Crypto World

What is Ripple Prime? Inside Ripple’s Prime broker

Ripple spent $1.25 billion to buy a prime broker that clears trillions of dollars a year, then wired it into the XRP Ledger and RLUSD. Here is what a prime broker actually does, what Ripple Prime offers, and whether any of it reaches XRP.

Summary

- Ripple Prime is Ripple’s institutional prime brokerage arm, built from its $1.25 billion acquisition of Hidden Road, offering clearing, financing, and trading across digital assets, foreign exchange, derivatives, swaps, and fixed income.

- A prime broker is the plumbing behind professional trading: it gives hedge funds and trading firms one account for execution, clearing, settlement, financing, and custody, with cross-margining that improves capital efficiency.

- The acquisition made Ripple the first crypto company to own and operate a global, multi-asset prime broker, and the business has grown roughly threefold since the deal was announced.

- Ripple has wired its own products into the platform: RLUSD is used as collateral, some derivatives clients hold balances in it, and Ripple plans to move post-trade activity onto the XRP Ledger.

- For XRP the token, the benefit is indirect and unproven, because Ripple Prime is institutional infrastructure, not a retail venue, and the token has not tracked the platform’s growth.

Ripple Prime is Ripple’s institutional prime brokerage platform, a one-stop service that lets large trading firms clear, finance, and trade across both traditional and digital assets through a single account. It exists because in 2025 Ripple paid $1.25 billion to acquire Hidden Road, one of the largest non-bank prime brokers in the world, and rebranded it. That deal turned Ripple from a payments and stablecoin company into an operator of the kind of core market infrastructure that hedge funds and banks have relied on for decades. This explainer covers what a prime broker is, how Ripple Prime works, how Ripple has connected it to RLUSD and the XRP Ledger, and the honest answer to the question every XRP holder asks: does it help the token?

First, what is a prime broker?

Before Ripple Prime makes sense, the underlying concept has to. A prime broker is a firm that sits behind professional trading operations and bundles together the services those operations need to function. In traditional finance, a hedge fund does not open a separate relationship with every exchange, lender, and custodian it uses. Instead it routes much of that activity through a prime broker, which provides trade execution and access to markets, clearing and settlement of those trades, financing and securities lending so the fund can use leverage, and custody of the assets. The prime broker becomes the single hub through which capital and positions flow.

The reason this matters is capital efficiency. A prime broker can look at all of a client’s positions together and net them, so the client posts collateral against the combined risk of the book instead of against each trade in isolation. This is called cross-margining, and it frees up capital that would otherwise sit idle backing individual positions. A fund running many strategies at once can therefore do more with the same balance sheet. Prime brokers also extend credit, letting clients borrow to amplify positions, and manage the risk of that credit in real time.

In short, prime brokers are the professional-grade infrastructure that makes large-scale, multi-strategy trading possible. They bring credibility, credit, and operational scale, the things institutions expect from legacy finance. For years, crypto largely lacked a prime broker of this caliber, which was one reason big institutions hesitated to trade digital assets at scale. Filling that gap is exactly what Ripple set out to do.

From Hidden Road to Ripple Prime: the $1.25 billion deal

Ripple did not build a prime broker from scratch. It bought one. In April 2025, at Paris Blockchain Week, Ripple announced an agreement to acquire Hidden Road for $1.25 billion, one of the largest deals the digital-asset industry had seen. Hidden Road was a fast-growing non-bank prime broker that cleared roughly $3 trillion a year across markets and served more than 300 institutional clients, including hedge funds, proprietary trading firms, and major liquidity providers. Ripple had been an investor in Hidden Road and a customer of its platform, so it knew the business from the inside before buying it.

The acquisition closed in October 2025, and Hidden Road was immediately rebranded as Ripple Prime. The move made Ripple the first crypto company to own and operate a global, multi-asset prime broker, giving it a financing and clearing engine of a type that had previously belonged only to traditional financial firms. Ripple committed to inject significant capital into the business to expand its capacity, and by its own account the platform grew roughly threefold in activity between the announcement and the close. Hidden Road founder Marc Asch stayed on to work alongside Ripple leadership through the integration.

The strategic logic was that core infrastructure is what unlocks the next phase of institutional crypto adoption. Payments and custody move value and store it, but a prime broker is where institutions actually trade and finance positions at scale. By owning one, Ripple positioned itself to sit at the center of institutional digital-asset activity instead of at the edges, and to bring its own assets, XRP and the RLUSD stablecoin, into that flow.

What Ripple Prime actually does

Ripple Prime offers the full prime-brokerage stack across an unusually broad range of markets. Its services span clearing, prime brokerage, and financing across foreign exchange, digital assets, precious metals, exchange-traded derivatives, over-the-counter swaps, and fixed income repo. Clients can access markets through over-the-counter desks, sponsored access, and direct market access, with real-time risk management, cross-margining across their positions, and risk-based margin financing. That breadth is the point: an institution can manage exposures across traditional and digital assets from one platform instead of stitching together many providers.

In November 2025, shortly after the deal closed, Ripple launched digital-asset spot prime brokerage for the United States market under the Ripple Prime brand. This let US-based institutional clients execute over-the-counter spot transactions across dozens of major digital assets, including XRP and RLUSD, and cross-margin those spot positions alongside swaps and exchange-listed futures and options. It combined Ripple’s regulatory licenses with Hidden Road’s prime-brokerage infrastructure into a single US offering, complementing the derivatives services the platform already ran.

The platform has kept adding connectivity. Ripple Prime enabled support for Hyperliquid, a high-performance decentralized derivatives protocol, letting institutional clients reach on-chain derivatives liquidity while cross-margining their decentralized-finance exposure against all other asset classes on the platform. That combination, a regulated institutional prime broker reaching directly into on-chain markets, is a concrete example of the bridge between traditional finance and decentralized finance that Ripple describes as its goal.

RLUSD as collateral: the cross-margining hook

One of the most important features of Ripple Prime is how it uses RLUSD, Ripple’s dollar-backed stablecoin. RLUSD is being used as collateral across a range of prime-brokerage products, and Ripple has positioned it as the first stablecoin to enable efficient cross-margining between digital assets and traditional markets. In practice, an institution can post RLUSD as margin and have it recognized across both its crypto and its traditional exposures, which is exactly the kind of capital efficiency prime brokers exist to provide.

Adoption of this feature has been concrete instead of theoretical. Some derivatives customers have chosen to hold their balances in RLUSD, and Ripple expects that to grow. RLUSD has been approved as margin collateral on the OKX exchange across more than 280 trading pairs, and Ripple Prime clients can trade Bitcoin options on the Bullish exchange using RLUSD as collateral. To support the stablecoin’s institutional credibility, Bank of New York Mellon serves as the primary reserve custodian of RLUSD, a signal aimed squarely at the compliance expectations of large institutions.

The reason this matters is that it gives RLUSD a real institutional job to do. Many stablecoins circulate mostly among crypto traders; RLUSD, through Ripple Prime, is being embedded into the margin and settlement plumbing that professional firms use. That is a more durable form of demand than speculative trading, because it ties the stablecoin to the operational needs of institutions rather than to market sentiment. It is also the clearest way that Ripple Prime strengthens one of Ripple’s own products, as distinct from the broader industry.

The XRP Ledger connection

Ripple has also linked Ripple Prime to the XRP Ledger, the blockchain whose native asset is XRP. The plan Ripple has described is to migrate parts of Hidden Road’s post-trade activity, the clearing and settlement that happens after a trade is agreed, onto the XRP Ledger. The goal is to streamline settlement and lower operational costs, while showcasing the ledger as institutional-grade infrastructure for decentralized finance. If that migration proceeds at scale, real institutional settlement volume would run across the XRP Ledger.

