Crypto World

Justin Sun Sues World Liberty Financial Over WLFI Crypto Token Freeze

Justin Sun has filed a federal lawsuit in California against World Liberty Financial, alleging breach of contract, fraud, and conversion after WLFI crypto froze approximately 540 million of his unlocked tokens and barred him from governance participation.

The filing, by Sun and affiliated entities, exposes an admin-controlled blacklist function embedded in WLFI’s smart contract that allowed the team to unilaterally freeze any wallet’s transfers, sales, and protocol interactions without, Sun alleges, disclosing that capability to investors.

The core question this lawsuit raises is not who is legally right. It is whether a governance token that can be frozen by a centralized admin function was ever meaningfully decentralized to begin with – and what that means for every other WLFI holder.

- Filing: Sun sued World Liberty Financial in California federal court, charging breach of contract, fraud, and conversion over frozen WLFI holdings.

- Token freeze details: WLFI froze 540 million of Sun’s unlocked tokens and 2.4 billion locked tokens – holdings that dropped from over $107 million at the September 2025 freeze to an estimated $43–60 million by April 2026.

- Governance dispute: Sun alleges WLFI excluded him from governance activities and that the blacklist function enabling the freeze was never disclosed to investors.

- Market impact: WLFI fell 15% to a record low after Sun publicly accused the project of embedding an undisclosed backdoor on April 12, 2026.

- Sun’s exposure: Sun invested approximately $75 million directly into WLFI – the project’s largest known outside investor – with total exposure to Trump-affiliated crypto ventures reaching $175 million.

- Key watch item: The California court’s ruling on Sun’s motion for immediate token unfreezing will be the first hard signal on whether the blacklist function survives legal scrutiny.

Discover: The best crypto to diversify your portfolio with

What the Token Freeze Actually Reveals About WLFI Crypto Architecture

The dispute is, at its structural core, a governance architecture failure, not a standard investor disagreement.

WLFI’s smart contract contains an admin-controlled blacklist function that enables the project team to freeze any wallet’s ability to transfer, sell, or interact with tokens. Sun claims this capability was not disclosed to investors as required, a material omission for a project marketed as a decentralized governance platform.

The freeze was triggered in September 2025 after Sun transferred roughly $9 million worth of WLFI tokens to external wallets following the governance token launch, a move WLFI characterized as a potential violation of his investor agreement.

The project defended the blacklist as a standard compliance tool comparable to those used in USDT or USDC.

That framing matters, because it concedes the function operates like a centralized stablecoin control mechanism, not a decentralized governance token.

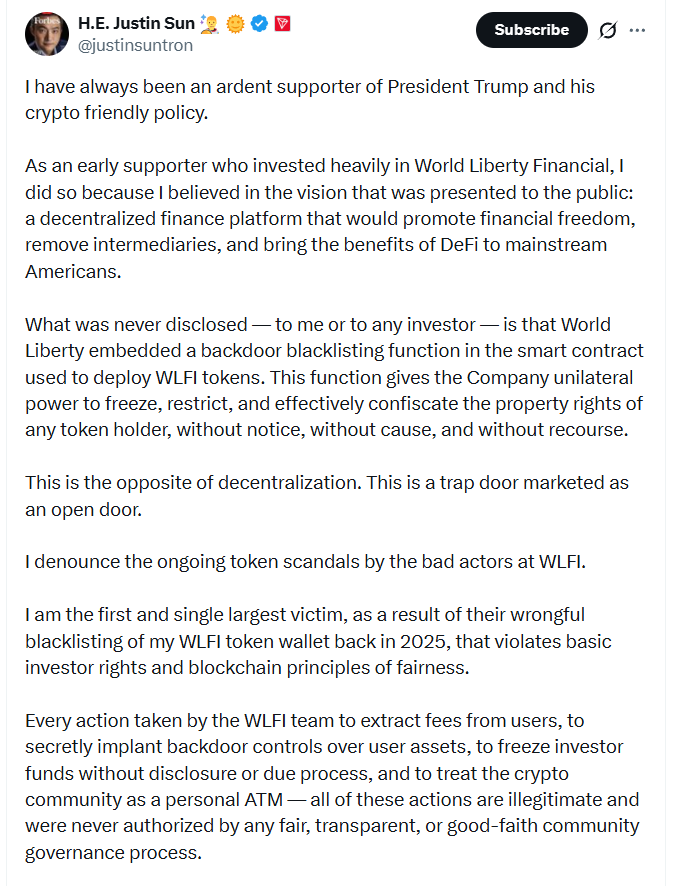

Today, I filed a lawsuit in California federal court against World Liberty Financial to protect my legal rights as a holder of $WLFI tokens. — H.E. Justin Sun

I have always been—and remain—an ardent supporter of President Trump and his Administration’s efforts to make America crypto friendly.…

(@justinsuntron) April 22, 2026

(@justinsuntron) April 22, 2026

Sun’s lawsuit seeks a court order to unfreeze his holdings, trial-determined damages, and an injunction barring WLFI from burning or otherwise tampering with his tokens.

The allegations, if proven, would indicate that WLFI’s governance token design gives its founding team veto power over any holder’s economic rights, a structural reality that extends well beyond Sun’s individual dispute. Governance disputes and frozen assets remain a documented risk across DeFi projects, as recent protocol-level failures have shown.

Discover: The best pre-launch token sales

The post Justin Sun Sues World Liberty Financial Over WLFI Crypto Token Freeze appeared first on Cryptonews.

Network News

KELP DAO EXPLOIT: A cross-chain bridge holding nearly a fifth of a restaked ether token’s circulating supply just got drained, and the fallout is moving through DeFi faster than Kelp DAO can pause contracts. An attacker drained 116,500 rsETH (restaked ether) from Kelp DAO’s LayerZero-powered bridge at 17:35 UTC over the weekend, worth roughly $292 million at current prices and representing about 18% of rsETH’s 630,000 token circulating supply tracked by CoinGecko. LayerZero is a cross-chain messaging layer, or the infrastructure that lets different blockchains send verified instructions to each other. Kelp DAO is a liquid restaking protocol, which takes user-deposited ETH, routes it through EigenLayer to earn additional yield on top of standard Ethereum staking rewards, and issues rsETH as a tradeable receipt. The bridge that was drained held the rsETH reserve backing wrapped versions of the token deployed on more than 20 other blockchains. The attacker tricked LayerZero’s cross-chain messaging layer into believing a valid instruction had arrived from another network, which triggered Kelp’s bridge to release 116,500 rsETH to an attacker-controlled address. Kelp’s emergency pauser multisig froze the protocol’s core contracts 46 minutes after the successful drain, at 18:21 UTC. Two follow-up attempts at 18:26 UTC and 18:28 UTC both reverted, each carrying the same LayerZero packet attempting another 40,000 rsETH drain worth roughly $100 million. — Shaurya Malwa Read more.

