Crypto World

Strive climbs 5.8% on Q1 debt clearance, unveils daily dividends

Strive Inc., the Bitcoin-focused company founded by Vivek Ramaswamy, has unveiled a bold shift toward a “Daily Dividend Company” model while reporting a debt-free quarter. In a GlobeNewswire release outlining its first-quarter 2026 results, Strive said its Variable Rate Series A Perpetual Preferred Stock, ticker SATA, will begin paying dividends every business day starting June 16, at an annualized rate of 13%. The payouts will be funded by income generated from the company’s Bitcoin treasury strategy, marking a notable departure from traditional buy-and-hold stances.

CEO Matt Cole framed the move as a milestone in a focused push to reward shareholders while leveraging Bitcoin holdings. He described a balance sheet that is no longer burdened by debt or margin requirements, positioned to weather the volatility inherent in a Bitcoin-centric strategy. The decision to deploy daily dividends follows a path similar to approaches popularized by Strategy, Michael Saylor’s venture that has used perpetual preferred stock to finance Bitcoin purchases while delivering investor payouts on a biweekly cadence. Bitcoin For Corporations contributor Adam Livingston highlighted the pace of innovation in digital credit that this approach represents, calling the daily payout model a striking development for crypto treasury management.

The company also reported an unrealized net loss of $265.9 million for Q1, attributed to a 23% decline in Bitcoin’s market value over the quarter. Strive noted that the unrealized loss largely reflects the mark-to-market hit on its Bitcoin holdings, not a realized cash outflow. The quarter’s performance underscores the ongoing challenge of aligning a volatile crypto treasury with financing and dividend objectives.

In another balance-sheet update, Strive announced it had ended the quarter with no outstanding debt after repurchasing the remaining long-term notes. The company also emphasized zero margin requirements and zero encumbered Bitcoin, portraying a debt-free, liquidation-ready posture designed to endure price swings in its flagship asset.

Strive’s stock responded to the news, rising 5.8% to $17.70 on the session and edging higher in after-hours trading. The shares are up about 2.4% for the year but remain down more than 80% over the last 12 months, reflecting the broader bear market pressures facing many crypto-focused firms. As the quarter closed, Strive reported a Bitcoin position of 15,009 coins, up from 13,628 at the end of Q1 after adding 1,381 through ongoing treasury activities. Based on current prices, those holdings were valued at roughly $1.22 billion. The company had previously disclosed it held 13,628 Bitcoin, including 5,048 acquired via its Semler Scientific deal earlier in the quarter.

Market participants will be watching how the daily dividend initiative interacts with the company’s Bitcoin yield strategies and the evolving regulatory and macro environment. The arrangement ties investor income directly to the performance and income of the Bitcoin treasury, rather than to discretionary cash flows alone. The strategy’s proponents argue it creates a more predictable income stream, even as the underlying Bitcoin price remains volatile.

In the broader crypto earnings landscape, other notable players moved in tandem with the market’s mixed tone. Nakamoto reported a substantial QoQ revenue gain in Q1—up 500% to $2.7 million, with $1.1 million coming from using its Bitcoin holdings as collateral to earn yield. Circle rose about 15% after posting a quarter with revenue up 20% QoQ to $694 million, exceeding expectations, while Coinbase posted a sizable first-quarter revenue decline, and Robinhood’s revenue also missed estimates, contributing to a mixed sector backdrop as investors digest crypto-adjacent earnings.

For context, Strive’s path sits among several crypto treasury players experimenting with increasingly sophisticated capital structures to fund Bitcoin accumulation while delivering investor value. The daily-dividend approach, if sustained, could raise the bar for how crypto-native firms think about capital markets access and liquidity during bear markets. It also invites questions about tax treatment, payout sustainability, and how such a model scales as Bitcoin pricing and volatility evolve.

Key takeaways

- Strive announces SATA daily dividends starting June 16, at a 13% annual rate, funded by its Bitcoin treasury income.

- The company exits Q1 2026 debt-free after buying back remaining long-term notes, with zero margin requirements and no encumbered Bitcoin.

- Q1 2026 posted an unrealized net loss of $265.9 million due to a 23% quarterly drop in Bitcoin’s market value.

- Strive holds 15,009 Bitcoin, valued at roughly $1.22 billion at current prices, up from 13,628 at quarter’s end.

- Stock reaction was positive, with a 5.8% intraday gain to $17.70 and a further uptick in after-hours trading; year-to-date gain around 2.4% but down about 81% year over year.

A debt-free, dividend-focused path amid Bitcoin volatility

The new daily dividend framework marks a strategic expansion for Strive beyond a simple buy-and-hold stance. By aiming to distribute daily income to SATA holders, the company attempts to offer ongoing value to investors regardless of short-term price swings in Bitcoin. The approach mirrors the broader industry tendency to blend traditional equity mechanics with crypto treasury strategies, creating hybrid instruments designed to attract income-focused investors while maintaining exposure to Bitcoin’s upside potential.

Strive’s debt elimination reshapes its balance sheet and risk profile. With no margin loans or encumbrances on its Bitcoin, the company emphasizes resilience against liquidity squeezes and market downturns. As the market digests the implications of daily payouts, investors will assess whether the yield cadence can be maintained even as Bitcoin’s price oscillates—particularly in the wake of a quarter defined by material price declines.

What the numbers suggest for the quarter ahead

Looking forward, the Q1 results illustrate a contrast between income ambitions and asset volatility. While the daily dividend program may attract income-seeking investors, the realized reality of the quarter’s mark-to-market losses underscores the sensitivity of these strategies to Bitcoin price movements. The combination of debt-free leverage, a sizable Bitcoin treasury, and daily payout commitments makes Strive a case study in crypto-native financing that could influence how peers structure capital rounds, yield-bearing instruments, and shareholder communications during a prolonged phase of price volatility.

Market observers will also be watching how Strive’s approach compares to contemporaries pursuing similar models. For example, Nakamoto’s Q1 performance showed meaningful revenue growth from yield-based strategies, while Circle and Coinbase provided a broader market backdrop—highlighting divergent outcomes among crypto-influenced firms in the same period. As the sector weighs these developments, Strive’s daily dividend initiative stands out as a notable experiment at the intersection of crypto governance, investor income, and treasury management.

Next up, investors should monitor how the daily payout schedule intersects with quarterly performance, how the Bitcoin position evolves through subsequent treasury activity, and whether the model sustains itself as macro conditions shift. The coming quarters will reveal whether this dividend strategy can deliver durable value in a volatile market while keeping Strive debt-free and nimble.