That connection took a further step through traditional clearing infrastructure. Ripple Prime, still listed under the Hidden Road name in the relevant notice, was integrated into the participant directory of the Depository Trust and Clearing Corporation’s National Securities Clearing Corporation, the backbone of US securities clearing. Ripple’s chief technology officer at the time flagged the development as significant, because it connects a crypto-owned prime broker to the same clearing rails that settle Wall Street’s equity trades. Ripple Prime also received an investment-grade rating from Kroll in April 2026, a distinction Ripple says no other crypto-affiliated prime broker holds, which opens the door to conservative institutions such as pension funds, banks, and insurers.

Taken together, these moves position the XRP Ledger and RLUSD as pieces of institutional market infrastructure instead of purely retail crypto assets. The migration of post-trade activity, the DTCC connection, and the investment-grade rating are all steps toward embedding Ripple’s technology into the machinery of regulated finance. Whether that machinery ends up generating meaningful demand for XRP the token is a separate question, and an important one.

Why Ripple Prime matters for crypto

Zooming out, Ripple Prime matters because it imports a missing layer of financial infrastructure into digital assets. Crypto has never lacked exchanges or wallets, but it has lacked a large, credible, multi-asset prime broker of the kind institutions take for granted in traditional markets. By acquiring one that already cleared trillions of dollars a year and serving 300-plus institutional clients, Ripple gave the industry a bridge between the way hedge funds and banks already operate and the way digital assets trade and settle.

For Ripple itself, the deal marked a transformation. The company had been known primarily for cross-border payments and, more recently, for its RLUSD stablecoin and custody services. Ripple Prime added institutional trading and financing to that stack, so Ripple now spans payments, custody, a stablecoin, and a prime broker. That makes it one of the more vertically integrated firms in crypto, able to offer institutions a connected suite instead of a single product. It also gives Ripple multiple ways to weave XRP and RLUSD into institutional workflows.

The broader significance is about legitimacy. Institutional adoption of digital assets has been held back partly by the absence of familiar, trusted infrastructure. A prime broker with an investment-grade rating, a connection to DTCC clearing, and bank-grade custody speaks the language institutions understand. If Ripple Prime succeeds, it lowers a real barrier to large-scale institutional participation in crypto, which is a meaningful development regardless of what happens to any single token’s price.

Does Ripple Prime actually help XRP?

Here is the question that matters most to XRP holders, and it deserves a straight answer instead of a hopeful one. The connection between Ripple Prime and XRP is infrastructure-driven, not retail-facing. Ripple Prime is a service for institutions; it does not change how ordinary users buy or trade XRP, which still happens on exchanges. The potential benefit to XRP is indirect: if institutional settlement volume grows on the XRP Ledger through Ripple Prime, that could raise network usage, and XRP, as the ledger’s native asset used for transaction fees and liquidity, might see more demand over time.

The trouble is that this benefit has not shown up in the token’s price. Over the year following the acquisition, Ripple Prime delivered on its roadmap, earning an investment-grade rating, launching US spot prime brokerage, and integrating RLUSD as collateral, while XRP fell rather than rose. The token dropped sharply even as the platform executed, which underlines a recurring pattern with Ripple news: the company’s commercial progress and the token’s price are only loosely connected. Much of the value Ripple Prime creates accrues to Ripple the company, to RLUSD, and to the institutions using the platform, not automatically to XRP.

That does not mean Ripple Prime is irrelevant to XRP. The post-trade migration to the XRP Ledger, if it reaches scale, is a genuine potential channel of demand, and a maturing institutional ecosystem around the ledger could matter over a long horizon. But the honest framing is that Ripple Prime is a strong development for Ripple and its institutional ambitions, an indirect and unproven one for XRP, and no substitute for the broad demand that actually moves the token. As with most Ripple news, the wise approach is to separate the company’s execution from the token’s price and to watch for real ledger usage rather than announcements.

The risks and open questions for Ripple Prime

For all its promise, Ripple Prime is not a finished story, and a balanced view has to weigh what could go wrong or fail to materialize. The first question is integration. Merging a large prime broker into a crypto company is complex, and the value of the deal depends on combining Hidden Road’s infrastructure and client relationships with Ripple’s licenses, custody, and stablecoin without friction. Integrations of this size take time, and the benefits Ripple describes assume the two businesses knit together smoothly.

Prime brokerage itself carries inherent risks that Ripple now owns. A prime broker extends credit and holds client assets, which means it takes on counterparty and credit risk: if a large client fails or a market move is violent enough, the broker can be exposed. Managing that risk in real time is the core discipline of the business, and it is why prime brokers live or die on their risk engines and capital buffers. The business is also cyclical, tied to trading volumes and market conditions that rise and fall, so revenue is not guaranteed to grow in a straight line.

Competition is intensifying as well. Other crypto-native firms and incumbent traditional players are building or expanding their own institutional prime services, so Ripple Prime has to win and keep clients in a crowded field. Its differentiators, an investment-grade rating, a connection to traditional clearing, and the integration of RLUSD, are meaningful, but competitors will not stand still, and institutions can multi-home across several prime brokers.

The largest open question for XRP holders specifically is execution on the XRP Ledger. Ripple has said it plans to migrate post-trade activity onto the ledger, but plans and delivery are different things. The scale, timing, and real economic impact of that migration remain to be seen, and much of the token-level thesis rests on it actually happening at volume. Until the ledger is carrying meaningful institutional settlement, the connection between Ripple Prime’s growth and XRP demand stays more potential than proven. None of this makes Ripple Prime a weak business; it makes it a young one whose full impact, on Ripple and on XRP, will be judged over years, not announcements.

Frequently Asked Questions

What is Ripple Prime in simple terms?

Ripple Prime is Ripple’s institutional prime brokerage platform. It gives large trading firms and institutions a single service for clearing, financing, and trading across digital assets, foreign exchange, derivatives, swaps, and fixed income. It was created when Ripple acquired the prime broker Hidden Road for $1.25 billion in 2025 and rebranded it. It is built for professional institutions, not retail traders.

What is a prime broker?

A prime broker is a firm that bundles the services professional traders need into one relationship: trade execution and market access, clearing and settlement, financing and lending for leverage, and custody. Its key advantage is cross-margining, which lets a client post collateral against the combined risk of all their positions instead of each trade separately, freeing up capital and improving efficiency.

How much did Ripple pay for Hidden Road?

Ripple agreed to acquire Hidden Road for $1.25 billion, announced in April 2025 and closed in October 2025. Hidden Road was a non-bank prime broker that cleared roughly $3 trillion a year across markets and served more than 300 institutional clients. After closing, Ripple rebranded it as Ripple Prime, becoming the first crypto company to own and operate a global, multi-asset prime broker.

How does Ripple Prime use RLUSD?

RLUSD, Ripple’s dollar-backed stablecoin, is used as collateral across Ripple Prime’s products, positioned as the first stablecoin to enable cross-margining between digital assets and traditional markets. Some derivatives clients hold balances in RLUSD, it is approved as margin collateral on OKX across 280-plus pairs, and Ripple Prime clients can trade Bitcoin options on Bullish using RLUSD. Bank of New York Mellon is its primary reserve custodian.

Does Ripple Prime run on the XRP Ledger?

Not entirely, but Ripple plans to migrate parts of the platform’s post-trade activity, its clearing and settlement, onto the XRP Ledger to lower costs and showcase the ledger for institutional use. Ripple Prime has also been integrated into the DTCC’s securities clearing directory and received an investment-grade rating from Kroll, steps that position the ledger and RLUSD within regulated financial infrastructure.

Is Ripple Prime good for the XRP price?