NORTH KOREA CRYPTO HEIST PLAYBOOK: Less than three weeks after North Korea-linked hackers used social engineering to hit crypto trading firm Drift, hackers tied to the nation appear to have pulled off another major exploit with Kelp. The attack on Kelp, a restaking protocol tied into LayerZero’s cross-chain infrastructure, suggests an evolution in how North Korea-linked hackers operate, not just looking for bugs or stolen credentials, but exploiting the basic assumptions built into decentralized systems. Taken together, the two incidents point to something more organized than a string of one-off hacks, as North Korea continues to escalate its efforts to hijack funds from the crypto sector. “This is not a series of incidents; it is a cadence,” said Alexander Urbelis, chief information security officer and general counsel at ENS Labs. “You cannot patch your way out of a procurement schedule.” More than $500 million was siphoned across the Drift and Kelp exploits in just over two weeks. At its core, the Kelp exploit did not involve breaking encryption or cracking keys. The system actually worked the way it was designed to. Rather, attackers manipulated the data feeding into the system and forced it to rely on those compromised inputs, causing it to approve transactions that never actually occurred. — Margaux Nijkerk Read more.

AAVE AFFECTED BY KELP DAO HACK: An attacker exploited that setup by forging a transfer message that appeared valid. The system approved the transfer even though the tokens were never taken out of the sending chain, meaning new tokens were effectively created without backing, releasing 116,500 rsETH from the Ethereum-side bridge. Rather than selling the assets on the open market, the attacker deposited 89,567 rsETH into Aave as collateral and borrowed roughly $190 million in ETH and related assets across Ethereum and Arbitrum, according to the report. This left Aave exposed to collateral whose backing may be significantly impaired. Aave Labs said it moved quickly to contain the risk. Within hours, the protocol froze rsETH markets across its deployments, set loan-to-value ratios to zero, and halted new borrowing against the asset. The outcome now depends largely on how Kelp handles the shortfall. If losses are spread across all rsETH holders, the token would face an estimated 15% depegging (meaning the value of the staked tokens would not match the value of actual ETH), resulting in about $124 million in bad debt for Aave. If losses are instead isolated to Layer 2 networks, the impact would be far more severe, with bad debt rising to roughly $230 million and concentrated on networks such as Arbitrum and Mantle.— Margaux Nijkerk Read more.

COINBASE COMMISSIONS PAPER ON QUANTUM COMPUTING RISKS: A new report commissioned by Coinbase sounds a cautious, but urgent, alarm: Quantum computing won’t break crypto tomorrow, but the industry can’t afford to wait. The 50-page paper, authored by an independent advisory board that includes prominent cryptographers and academics like Dan Boneh of Stanford University, Justin Drake of the Ethereum Foundation and Sreeram Kannan of Eigen Labs, concludes that while today’s blockchains remain secure, a future “fault-tolerant quantum computer” capable of breaking widely used encryption is increasingly plausible, and preparation must begin now. In recent months, concerns around quantum risk have moved further into the mainstream. Google researchers have published estimates suggesting that a sufficiently advanced quantum computer could one day break Bitcoin’s cryptography. Major crypto ecosystems have already started mapping out their responses. The Ethereum Foundation has proposed new types of digital signatures that are designed to be safe against quantum computers, while Solana and others are experimenting with quantum-resistant wallet designs. The report stresses that current quantum machines are far from powerful enough to crack the cryptography underpinning Bitcoin, Ethereum and other networks. Breaking standard encryption would require vast computational overhead, a milestone still considered a major engineering challenge. — Margaux Nijkerk Read more.

In Other News

- A chunk of the Kelp DAO haul is no longer going anywhere. Arbitrum’s Security Council froze 30,766 ETH worth roughly $71 million on Monday night, moving funds linked to Saturday’s $292 million rsETH exploit into an intermediary wallet that can only be accessed through further Arbitrum governance action. The council said it acted on law enforcement’s input regarding the exploiter’s identity and executed the freeze “without impacting any Arbitrum users or applications.” The transfer completed at 11:26 p.m. ET on April 20, according to Arbitrum’s statement on X. The stolen funds are no longer under the control of the address that originally held them. — Shaurya Malwa Read more.

- A Polymarket contract on whether Kelp DAO will spread the losses from the weekend’s $292 million exploit beyond those directly affected is pointing to a clear answer: probably not. Bettors are giving a 14% chance that Kelp will “socialize the losses,” or implement a mechanism forcing rsETH holders on Ethereum, which wasn’t hit, to share the pain of users on other chains. The attackers drained roughly 116,500 rsETH from a LayerZero-powered bridge that held the reserves backing the token across more than 20 blockchains. That left parts of the system undercollateralized, with some holders effectively owning tokens no longer fully backed by ether (ETH). “Socializing the losses” would mean Kelp redistributes the shortfall across all rsETH holders, including those on the Ethereum mainnet, rather than leaving losses concentrated among users and protocols tied to the compromised bridge. The most widely cited precedent of this approach came in 2016, when Bitfinex imposed losses on all users after a $60 million hack, effectively mutualizing the hit to avoid shutting down. — Sam Reynolds Read more.

Regulatory and Policy

- April appears to be a lost cause for the crypto Clarity Act, but a U.S. Senate committee hearing sometime in May could keep the critical market structure legislation alive, as long as it can reach a final vote of the overall Senate by July, according to lobbyists and a lawmaker aide focusing on the market structure bill’s sluggish progress. The legislative calendar is running out of room for this year, but a Senate aide told CoinDesk that a potential new delay of a couple of weeks — allowing Republican Senator Thom Tillis to finish discussions with bankers over stablecoin-yield concerns — is not yet pushing this work past the point of no return. The aide also said that earlier negotiations over decentralized finance (DeFi) protections are effectively settled, leaving few other impediments in the way of a committee approval.One of the chief problems the crypto industry faces (if it can leap the stubborn hurdle of the banking sector’s objections about stablecoin rewards) is that the Senate Banking Committee hearing that the bill needs to clear would be only a first step of many. — Jesse Hamilton Read more.