Source disclosures and quotes accompany this coverage, including the GlobeNewswire release detailing Strive’s Q1 2026 results and the company’s statements on debt elimination and daily dividends. Further context comes from related crypto treasury developments and contemporaneous earnings reports from peer companies in the sector.

The rest of the Clarity Act depends on that guarantee, because there is no digital asset market to regulate if the people who build it cannot afford to build it in the U.S. The provision survived the committee markup intact, despite a filed amendment that would have gutted it, and it must stay in through the final vote, fully and without dilution.

Here is why this matters to people who will never read a word of the statute. The engineers who write this software, from core Solana contributors to the designers of new DeFi protocols, publish code that anyone in the world can download and use. They hold no money. They cannot freeze an account or move funds, because they never touch them. Treating a software developer like a bank teller makes about as much sense as calling an email app’s engineer a mail carrier. Treasury’s 2019 FinCEN guidance already recognized that merely providing software or network tools used by money transmitters does not, by itself, make someone a money transmitter. The BRCA aligns the criminal code with that standard.

When laws are murky, regulators and prosecutors fill the gap. Treasury has pursued builders who wrote and released software but never held a customer’s assets. The conviction of Tornado Cash developer Roman Storm for conspiring to operate an unlicensed money transmitting business is the case people know, and it fits a pattern that should worry anyone who cares about American innovation. Cases like it are already pushing developers overseas.

Crypto World

Wallet V Launches Public Performance Benchmark for AI Trading Agents on Hyperliquid and Aster

[PRESS RELEASE – Road Town, British Virgin Islands, June 15th, 2026]

Wallet V, a self-custody Web3 wallet, launched a public performance benchmark for the AI trading agents that its users have configured on the third-party decentralized derivatives platforms Hyperliquid and Aster. The benchmark publishes aggregate cohort performance and is hosted on the Wallet V website.

The benchmark covers 688 agents created by Wallet V users over the prior two months. Each agent was configured by the user, used a large language model selected by the user to generate trading decisions, and executed on Hyperliquid or Aster. Wallet V aggregates the on-platform performance of those agents by underlying model. Performance is refreshed as new agents are deployed.

The cohort spans seven large language model families. Across the cohort, 42 percent of agents recorded a profit and loss balance of zero or higher over the period. Peak agent-level return on investment in the dataset ranged from negative 30 percent on the lowest-performing model to positive 307 percent on the highest. Models represented by fewer than 10 agents in the cohort are reported as directional rather than statistically conclusive.

Agents in the cohort executed strategies as perpetual futures across four asset classes available on Hyperliquid and Aster. These include major digital assets such as BTC, ETH, and SOL; equities, including pre-initial public offering equity exposure; commodities including gold, silver, and oil benchmarks; and major foreign exchange pairs. All instruments are accessed through third-party venues.

“At Wallet V, the focus has been on building infrastructure for the next phase of crypto. This benchmark is what that next phase looks like up close. Users now decide which AI model to configure their agent in the same way institutions evaluate managers, by reviewing observable performance over time,” said Adam Cai, Founder & CEO of Virgo Group.

Wallet V plans to extend the benchmark in subsequent releases. Future releases include the addition of newer model families, support for prediction markets, advanced analytics features for copilot trading and personalized AI prompt generation tailored to each user’s trading style.

The Wallet V applications for iOS and Android are available at dl.walletv.io.

About Wallet V

Wallet V is a Web3 self-custody wallet that gives users access to third-party AI models to configure AI agents and execute user-defined trading strategies. The application connects to third-party platforms supporting cross-chain swaps, perpetual futures, prediction markets, and onchain exposure to tokenized equities.

Wallet V is an incubation project by Virgo Group, a digital asset service provider led by CEO Adam Cai. Virgo Group is backed by investors including Draper Dragon, OKX Ventures, Vaulta Foundation, Cobo Ventures, Waterdrip Capital, and Sora Ventures.

Disclaimer

Trading crypto, perpetual contracts, tokenized assets, and prediction markets involves significant risk of loss and is offered by third-party platforms. Wallet V is a software provider that connects to external platforms and does not offer trading services or AI automation tools directly or indirectly. Wallet V does not provide investment, tax, or legal advice. Access to certain products may be restricted in some jurisdictions.

The post Wallet V Launches Public Performance Benchmark for AI Trading Agents on Hyperliquid and Aster appeared first on CryptoPotato.

Standard Chartered is projecting a major expansion of decentralized finance activity tied to tokenized assets, forecasting that the total value of tokenized assets actively used in DeFi could rise from today’s small base to roughly $2.7 trillion by the end of 2030.

In a research note released on Monday, Geoff Kendrick, head of digital assets research at Standard Chartered, said the growth would be powered by two streams: tokenized real-world assets (RWAs) finding their way into onchain lending, liquidity and trading venues, and crypto-native assets being routed through DeFi protocols.

Key takeaways

- Standard Chartered expects tokenized assets active in DeFi to grow 37x to about $2.7 trillion by 2030.

- Only a small portion of currently circulating stablecoins and tokenized RWAs are used in DeFi today, according to the bank.

- Standard Chartered forecasts the share of tokenized value used in DeFi to increase to 30% by 2030, from around 3.5% currently.

- The bank sees Uniswap as a plausible hub for tokenized markets as more assets move onchain.

- Other industry voices warn that tokenization alone does not ensure liquidity or unified markets, and may increase fragmentation.

Standard Chartered’s 2030 DeFi tokenization forecast

Kendrick’s central estimate is that the amount of tokenized assets “active in DeFi” will expand by a factor of 37 by the end of 2030. He framed DeFi protocols as the next major channel for wealth-building and scaling exposure to onchain assets.

The bank’s assumptions start from a relatively low present-day level of DeFi participation. Kendrick said only about 3% of stablecoins and roughly 10% of tokenized RWAs are currently used in DeFi. From there, Standard Chartered projected a substantial shift in utilization: the proportion of tokenized assets used in DeFi should rise to about 30% by the end of 2030, up from around 3.5% at present.

While the directional logic is straightforward—more tokenization could mean more onchain activity—Standard Chartered’s own math implies a demanding pathway. Reaching the $2.7 trillion outcome would require both rapid growth in the underlying stock of onchain assets and a steep increase in the fraction of tokenized value actually routed into DeFi protocols.