The benefit to XRP is indirect and, so far, unproven. Ripple Prime is institutional infrastructure, not a retail venue, so it does not change how people trade XRP. If settlement volume grows on the XRP Ledger through the platform, XRP demand could rise over time. But XRP fell during the year Ripple Prime executed its roadmap, showing how loosely Ripple’s progress and the token’s price are connected.

How is Ripple Prime different from a crypto exchange?

An exchange is a venue where users, including retail traders, buy and sell assets directly. A prime broker sits behind professional institutions, providing credit, clearing, settlement, custody, and cross-margining across many venues and asset classes. Ripple Prime serves hedge funds, trading firms, and other institutions with portfolio-level financing and risk management, not everyday retail trading. The two operate at different layers of the market.

Why does Ripple Prime matter for crypto?

It imports a missing layer of financial infrastructure into digital assets. Institutions rely on prime brokers in traditional markets, and crypto had lacked a large, credible one. By acquiring Hidden Road, Ripple gave the industry an investment-grade prime broker connected to traditional clearing rails and bank-grade custody, lowering a real barrier to institutional participation and transforming Ripple into a firm spanning payments, custody, a stablecoin, and prime brokerage.

Disclaimer: This article is for information and educational purposes only and does not constitute financial, investment, or trading advice. Details of Ripple Prime’s services and integrations may change over time. Nothing here is a recommendation to buy or sell any asset. Always do your own research and consult a qualified professional before making financial decisions. Information is accurate as of July 2, 2026, and may change.

While Strategy’s preferred STRC shares ended July well below their $100 par value, investors were told that their August dividend will not increase, holding at 12%.

Executive chairman Michael Saylor delivered the news in a tweet on Saturday, continuing to pitch STRC as a way to “stretch your income.” August will be the second month that the dividend will be paid semi-monthly after shareholders approved that change in June.

STRC shares closed at $89.46 on Friday, clocking a 5.42% price increase for the month which began with a dividend hike — 50 basis points to 12% — after a poor stock performance in June. The volume on the Nasdaq-traded shares on Friday were about two-thirds of their daily average.

STRC shares continued to trade significantly below their $100 par value in July.

Source: TradingView

On Friday, Strategy CEO Phong Le reiterated that management’s “corporate objective is for STRC to trade at $99-$100 over time,” without elaborating when investors might expect that to transpire.

Related: Bitcoin ETFs end July in the green despite late-month selling

Building cash reserve to make preferred payouts

Saylor, however, did take to social media on Sunday to dangle the possibility that the company will be making an announcement of a change in its Bitcoin treasury holdings. “Bitcoin Drive engaged,” read his X post, following a familiar pattern of posting a chart of Strategy’s BTC buys from Saylortracker.com to start off the week.

Last week, Strategy reported an $8.22 billion second-quarter net loss, driven primarily by an $8.32 billion unrealized loss on its Bitcoin (BTC) holdings as the cryptocurrency’s price declined during the quarter.

The Bitcoin treasury company said it has built a $3.75 billion cash reserve to support preferred stock payouts following the launch of its BTC monetization program.

Strategy also said it has built a $3.75 billion U.S. dollar reserve, enough to cover more than two years of preferred dividend payments and interest obligations. The company recently repurchased $25 million of its STRC preferred shares at a discount to par and said it intends to continue buying the securities while they trade below $100.

Magazine: Here’s why the CLARITY Act’s ethics deal may be so hard to reach

Minnesota’s prediction market ban remained blocked on Aug. 2, one day after the law was scheduled to take effect.

Summary

- July 27 injunction keeps Kalshi and Polymarket operating while Minnesota’s preemption case continues in court.

- Walz barred state employees from using confidential information to trade prediction markets for private benefit.

- Fairshake reported $126.97 million cash on hand through June, amplifying crypto’s broader election influence nationwide.

U.S. District Judge Katherine Menendez granted a preliminary injunction on July 27 to the Commodity Futures Trading Commission, Kalshi and Polymarket US. The order prevents Minnesota from enforcing its new statute against CFTC-registered designated contract markets while three related cases continue.

The Minnesota law would make it a felony for businesses to create, operate or intentionally support covered prediction markets. It also reaches certain data providers, payment services and advertisements. Menendez found that the plaintiffs were likely to succeed on at least part of their federal preemption claim because many event contracts may qualify as swaps under the Commodity Exchange Act.

Court win protects federal markets, but only for now

The ruling does not settle the dispute. Menendez found that the CFTC’s exclusive jurisdiction probably covers a “considerable swath” of contracts offered by Kalshi and Polymarket. However, she also said the platforms had not shown that every listed event contract meets the federal definition of a swap. Any permanent injunction could therefore protect fewer products than the current order.

Minnesota Attorney General Keith Ellison said prediction markets are “gambling, plain and simple.” That remains the state’s legal position, not a final court finding. Kalshi responded that “States cannot ban things that they don’t have jurisdiction over.” The company’s statement likewise reflects its interpretation of federal law rather than the case’s final outcome.

The injunction only covers the new prediction market statute as applied to CFTC-registered markets. It does not decide whether Minnesota can apply older gambling laws to individual sports or entertainment contracts. The Department of Public Safety has not said whether it views the platforms as illegal under those existing provisions or whether another enforcement action is underway.

As previously reported, the current relief will remain in place until the district court reaches a final decision unless a later order or appeal changes it. The court could ultimately distinguish between contracts with financial or economic consequences and products that more closely resemble ordinary wagers.

Walz shifts Minnesota’s focus to insider trading

Governor Tim Walz responded one day after the ruling with Executive Order 26-09. It prohibits covered state employees, including the governor, lieutenant governor and agency commissioners, from using nonpublic or confidential government information to trade prediction-market contracts for private benefit.

The order does not cover the legislature, courts, independent elected officials or several boards and commissions. Walz encouraged those institutions to adopt similar policies. It becomes effective 15 days after publication in the State Register and filing with the secretary of state.

A new federal enforcement case also shows that CFTC oversight does not leave manipulation entirely unpoliced. On July 31, the agency ordered former U.S. Representative George Santos to disgorge $17,569.98, pay a $17,500 penalty and accept a three-year trading ban over manipulative activity in a State of the Union event contract.

The CFTC order said Santos traded on whether he would attend the speech while making misleading public statements about his plans. The agency said those statements moved contract prices in a direction that favored his positions.

Meanwhile, as crypto.news reported, Kalshi has introduced employer disclosures, risk scoring and expanded surveillance for higher-risk contracts. The company said it blocked more than 100 potential insider trades and made 20 law-enforcement referrals during the first quarter of 2026. Those remain company-reported figures.

U.S. politics could pull crypto lawmakers and PACs into the fight

The Minnesota ruling could give pro-crypto lawmakers another example for arguing that national financial markets need one federal framework. The CLARITY Act does not regulate prediction markets directly. However, its supporters are also seeking a larger CFTC role in U.S. digital asset oversight. Senate lawmakers released updated market-structure text on July 22 after the Banking Committee advanced the measure in May.

The court dispute also creates a counterargument for lawmakers wary of expanding the commission’s mandate. A July 21 Senate letter asked the Government Accountability Office to review a reported 25% reduction in CFTC staffing and weaker enforcement activity. Critics could argue that Congress should not widen the regulator’s duties without ensuring it has enough staff to oversee both digital assets and fast-growing event markets. This is a political inference based on the agency’s expanding workload and the staffing concerns raised in Congress.

The case does not involve Fairshake or another crypto PAC. Still, it could shape campaign arguments surrounding candidates supported by the industry. FEC records showed that Fairshake held approximately $126.97 million in cash at the end of June and had spent $74.25 million during the current two-year reporting period.

In related coverage, Protect Progress spent more than $2 million in Michigan’s 13th District race, where challenger Donavan McKinney tied crypto lobbying to President Donald Trump’s business interests. Similar campaign attacks could connect support for broader CFTC authority with the Trump family’s prediction-market relationships.