- Tron creator Justin Sun sued World Liberty Financial, the stablecoin and crypto firm backed by members of U.S. President Donald Trump’s family, on Tuesday, alleging that the project had unfairly locked up his $WLFI holdings, made fraudulent misrepresentations, and threatened and defamed Sun. The lawsuit filed, which includes a line about Sun’s support for Trump himself, alleged that World Liberty’s leadership had engaged “in an illegal scheme to seize property” in the form of Sun’s tokens, which Sun alleged he had purchased after being solicited by the World Liberty team in 2024. “At that pivotal time for World Liberty, Mr. Sun invested $45 million to purchase $WLFI tokens from World Liberty not only because of the project’s claims that it would promote adoption of decentralized finance — an issue Mr. Sun cares deeply about and to which he has devoted much of his life’s work — but also because of the Trump family’s association with the project,” the suit said.— Nikhilesh De & Sam Reynolds Read more.

Calendar

- May 5-7, 2026: Consensus, Miami

- June 2-3, 2026: Proof of Talk, Paris

- June 8-10, 2026: ETHConf, New York

- Sept. 29-Oct.1, 2026: Korea Blockchain Week, Seoul

- Oct. 7-8, 2026: Token2049, Singapore

- Nov. 3-6, 2026: Devcon, Mumbai

- Nov. 15-17, 2026: Solana Breakpoint, London

Blockchains were built as public networks in the best tradition of open-source technology. But their future is private. And that future is arriving faster than most people realize.

This month, Tempo — the Stripe-backed payment blockchain that raised $500 million at a $5 billion valuation, with Visa, Mastercard, Paradigm, and UBS among its backers — published a detailed architectural proposal for private enterprise stablecoin transactions. Tempo is not a scrappy privacy-native project. It is arguably the most institutionally credentialed blockchain launch in years, built by people who deeply understand what banks, payment processors, and enterprises actually need. When a network with that pedigree makes privacy a launch-week priority, it isn’t a signal. It’s a verdict.

The question of whether or not institutional chains will be private has been settled. What remains is the harder one: what kind of privacy are we actually building?

The problem with public chains

Bitcoin solved a problem that had stumped computer scientists and bankers for decades: how to transfer value between strangers without a trusted intermediary. Ethereum took blockchains further, offering programmable value alongside value transfer — smart contracts that could encode agreements, automate settlement, and eliminate entire categories of middlemen. Then came stablecoins, which married programmability to the stability of the dollar, and from there, the migration of real-world assets to onchain protocols began.

Each wave has brought added institutional interest, capital, and ambition. And now, as regulatory clarity emerges, institutions are ready to deploy resources onchain.

But there’s one thing holding them back — a fundamental flaw that becomes more consequential the larger the numbers get.

Everything is visible. Every wallet. Every balance. Every transaction, in real time, is readable by anyone with a browser. In financial markets, this is not a feature. It is an existential problem. Imagine if every hedge fund’s positions, every corporate treasury’s holdings, every pension fund’s rebalancing trade appeared on a public screen the moment it was executed. Sophisticated counterparties would front-run. Competitors would map your strategy. Criminals would identify targets. The financial system as it exists today would seize up overnight.

Blockchains have been asking institutions to accept exactly that. Tempo’s announcement on April 16 is the clearest possible signal that institutions have finally said: no.

Architecture is destiny

Here is where the conversation gets more consequential — and more nuanced.

Tempo’s solution is Zones: private parallel blockchains connected to the main network. Within a Zone, participants transact privately. The public sees only cryptographic proofs of validity, not underlying data. Compliance controls travel with the token automatically. Assets remain interoperable with Tempo Mainnet. For enterprises running payroll, treasury operations, or settlement workflows, it is a thoughtful and practical design.

But Tempo’s privacy model is operator-visible. The Zone operator — an enterprise or infrastructure provider — sees all transactions within its Zone. The public sees nothing. The operator sees everything. For many regulated institutions, this is acceptable, and may even be required. But it means privacy is contingent on trusting an intermediary. You have moved the visibility problem; you have not eliminated it.

This is not a criticism of Tempo. It is a description of a genuine architectural choice — one with real consequences for anyone thinking carefully about risk.

Zero-knowledge cryptography offers a different path. ZK proofs allow a party to prove that a transaction is valid without revealing the underlying data. A new generation of ZK-native blockchains builds this privacy-preserving functionality into the execution layer itself. Accounts execute transactions locally, with the chain storing only a cryptographic commitment. Nothing sensitive ever touches a public ledger. Transaction history is not browsable. And crucially, no operator has a god’s-eye view — privacy is enforced at the base layer, not delegated to an intermediary.

If Bitcoin gave us trustless transfer and Ethereum gave us programmable trust, ZK-native blockchains offer verifiable privacy: the ability to prove that everything happened correctly without revealing what actually happened.

Compliance without full transparency

The obvious objection is regulatory. Privacy and compliance have long been framed as incompatible — oil and water. That framing is becoming obsolete.

Regulatory compliance does not require that everyone can see your transactions. It requires that the right parties, under the right conditions, can verify that your transactions were legitimate. That is a meaningful distinction, and it is one that ZK cryptography is uniquely positioned to enforce. Selective, programmable disclosure — revealing what regulators need to see, nothing more — is not a workaround. It is a more precise implementation of what compliance actually demands.

Tempo’s model handles this at the operator level. ZK-native approaches handle it at the cryptographic level. Both satisfy the compliance requirement. But they distribute trust very differently.

The question that matters

The financial industry knows it needs to move onchain. It now knows — Tempo’s announcement makes this undeniable — that it cannot do so on fully public infrastructure. The era of public-by-default blockchains as the assumed standard for institutional finance is ending.

What comes next depends on a choice the industry is only beginning to make clearly: privacy through trusted operators, or privacy through cryptographic guarantees that require no trust at all.

Both are legitimate answers. But they are not equivalent. The privacy model you choose determines your risk surface, your compliance posture, and your exposure to the failure modes of the intermediaries you depend on. Architecture is not a technical detail to be resolved later. It is the decision that determines everything else.

The question for the industry is not whether privacy. That debate is over.

The question is what sort of privacy — and who, if anyone, you are willing to trust with the view.

TLDR

- IO Global submitted nine treasury proposals for 2026 to support Cardano’s Leios scaling roadmap.

- The company requested just under 50% of the funding it sought last year.

- Voting on the Cardano treasury proposals will remain open until May 24.

- Leios is expected to enter testnet in June with a mainnet launch planned by late 2026.

- IO Global projected a 10% to 65% throughput increase under the Leios upgrade.

Input Output Global has filed nine treasury proposals for 2026 as it prepares the Leios scaling rollout. The company said it seeks just under 50% of last year’s funding request. Voting remains open until May 24, while the roadmap centers on Leios testnet progress and a planned 2026 mainnet launch.

Cardano Treasury Request Targets Core Upgrades

Input Output Global detailed nine proposals tied to core infrastructure, developer tools, and economic changes. The firm said its combined request equals just under 50% of the prior year’s ask. It confirmed that community voting will remain open through May 24.