Previous RWA outlook, and why DeFi adoption is the crux

The forecast builds on earlier work from Standard Chartered, including a previous projection that non-stablecoin tokenized RWAs could reach $2 trillion by the end of 2028. That earlier view highlighted tokenized money-market funds and US equities as major components of projected growth.

However, Monday’s note puts the spotlight on utilization rather than issuance. Tokenization may increase the total addressable market, but investors ultimately benefit from an ecosystem where tokenized assets can be accessed, traded, and used efficiently—often through DeFi infrastructure.

This is where Standard Chartered’s numbers become both persuasive and challenging. A near ninefold rise in the share of tokenized value used in DeFi would be required to support the $2.7 trillion estimate, suggesting that liquidity routing, custody, compliance frameworks, and market-making would all need to evolve alongside the growth of tokenized supply.

Liquidity fragmentation remains a key concern

Some market participants have cautioned that tokenization does not automatically solve liquidity and market-structure problems. Axis CEO Chris Kim previously told Cointelegraph that issuing “the same asset” across multiple blockchains and formats can lead to siloed liquidity, pricing gaps, and higher costs—factors that can limit how easily tokenized assets trade even as overall market size increases.

Similarly, Oya Celiktemur, Ondo Finance’s sales director for Europe, the Middle East and Africa, said at Paris Blockchain Week in April that tokenizing an illiquid asset does not “magically” make it liquid. The implication for Standard Chartered’s outlook is clear: the path to a larger DeFi share likely depends on whether market design and distribution reduce fragmentation rather than amplify it.

Why Uniswap could matter for tokenized markets

Kendrick also pointed to decentralized exchanges as potential distribution and liquidity layers for tokenized assets. In his view, Uniswap could develop into a key hub for trading tokenized markets as more of these assets move onto public blockchains.

He cited Uniswap’s scale, its brand recognition, and its long operational history through multiple crypto market cycles. Kendrick argued these strengths could be especially relevant to traditional financial institutions, which are likely to prioritize security, reliability, and established operational risk management when integrating tokenized RWAs into onchain systems.

Standard Chartered further suggested that if Uniswap can “commercialise enough” and secure enough TradFi partnerships to scale, its market cap-to-transaction fees multiple could rise—potentially narrowing the gap with Coinbase, according to the bank’s framing.

What to watch next

For investors and builders, the next signal will be whether tokenized assets increasingly find meaningful DeFi usage—moving beyond issuance headlines into sustained liquidity, cross-venue trading efficiency, and deeper integrations with major market participants. Standard Chartered’s forecast may be directionally aligned with tokenization trends, but the durability of that growth will likely hinge on whether fragmentation and liquidity limitations can be reduced as adoption accelerates.

Bitcoin has reclaimed the $66,000 level after remarks from U.S. President Donald Trump and reports of a tentative U.S.-Iran peace agreement revived risk appetite across global markets.

Summary

- Bitcoin climbed nearly 5% to $66,829 after Trump said oil ships were moving through the Strait of Hormuz and reports pointed to a tentative U.S.-Iran peace agreement.

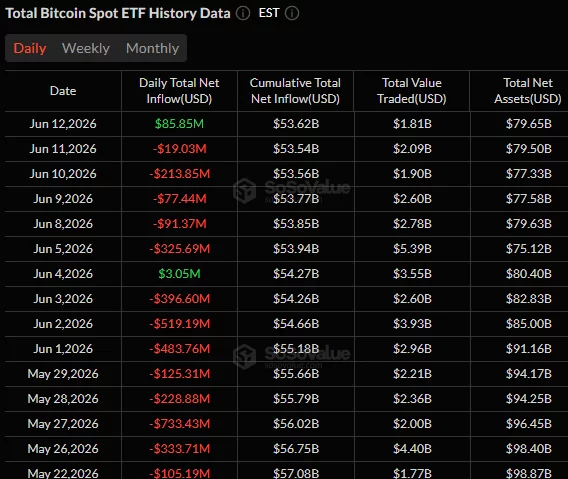

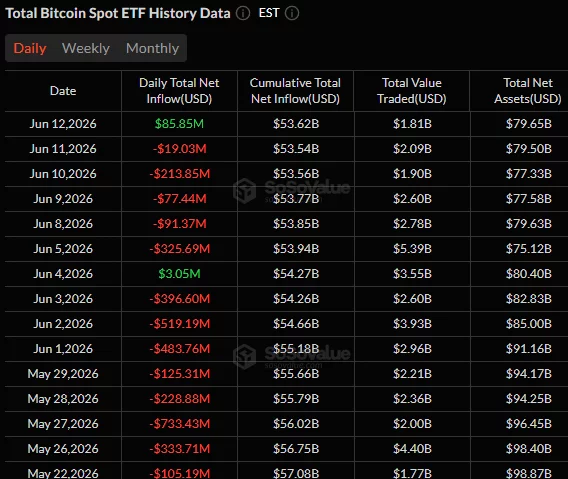

- Oil prices fell 5.7% to a two-month low below $80, while spot Bitcoin ETFs recorded $85.9 million in inflows and Strategy added 1,587 BTC worth about $100 million.

- More than $168 million in Bitcoin short positions were liquidated as BTC broke above key resistance near $65,150 and reclaimed bullish momentum.

According to data from crypto.news, Bitcoin (BTC) climbed nearly 5% to an intraday high of roughly $66,829 on June 15 before settling near $66,460 at press time.

Bitcoin price rallied following comments from U.S. President Donald Trump, who wrote on Truth Social that ships carrying oil were once again moving through the Strait of Hormuz, a key route for global energy supplies.

“Ships are starting to move, many loaded up with Oil, out of the Strait of Hormuz. They are going along the Southern “Highway,” which is totally safe, secure, and pristine. There are other areas of travel, also!!!”

The comments arrived shortly after reports that the U.S. and Iran had reached a tentative peace agreement expected to reduce risks surrounding the strategic waterway.

Crude oil fell about 5.7% to below $80 per barrel, hitting its lowest level in two months and unwinding part of the geopolitical risk premium that had built up during recent weeks. The decline eased concerns about renewed inflationary pressure and helped improve appetite for risk assets after a difficult start to June.

Institutional flows also showed early signs of stabilization. U.S. spot Bitcoin ETFs attracted $85.9 million in net inflows after five consecutive days of withdrawals. Even so, the rebound remains limited in scope. According to SoSoValue data, the funds have recorded positive flows on just two trading days since May 15 and have collectively lost roughly $5.71 billion over the past five weeks.