Kalshi named Donald Trump Jr. a strategic adviser in January 2025. Polymarket later added him to its advisory board when his investment firm, 1789 Capital, took a stake in the company. Those corporate relationships are confirmed, although they do not prove that the White House directed the CFTC’s Minnesota litigation.

Sports-law attorney Daniel Wallach described the change in federal policy as “classic regulatory capture.” That is his assessment, not a judicial or regulatory conclusion. However, the family relationships may give opponents of pro-crypto candidates a clearer campaign message about industry access, federal authority and possible conflicts.

Conflicting state cases keep national rules unsettled

Minnesota is one part of a wider federal-state contest. The CFTC has filed cases against several states to defend what it calls exclusive jurisdiction over registered prediction markets. Yet courts have not produced one nationwide answer. Minnesota’s injunction favored the platforms, while rulings involving Wisconsin and Washington allowed state gambling challenges to advance.

New York added another case on July 31 by suing Kalshi and alleging that its platform operates as unlicensed gambling. The state seeks an injunction, restitution, penalties and forfeiture of alleged gains. Those claims remain allegations that Kalshi can contest in court.

The CFTC’s proposed prediction-market rule is another key track. The public comment period closed on July 27. The proposal would define “gaming,” establish factors for public-interest reviews and create a process lasting as long as 90 days for certain event contracts. The commission has not issued a final rule.

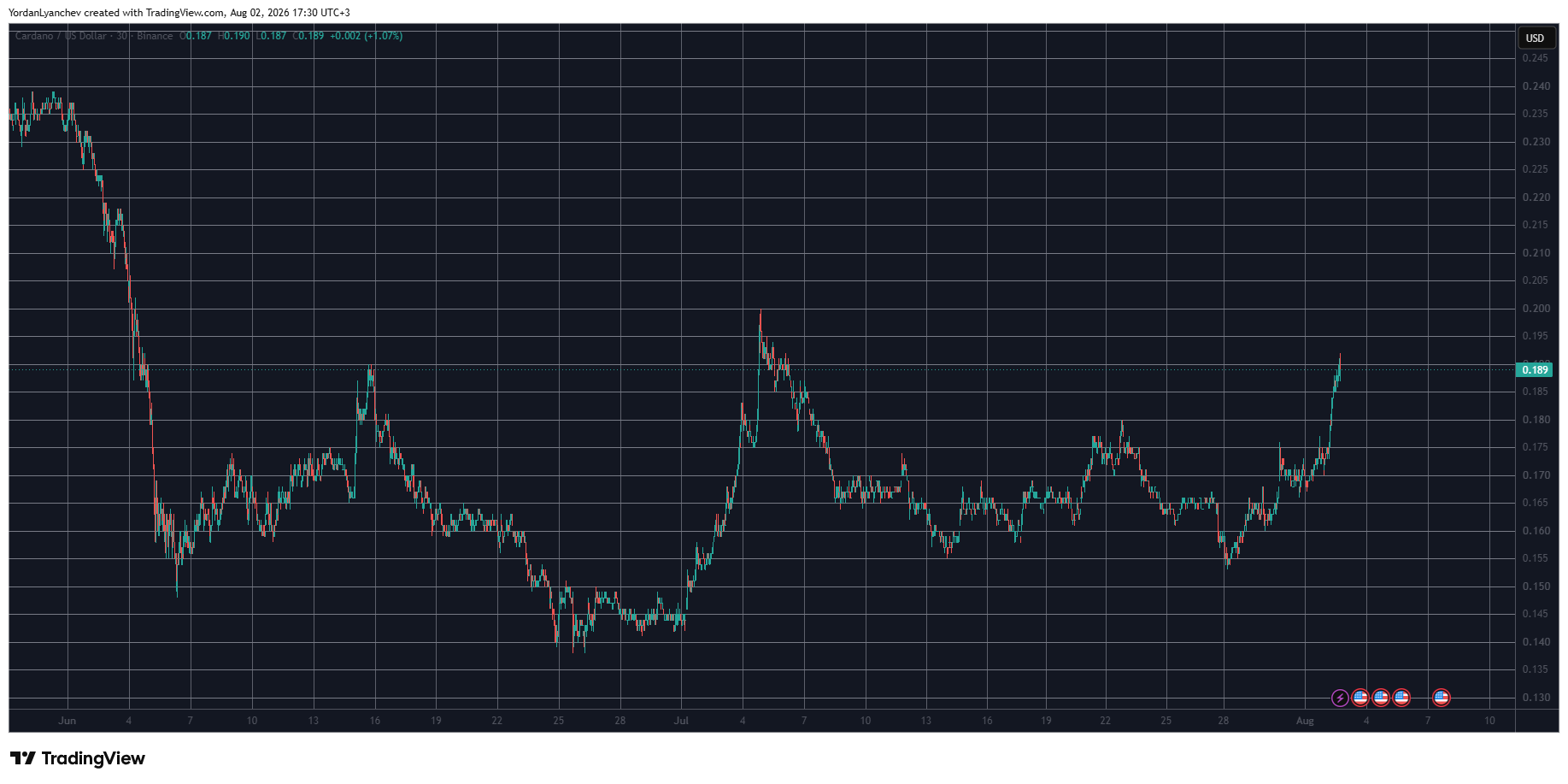

There’s rarely a big altcoin gainer during the current market conditions, in which every breakout attempt is halted in its tracks. This is particularly true for weekend moves, as the market tends to freeze on Saturday and Sunday.

The latest example came in the past 36-48 hours. Even though the situation in the Middle East continues to develop quickly, with Trump claiming a Hormuz Strait deal is in the making and Iran refuting his statement once again, BTC and most altcoins have remained sluggish.

However, Cardano’s ADA has emerged as the clear winner this weekend, gaining over 9% and jumping past $0.19 hours ago for the first time in almost a month. Here’s the most likely reason and what could follow next.

Whales Are Buying

Since we are excluding a rally from the broader market, perhaps the most obvious reason behind ADA’s impressive resurgence over the past day has been the recent behavior of whales. These large market participants, who can influence the underlying asset’s price moves with big purchases or sales, have gone on an accumulation spree.

Santiment Intelligence data shared by Ali Martinez shows that whales have scooped more than 240 million ADA in less than a week. Their total holdings went to 14.55 billion before retracing slightly.

The analyst concluded that this substantial acquisition has helped fuel the asset’s notable 22% surge in the past five days, while the rest of the market stagnates.

Whales loaded up. Cardano took off.

Over 240 million $ADA have been accumulated in the past five days, helping fuel a 22% price surge per data from @SantimentData. pic.twitter.com/6Q6P6luBZn

— Ali Charts (@alicharts) August 2, 2026

Major Breakout Knocking on the Door

Another analyst going under the X moniker, Gerla, noted that ADA is “knocking on the door of a major breakout.” Their chart shows that ADA is fighting for the $0.19-$0.20 resistance level now, which capped its previous breakout attempt last month.

However, the bullish RSI divergence and the completion of an inverse head-and-shoulders suggest that ADA finally has the strength to overcome that obstacle and aim at the next one, positioned at around $0.30.

ZAYK Charts was even more bullish, indicating that a successful surge past the first resistance level could pave the way for another leg up toward $0.50.

The post Why Is Cardano (ADA) Up 9% Today While the Crypto Market Stalls? appeared first on CryptoPotato.

After several failed attempts to extend its recovery, Ethereum is beginning to show signs of exhaustion beneath the major100-day MA. The latest rejection from this zone has weakened short-term momentum and increases the probability of a broader pullback if key support levels fail to hold.

