected cost of over $1 billion annually in additional teachers and space modifications.

Critics argue the policy exacerbates inefficiencies. Funds flow to hire more staff in already compliant or low-enrollment schools while some buildings sit half-empty. Officials have explored repurposing space, but community resistance to mergers or closures remains fierce.

Political and Community Pushback

Mayor Zohran Mamdani’s administration has prioritized education spending, allocating record sums in the latest budget for class-size efforts, pre-K and mental health. Yet fiscal watchdogs urge tying funding more closely to actual enrollment, accelerating consolidations and pausing new construction in declining areas.

Parents in affected neighborhoods often fight to keep schools open, viewing them as vital community anchors. Past closure attempts have sparked protests, lawsuits and political backlash. Recent proposals on the Upper West Side and in Brooklyn ignited debates over equity, with families arguing that shuttering schools in lower-income areas disproportionately harms vulnerable students.

Advertisement

Education advocates acknowledge the tension. While small schools can offer personalized attention, extremely low enrollment limits course offerings, extracurriculars and specialized support. Larger, efficiently run schools often provide broader opportunities.

Potential Solutions and Trade-offs

Experts propose several paths forward. Strategic mergers could combine under-enrolled schools, preserving jobs while creating more robust programs. Repurposing excess space for community centers, early childhood programs or charter co-locations offers another option. Some suggest incentivizing families to fill seats through improved academics and safety measures.

Budget alignment represents the biggest lever. Shifting to a weighted student funding model — where dollars follow children more directly — could encourage efficiency without abrupt closures. The city could also revisit class-size mandates in light of demographic reality, seeking flexibility from Albany.

Longer term, addressing root causes like housing affordability, family support services and economic vitality could help stabilize enrollment. Without broader population recovery, however, the system must adapt to a smaller footprint.

Advertisement

Looking Ahead

As the 2026-27 school year approaches, with a later September start date, decisions on consolidations and budgets will intensify. The Department of Education faces pressure to balance fiscal responsibility with educational quality and community needs.

The 380 under-capacity schools symbolize a larger reckoning for urban education nationwide. Cities from Chicago to San Francisco grapple with similar declines. New York’s scale makes its choices particularly consequential.

For now, the empty desks and echoing hallways in hundreds of buildings underscore an uncomfortable truth: the city built for a million students must now thoughtfully right-size for far fewer while protecting outcomes for those who remain. How leaders navigate this transition will shape New York’s neighborhoods and the futures of its children for decades to come.

Shares of Nazara Technologies rallied as much as 18% to their day’s high of Rs 314 on the BSE on Friday after a large block deal involving nearly 4.9% of the company’s equity took place during the morning session.

As per a CNBC-TV18 report, Nikhil Kamath of Zerodha and existing shareholder Axana Estates are likely among the buyers in the transaction, while company founder Nitish Mittersain is believed to be the seller.

At the end of the March quarter, Nitish Mittersain held a 2.18% stake in the company, while Axana Estates LLP owned 5.4%.

Nazara Tech Q4

Nazara Technologies reported revenue of Rs 398 crore for Q4FY26, down 23% from the year-ago period. However, net profit surged more than 13-fold to Rs 56 crore from Rs 4 crore reported a year earlier. The company’s total expenses declined 29% to Rs 375 crore during the quarter, with advertising and business promotion expenses remaining the largest component of overall expenditure.

Advertisement

Live Events

Commenting on the company’s outlook, Nitish Mittersain said artificial intelligence is expected to significantly benefit the business and that the company is already actively investing in the space. He added that Nazara’s latest acquisition also has a strong AI focus, which is likely to strengthen capabilities further. Mittersain also welcomed Mithun Sacheti to the board as a non-executive director, citing his entrepreneurial experience and strategic expertise. Among Nazara’s three core business segments of gaming, esports and ad tech, the gaming business emerged as the largest contributor during the quarter, with revenue rising 78% to Rs 278 crore.Earlier this year, the company announced plans to raise Rs 500 crore through a preferential issue of warrants, attracting participation from Riambel Capital, S Gupta Family Investments, Plutus Investment and Holding, Classic Enterprises and Founders Collective.

Nazara also revealed plans to acquire a 50% controlling stake in Spain-based gaming studio Bluetile Games and its engagement platform BestPlay Systems for $100.3 million, or around Rs 918 crore, marking the company’s largest acquisition so far.

The company also approved fresh investments in Rusk Media and Ncore Games.

