Business

Costa Rica receives first group of deported migrants under third-country agreement with US

NEW DELHI — Millions of anxious students and parents across India are on edge as the Central Board of Secondary Education prepares to declare the CBSE Class 10 results 2026 for the first phase of board examinations, with strong indications pointing to an announcement as early as this week.

.

The Class 10 exams, conducted from February 17 to March 11, 2026, saw approximately 25 lakh students appear for papers in core subjects including Mathematics, Science, Social Science and English. This year’s exams operated under the board’s new two-phase system, with the main session (Phase 1) results now in the final stages of processing and verification. A second phase for improvement or compartment cases is scheduled for May 15 to June 1, with those results expected around June 6.

CBSE officials have not yet issued an official date and time, but multiple sources and trends suggest the results could drop anytime after April 14, potentially by mid-to-late April. This marks an earlier-than-usual timeline compared to previous years, largely to accommodate the second-phase exams and allow students sufficient time for revaluation or supplementary processes. DigiLocker has already prepared a “Coming Soon” result window, heightening expectations that the declaration is imminent.

Students will be able to access their scorecards through multiple platforms once released. The primary official websites are results.cbse.nic.in, cbse.gov.in and cbseresults.nic.in. Results will also be available on the UMANG app, via DigiLocker accounts linked to Aadhaar, and through SMS services. To check results, candidates need their roll number, school code or center number, and admit card ID. The board advises keeping admit cards handy and creating DigiLocker accounts in advance for seamless download of digital marksheets.

The two-board experiment introduced this year allows students who wish to improve their performance a second opportunity without waiting a full year. Education experts view the change as a student-friendly reform aimed at reducing stress and providing flexibility, though it has also increased logistical demands on the board for faster result processing.

In recent years, CBSE Class 10 pass percentages have consistently hovered above 93%. In 2025, the overall pass rate stood at 93.66%, with girls outperforming boys by a notable margin — 95% for girls compared to 92.63% for boys. Over 1.99 lakh students scored above 90%, while more than 45,000 achieved 95% or higher. Similar trends are anticipated this year, though final statistics will only emerge with the official declaration.

The board discontinued the practice of releasing an official merit list of toppers in 2020 to reduce unhealthy competition and mental pressure on students. Instead, high achievers receive merit certificates. Last year’s standout performances included students securing perfect 500/500 scores, with names such as Ayan Dutta making headlines. Schools and coaching institutes are expected to celebrate local toppers once individual results are out.

Evaluation of answer sheets has been underway since mid-March, involving thousands of teachers across the country working under strict confidentiality protocols. CBSE Controller of Examinations Sanyam Bhardwaj has emphasized the board’s commitment to accuracy and transparency in the assessment process.

For students who do not clear all subjects, compartment or supplementary exams offer a second chance. Revaluation and photocopy of answer books will follow in June and July, with final revaluation results expected in August. The board has also outlined clear guidelines for students seeking verification or scrutiny of marks.

The run-up to results has triggered the usual mix of excitement, nervousness and strategic planning among Class 10 students. Many are already exploring stream options for Class 11 — Science, Commerce or Humanities — based on expected performance. Career counselors advise against panic, reminding students that board marks, while important, are only one milestone in a longer educational journey.

Parents and teachers have been urged to provide emotional support during this period. Mental health organizations have issued advisories highlighting the need to manage expectations and avoid undue pressure, especially in a competitive academic environment.

The early result timeline is particularly significant this year because of the two-phase structure. Students who opt for Phase 2 will have their performance evaluated separately, ensuring that the first-phase results do not delay future academic planning for the majority.

CBSE has modernized result access in recent years with features such as digital marksheets on DigiLocker that carry the same legal validity as physical documents. Students are encouraged to download and securely store both digital and printed versions for future use in admissions and job applications.

Regional variations in performance have been a consistent feature of CBSE results. In past years, regions such as Delhi, Chandigarh and some southern zones have recorded higher pass percentages, while remote and rural areas sometimes face challenges related to infrastructure and resources. The board continues efforts to bridge these gaps through improved digital learning initiatives and teacher training.

As anticipation builds, social media platforms are buzzing with hashtags and countdowns. Coaching centers and schools are organizing result-watching events and counseling sessions. Online portals have prepared dedicated result pages with live updates, how-to guides and post-result career advice.