Alongside the return of ETF demand, corporate accumulation re-emerged as a source of support. As reported by crypto.news, Strategy disclosed the purchase of 1,587 BTC worth approximately $100 million, just two weeks after its first reported Bitcoin sale in years raised questions about whether the company’s long-standing accumulation strategy was changing.

The latest acquisition helped restore confidence among investors who viewed the earlier sale as a potential sign of weakening institutional conviction.

Bitcoin breaks above key resistance as short sellers unwind

On the daily chart, Bitcoin has reclaimed a major support-turned-resistance zone near $65,150 that had repeatedly acted as a pivot throughout March and April. Bitcoin price has now moved back above that level after briefly falling below $60,000 during last week’s sell-off.

Momentum indicators have improved alongside the recovery. The daily MACD has produced a bullish crossover while its histogram has turned positive for the first time since the June decline began. Chaikin Money Flow has also recovered from deeply negative territory, suggesting capital is returning to the market after weeks of distribution.

The four-hour chart shows Bitcoin breaking out from a descending trendline that had capped price action since late May. Bulls have also pushed the asset above the 61.8% Fibonacci retracement level near $66,402, placing the next resistance zone around $68,640, which aligns with the 50% retracement level. Beyond that, the $70,880 region represents another key hurdle.

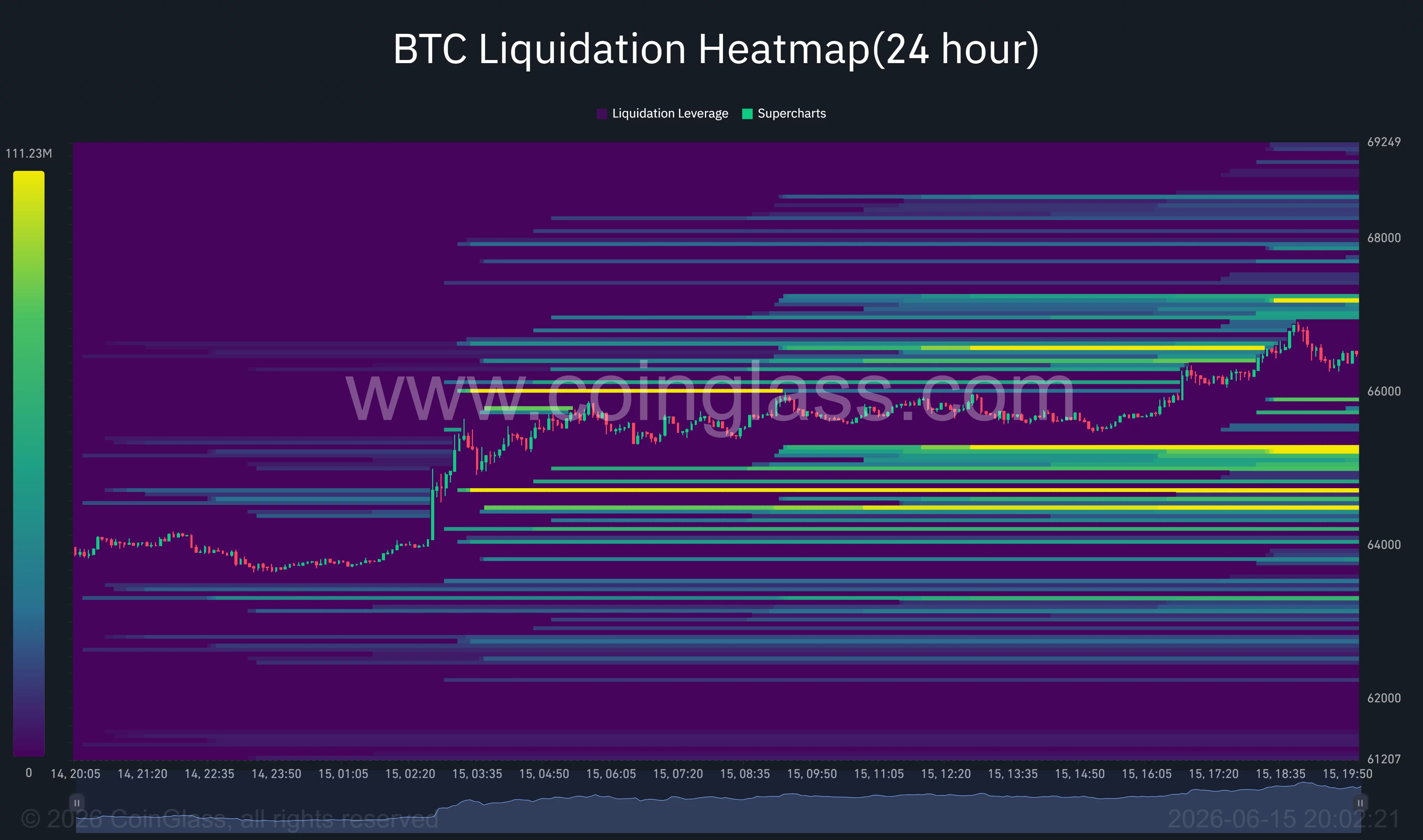

Derivatives activity accelerated the move. CoinGlass data showed more than $556.5 million in crypto liquidations over the past 24 hours, including roughly $459.9 million from short positions.

Bitcoin alone accounted for approximately $168.7 million in short liquidations compared with about $23 million from longs, highlighting the scale of the squeeze as traders rushed to cover bearish bets.

Liquidation heatmaps also show dense clusters of leverage concentrated between $67,000 and $68,000. Those zones could act as magnets for price if momentum continues, while substantial liquidity remains below the market around the $64,500-$65,000 area.

On-chain data suggests buyers have returned after Bitcoin’s correction to the $60,000 region. According to Glassnode, accumulation trend scores have increased across multiple wallet cohorts following the recent decline. The firm noted that supply is being absorbed after the move lower, a development that historically accompanies periods of renewed demand.

Options positioning presents another supportive factor. Glassnode observed that Bitcoin has moved back into a dense cluster of options exposure around the $65,000 strike, where dealer hedging flows may help stabilize price action after recent volatility.

Fed uncertainty and $65K support remain critical

Not all analysts view the move as a confirmed trend reversal. Commenting on the rally, crypto analyst Ted Pillows argued that recent price action looked more like a liquidity grab than a decisive breakout.