Nazara Technologies, India’s only listed gaming company, operates across mobile gaming, esports, ad tech and children’s edtech through brands including Kiddopia, Animal Jam, Fusebox Games, World Cricket Championship and Sportskeeda, along with offline entertainment brands Funky Monkeys and Smaaash Entertainment.

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

Greenville’s workforce keeps the city moving, from busy warehouses and construction sites to offices and healthcare settings where daily tasks rely on steady physical effort.

When an injury interrupts that rhythm, returning to work, even in a limited capacity, can feel like progress, but it also raises important questions about recovery and financial stability. Light-duty job offers often arrive during this uncertain phase, presenting a mix of opportunity and risk for injured workers trying to balance healing with income needs.

Understanding how these offers affect a worker’s compensation claim is essential, especially when the duties may not fully align with medical restrictions or long-term recovery goals. The details behind these arrangements can shape both treatment outcomes and benefit eligibility. A Greenville workplace injury lawyer can help review those offers carefully, ensuring that any return-to-work plan supports recovery while protecting the full value of the claim.

Why Employers Make These Offers

Employers often offer modified jobs to reduce time away from the workplace. Lower wage exposure can benefit the company, while an early return may appear cooperative to the insurer. For many injured workers, speaking with a workplace injury lawyer becomes important when a temporary assignment appears acceptable in writing but conflicts with lifting limits, pain levels, or reduced earnings. Small details in that offer can shape the claim for months.

What Light-Duty Work Usually Means

Light-duty work usually involves fewer physical demands than the pre-injury role. Common changes include less lifting, shorter standing periods, limited reaching, or reduced repetitive motion. Some employers shift a person into desk work, phone coverage, or training support. Others create temporary clerical tasks. The title matters less than the actual movements required during each hour of the day.

Advertisement

Doctor Restrictions Control the Analysis

Medical restrictions should direct every return-to-work decision. If the treating physician limits bending, pushing, twisting, or shift length, the offered position should closely match those terms. A poor fit can aggravate inflammation, increase pain, and delay tissue repair. Written restrictions carry more weight than hallway conversations, informal assurances, or verbal statements from a supervisor who does not control medical care.

Wages Can Change the Claim

Pay changes often affect the value of an injury claim. If a temporary position provides fewer hours or lower wages, partial disability benefits may still be owed. That issue warrants a close review of pay records, shift schedules, and overtime history. Lost premium pay can matter, too. A worker may return physically, yet still face measurable income loss after the accident.

Refusing an Offer Can Create Risk

Refusing a suitable light-duty job can create legal problems. An insurer may argue that wage loss ended once work became available within the stated restrictions. Still, every offer should be checked carefully before acceptance. If the tasks exceed medical limits, increase symptoms, or exist only on paper, a refusal may be justified with strong documentation and physician support.

Documentation Often Decides Disputes

Good records often influence better outcomes in disputed cases. The worker should keep the written offer, physician notes, pay stubs, and messages describing daily tasks. A short symptom log can also help, especially if swelling, numbness, or fatigue worsen after certain duties. Memory fades quickly. Therefore, consistent written proof usually carries greater weight than later recollection during a dispute.

Advertisement

Hidden Problems With Temporary Positions

Some modified assignments are legitimate and medically appropriate. Others change once the first shift begins. A position may start with seated tasks, then drift into lifting, prolonged standing, or faster production demands. That kind of shift can strain healing tissue and trigger fresh conflict in the claim. Early attention to actual duties helps reveal whether the placement is truly safe.

Medical Treatment Should Continue

A return to light-duty work does not mean the injury has healed. Follow-up visits, physical therapy, imaging, medication review, or specialist care may still be necessary. Skipping treatment can weaken the medical record and invite arguments that recovery is complete. Any symptom increase after a modified shift should be reported promptly, especially if pain, weakness, or restricted motion worsens.

A Short Review Before Saying Yes

Before accepting a position, the worker should compare the offer with the latest medical note. Important points to review include exact duties, expected pace, sitting time, standing demands, travel, and hourly pay. Clear answers reduce confusion for everyone involved. Vague terms deserve caution. Unclear expectations can hide physical demands that do not appear in the written description.

Conclusion

Light-duty work can support recovery when the assignment respects medical restrictions and preserves fair earnings. Trouble begins when the job exceeds physical limits, reduces pay, or creates a false picture of improvement. Each offer should be measured against written physician guidance, actual daily duties, and the full effect on benefits. A careful response helps protect healing, income, and the long-term strength of the claim.