Education Minister has previously emphasized the government’s focus on reducing examination stress through reforms like the two-board system and competency-based questions introduced in recent years. The 2026 papers reportedly featured more application-oriented questions aligned with the National Education Policy 2020.

Once declared, the results will provide critical data on overall academic standards, subject-wise performance trends and gender gaps. Analysts will scrutinize pass percentages, compartment cases and high-score clusters to assess the effectiveness of teaching methodologies and curriculum changes.

For the millions of 15- and 16-year-olds who sat for the exams, this week could bring life-changing news — whether jubilation over stellar scores or motivation to work harder in the supplementary round. Either way, the CBSE Class 10 results 2026 represent a pivotal moment marking the end of secondary schooling and the beginning of specialized senior secondary education.

Students and parents are advised to check official CBSE channels regularly for the exact announcement and to rely only on verified websites to avoid falling prey to fake result portals that often surface during this period.

As the board puts finishing touches on what promises to be one of the most significant academic announcements of the year, the entire education community waits with bated breath. Whether the results arrive on April 14, later this week or by the end of the month, one thing is certain — they will shape the immediate academic futures of lakhs of young Indians and spark nationwide conversations about performance, equity and the evolving landscape of school education in the country.

Michael Petersen

Good afternoon, ladies and gentlemen, and I’m Mike Petersen, Chair of Scales Corporation. And it’s my pleasure to welcome you all to this annual meeting. Thanks for coming out today. I know it’s a beautiful day outside, and you would probably rather be enjoying it in the sun. But we’re thrilled to have you in attendance here, not only in person but online as well as through the virtual meeting today.

It’s a 114th Annual Meeting of the company, the 12th since it became a listed company and my fourth as chair. Once again, we’re holding a hybrid annual meeting and whether you are here in person or joining us online, I’d like to thank you and welcome you all.

As you may recall, shareholders, proxies and guests attending the meeting virtually, will be able to hear and see a live webcast. In addition, shareholders and proxies have the ability to ask questions and vote on resolutions. I’ll provide further details on those matters shortly. Just wanting to roll off on the floor.

Some housekeeping matters for those of you who have joined us in person. First, I’d like to remind you as a matter of courtesy to please turn your mobile phones to silent. Also, if there’s an emergency we need to leave, please do so through the marked exits. Staff will be available to help us in the eventuality that, that happens.

I’m pleased to confirm that we have a quorum and, therefore, declare the 2026 Annual Shareholders Meeting of

China has lifted bans on procurement of the key steelmaking ingredient from mining giant BHP Group, sources tell Reuters, ending a months-long dispute following a visit by the miner’s top executives to its largest customer.

Thailand is transitioning from fragmented, sector-specific environmental regulations to a unified and comprehensive national framework through its proposed Climate Change Act (CCA). This legislative shift, driven by international trade pressures such as the EU’s carbon border adjustments and domestic net-zero commitments, aims to establish an economy-wide architecture for carbon management.

Key Points

- Structural Regulatory Shift: The draft CCA moves away from traditional pollution control toward a centralized governance regime that includes statutory emissions targets, mandatory reporting for designated operators, and market-based mechanisms.

- Core Market Mechanisms: The Act proposes an emissions trading scheme (ETS), a potential carbon tax based on emissions intensity, and a regulated framework for the verification and trading of carbon credits.

- Green Taxonomy Integration: Thailand has introduced a “traffic-light” (Green, Amber, Red) classification system to define sustainable economic activities, which is expected to become the standard for disclosure requirements and sustainable finance.

- Legal Risks: Companies face increasing exposure to litigation regarding “greenwashing” or misleading sustainability claims, which may be prosecuted under securities laws, consumer protection statutes, or the new CCA enforcement regime.

- Regional Interoperability: The legislation is designed to be technically compatible with foreign carbon markets, with long-term goals of integrating Thailand’s carbon mechanisms with those of neighboring ASEAN states.

- Adaptive Legislation: The Act is structured as “living legislation,” featuring a mandatory five-year review cycle that allows authorities to tighten targets and recalibrate regulatory tools without requiring constant parliamentary amendments.

- Preparation Strategy: Businesses are encouraged to establish emissions baselines and internal carbon pricing frameworks immediately, rather than waiting for the formal enactment of the law.