Ethereum Price Analysis: The Daily Chart

On the daily timeframe, ETH’s outlook is gradually shifting toward a bearish bias after multiple failed attempts to reclaim the 100-day moving average. The repeated rejection from this dynamic resistance around $1.95K, combined with the emergence of bearish daily candles, suggests buyers are losing momentum.

Meanwhile, Ethereum continues to struggle with the descending channel, with the upper boundary represented by the white trendline serving as the most critical support.

If sellers manage to push the price back inside this channel, it would confirm a bearish continuation and likely trigger a deeper decline toward the $1.56K to $1.64K demand zone. On the upside, bulls must first reclaim the $1.88K to $1.91K resistance area before attempting another move toward the 100-day MA near $1.95K.

ETH/USDT 4-Hour Chart

The 4-hour chart has turned more bearish after Ethereum broke below its ascending trendline, signaling that buyers have lost short-term control. This breakdown shifts the focus toward lower support levels unless bulls can quickly reclaim the broken structure.

The first support now lies within the $1.85K to $1.87K demand zone, where price is currently attempting to stabilize. Losing this area would likely accelerate the decline toward the next major demand zone between $1.75K and $1.79K.

On the other hand, the $1.88K to $1.91K supply zone has become the primary threshold for buyers. A successful reclaim of this region would invalidate the immediate bearish scenario and could allow Ethereum to challenge the descending resistance and the 100-day moving average once again.

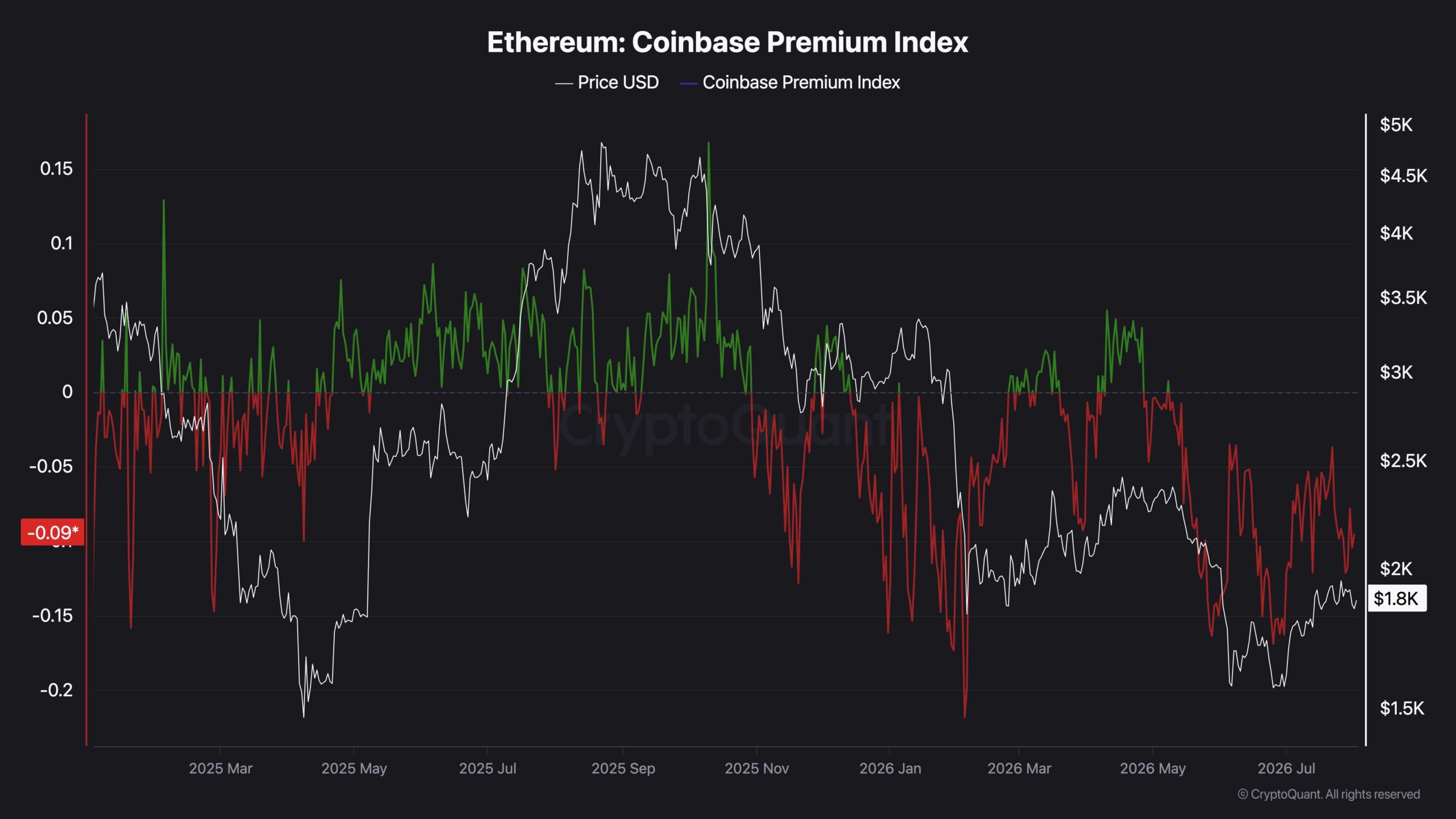

Sentiment Analysis

The Coinbase Premium Index remains in negative territory, indicating that Ethereum continues to trade at a discount on Coinbase relative to other major exchanges. This persistent negative premium suggests buying pressure from U.S.-based institutional participants remains relatively weak despite the recent recovery.

Historically, sustained positive readings have accompanied stronger bullish phases, whereas prolonged negative values often reflect cautious institutional sentiment. Until the premium returns to positive territory and remains there consistently, the current rebound may struggle to develop into a sustained uptrend, leaving Ethereum vulnerable to additional downside pressure if technical support levels begin to fail.

The post Ethereum Price Analysis: ETH’s Double Rejection at $2K Spells More Trouble Ahead appeared first on CryptoPotato.

Ripple’s XRP remains under steady selling pressure as the latest rebound attempts continue to lose momentum. The recent price action suggests sellers are maintaining control, while buyers are once again being forced to defend a critical support area.

Ripple Price Analysis: The Daily Chart

The daily chart shows little improvement compared to the previous analysis. The asset continues to trade beneath the descending resistance trendline while remaining well below the major moving averages, preserving the broader bearish market structure.

The latest candles indicate that sellers remain in control after another failed recovery attempt, pushing the price back toward the key demand zone around $1.01 to $1.04. This support has repeatedly prevented a deeper decline over the past several weeks, making it the most important level to monitor.

As long as XRP remains below the descending trendline and the main resistance between $1.24 and $1.29, the broader outlook favors continued weakness. A decisive breakdown below the $1.01 to $1.04 support zone would likely accelerate the decline toward the next major support around $0.89.

XRP/USDT 4-Hour Chart

On the 4-hour timeframe, rather than recovering from support, XRP has continued to print lower highs and lower lows while remaining capped by the descending resistance trendline.

The recent rejection near $1.09 was followed by another decline toward the $1.01 to $1.04 demand zone, showing that buyers have yet to regain control. This area remains the last significant short-term defense for the bulls.

If this support fails, the bearish momentum is likely to intensify and extend the decline toward lower levels. Conversely, buyers would first need to reclaim the descending trendline before any meaningful recovery toward the $1.24 to $1.29 resistance zone could be considered. Until then, rallies are likely to face selling pressure and remain corrective in nature.

The post XRP Price Analysis: Is a Drop Below $1 Inevitable as Sellers Stay in Control? appeared first on CryptoPotato.

Bitcoin continues to trade without a decisive directional bias as both buyers and sellers defend key technical levels. Until one side forces a confirmed breakout, the current environment is likely to remain dominated by range-bound price action and short-term liquidity grabs.