Raleigh runs on a steady kind of forward motion. Between the daily flow along the I-440 Beltline, the constant rush of state employees moving through downtown near the Capitol, the growing commuter traffic feeding into North Hills and Brier Creek, and the busy stretches of Capital Boulevard pulling visitors toward RDU, the City of Oaks rarely leaves much breathing room when something goes wrong.

A sudden injury here can feel especially disorienting, whether it stems from a wreck near the Beltline, a fall inside a busy retail corridor off Six Forks Road, or a job-site incident in one of the city’s many active construction zones. What often catches people off guard is how quickly the first settlement check shows up afterward, sometimes before the doctor has even mapped out the full treatment plan. That timing alone deserves a closer look. Speaking early with a Raleigh personal injury lawyer at CR Legal helps families weigh that offer against the recovery still ahead.

The First Number Rarely Fits

A first offer often appears before swelling settles, pain patterns stabilize, or work restrictions are clear. During that uncertain period, many families review treatment notes, missed earnings, and insurance limits, then speak with a lawyer about whether the proposed sum reflects future therapy, household strain, medication costs, and the chance that recovery will take months, not weeks.

The Full Picture Takes Time

Strains, disc injuries, and concussive symptoms do not always show their full effect right away. Some patients improve within days, while others develop headaches, nerve pain, sleep disruption, or reduced mobility later. Until physicians can estimate follow-up care, any payment figure rests on an incomplete record. Money accepted too soon may fall far short if treatment expands after new findings appear.

Early Records Shape Value

Claims are priced from documents, not from visible distress. Urgent care notes, imaging results, prescriptions, therapy orders, and work limits create the medical timeline. Missing appointments can weaken that timeline, even where cost or transportation caused the gap. More complete records usually give a clearer basis for valuing pain, physical loss, and the practical burden carried at home.

Advertisement

Statements Can Narrow a Claim

Recorded statements are often requested when a patient is exhausted, medicated, or still in shock. Under those conditions, a person may guess about speed, symptoms, or earlier health issues. Later chart entries can then be measured against those guesses. Even small differences may be framed as inconsistency, which can reduce bargaining strength before the injury pattern is fully understood.

North Carolina Fault Rules Matter

North Carolina uses a strict contributory negligence rule. Under that rule, even a small share of blame can block financial recovery. Casual comments made at a scene, or during a claim call, may later be treated as admissions. Photographs, witness statements, vehicle damage, and property conditions deserve close review before anyone accepts an insurer’s account of what happened.

Deadlines Should Still Be Tracked

More information is helpful, but time limits still matter. Many North Carolina injury claims must be filed within three years of the event date, although some matters follow different rules. Early legal review can preserve camera footage, identify additional defendants, and secure witness details. That preparation helps prevent a rushed settlement from becoming the only remaining option later.

Hidden Deductions Change the Result

The amount offered is rarely the amount kept. Hospital liens, health insurance reimbursement claims, unpaid balances, and case expenses can cut deeply into the final payment. An amount that sounds reasonable during a phone call may look much smaller after those deductions are listed. Net recovery, rather than the headline number, gives a truer measure of whether settlement makes sense.

Advertisement

Daily Losses Also Count

Financial harm reaches beyond emergency treatment and repair invoices. Missed overtime, canceled shifts, child care, travel for appointments, and help with lifting or cleaning can all affect a household budget. Pain also carries value, despite lacking a receipt. A careful review counts both visible expenses and the quieter losses that change daily function after physical trauma.

Releases Usually End the Matter

Settlement papers usually include a release that closes the claim permanently. Once signed, that document often bars future payment, even if new symptoms appear or treatment becomes more invasive. Few patients would knowingly exchange a lasting waiver for short-term relief. Reading each term closely, and asking direct questions, can prevent expensive regret after funds have already been issued.

Compare Gross and Net Numbers

A careful review starts with two direct questions. How was the figure calculated, and what amount remains after every deduction is paid? That comparison can expose weak assumptions about future care, wage loss, or shared fault. It also turns an emotional decision into a practical one, which is often safer while healing is still incomplete and expenses continue to rise.

Conclusion

Fast payment may ease a short-term crisis while creating a larger financial problem later. Once a claim is closed, added therapy, delayed symptoms, or extended wage loss may stay uncompensated. A careful decision rests on medical records, realistic recovery estimates, and a clear look at what money would remain after deductions. That slower review helps protect legal options and reduces the risk that one rushed signature will shape years of physical and financial strain.