Thailand is being driven to adopt a centralized, economy-wide carbon management framework (the draft Climate Change Act) by a combination of domestic policy imperatives and external market pressures.

Domestic Drivers

- Net-Zero Commitments: The primary domestic driver is the government’s commitment to achieving national net-zero policy goals, which require the transition from incremental, sector-specific regulations to a unified, enforceable legislative framework.

- Standardization of Sustainability: There is a need to establish a centralized governance regime that can effectively translate national emissions targets into binding obligations for specific sectors and operators.

- Integration of Fiscal and Market Tools: The government aims to move beyond traditional pollution control toward a system that integrates mandatory greenhouse gas reporting, emissions trading schemes (ETS), and potential carbon taxes to manage environmental impact at scale.

International Drivers

- International Trade Pressures: Thai exporters face significant risks from external regulations, most notably the EU’s Carbon Border Adjustment Mechanism (CBAM) . Without a domestic carbon pricing mechanism, Thai goods may be subject to carbon tariffs, placing them at a competitive disadvantage in global markets.

- Investor Demand: There is growing pressure from investors for credible, standardized sustainability regulation. This includes the use of a “traffic-light” green taxonomy to categorize economic activities against technical screening criteria, which influences sustainable finance and disclosure requirements.

- Regional Integration: Thailand is positioning its carbon management framework to be technically compatible with foreign carbon markets. The draft Act anticipates future connectivity with carbon markets in neighboring ASEAN states, which will likely evolve through bilateral or plurilateral arrangements based on regulatory equivalence and mutual recognition.

While political delays have pushed the timeline for enactment, legal experts advise businesses to proactively implement emissions tracking and internal governance systems to prepare for mandatory reporting, carbon pricing, and stricter sustainability disclosure standards.

Other People are Reading

Having always been a learning machine, I speak five languages, have worked as a sales agent, project manager, translator, computer consultant, software engineer, built a house with my own hands, published books and essays on literature, philosophy and art, have written for magazines of various kinds in different countries. After retiring early in 2004, little by little, I have become a fund manager for some friends and myself, following the principles of value investing laid out by Benjamin Graham, Phil Fisher, Charlie Munger and Warren Buffett. In my article “The Portfolio For Early Retirees” I presented a simple and practical way to structure an investment portfolio for early retirees. In 2015 I won the Seeking Alpha Contrarian Contest and was among the winners of several other competitions in later years. I have also been a regular contributor to Seeking Alpha Pro right from the start.I strive to gather above-average knowledge about my stock picks. As this takes many hours, despite managing my portfolio full-time, you should not expect me to throw out new ideas each and every week. My Investment Strategy Statement can be found here.Legal Disclaimer: My contributions to Seeking Alpha, or elsewhere on the web, are to be construed as personal opinion only and do NOT constitute investment advice. An investor should always conduct personal due diligence before initiating a position. Provided articles and comments should NEVER be construed as official business recommendations. In efforts to keep full transparency, related positions will be disclosed at the end of each article to the maximum extent practicable. I am not registered as an investment adviser, nor do I have any plans to pursue this path. No statements should be construed as anything but opinion, and the liability of all investment decisions reside with the individual. Although I do my utmost to procure high quality information, investors should always do their own due diligence and fact check all research prior to making any investment decisions. Any direct engagements with readers should always be viewed as hypothetical examples or simple exchanges of opinion as nothing is ever classified as “advice” in any sense of the word.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of DTEGF either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

NEW YORK — David Letterman, the longtime face of CBS’s late-night television, has sharply criticized the network’s decision to end “The Late Show with Stephen Colbert” after more than three decades of the franchise and hand the coveted 11:35 p.m. time slot to syndicated programming from media mogul Byron Allen.

In a candid conversation on his Netflix podcast released Friday, the 79-year-old comedy icon described the move as a clear cost-cutting measure rather than a creative choice. “They don’t want to spend any money, so they’re going to make money,” Letterman said while speaking with former “Late Show” executive producers Barbara Gaines and Mary Barclay.

CBS announced earlier this month that Colbert’s final episode will air May 21. Starting May 22, the network will air back-to-back half-hour episodes of Allen’s “Comics Unleashed” in the former “Late Show” slot, followed by Allen’s game show “Funny You Should Ask” at 12:35 a.m. The arrangement is a time-buy deal for the 2026-27 television season under which Allen Media Group pays CBS for the airtime and sells all the advertising itself.