“If $BTC can maintain strength above $65,000, a move toward the $68,000-$70,000 range is possible.”

Despite the bullish price action, Pillows said the overall market trend remains bearish until further confirmation appears.

A different view came from crypto analyst Scott Melker, who pointed to Bitcoin’s repeated defense of its 200-week moving average and a bullish divergence on the weekly RSI. Melker noted that similar conditions have historically appeared near major market bottoms.

Attention now turns to next week’s Federal Reserve meeting on June 16-17. Any indication from policymakers that inflation remains a concern despite the recent decline in oil prices could weigh on risk assets and challenge Bitcoin’s recovery.

From a technical standpoint, a sustained move back below $65,000 would weaken the recent breakout and place the $63,200-$64,000 support region back into focus.

From a technical perspective, a move back below $65,000 would place the reclaimed support zone at risk and expose Bitcoin to another test of the $63,200-$64,000 area, where the recent breakout structure would begin to weaken.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Last week, tens of thousands of crypto wallets pledged over half a billion dollars worth of digital assets for SpaceX shares, and received none. Unfortunately, the industry’s tokenized stock failure was a repeat performance.

For nearly a decade, thousands of crypto promoters have insisted that blockchain technology will deliver tremendous value through tokenized trading of equities.

However, despite wholehearted attempts and financial support from the industry’s largest companies, trading volumes of tokenized stock remain well below a fraction of one percent of traditional stock trading volumes.

Indeed, last week, 27,689 wallets pledged $557 million worth of digital assets to participate in a tokenized version of the SpaceX IPO via Binance alone.

Across listings on various crypto exchanges, including Bybit and Bitget Wallet, all of those orders failed to deliver SpaceX shares.

For years, crypto pitched its technology as an obvious efficiency improvement over slow and expensive clearinghouses, not to mention the benefit of widenening the pool of liquidity to a global audience that struggles to open traditional brokerage accounts.

It just never worked. Again and again, promoters’ sales pitches failed to live up to the promise.

On June 12, the day SpaceX debuted on Nasdaq, Binance, Bybit, and Bitget Wallet all canceled their pre-IPO tokenized SpaceX campaigns.

By then, customers had committed more than $1 billion but got none of the shares they wanted.

Backed Finance’s xStocks, the tokenized-equity issuer acquired by crypto exchange Kraken, seemed to be a root of the problem. When xStocks could not source its underlying shares, crypto contracts around the world failed. In a representative apology, Bybit admitted, “Due to xStocks’ inability to deliver the underlying assets, no SpaceX allocations were received.”

Binance blamed similar circumstances beyond its control.

Crypto’s pattern of tokenized stock failures

The excuse, as always, was that the blockchains worked fine, if only the traditional finance plumbing would have just cooperated.

As early as December 2020, Do Kwon’s Mirror Protocol launched tokenized stocks, allowing traders to buy “mirrored” versions of Apple and Tesla stock with no brokerage account.

Although the value of mAssets had already vaporized alongside Kwon’s Terra LUNA implosion in May 2022, the SEC later described those mirrored assets (mAssets) as unregistered “security-based swaps.”

By 2023, commissioners belatedly sued Terraform Labs and Do Kwon for violating US securities laws.

Read more: Binance draws heat in Europe for stock tokens, lists MicroStrategy anyway

In 2021, crypto pitched tokenized stocks again; and again they failed.

Binance launched tokenized Tesla, Coinbase, and MicroStrategy stocks through German broker CM-Equity. FTX, meanwhile, ran a near-identical offering through the same German broker.

Regulators objected within weeks, and both exchanges backpedaled quickly.

Binance pulled those tokenized offerings by July 16, with support ending that October. FTX’s stock tokens were also gone well before the Sam Bankman-Fried fraud collapsed in November 2022.

This year, Binance’s tokenized SpaceX campaign pulled in roughly $557 million in USDC from over 27,000 wallets, and delivered no shares.

It refunded users their pledges and promised an airdrop as a consolation prize. Bybit similarly refunded customers.

Despite years of marketing, crypto technologies still have not brought tokenized stocks to the masses.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

The team behind Pi Network has remained consistent in its efforts to expand the ecosystem and strengthen the community through new initiatives and upgrades.

PI’s price has finally staged a decisive rebound, mirroring the bullish conditions of the broader crypto market following the peace deal between the USA and Iran.

What Happened Lately?

The Core Team has been quite active lately, completing major milestones on several fronts. At the start of the month, they disclosed the successful transition to protocol v24, an upgrade primarily focused on improving the underlying infrastructure supporting node operations and mainnet activity.

Most recently, Pi Network updated the participation and flow model for the Pi Launchpad, allowing Pioneers to test a second token called “SLICE” for two weeks. The platform is designed to help new projects grow and reach the community. It uses insights gathered from the first testnet token that began testing on PiDay 2026 (March 14).

The team revealed that more than 478,000 Pioneers participated in the initial Launchpad testing and “generated valuable feedback on the Launchpad mechanism.” It also detailed the steps for those who wish to join. They must open Pi Launchpad in Pi Browser, review the SLICE test token and project, choose a commitment amount in Test-Pi, confirm participation, and finally engage with the Slice of Pi app and provide feedback.

In addition to these efforts, Pi Network also made progress in the gaming sector. As CryptoPotato reported, CiDi Games (an entity part of the ecosystem) released four new games for Pioneers. Those include Coin Whack, Fruit Stack, Gemnova, and RainbowCubes. Earlier today (June 15), one X user revealed that CiDi Games had reached a milestone of over 6 million PI staked in its ecosystem and hinted at an announcement of a new game next week.

Waiting for These

Pi Network’s next big update appears to be the transition to protocol v25. The team initially set June 18 as the completion deadline but later clarified that it might need more time, indicating a likely delay.

Another highly anticipated event in the Pi Network community is Pi2Day, celebrated on June 28 (6/28) because it represents the mathematical constant 2π.

Speculation is mounting that the team may announce a major ecosystem update, launch new features, or even a listing on Binance. However, nothing is confirmed, and we’ll have to see whether the day will bring anything meaningful at all.

PI Price Outlook

Earlier this month, PI’s price crashed below $0.12, marking the lowest level in its history. Over the past few days, though, it has followed the broader crypto market’s resurgence and now trades at around $0.14, representing a 4% weekly increase.