The roadmap aligns with its 2030 Vision for network growth and higher transaction capacity. The consensus proposal stated, “Cardano must scale from today’s approximately 800,000 transactions per month to over 27 million.” It added that “Leios is the mechanism purpose-built to get there.”

IO Global expects Leios to enter testnet in June and plans mainnet deployment by late 2026. However, its public tracker shows development in mid-stage, with testnet progress near 24%. Specifications appear largely complete, while testing continues toward broader validation.

The company projected a 10x to 65x throughput increase under the Leios upgrade. It said the change will preserve Cardano’s existing consensus mechanism. IO linked the scaling effort to support for DeFi, real-world assets, and enterprise use cases.

Layer 2 and Developer Reforms Expand Roadmap

IO Global placed Layer 2 initiatives within the broader scaling plan and named Hydra and Midgard rollup. The proposal stated that “only with both does Cardano have a credible L2 story.” It positioned the two systems as complementary components of the network’s expansion.

The company also requested 62.1 million ADA for ongoing network maintenance and operations. It valued the amount at over $15.8 million based on current market prices. IO said the funds will support node upgrades, monitoring tools, and security systems.

Several proposals addressed developer experience and onboarding challenges within the ecosystem. IO described the current environment as “fragmented” and said it deters growth. A six-month initiative will streamline tooling and reduce onboarding costs.

Internal research showed many developers leave due to high setup demands and unclear processes. One proposal aims to expand formal verification across smart contract development. IO said it will improve Plutus tooling so users avoid “a PhD and three months of setup.”

Other measures focus on user interaction and new economic functions within the protocol. Planned upgrades include “Babel Fees,” which would allow transaction fees in tokens other than ADA. The company also proposed wallet-based micro-fees to create fresh revenue streams.

A separate proposal called Pogun targets bitcoin liquidity within the ecosystem. The document described BTC as “the world’s most valuable digital asset” that remains “almost entirely idle.” IO said Cardano could serve as a credit and yield layer for that capital.

U.S. Treasury Secretary Scott Bessent arrives to testify during a Senate Committee on Appropriations, Subcommittee on Financial Services and General Government hearing in the Dirksen Senate Office Building on April 22, 2026 in Washington, DC.

Chip Somodevilla | Getty Images

Treasury Secretary Scott Bessent said on Wednesday that “many” oil-rich U.S. allies in the Persian Gulf have requested a financial backstop amid economic turbulence from the war with Iran.

Bessent’s comments go further than White House assertions to CNBC on Tuesday, where an official said the U.S. had not yet been formally asked to establish a currency swap line by the United Arab Emirates, only that there had been discussions about the topic.

Such a swap line would provide the UAE or other Gulf nations with liquidity in the U.S. dollar, but comes loaded with political risk as U.S. consumers weather higher prices from the war for food, gas and other everyday purchases.

“Many of our Gulf allies have requested swap lines,” Bessent said. “Swap lines, whether it’s from the Federal Reserve or the Treasury, are to maintain order in the dollar funding markets and to prevent the sale of the U.S. assets in a disorderly way.”

“The swap line would both benefit the UAE and the U.S., and as I said, numerous other countries, including some of our Asian allies [who] have also requested them,” he said, without specifying which other countries.

Gulf countries, including the UAE, have been hit hard by the war with Iran. Tehran has fired missiles at U.S. allies in the region, damaging economic infrastructure. Iran’s closure of the Strait of Hormuz has also choked oil revenues that are critical to Gulf nations.

A currency swap could also be necessary to ensure the U.S. dollar, which is dominant in nearly all oil exchanges, remains in use.

President Donald Trump said on CNBC’s “Squawk Box” on Tuesday that he would like to assist the UAE if it’s possible.

“If I could help them, I would,” the president said.

Sen. Steve Daines, R-Mont., who serves on both the Senate Finance and Foreign Relations Committees, was supportive of a currency swap with the UAE in a Tuesday interview with CNBC.

Daines said he thinks “[Bessent] is moving in that direction, and I support him in that.”

Democrats, however, are likely to take advantage of the political opening from a currency swap, especially with wealthy nations in the Middle East. The UAE has one of the highest per-capita incomes in the world.

Sen. Chris Van Hollen, D-Md., who questioned Bessent on the potential currency swap at the hearing, highlighted the domestic economic circumstances under which a swap would occur.

“The war in Iran has already cost us dearly, Van Hollen said. “In addition to lives lost, we’re talking about over a billion dollars a day in taxpayer money, we’re talking about higher gas prices, higher prices overall, and now we understand that the UAE is asking you to provide them a swap line through the Exchange Stabilization Fund.”

Van Hollen also noted troves of recent reporting on the UAE-U.S. relationship, including reported investments from members of the Gulf nation’s government in the Trump family’s business and the relaxing of protections around advanced artificial intelligence chips.

—Megan Cassella contributed to this report.

The crypto industry is frequently finding bankers involved in its top-priority regulatory efforts, and this time, a coalition of bank trade associations has asked the U.S. Department of the Treasury to extend the window in which the public can weigh in on implementation of last year’s Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act.

In a letter sent this week to the Treasury Department and the Federal Deposit Insurance Corp., bankers in the U.S. are asking that three different GENIUS Act rule proposals get extended comment periods, at least 60 days after another rule effort (at the Office of the Comptroller of the Currency) is finished. The OCC’s push to implement its rule for policing stablecoin issuers is meaningful to the outcome of other rules being pursued at the Treasury’s Office of Foreign Assets Control (OFAC) and the Financial Crimes Enforcement Network (FinCEN), plus a related rulemaking at the FDIC.

All the efforts are “directly contingent on the OCC’s final framework,” the bankers contend. The collective efforts, in addition to regulatory proposals that haven’t yet emerged from the Federal Reserve and other agencies, “represent a body of regulatory work of extraordinary scope and complexity.”

The banking organizations, including the American Bankers Association and the Bank Policy Institute, said that their comments “will necessarily be more comprehensive, and therefore more useful to the agencies, if we have sufficient time to evaluate the proposed rules together and to evaluate each against the finalized OCC framework.”

The GENIUS Act is meant to be in place by 2027, though it’s not unusual for federal agencies to grant extensions of comment periods on complex rules. The Treasury Department didn’t immediately respond to a request for comment on the bank industry’s request.

The same bankers are also embroiled in a stablecoin-related debate with the crypto industry that’s so far managed to delay the Digital Asset Market Clarity Act for months, and potentially jeopardize its potential for becoming law this year.

Read More: U.S. Treasury proposes demands that stablecoin firms be set to police bad transactions

Even after more than a decade and a half, the identity of Bitcoin’s pseudonymous creator, Satoshi Nakamoto, is still an active mystery that provokes discourse and disagreement.