Bitcoin Price Analysis: The Daily Chart

The daily chart suggests Bitcoin is still locked in a prolonged consolidation phase between the major support around $57.8K to $60.2K and the primary resistance at $66.2K to $66.8K. Despite several attempts by both buyers and sellers, neither side has managed to establish a sustained trend beyond these boundaries.

This type of market structure typically favors liquidity sweeps and stop hunts around local highs and lows before a genuine directional move develops. As long as the asset remains trapped between these two zones, traders should expect continued choppy price action rather than a sustained trend.

A confirmed breakout above the $66.2K to $66.8K resistance could trigger another leg toward the higher resistance around $72K to $74K. Conversely, losing the $57.8K to $60.2K demand zone would invalidate the current consolidation and expose Bitcoin to a deeper correction.

BTC/USDT 4-Hour Chart

On the 4-hour timeframe, Bitcoin is trading inside an even tighter range within the broader daily consolidation. Buyers continue defending the support region at $61.8K to $62.2K, while sellers repeatedly cap rallies below the resistance around $64.9K to $65.6K.

Holding above the buyers’ defense could allow another recovery attempt toward the upper boundary of this range. However, the recent sequence of lower highs indicates that sellers still hold a slight advantage, making a breakdown below the $61.8K to $62.2K support zone the more likely scenario if buying momentum continues to weaken. Such a move could accelerate selling pressure toward the lower boundary of the broader daily range.

Sentiment Analysis

The two-week liquidation heatmap shows a notable concentration of liquidity just beneath Bitcoin’s recent lows. This suggests futures market participants have been actively defending that area, with buyers stepping in to absorb selling pressure whenever the price approaches the lower liquidity cluster.

At the same time, a substantial pool of liquidity remains above the market around the $66K to $67K region, indicating that both sides still have attractive liquidation targets. As long as Bitcoin remains inside its broader consolidation, the price is likely to continue oscillating between these liquidity zones before a decisive breakout determines the next major trend.

The post Bitcoin Price Analysis: Will the Next Liquidity Sweep Push BTC Below $60K? appeared first on CryptoPotato.

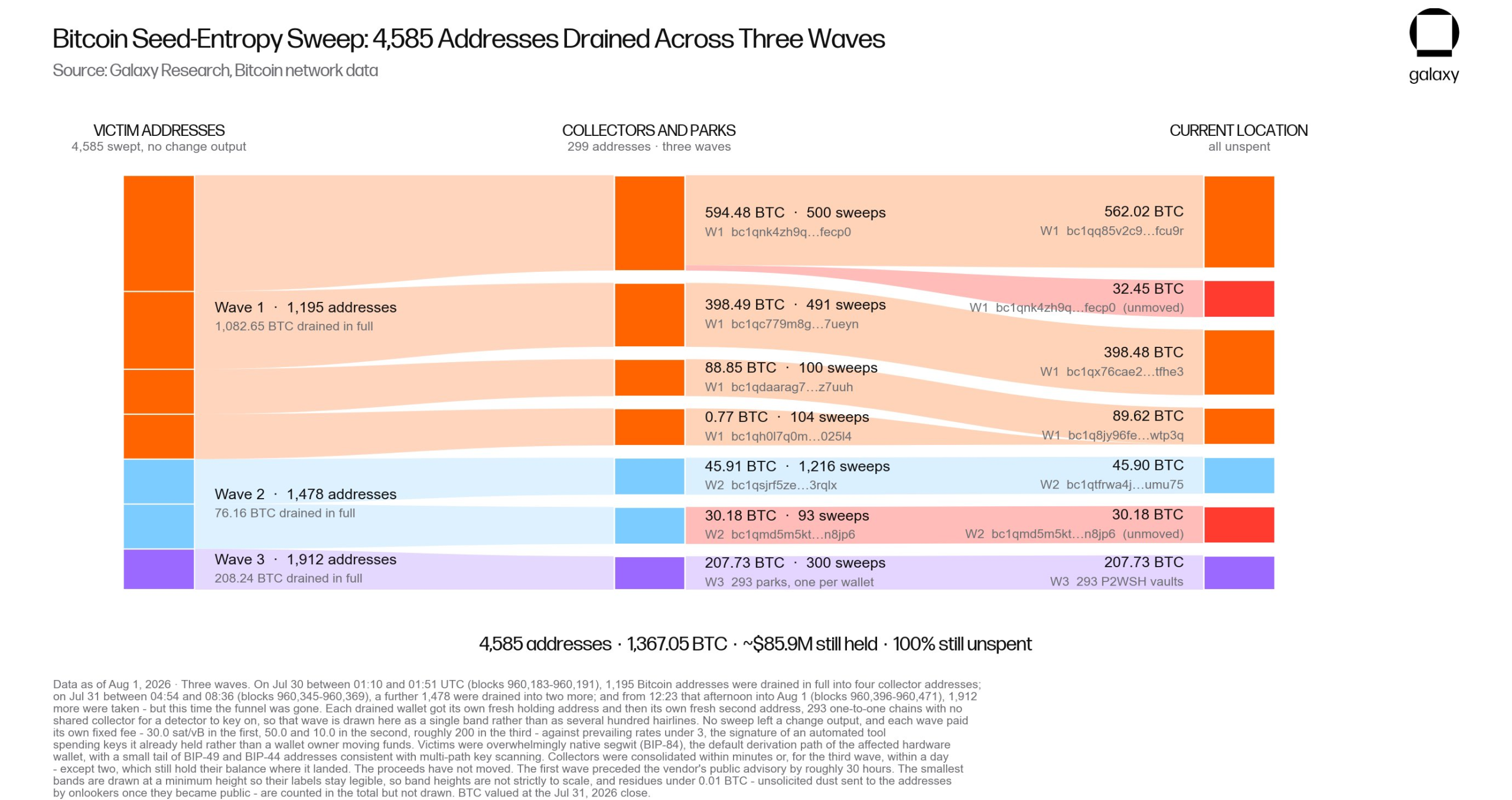

A Canadian entrepreneur lost more than $1.6 million in Bitcoin (BTC) from a Coldcard hardware wallet in under seven minutes, part of a wave that may total 1,367.05 BTC.

The case exposes an uncomfortable truth about self-custody: doing everything right may not be enough.

How One Holder Lost 18 BTC in Seven Minutes

Cold storage means keeping private keys on a device that never touches the internet. Jonathan Goodman followed that principle carefully, storing his Coldcard in a safety deposit box.

His 18.25 BTC sat in wallets secured across multiple safes. He never shared his seed phrase and kept every device isolated from online exposure.

None of it mattered on July 29, 2026. Between 9:36 and 9:43 that evening, every wallet he controlled was emptied.

Follow us on X to get the latest news as it happens.

Goodman first heard about a broader problem while at his cottage.

Assuming it would not affect him, he checked the balances in the Wasabi wallet software and found a series of red withdrawal transactions.

The vulnerability traces back to 2021. A flaw in the code that generates seed phrases left certain devices exposed, and attackers allegedly used artificial intelligence to brute-force the affected seed phrases.

He is filing reports with the police and the Ontario Securities Commission. Recovery hopes remain slim, though he wrote that the hardest part was having done everything right.

The scale extends far beyond one victim. Galaxy Research identified three suspected attack waves targeting addresses generated by Coldcard devices.

Those waves involved 4,585 source addresses and drained 1,367.05 BTC, worth roughly $88.6 million at the time of reporting.

What Galaxy Research Found in the Attack Data

Galaxy Research head Alex Thorn indicates that the attacks appear to be ongoing. He urged users who have not moved funds from potentially vulnerable setups to act immediately.