The bulls are now hoping for a further rally, which will largely depend on whether Bitcoin (BTC) and the leading altcoins can sustain their positive momentum. Meanwhile, the reduced token unlocks and some other important factors also suggest that PI’s valuation may post additional gains in the near future.

The post Pi Network News and PI Price Update Today: June 15 appeared first on CryptoPotato.

Key Highlights

- Salesforce has entered into an agreement to purchase AI agent specialist Fin, previously known as Intercom, in a transaction valued at $3.6 billion

- The transaction is anticipated to finalize during Salesforce’s fiscal fourth quarter of 2027

- Shares of CRM increased 0.8% to reach $167.10 on Monday, potentially breaking a nine-day decline

- Fin operates its own AI technology platform, Apex, designed exclusively for customer service applications

- Salesforce’s Agentforce platform reported a 20% increase in annual recurring revenue, reaching $1.2 billion in the company’s fiscal first quarter of 2027

On Monday, Salesforce revealed its plans to purchase Fin, the artificial intelligence agent firm that was previously operating as Intercom, through a $3.6 billion acquisition agreement.

Shares of CRM traded higher by 0.8% to $167.10 during Monday’s session. This uptick would mark the end of a nine-day downward trend. However, the stock remains down 37% on a year-to-date basis.

This strategic acquisition arrives at a time when Salesforce is experiencing increased scrutiny from shareholders concerned that AI-powered coding solutions might enable clients to develop their own customized Agentforce alternatives, potentially diminishing demand for Salesforce’s offerings.

Fin’s flagship offering is an AI agent designed to manage customer inquiries from start to finish. The technology operates seamlessly across multiple communication channels including live chat, email, WhatsApp, text messaging, phone calls, and Slack.

The platform operates using Fin’s proprietary model known as Apex. According to Salesforce, Apex has been specifically engineered for customer support applications and delivers superior resolution rates compared to leading commercial models available today.

Marc Benioff, Chief Executive Officer, described the acquisition as an ideal match. “Fin delivers battle-tested agent technology, a strong dedication to customer satisfaction, and an exceptional AI team that will enhance Agentforce with robust service agent functionalities,” Benioff stated.

Eoghan McCabe, CEO and co-founder of Fin, emphasized that the partnership provides scale his organization couldn’t achieve independently. “Through this combination with Salesforce, we can implement it extensively at a pace we never could have reached working alone,” McCabe explained.

Understanding Agentforce’s Current Performance

Agentforce demonstrated a 20% growth in annual recurring revenue, achieving $1.2 billion during fiscal Q1 2027. The addition of Fin is projected to broaden this platform’s capabilities within customer service environments.

The transaction is scheduled to conclude during Salesforce’s fiscal fourth quarter of 2027, pending specific price adjustment provisions.

Analyst Community Expresses Mixed Views

Rishi Jaluria, an analyst at RBC Capital Markets, acknowledged the strategic merit of the acquisition, particularly for customer engagement purposes. However, he raised several reservations.

“We remain uncertain about certain aspects of the acquisition rationale and recognize that this introduces further integration and execution challenges considering that Informatica, Contentful, and various smaller acquisitions are being incorporated simultaneously,” Jaluria noted on Monday.

Barron’s withdrew its recommendation for Salesforce last week, reversing its original buy rating from December.

The software industry overall has faced headwinds this year from what market observers have dubbed the “SaaSpocalypse” — apprehension that AI agents might diminish reliance on conventional SaaS products.

Heading into this week, Salesforce shares have declined 37% year-to-date.

Standard Chartered is forecasting a major acceleration in how decentralized finance (DeFi) can absorb tokenized assets. In a research note released Monday, Geoff Kendrick—head of digital assets research at the bank—projected that assets actively used in DeFi could expand 37-fold to $2.7 trillion by the end of 2030.

The estimate hinges on a shift in where tokenized value goes once it is issued. Kendrick argued that DeFi protocols could become a key distribution channel not only for crypto-native assets, but also for tokenized real-world assets (RWAs) that are increasingly being developed by traditional finance participants.

Key takeaways

- Standard Chartered expects DeFi-active tokenized assets to reach $2.7 trillion by 2030, implying a 37x increase from current levels.

- The forecast depends on both tokenized RWAs and crypto-native assets finding their way into onchain lending, trading, and other DeFi use cases.

- According to Kendrick, only 3% of stablecoins and 10% of tokenized RWAs are currently used in DeFi.

- Standard Chartered projects tokenized asset usage in DeFi rising to about 30% by end-2030, from roughly 3.5% today.

- The bank points to Uniswap as a possible hub for tokenized markets, though other researchers warn tokenization alone doesn’t solve liquidity fragmentation.

Standard Chartered’s 2030 DeFi absorption forecast

Kendrick’s central claim is that DeFi could be the next major engine for “generational wealth” in digital assets. He estimated that the amount of tokenized assets active in DeFi will grow 37x by the end of the decade.

While tokenization is often discussed as a way to bring real-world finance onto public blockchains, the investment question is how that tokenized value translates into real onchain participation. Kendrick’s projections address that by focusing on usage rates—how much of the overall tokenized supply is actually deployed inside DeFi protocols.

Per the research note, only 3% of stablecoins and 10% of tokenized RWAs are currently used in DeFi. Standard Chartered expects those tokenized shares to rise sharply over the next several years, with the portion of tokenized value used in DeFi projected to reach 30% by end-2030, up from about 3.5% today.

The scale of the jump is important: growing the absolute figure to $2.7 trillion would require both (1) rapid growth in total onchain tokenized assets and (2) a near ninefold increase in the share of that tokenized value being put to work in DeFi.

Why tokenized value may not automatically become liquid

The bank’s outlook reinforces the broader institutional argument that tokenization could re-route capital flows toward onchain systems. However, the path from issuance to deep markets is not straightforward.

The research note acknowledges—and the wider debate around tokenization highlights—that tokenization does not inherently guarantee liquidity or a unified market structure. Other researchers have warned that tokenized assets can still trade in ways that remain fragmented across ecosystems.

Earlier coverage from Cointelegraph noted concerns raised by Axis CEO Chris Kim that issuing the same asset across multiple blockchains and formats can create “siloed liquidity,” leading to pricing gaps and higher costs. In practical terms for traders and liquidity providers, that fragmentation can make it harder for market participants to find consistent pricing and for liquidity to pool efficiently—even if total market value grows.