In the last couple weeks, a New York Times piece authored by investigative journalist John Carreyrou suggested that Satoshi is in fact Adam Back, while the recent documentary Finding Satoshi pegged a two-person team, namely Hal Finney and Len Sassaman.

Protos has reviewed the evidence pointing to several of the internet’s favored candidates for this illustrious role and laid out our findings below.

Adam Back

Adam Back, the chief executive officer (CEO) of Blockstream, has often been labeled as a likely candidate for Satoshi.

Among the reasons for this is his identity as a cypherpunk, an online community which believed in the beneficial effects of freedom technology tools developed using cryptography.

Satoshi generally appears to be a cypherpunk, or at the very least to be sympathetic to cypherpunk ideas, regularly citing and conversing with others in the community.

Back was also behind HashCash, another cryptographically based digital cash technology that was cited by Satoshi.

Notably, there exist emails that Back has shared in court cases which seem to show Satoshi reaching out to Back to make sure that he appropriately cites the HashCash paper. This has led Carreyrou to ask us to consider if “Mr. Back…sent those emails to himself as a cover story.”

Carreyrou’s reporting also emphasized the fact that Back shared certain stylistic markers with Satoshi.

Among these similarities were certain phrases like “backup” and “human friendly” as well as inconsistent hyphenation in words like e-mail/email.

Despite these stylistic similarities, there are still differences, with Carreyrou noting, “Mr. Back made a lot of typos and had a rambling style when he posted to mailing lists, while Satoshi’s writing was crisp and mostly typo-free.”

Others, like YouTuber BarelySociable, have also suggested that Back is the most likely Satoshi candidate.

Back strongly denies being Satoshi.

He was also briefly considered as a candidate by Finding Satoshi; however, it concluded he didn’t post at the appropriate times to be Satoshi.

Hal Finney

Hal Finney was a cryptographer who was the first person to receive bitcoin (BTC) from Satoshi.

Like Back, he seems to have many of the necessary skills, even working on a previous digital cash, Reusable Proofs of Work.

Finney was the first person to participate in a BTC transaction with Satoshi.

Read more: Why Hal Finney might not be Satoshi Nakamoto

Multiple previous analyses have pointed to Finney as one of the more likely Satoshi candidates.

Even the stylistic analysis commissioned by Carreyrou initially concluded, “After comparing papers from the 12 suspects to the Bitcoin white paper, Mr. Cafiero’s stylometry program showed Mr. Back as the closest match. But he said it wasn’t a snug fit and that Mr. Finney was a very close second. In fact, the difference between them was barely distinguishable, he said, and he considered the overall result inconclusive.”

In response to this inconclusive result, Carreyrou suggested that Cafiero change the methodology, and “Mr. Cafiero changed the way he computed the distance between the 12 suspects’ texts and Satoshi’s white paper. The result was the opposite of what I’d hoped: Other candidates pulled ahead of Mr. Back. Mr. Cafiero said he considered these results inconclusive too.”

However, there are key stylistic differences between Finney and Satoshi, especially the use of British spellings for many of the words.

Interestingly, Finney at one point proposed creating a protocol called P2Poker that would use his digital cash, RPOW, for poker. Similarly, the original Bitcoin client contained code for a poker client.

Finney was one of the two candidates that Finding Satoshi flags as the likely Satoshi. This was supported by the times of day at which Finney posted.

Additionally, the failure of Satoshi to cite Finney is used as evidence that Finney might be trying to misdirect.

Finney also was apparently quite unproductive in the two months before Bitcoin launched and was coding at that time in C++, the language that the original client used.

Jameson Lopp, a developer in the Bitcoin ecosystem, was interviewed for the documentary due to his post insisting that Finney wasn’t Satoshi.

Lopp focuses on various emails and transactions that were sent by Satoshi while Finney was running a race.

Finney and his wife have both denied that he was Satoshi.

Paul Le Roux

Paul Le Roux created Encryption for the Masses and may be behind TrueCrypt (although denies involvement in the project).

Additionally, Le Roux was behind an international drug cartel, got involved with arms dealing, and was involved in a variety of murders and assassinations.

Besides that illustrious career, some speculate that he may be behind Bitcoin.

Le Roux has been included as a possible Satoshi since 2019 when Evan Ratliff suggested it as a possibility in an article in Wired.

However, Ratliff also noted that there was insufficient evidence at the time to substantiate the idea.

One of the reasons that Le Roux is an attractive candidate is that his arrest corresponds somewhat to some of the late Satoshi posts, suggesting to some viewers that Satoshi’s withdrawal from the public may have been rooted in these legal issues.

Le Roux was arrested in September 2012, after several of his conspirators and associates had been arrested in the months beforehand. Satoshi told Mike Hearn that he’d “moved on to other things” in April 2011.

However, we should note that there are 17 months between these two dates, over a year, for a technology that was only a few years old.

Finding Satoshi considered Le Roux before concluding that he wasn’t the Satoshi candidate, believing he didn’t fit the profile they constructed for him.

Craig Wright

Craig Wright is one of the least likely candidates, despite his prolific claims to being Satoshi.

Wright has spent years in complex legal cases trying to claim various levels of creation, control, or ownership over the Bitcoin system as a whole, eventually committing his reputation to a fork of a fork, Bitcoin Satoshi Vision.

Read more: Craig Wright trial reveals never-before-seen emails from Satoshi Nakamoto

Throughout Wright’s legal battles, judges, lawyers, critics, journalists, and neutral viewers of every sort have regularly observed his willingness to flout reality and invent history.

Eventually courts in the UK ordered Wright to display a notice that made clear that he wasn’t Satoshi, and acknowledge that he had “lied to the Court extensively and repeatedly.”

Dave Kleiman

Dave Kleiman was, largely, pulled posthumously into Satoshi speculation by Wright.

Kleiman was initially suggested as a possible Satoshi candidate when documents suggesting his involvement with Wright to create Bitcoin were distributed to the press in 2015.

Wright would later endorse this theory publicly.

Read more: David Kleiman’s estate appeals Bitcoin verdict, says ‘Wright is wrong’

Kleiman’s family would end up suing Wright, claiming he’d misappropriated Bitcoin-related intellectual property from the partnership between the men.

Wright owes the Kleiman estate substantial amounts in this case.

Len Sassaman

Len Sassaman was a cryptographer and cypherpunk.

Sassaman has been proposed a couple times, often again because he had both the technical skills and desire to build this kind of thing.

There are also some stylistic similarities between the two.

Sassaman died by suicide in July 2011, several months after Satoshi said he had “moved on to other things.”