Ministers have set the high street banks on notice. The Treasury has commissioned an independent review into the impact of more than 6,700 bank branch closures across the UK, and has signalled it is prepared to compel lenders to provide face-to-face services where the evidence shows communities and small businesses are being left adrift.

The Access to Banking Review, announced on Thursday by Lucy Rigby, the economic secretary to the Treasury, will be led by Richard Lloyd OBE, the former executive director of consumer group Which? and a one-time interim chair of the Financial Conduct Authority. Lloyd has been asked to report back by October, gathering evidence on where branch withdrawals have bitten hardest, who has suffered most and where new intervention is needed.

The review lands alongside the government’s Enhancing Financial Services Bill, trailed in the King’s Speech, which the Treasury said would arm ministers with powers to “act swiftly if the evidence supports intervention on access to banking services”. In Whitehall parlance, that is unusually direct language — and a clear shot across the bows of an industry that has spent a decade thinning out its physical estate.

A decade of decline

The scale of the retreat is striking. According to consumer champion Which?, 6,719 branches have shuttered since 2015 — an average of roughly two a day. Lloyds Banking Group, NatWest, Barclays, HSBC and Santander have all taken the axe to their networks, with a fresh tranche of more than 130 closures pencilled in for May and June alone.

The economics from the banks’ perspective are not in dispute. Customers have migrated en masse to mobile apps, footfall has collapsed and the cost of running a Victorian-era branch estate has become harder to justify to shareholders. But the human and commercial fallout has been uneven, with rural towns, older customers and cash-reliant small traders disproportionately affected — a pattern Business Matters has tracked over several years and documented in its reporting on more than 6,000 UK branch closures.

Advertisement

Hubs: helpful, but not enough

The industry’s answer has been the shared banking hub: a Post Office counter for everyday cash and cheque needs, with the big lenders taking it in turns to send their own staff into a private room for more complex queries, typically one bank per weekday. Some 234 hubs have opened since April 2021, and Labour pledged in its manifesto to push the total to 350 by 2029.

Yet hubs come with a structural weakness. While the Financial Conduct Authority polices access to cash, there are no statutory rules governing what banking services must actually be provided inside a hub, those decisions remain at the banks’ discretion. The Post Office’s role as the de facto banking partner has been a lifeline for many high streets, but small business owners say the model still falls short on lending conversations, complex account servicing and the kind of relationship banking that used to be taken for granted.

That gap matters. For owner-managers running a café, a building firm or a one-van logistics operation, the disappearance of a local branch is not an inconvenience, it is a productivity tax. Cash takings have to be banked further afield. Loan applications increasingly run through opaque, centralised credit-scoring systems. And the local manager who once knew the business, and could vouch for it, has all but disappeared.

A turning tide?

There are tentative signs the industry is reading the room. Barclays last year began reopening high street branches and reinstating the role of the bank manager, an explicit bet that physical presence, and human judgement, is once again a competitive advantage. Whether that becomes a trend or remains a marketing flourish will depend in no small part on what Lloyd’s review concludes.

Advertisement

Rigby was careful to frame the exercise as evidence-led rather than punitive. “We are supporting industry’s rollout of banking hubs, but we also need a clear picture of where communities are still losing out,” she said. “This independent review will show us where the problems are and what further action may be required, and we will move quickly to legislate where the evidence shows it is needed.”

Lloyd, for his part, signalled an open-door approach. “It’s important to take stock of the impact that the big shift to digital services has already had, and to understand the need for access to in-person banking in the future,” he said. “I hope to hear from as wide a range of views as possible.”

What it means for SMEs

For Britain’s 5.5 million small businesses, the review is more than a consumer issue dressed up in policy language. Access to a banker who understands the trading rhythms of a local economy has historically been a quiet but consequential ingredient in SME growth. Should Lloyd’s report conclude — as campaigners expect — that hubs alone cannot plug the gap, the Enhancing Financial Services Bill gives ministers the statutory teeth to mandate minimum service levels.

That would represent a significant philosophical shift: from leaving branch strategy to commercial discretion, to treating face-to-face banking as something closer to a regulated utility. The banks will lobby hard against any such reframing. But after a decade in which the lights have gone out above 6,700 high street branches, the political mood in Westminster, and the patience of small business owners, is wearing visibly thin.

Advertisement

Amy Ingham

Amy is a newly qualified journalist specialising in business journalism at Business Matters with responsibility for news content for what is now the UK’s largest print and online source of current business news.

You must be logged in to post a comment Login