Similarly, Oya Celiktemur of Ondo Finance told Cointelegraph at Paris Blockchain Week in April that tokenizing an illiquid asset does not “magically” make it liquid. The implication is that deeper liquidity depends on market design, distribution, and the incentives that keep trading and settlement efficient once tokenized assets reach users.

From earlier RWA estimates to a DeFi-centered distribution thesis

Standard Chartered has previously linked tokenization growth to large market expansions. The new DeFi-focused forecast builds on an earlier projection that non-stablecoin tokenized RWAs could grow to $2 trillion by the end of 2028, according to Kendrick—where tokenized money-market funds and US equities are expected to represent much of the projected market.

What’s new here is the emphasis on where those tokenized instruments are used rather than just their total outstanding value. The shift matters because DeFi impact is not measured only by token counts or issuance volumes; it’s measured by how much liquidity and trading activity migrates into onchain protocols that support borrowing, trading, and settlement.

By framing DeFi as a destination for tokenized capital, Standard Chartered is effectively proposing that tokenization’s biggest long-term value creation could be tied to protocol-level adoption—rather than confined to isolated token issuances or simple exposure products.

Uniswap as a potential liquidity bridge for tokenized markets

Alongside the usage-rate assumptions, Kendrick singled out Uniswap as a venue that could play a growing role in trading tokenized assets as more of them move onchain. He pointed to the decentralized exchange’s scale, branding, and track record of operating through multiple crypto cycles.

In his view, these characteristics could be especially relevant for traditional financial institutions that are likely to prioritize security and reliability when integrating tokenized RWAs into DeFi. Kendrick also suggested that if Uniswap is able to “commercialise enough” and form meaningful TradFi partnerships that improve scale, it could strengthen its fee-generation relative to its market capitalization—potentially narrowing the gap with major centralized exchanges.

The bank’s bet on Uniswap aligns with the thesis that tokenized-market liquidity will depend on venues capable of onboarding new assets at meaningful volume. Still, it sits in tension with the liquidity-fragmentation warnings raised by other researchers: even if a venue is technically capable of supporting tokenized assets, liquidity can remain dispersed if the same instruments arrive in multiple formats, across multiple chains, or with mismatched trading infrastructure.

Looking ahead, investors and builders should watch whether DeFi protocols can convert rising tokenization volumes into sustained onchain usage—particularly by tracking how stablecoins and tokenized RWAs distribute across different DeFi activities. The key uncertainty is whether liquidity consolidates around major venues like Uniswap or continues to fragment as tokenized assets proliferate across ecosystems.

Strategy, the publicly listed company controlled by Michael Saylor, added more Bitcoin to its treasury last week, purchasing 1,587 BTC for $100 million while the token traded below the firm’s reported average cost basis.

According to Strategy’s filing with the US Securities and Exchange Commission, the acquisitions took place between June 8 and Sunday. The company reported an average purchase price of $63,024 per bitcoin, slightly lowering its overall average cost basis to about $75,656.

Key takeaways

- Strategy bought 1,587 BTC for $100 million between June 8 and Sunday, per an SEC 8-K filing.

- The purchases were executed at an average price of $63,024 per BTC, reducing Strategy’s average cost basis to roughly $75,656.

- Strategy now holds 846,842 BTC, with CoinGecko valuing the holdings at about $56.1 billion at roughly $66,216 per BTC.

- The latest buy was financed through sales of Strategy’s Class A common stock, while its preferred share programs showed no activity during the week.

- Ongoing discussion around Strategy’s willingness to sell Bitcoin remains tied to its need to fund dividend-style digital credit products.

Another tranche of Bitcoin purchases

Strategy’s newest move reinforces its continued accumulation strategy, even as market prices sit under its average entry cost. The company’s SEC 8-K states that it acquired 1,587 BTC for $100 million during the period spanning June 8 through Sunday.

At an average acquisition price of $63,024, the buy occurred at a level materially below Strategy’s average cost basis of approximately $75,700 referenced in the filing details. After this round, Strategy’s overall average cost basis fell slightly to $75,656.

Where the company’s Bitcoin stands today

With the latest acquisition, Strategy’s total Bitcoin holdings reach 846,842 BTC, accumulated at a combined cost of $64.07 billion. Based on CoinGecko market pricing of about $66,216 per BTC, the current value of those holdings is roughly $56.1 billion.

That gap between carrying cost and current market value matters for both equity investors and crypto-focused observers, because Strategy’s balance sheet is built around Bitcoin exposure. When BTC trades below the company’s average cost basis, each incremental purchase can help reduce that average—though it does not automatically offset the unrealized difference in value unless the market moves meaningfully higher.

Financing the buy through MSTR share sales

Strategy’s filing indicates that the purchase was funded similarly to its prior additions: by selling shares of its Class A common stock rather than relying on activity within certain preferred stock programs.

Specifically, the company said it raised about $209 million by selling 1.73 million shares during the period. It also noted that preferred share programs—including STRC, STRF, STRK, and STRD—showed no activity over the week covered by the filing.

This structure is a key element of Strategy’s approach. Rather than treating Bitcoin accumulation as an isolated treasury action, the company ties growth in BTC holdings to capital markets operations that can provide liquidity for continued buying.

Preferred stock below par and the broader sale debate

While Strategy did not report preferred program activity during the week, outside trackers have continued to highlight market pricing pressure around at least one preferred instrument. According to STRC.live, STRC remained below its $100 par value for a fourth consecutive week as of June 12, lingering in the mid-$96 range and marking the longest stretch below par since its launch.

On Friday, STRC closed at $94.80, down about 1%, according to TradingView data cited via STRC.live.

Separately, the context for why Strategy continues to sell assets to fund Bitcoin buying—and, at times, sell BTC itself—has remained a live issue in the crypto community. The company disclosed its first reported Bitcoin sale in years in connection with an earlier transaction referenced in Cointelegraph coverage: a sale of 32 BTC on June 1. Even though that amount was small relative to its overall holdings, it sparked debate about whether Strategy is shifting away from its historically strict “buy and hold” narrative.

Michael Saylor later defended the rationale, telling Cointelegraph that Bitcoin treasury companies need the ability to sell holdings to support dividend-paying securities tied to its digital credit business.

What to watch next

Investors will likely focus on whether Strategy continues to fund Bitcoin buys primarily through common stock issuance, how preferred programs trade relative to par, and—most importantly—whether future SEC disclosures show continued accumulation at prices that further narrow the company’s cost basis versus BTC’s prevailing market level.