Read more: Will HBO documentary unveil Bitcoin’s creator, Satoshi Nakamoto?

Sassaman was the other candidate flagged by Finding Satoshi because of the times that he posted.

Additionally, we are told by Sassaman’s widow that Sassaman was very interested in pseudoynyms and avoiding stylometric analysis.

Interestingly, as the documentary observes, Sassaman regularly publicly criticized Bitcoin.

Peter Todd

Peter Todd, a bitcoin developer, was the candidate flagged as Satoshi in the HBO documentary Money Electric.

This theory relied on Todd’s background as a cryptographer, raised by an economist.

Todd denies being Satoshi.

Todd has also been accused of sexual misconduct, allegations he also denies, and he has filed a suit against the person who made the allegations.

Nick Szabo

Nick Szabo is a programmer, cryptographer, and the creator of smart contracts and Bit Gold.

Szabo is one of the forerunners cited in the Bitcoin whitepaper and has been put forward as a Satoshi candidate for years.

Szabo was considered a possible candidate by Finding Satoshi before concluding he didn’t post at the appropriate times to be Satoshi.

Other Satoshi candidates

Dorian Satoshi Nakamoto was originally flagged by Newsweek in a disastrous misdiagnosis.

Wei Dai was considered as a possible Satoshi by Finding Satoshi; however, it concluded he didn’t post at the right times.

Other even less credible candidates have been put forward, including Elon Musk, Ross Ulbricht, and assorted random mathematicians and cryptographers.

Did Finding Satoshi find Finney and Sassaman?

Put simply, the documentary provides effectively zero new insight into the long-standing question: Who is Satoshi Nakamoto?

At one point, Kathleen Puckett, a former behavioral analyst at the FBI, makes the argument that Satoshi is an individual because Satoshi always used “we,” a plural pronoun, just like Theodore Kaczynski, the Unabomber, who she exposed.

That isn’t evidence.

Another piece of “evidence” she cites is the fact that Satoshi cited a book from the 1950s, An Introduction to Probability Theory and Applications, in the whitepaper.

Puckett believes this suggests that Satoshi is either older than we thought or a free thinker.

However, Satoshi cited this paper because he believed that the best way to capture the probability of an attacker catching the honest chain was an example of a “Gambler’s Ruin” problem.

So rather than being evidence about the type of person that Satoshi is, instead it mostly tells us that he knew probability math.

The very fact that every serious investigative journalist, documentarian, and random Twitter personality has their own candidate really suggests that we need to stop trying.

Each and every one uses a different combination of stylistic analysis, a different set of vibes, and a different set of hunches from people who maybe worked with Satoshi; at the end of the day they’re all speculating.

There are quite a few people who have the interest, who have the capability, who were present in these communities at this time.

None of these candidates are willing to sign; none of these candidates are willing to move BTC; none of these candidates (at least the believable ones) claim to be Satoshi.

This is a cryptographic system where every person who investigates it is forced to rely on weak circumstantial evidence, because the cryptography that would provide real evidence will not appear.

Let dead men lie.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Russia moved closer to formal crypto regulation after lawmakers advanced a key digital currency bill in its first reading. The proposal sets a timeline for licensed trading and stricter controls. It outlines phased enforcement starting in 2026 and extending into 2027.

Russia Advances Licensed Crypto Framework

The State Duma approved draft bill No. 1194918-8 during its first reading this week. The legislation defines a core structure for digital currency operations across Russia. It places crypto trading under the supervision of the Bank of Russia.

The proposal allows residents to buy and sell crypto through approved intermediaries starting July 2026. However, it bans unlicensed platforms from operating by July 2027. Authorities aim to shift activity into regulated channels and reduce informal trading networks.

Lawmakers also introduced related bills alongside the main framework. Another draft, No. 1194929-8, passed its first reading during the same session. Together, these measures outline a broader plan to reshape the domestic crypto market.

Key Rules Target Retail Access and Market Limits

The bill sets strict eligibility rules for digital assets available to retail users. Authorities limit access to highly liquid cryptocurrencies meeting defined thresholds. These thresholds include market capitalization, trading volume, and operational history.

Assets must maintain an average capitalization above five trillion rubles over two years. They must also show daily trading volume above one trillion rubles during that period. Additionally, each asset must have at least five years of trading history.

Retail participants must pass a qualification test before accessing crypto markets. Moreover, the bill caps annual purchases at 300,000 rubles through a single intermediary. These rules aim to control exposure while maintaining supervised participation.

The legislation also permits residents to use foreign accounts for crypto purchases. However, users must report all such transactions to tax authorities. At the same time, the law continues to ban crypto payments inside Russia.

Enforcement Plans Face Legal and Industry Concerns

Lawmakers introduced separate drafts to define penalties for violations under the new system. Draft No. 1209607-8 proposes criminal liability for unlicensed crypto services. It also mandates registration with the central bank for all operators.

However, the Supreme Court of Russia reviewed the proposal and declined support in its current form. The court stated that enforcement rules depend on the main framework. It noted that penalties cannot function without a finalized regulatory base.

This response signals delays in implementing strict enforcement mechanisms. Authorities must first finalize the core digital currency legislation. Only then can supporting measures take full effect across the system.

Meanwhile, industry participants continue to assess the proposed structure. Some local stakeholders warn that strict controls could shift activity outside regulated platforms. They argue that excessive limits may push trading into informal channels instead of formal markets.

Russia has maintained a cautious stance toward crypto since its 2021 digital assets law. That framework allowed ownership but banned payments using digital currencies. The new legislative package builds on that approach while tightening oversight and market access.

Consequently, the current bill represents a significant step toward centralized control of crypto activity. It reflects a policy direction focused on supervision, compliance, and restricted participation. Further readings and amendments will determine the final shape of Russia’s crypto market structure.

The crypto exchange advocated for two key changes to US tax law affecting crypto users to “eliminate millions of unnecessary forms.”