The first two waves showed similar transaction patterns and may share a common operator, though that remains unconfirmed. The third differed significantly, suggesting either updated tools or a separate actor exploiting the same key space.

The stolen Bitcoin remains in attacker-controlled addresses, with no further movement. Drained holdings had sat dormant for an average of 3.18 years, suggesting most victims were long-term holders rather than institutions.

Galaxy stressed an important caveat. Its findings rely solely on on-chain data and have not definitively confirmed insufficient randomness in the generation of the affected addresses.

“…this is a blow to bitcoin self-custody and we need to do better as a community: with security, with education, and with being realistic about complexity, expectations, and recommendations we make to friends, family, and the public…,” Alex Thorn said.

Analyst Shanaka Anslem Perera highlighted a deeper irony in Coldcard’s own documentation. The manual describes its default seed-generation method as the one it trusts most, while labeling it as low risk to users.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights.

Alternatives exist within the same device. Users can combine hardware output with dice rolls, or rely on dice alone, which the manual says removes all trust in the hardware. Most users likely followed the default path. That is precisely the method Galaxy Research now links to the losses.

The conceptual tension runs deeper. Reproducibility, prized for verifying firmware, becomes a liability in secret generation, since both weak and strong seeds produce valid 24-word phrases that appear identical.

Devices marketed under a “Don’t Trust, Verify” ethos can still harbor entropy flaws, leaving no visible trace. Affected users should assess their setups and migrate funds where necessary.

The post $1.6 Million Drained in a Blink: User Recounts His Dramatic Coldcard Wallet Hack appeared first on BeInCrypto.

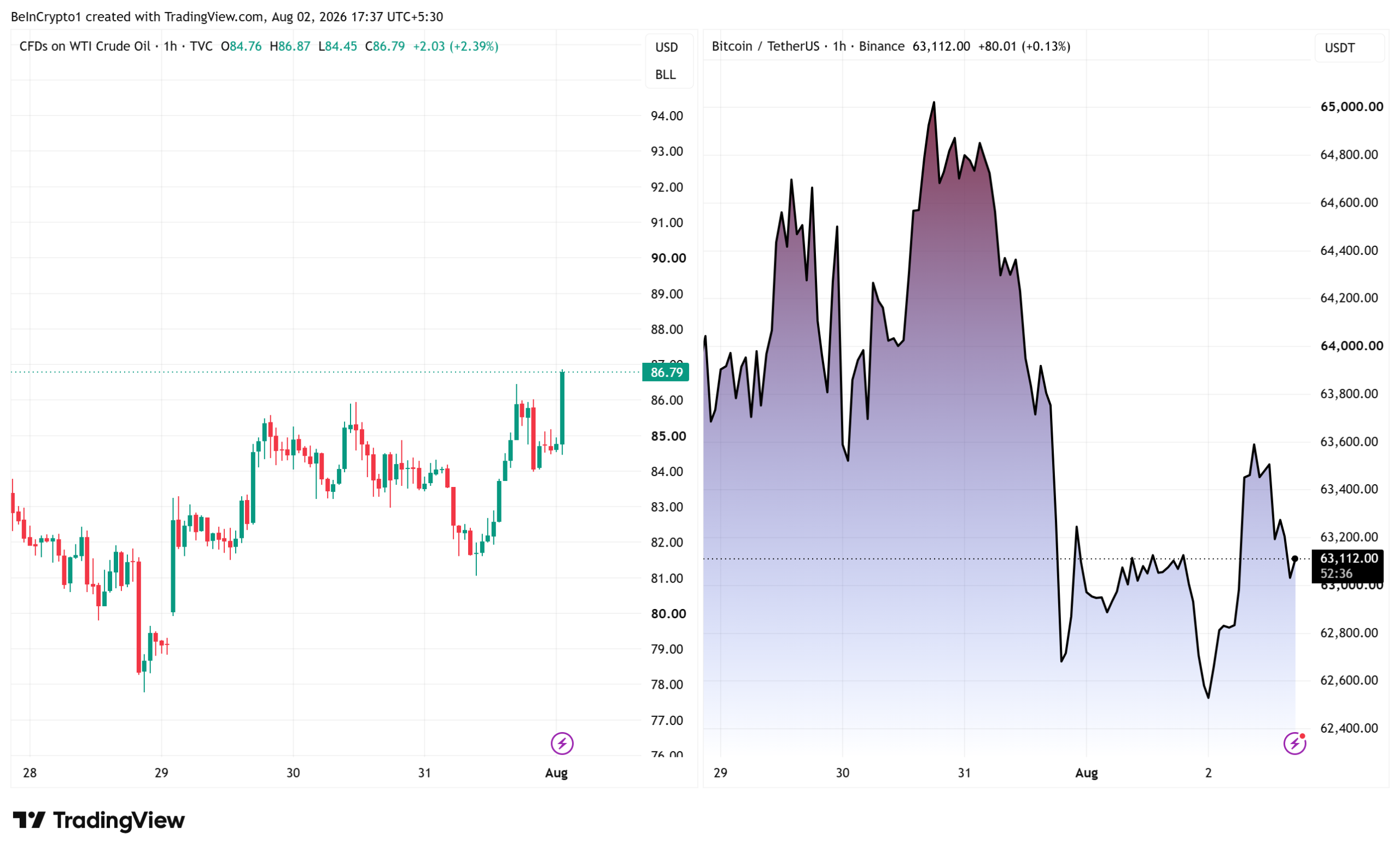

Iran has denied President Donald Trump’s claim that a deal exists to reopen the Strait of Hormuz, the world’s busiest oil route. Oil jumped on the denial.

Bitcoin (BTC) barely moved. That gap says a lot about what crypto traders now choose to ignore.

Trump Says a Hormuz Deal Exists. Iran Says It Does Not

Trump posted on Truth Social early Sunday. He said he had canceled a planned strike on Iran.

He wrote that Iran and its neighbors asked him to hold off. The reason, he said, was that “the perimeters of a deal has been agreed to.”

That deal would open the Strait of Hormuz right away. It would also end Iran’s nuclear threat.

Iran answered within hours. Fars News Agency quoted a source close to the nuclear talks.

“There is no agreement regarding the reopening of the Strait of Hormuz, and the news published about it is false,” Fars News Agency, via CGTN.

Follow us on X to get the latest news as it happens

Iran’s acting defense minister, Seyyed Majid Ibn Al-Reza, called Trump’s words psychological warfare. Fars International called Trump’s terms a wish list.

None of this is new. An earlier pause in strikes in late July also went nowhere.

Talks did happen, though. Qatari mediators met Iran’s foreign minister, Abbas Araghchi, and US envoy Steve Witkoff on Saturday. Saudi Crown Prince Mohammed bin Salman urged Trump to cool things down.

Why Oil Jumped and Bitcoin Did Not

Start with the map. The Strait of Hormuz is a narrow sea lane between Iran and Oman.

About 20 million barrels of oil passed through it every day in 2024, EIA data shows. That is roughly a fifth of the oil the world uses.

Here is the problem. Only about 2.6 million barrels a day can go around it, through pipelines in Saudi Arabia and the UAE.

The rest has nowhere else to go. That is why one denial can move a market this big.

WTI crude, the US benchmark, closed at $84.67 on Friday. It then rose about 2.4% to trade near $86.79.

The denial also puts an official forecast in doubt. On July 7, the EIA cut its Brent crude forecast for this quarter by $27 a barrel, to $74. It cited the June US-Iran deal and busier traffic through the strait.

That June deal has since fallen apart. Analysts tracking Hormuz reopening timelines now expect the route to stay restricted into 2027.

Bitcoin did almost nothing. It added 0.08% in 24 hours and sat near $63,063.