Paradigm has led a $9 million Series A funding round for Latin American payments platform El Dorado as the company expands stablecoin-powered cross-border transfers across underserved markets in the region.

Summary

- Paradigm led a $9 million Series A round for Latin American payments app El Dorado, with Coinbase Ventures and Verda Ventures also participating.

- El Dorado said it serves more than 100,000 active users, has processed over 5 million transactions, and operates across 12 countries in Latin America.

- The company has expanded into business payments on the Tempo blockchain, onboarding more than 100 corporate clients and supporting cross-border trade flows, including electric vehicle imports from China.

According to a June 15 announcement from Paradigm, the investment was made alongside Coinbase Ventures and Verda Ventures, with the firms backing El Dorado’s effort to build payment infrastructure for cross-border transactions in Latin America.

Ricardo de Arruda, partner for investing and research at Paradigm, said the region handles more than $100 billion in annual cross-border payment volume but continues to rely on systems that are slow, expensive, and difficult to navigate.

“Cross-border payments in Latin America represent one of the most underserved and underreported opportunities in global finance,” de Arruda said.

“The region moves well over $100 billion across borders annually, but is plagued by slow, expensive and opaque infrastructure. El Dorado is building the payments layer this market has long needed.”

Founded in 2022 by Latin American immigrants, El Dorado said it now serves more than 100,000 active users and has processed over 5 million transactions across the region. The company currently operates in 12 countries, including Argentina, Bolivia, Brazil, Colombia, Costa Rica, the Dominican Republic, and Ecuador.

El Dorado targets overlooked payment corridors

Offering a different view of the market opportunity, El Dorado co-founder and CEO Guillermo Goncalvez said in an accompanying statement that the annual cross-border payment activity in Latin America is closer to $1 trillion when broader flows are considered.

According to Goncalvez, roughly 60% of those transactions involve business-to-business payments tied to imports and exports between the U.S. and Latin America. Beyond those well-known routes, he said some of the strongest demand comes from payment corridors that large financial technology firms often overlook.

One of El Dorado’s busiest routes today connects Brazil and Bolivia, a market Goncalvez said remains underserved despite strong commercial activity. He added that countries such as Bolivia, Paraguay, Ecuador, and Peru receive less attention from larger fintech providers including Nubank and Wise.

Alongside consumer payments, El Dorado has introduced a dedicated business platform for companies moving money across borders. According to the company, the service combines fiat and stablecoin payment rails within a single application while supporting multi-signature and multi-organization account structures.

Goncalvez added that more than 100 business customers have joined the platform, with imports of electric vehicles from China emerging as one of the most common use cases.

Built on Tempo, a Layer 1 blockchain developed through a partnership between Paradigm and Stripe, the service forms part of a payment infrastructure strategy both organizations have been developing this year. Josh Itzkovitz, GTM at Tempo, said the network allows businesses worldwide to open accounts regardless of whether they maintain a U.S. legal entity.

The investment also adds to Paradigm’s growing activity outside traditional crypto venture funding. In recent months, the firm has backed manufacturing company SendCutSend in a $110 million funding round, partnered with Stripe on the Tempo blockchain network, and participated in policy discussions surrounding stablecoin regulation in the U.S.

Earlier this month, Paradigm submitted comments to the Federal Deposit Insurance Corporation urging regulators not to restrict third-party stablecoin reward programs, arguing that such limitations extend beyond what Congress approved under the GENIUS Act. Those efforts, together with the launch of Tempo and the El Dorado investment, place stablecoin-based payment infrastructure at the center of several of the firm’s recent initiatives.

Plans to replace empty hotel with four-storey apartment block

If America wants to lead in crypto, it must protect the people who build it

Here’s What Pineapples Are Really Made From

-

Business1 day ago

Business1 day agoNo Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

-

Crypto World4 days ago

Crypto World4 days agoOppenheimer backs SpaceX as $70 billion retail frenzy builds

-

Crypto World4 days ago

Crypto World4 days agoMarkets Rally as SpaceX IPO Looms Amid Iran Tensions and Inflation Surge

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Tuckernuck – Corporette.com

-

Sports7 days ago

Sports7 days agoFIFA WC 2026 Group C: Morocco, Scotland challenge Brazil’s hunt for glory | FIFA World Cup 2022

-

Crypto World16 hours ago

Crypto World16 hours agoZimbabwe Requires Crypto Businesses to Register Annually Under New FIU Regulations

-

Entertainment6 days ago

Entertainment6 days agoThe Ryan Gosling True Crime Thriller On Netflix That Gets Even Stranger, Stream It Now

-

Sports6 days ago

Sports6 days agoBangladesh beat Australia after 20 years in ODIs, register only their second win over six-time world champions | Cricket News

-

Tech3 days ago

Tech3 days agoNanoClaw integrates JFrog registries to secure AI agent downloads

-

Tech3 days ago

Tech3 days agoThis Week In Security: Microsoft On Microsoft, Register Your Domains, Linux On ARM, And FreeBSD Joins The File Cache Club

-

Crypto World2 days ago

Crypto World2 days agoBitget enters Argentina’s regulated crypto market through PSAV registration

-

Politics4 days ago

Politics4 days agoPolitics Home | Healey Resignation Is “Colossal Failure Of Government”, Says Former Labour Defence Secretary

-

Tech4 days ago

Tech4 days agoDutton Ranch star claims they ‘didn’t see any disruption’ on set following Chad Feehan’s exit from Yellowstone spinoff fueled by Taylor Sheridan clash rumors

-

Tech5 days ago

Tech5 days ago‘This is Seattle’s position on AI’: City Council votes unanimously to pause big new data centers

-

NewsBeat4 days ago

NewsBeat4 days agoEl Nino has formed in the Pacific and could set records, forecasters say

-

Entertainment4 days ago

Entertainment4 days agoDonnie Wahlberg & More Heat Up Las Vegas at Circa’s Barry’s Downtown Prime

-

Sports4 days ago

Sports4 days agoFirst Time Since 1971: Australia Register Historic Low In ODI Cricket

-

Tech4 days ago

Tech4 days agoOpendoor Ends India Operations, Fueling a Bigger Conversation About AI and Outsourcing

-

Politics4 days ago

Politics4 days agoBelfast burns, while Met chief points finger at Iran and Russia

-

Business5 days ago

Business5 days agoThailand Ranks Second Worldwide for AI Adoption Growth, Microsoft Reports

You must be logged in to post a comment Login