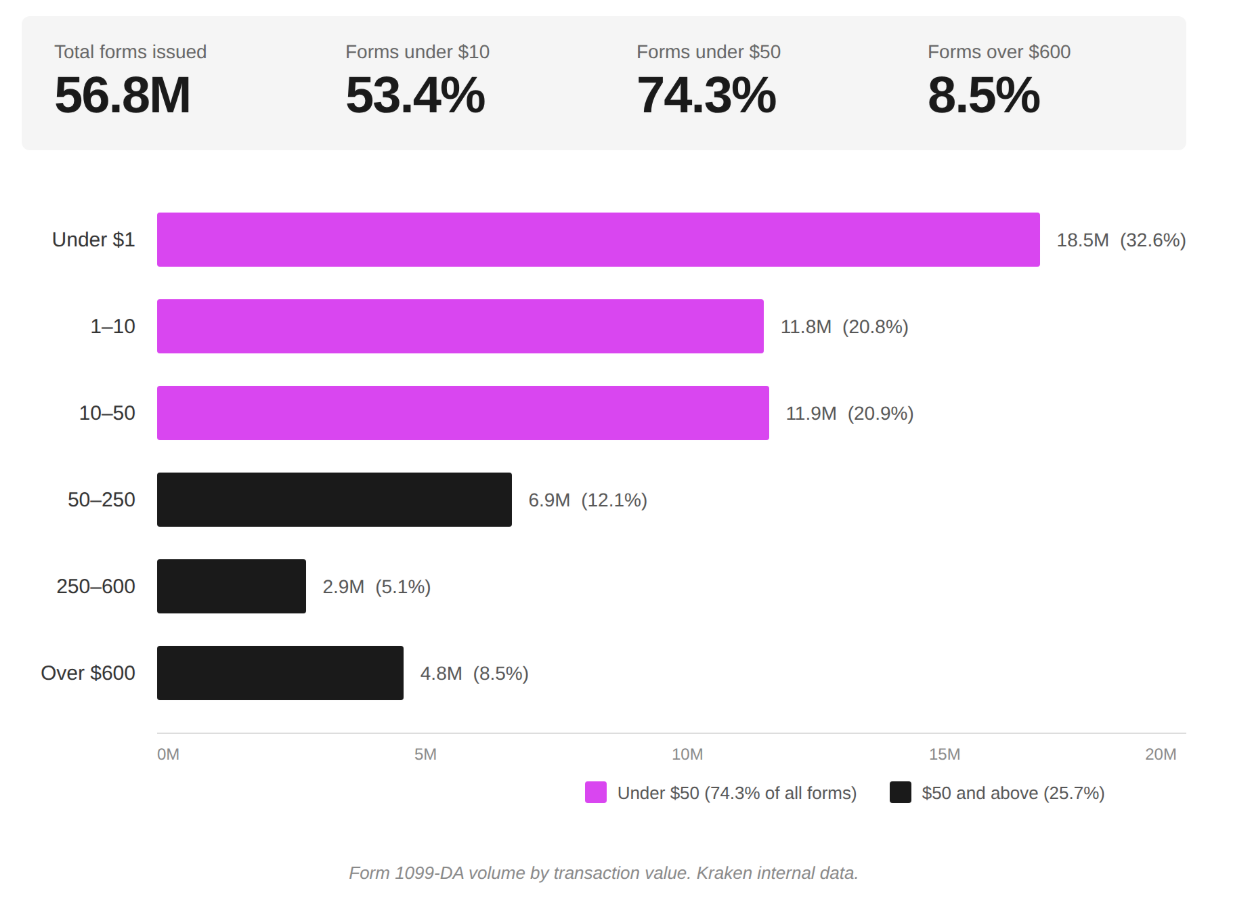

Cryptocurrency exchange Kraken called for a change in US tax policy after reporting millions of cases of transactions “worth less than $1” as part of its reporting requirements for 2025.

In a Wednesday blog post, Kraken said it issued more than 56 million tax forms — 1099-DAs — to the US Internal Revenue Service (IRS) in 2025 as now required by law. However, the exchange said that about 18.5 million of those forms were for transactions under $1, with about 28 million for $10 or less and 75% under $50.

In an effort to “eliminate millions of unnecessary forms,” the exchange called for a de minimis exemption for taxes to exclude “small, routine digital asset payments from capital gains reporting.” It similarly advocated for an end to “phantom” income derived from staking cryptocurrencies, requiring holders to “owe taxes on value they have not realized” by not selling their staking rewards.

“This is not about helping crypto companies,” said Kraken about its recommendations. “It is about 55 million Americans, spanning every state, age bracket and industry, who are navigating a tax system designed before digital assets existed. Congress should act to make taxpayers’ lives easier.”

Reporting requirements for both holders and exchanges have changed significantly since the advent of cryptocurrencies. Although there have been proposals for a de minimis tax exemption for cryptocurrencies like Bitcoin (BTC), the most recent draft bill in the US Congress suggested that only stablecoin transactions under $200 trigger reporting to the IRS.

Related: NY lawmaker proposes ‘AI dividend’ to address potential job losses

According to a Fortune report citing data from the nonprofit Tax Foundation, individual returns cost US taxpayers $146 billion in time and out-of-pocket expenses. The Trump administration ended the IRS’s free Direct File tax filing program in November 2025. The program had allowed eligible taxpayers to file their taxes online at no cost.

Kraken still reportedly considering IPO

After the crypto exchange filed for a confidential initial public offering (IPO) with the US Securities and Exchange Commission in November 2025, reports signaled that Kraken may have put its plan on hold amid volatile market conditions. However, Kraken co-CEO Arjun Sethi confirmed reports at a Semafor event in April that the company would likely go public soon.

Magazine: How to fix insider trading on platforms like Polymarket and Kalshi

TLDR

- Spirit Aviation (FLYYQ) stock exploded by as much as 218% Wednesday following news of potential federal rescue financing

- Trump White House reportedly in final stages of negotiations for approximately $500 million emergency loan

- Proposed agreement may include warrants granting government potential equity ownership in the airline

- The discount carrier was approaching possible liquidation without external financial intervention

- Soaring jet fuel costs, which have roughly doubled in certain U.S. regions, compound the airline’s financial woes

The struggling discount airline has been navigating turbulent waters for months. Wednesday’s developments, however, sparked renewed optimism among shareholders — though uncertainty remains.

Spirit Aviation Holdings (FLYYQ) rocketed as much as 218% during Wednesday’s trading session after news broke that the Trump White House is conducting final-stage negotiations to extend approximately $500 million in emergency capital to the financially troubled budget carrier.

Spirit Aviation Holdings, Inc., FLYY

Shares had already climbed roughly 122% during Tuesday’s session when initial reports surfaced that Spirit had approached Washington seeking federal assistance.

According to The Wall Street Journal’s initial coverage and subsequent CNBC confirmation via anonymous sources with direct knowledge, the discussions are progressing rapidly.

Under the contemplated arrangement, federal authorities would extend senior-level financing, positioning the government ahead of existing creditors. The package may also feature warrant provisions, granting Washington the option to purchase equity at predetermined prices — potentially establishing the government as a significant stakeholder.

President Trump acknowledged the situation Tuesday during a CNBC Squawk Box interview, stating: “Spirit’s in trouble, and I’d love somebody to buy Spirit. It’s 14,000 jobs, and maybe the federal government should help that one out.”