It also trades about 50% below its record of $126,080, set on October 6, 2025. The muted Bitcoin price reaction suggests traders now ignore headlines that change nothing on the water.

What Happens Next

Oil matters to crypto for one reason. It feeds inflation.

June proved the link. US energy prices fell 5.7% that month, the steepest drop since April 2020.

The BLS said energy did most of the work. Headline prices fell 0.4% over the month. Annual inflation cooled to 3.5% from 4.2%.

Energy is still expensive over a full year, however. Gasoline is up 26.7%.

So a lasting jump in oil would undo that progress. That makes Federal Reserve rate cuts harder to justify. Rate cuts are what assets like Bitcoin want.

The next check comes August 12, when the BLS publishes July inflation.

Until ships can sail through Hormuz freely, oil keeps its war premium. Bitcoin keeps waiting.

The post Iran Denies Trump’s Hormuz Deal, Oil Jumps but Bitcoin Watches appeared first on BeInCrypto.

South Koreans sent $367 million more in stablecoins out of the country than they brought back in June. It was the 18th month in a row that money left.

The Financial Supervisory Service (FSS) handed those numbers to lawmaker Lee Jong-wook. The streak started in January 2025. Traders are chasing something they cannot get at home.

Why South Korea’s Stablecoin Outflows Keep Widening

Five exchanges handle almost all local crypto trading. They are Upbit, Bithumb, Coinone, Korbit, and Gopax.

In June, they sent roughly $1.8 billion in stablecoins to foreign platforms. About $1.44 billion came back. The gap was $367 million.

Local media reported that across the whole second quarter, close to $1.1 billion left.

Follow us on X to get the latest news as it happens

The size is what caught the attention of lawmakers. Koreans bought about $470 million of foreign shares in June, according to the Korea Securities Depository. The stablecoin outflow matched 77.6% of that figure.

A year earlier, the ratio sat near 20%. Crypto money now leaves the country almost as fast as stock money.

The trend held even as the local market shrank. Seoul confirmed a 22% crypto tax for 2027, and domestic trading volume fell nearly 55% in the first half.

One caveat belongs here. The FSS counts only the five licensed exchanges, so coins sent to private wallets first never show up.

What Foreign Exchanges Offer That Seoul Cannot

Korean platforms mostly offer plain spot trading. That is the whole problem.

Foreign venues offer far more.

- Crypto derivatives with heavy leverage

- Dollar-based real world assets (RWAs)

- Decentralized Finance (DeFi) protocols

- Staking rewards

Some also list Samsung Electronics, SK Hynix, and Hyundai Motor as tradable contracts. Leverage on those can run into the tens of times. A stablecoin transfer is the cheapest way in.

The same hunger shows up in regulated markets. Koreans put a net $1.28 billion into foreign leveraged exchange-traded funds (ETFs) in June. That was more than triple the May total.

Seoul did try to compete. Korea listed its first single-stock leverage ETFs on May 27. Less than a month later, FSS Governor Lee Chan-jin publicly criticized them.

A bigger fix is on the way. Four agencies published a plan on July 19 to legalize won-backed stablecoins. A separate bill would treat crypto as national wealth.

The Leverage Unwind Sitting Behind the Numbers

The regulator’s worry proved well founded. Fourteen leveraged ETFs track Samsung and SK Hynix. Their assets shrank from about $10.7 billion at the end of June to $6.3 billion by July 13.

Margin loans fell too. Korean brokerages held roughly $21.8 billion on July 30, down about $4.4 billion since June 24.

The Kobeissi Letter says $67 billion has drained from margin accounts across Korea, China, and Taiwan. BeInCrypto could not confirm that total.

The KOSPI lost 22.19% in July, its worst month since 1997. Then it jumped 17.91% on July 31, a record single day.

Economist Steve Hanke blames global fatigue with AI hype. That rebound, led by a 29.95% gain in SK Hynix, cuts against the idea. Asia’s unwinding AI trade has swung just as hard in Tokyo.

The stablecoin figures tell a steadier story. Korean money is not hiding. It is relocating, much as it did when Korean investors cashed out late last year.

Lee sits on the National Assembly’s finance committee for the People Power Party. He wants the government to act.

“As the ‘coin move’ from domestic to overseas spreads, funds are flowing abroad, and investors are being defenseless against high-risk derivatives on foreign exchanges,” local media reported, citing Lee.

Seoul can close the exits or widen the menu at home. That choice decides what month 19 looks like.

The post South Koreans are Sending Stablecoins to Foreign Exchanges at Record Rate appeared first on BeInCrypto.

Everything under one login

Round-the-clock trading is one part of the plans exchanges have for traditional assets. Coinbase and Binance want customers to trade crypto, stocks and other products through one account, a model both have described as an “everything exchange” or financial super app.

Coinbase is preparing to offer U.K. customers equities and derivatives alongside crypto after securing investment-services authorization from the Financial Conduct Authority under rules based on the Markets in Financial Instruments Directive, or MiFID.

The authorization allows Coinbase to offer traditional shares to retail customers and crypto, equity and commodity perps to eligible institutional and advanced traders, the company said.

“Perpetual futures are a core focus of what Coinbase is trying to bring to market,” said Keith Grose, U.K. CEO at Coinbase, in an interview with CoinDesk. “We’re really focused on being the ‘everything exchange.’”

Grose said the longer-term plan is to bring spot crypto, perpetual futures, traditional equities, and eventually tokenized versions of other assets into one place. That could allow customers to use positions across different markets as collateral or borrow against their equities.

Using stocks as collateral

Binance is testing another part of the model by allowing some high-net-worth clients to use tokenized stock positions as collateral for other trades.

“We recognize you could have Nvidia or SpaceX stock, a tokenized version,” Jan said. “You could actually have a tokenized stock put on our exchange, and we’ll use that as collateral for you to trade something else. It could be a crypto derivative.”

WWE SummerSlam 2026 card: Complete list of matches for Night 2 on Sunday

UV Printer? 3D Printer? HeyGears Says “Why Not Both”?

Indian Real big money…. #shorts #money #india #indiamoney

-

Sports7 days ago

Sports7 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Business4 days ago

Business4 days agoWhy Trees Belong on the Risk Register

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Wit & Wisdom

-

Tech7 days ago

Tech7 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Politics2 days ago

Politics2 days agoMeta enters AI-training agreement with far-right ‘propaganda rag’ Newsmax

-

Politics6 days ago

Politics6 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Crypto World1 day ago

Crypto World1 day agoMicroStrategy Post-Earnings CLARITY Act Push Could Add New Catalyst for Its Stock

-

Politics5 days ago

Politics5 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

Entertainment5 days ago

Entertainment5 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

News Videos7 days ago

News Videos7 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Business4 days ago

Business4 days agoMajor shareholder moves on Canyon

-

News Videos3 days ago

News Videos3 days agoBitcoin Enters the 3rd Stage of the Bear Market

-

Crypto World1 day ago

Crypto World1 day agoXRP Ledger v3.3.0 brings five institutional features

-

Crypto World5 days ago

Crypto World5 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

Tech6 days ago

Tech6 days agoNew macOS Sequoia & Sonoma security updates for older Macs

-

News Videos5 days ago

News Videos5 days agoClaude: Build Financial Dashboards in Minutes (2026)

-

Politics3 days ago

Politics3 days agoLuke Littler’s dominance sparks GOAT debate

-

Sports3 days ago

Sports3 days agoSeema Kaliramna Wins Discus Throw Bronze, Takes India’s CWG Medals Tally To 17

-

Business5 days ago

Business5 days agoJohnson & Johnson agrees to $5.5B settlement over talc cancer claims

-

Crypto World6 hours ago

Crypto World6 hours agoCrypto PAC spending tops $2M in Michigan House race

You must be logged in to post a comment Login