White House communications also targeted the former administration’s policies. Press representative Kush Desai noted that Spirit “would be on a much firmer financial footing had the Biden administration not recklessly blocked the airline’s merger with JetBlue.”

Spirit refused to address the financing negotiations specifically. The company issued this statement: “We are operating our business as normal; Guests can continue to book, travel and use tickets, credits and loyalty points as usual.”

The Association of Flight Attendants-CWA, representing Spirit’s flight crew members, expressed support for federal intervention. “We are hopeful that the government will recognize the needs for emergency funds especially in the current economic environment,” a union representative stated.

A Long Road to This Point

Spirit entered its second Chapter 11 bankruptcy filing this past August, barely one year following its initial reorganization. The airline had been implementing aggressive cost-reduction measures, downsizing its aircraft fleet, and concentrating operations on profitable routes. Labor unions representing pilots and cabin crew accepted temporary furloughs as part of survival efforts.

Management projected a bankruptcy exit during late spring or early summer in February announcements. However, that projection faced significant headwinds when aviation fuel prices surged nearly 100% across multiple U.S. markets, further eroding already-thin profit margins.

The failed JetBlue acquisition attempt two years prior eliminated what Spirit viewed as a crucial pathway to stability.

What the Deal Could Look Like

Federal financing of this magnitude directed toward a single carrier represents uncommon territory. Previous government airline assistance programs — including post-9/11 support and pandemic relief — distributed funding industry-wide rather than targeting individual operators.

The current administration has previously acquired equity positions in enterprises deemed strategically critical, such as Intel and USA Rare Earth. Spirit would mark an unprecedented case of such intervention involving a company currently operating under bankruptcy protection.

Specific agreement terms remain unconfirmed and subject to modification.

Spirit Aviation currently lacks Wall Street analyst coverage. According to TipRanks’ Technical Analysis tool, the stock presently displays a Buy signal derived from three Bullish indicators versus two Bearish signals recorded over the most recent month.

TRON founder takes the Trump-linked DeFi project to California federal court, escalating a months-long feud over blacklisted tokens and governance rights.

TRON founder Justin Sun has filed a lawsuit against World Liberty Financial in California federal court, according to an X post from Sun Tuesday night. The lawsuit marks the latest escalation in a bitter public feud between WLFI’s largest investor and the Trump family’s DeFi project.

Sun, who invested $75 million in WLFI, alleges that the project wrongfully froze his tokens, stripped his governance voting rights, and has threatened to permanently burn his holdings, all without justification. He says he exhausted good-faith efforts to resolve the dispute before turning to litigation.

“They have left me with no choice but to turn to the courts,” Sun wrote on X.

The conflict traces back to September 2025, when WLFI blacklisted a wallet holding more than 500 million of Sun’s tokens after on-chain analysts flagged transfers routed through HTX, a crypto exchange that Sun is affiliated with.

Sun is also pushing back against a new governance proposal published by WLFI on April 15 that restructures token unlocks for all major holder categories, placing early supporter tokens on a two-year cliff followed by a two-year linear vest — a timeline that would extend well past Trump’s second term. Holders who decline the new terms face indefinite token locks. Sun says that because his tokens are frozen, he cannot vote on the proposal at all, as The Defiant reported last week.

Throughout his statement, Sun was careful to distinguish the project operators from President Trump himself, reaffirming his support for the administration while directing criticism at “certain individuals on the World Liberty project team.”

WLFI has fallen roughly 76% from its all-time high reached soon after launch, now trading around $0.08. The token is down 44% year to date.

Sun himself has previously been accused of fraud, namely by the U.S. Securities and Exchange Commission, which filed a lawsuit against Sun and three of his firms in 2023, alleging wash trading to manipulate the price of TRX.

The SEC dismissed the charges with prejudice last month.

This article was written with the assistance of AI workflows. All our stories are curated, edited and fact-checked by a human.

Free and inexpensive cybersecurity courses to consider in 2026

How to save money for your child!!! #wealth #savings #money #investing #finance #529 #investments

Maola introduces ultrafiltered milk

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

US brings back mandatory military draft registration

How to save money for your child!!! #wealth #savings #money #investing #finance #529 #investments

Indian Real big money…. #shorts #money #india #indiamoney

5 Financial Habits you should have.#ideapreneurnepal #financialfreedom #habitsofsuccessfulpeople

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Theodora Dress

-

Sports5 days ago

Sports5 days agoNWFL Suspends Two Players Over Post-Match Clash in Ado-Ekiti

-

Politics5 days ago

Politics5 days agoPalestine barred from entering Canada for FIFA Congress

-

Entertainment3 days ago

NBA Analyst Charles Barkley Chimes in on Ice Spice McDonald’s Fiasco

-

Business3 days ago

Business3 days agoPowerball Result April 18, 2026: No Jackpot Winner in Powerball Draw: $75 Million Rolls Over

-

Tech4 days ago

Tech4 days agoAuto Enthusiast Scores Running Tesla Model 3 for Two Grand and Turns It Into Bare-Bones Go-Kart

-

Politics3 days ago

Politics3 days agoZack Polanski demands ‘council homes not luxury flats for foreign investors’

-

Crypto World5 days ago

Crypto World5 days agoRussia Pushes Bill to Criminalize Unregistered Crypto Services

-

Politics2 days ago

Politics2 days agoGary Stevenson delivers timely reminder to register to vote as deadline TODAY

-

Tech7 days ago

Tech7 days ago‘Avatar: Aang, The Last Airbender’ Leaked Online. Some Fans Say Paramount Deserves the Fallout

-

Business6 days ago

Business6 days agoCreo Medical agree sale of its manufacturing operation

-

Business9 hours ago

Business9 hours agoRolls-Royce Voted UK’s Most Iconic Trade Mark as IPO Register Hits 150

-

Crypto World5 days ago

Crypto World5 days agoRussia Introduces Bill To Criminalize Unregistered Crypto Services

-

Crypto World4 days ago

Kelp DAO rsETH Bridge Hack Drains $292M as DeFi Losses Top $600M in Two Weeks

-

Sports7 days ago

Sports7 days agoBritish climbers complete new route in Swiss Alps

-

Tech7 days ago

Tech7 days agoFord EV and tech chief leaving automaker

-

Sports7 days ago

Sports7 days ago“Felt Much Better Today”: Josh Hazlewood Opens Up On His Recovery Win Over LSG

-

Business6 days ago

Business6 days agoCheaper Doritos and Lays helps PepsiCo win back struggling snackers

-

Entertainment7 days ago

Entertainment7 days agoRuby Rose Accuses Katy Perry Of Sexual Assault, Police React

-

Entertainment6 days ago

Entertainment6 days agoClavicular Says Streaming May Not Work Without Substances

You must be logged in to post a comment Login