Letterman, who hosted “Late Night with David Letterman” on NBC from 1982 to 1993 before moving to CBS to launch “The Late Show” in 1993 and retiring in 2015, suggested the shift marks the end of an era for big-budget, network-produced late-night talk shows. He characterized Allen’s panel-style format positively but bluntly tied the decision to finances. “They charge Byron Allen some reasonable price. He sells all the advertising for his ‘Comics Unleashed,’ and it’ll be, I think, 90 minutes or two hours of comics talking about funny stuff,” Letterman said. “The show is a pretty good idea. It’s all panel. Nobody’s doing any stand-up, except they’re seated doing stand-up.”

The comments come as the traditional late-night model faces mounting economic pressures. Ratings for “The Late Show with Stephen Colbert” have declined in recent years amid broader industry challenges, including audience fragmentation across streaming platforms and competition from YouTube, podcasts and cable news. Colbert’s program, known for its sharp political satire, often targeted former President Donald Trump and other conservative figures, drawing both praise and criticism depending on the viewer’s perspective.

CBS, now under Paramount Skydance ownership, has described the change as a way to turn a financially challenged late-night hour into a profitable one without the high production costs associated with a full-scale talk show featuring a house band, celebrity guests, writers’ rooms and extensive staff. Industry insiders say the time-buy model allows the network to collect revenue while offloading creative and operational responsibilities to Allen Media Group.

Byron Allen, a comedian, producer and billionaire businessman who built Allen Media Group into a major independent syndication force, has long aired “Comics Unleashed” in later time slots. The show features Allen moderating a panel of comedians riffing on topics in a roundtable format. Allen has called the upgrade to the 11:35 p.m. slot a career milestone, joking in recent interviews that after decades in the business he is ready for the spotlight. Reports indicate he is paying tens of millions of dollars for the lease, betting that strong ad sales and broader distribution will make the venture lucrative.

The transition ends a 33-year run for “The Late Show” brand on CBS. Letterman’s version defined the franchise with its quirky humor, innovative segments and memorable interviews. Colbert, who took over in 2015 after a successful run on Comedy Central’s “The Colbert Report,” brought a more politically charged voice that resonated during the Trump era but faced declining viewership in recent seasons.

Some television observers view the move as part of a larger industry reckoning. As streaming services and digital platforms siphon younger audiences, traditional broadcast networks are rethinking expensive original programming in fringe hours. Similar cost-conscious experiments have appeared at other networks, though none have fully abandoned the late-night talk format yet.

Letterman’s remarks carry extra weight given his deep history with CBS. He expressed disappointment that the network appeared unwilling to invest in developing a new high-profile host or sustaining the established brand. His podcast comments quickly spread across social media, with fans and industry figures debating whether the change signals the death of traditional late night or simply an evolution toward more sustainable models.

Allen, who began his career as a stand-up and later became one of the most successful Black media executives in Hollywood, brings a different energy. His programming emphasizes accessible comedy without heavy political commentary, potentially appealing to a broader, less polarized audience. Supporters argue the format could attract advertisers wary of controversy, while critics lament the loss of a platform for cultural and political satire that “The Late Show” provided under Colbert.

CBS has not publicly responded to Letterman’s comments. A network spokesperson previously described the Allen deal as a strategic step to ensure profitability in late night while maintaining comedy programming. The network will continue airing local news lead-ins, preserving the traditional flow into the 11:35 p.m. hour.

For viewers, the change means a shift from monologues, celebrity interviews and musical performances to a steady diet of panel comedy and game-show laughs. Whether the new lineup can retain the audience that tuned in for Colbert remains to be seen. Early social media reactions have been mixed, with some praising the lighter tone and others expressing nostalgia for the “Late Show” era.

Letterman, who has largely stayed out of the spotlight since retiring and focusing on his Netflix series “My Next Guest Needs No Introduction,” used the podcast moment to reflect on the business realities of television. At 79, he continues to offer unfiltered opinions shaped by decades at the top of the industry.

The final weeks of “The Late Show with Stephen Colbert” are expected to feature emotional farewells, high-profile guests and retrospectives. Colbert has not yet detailed his post-CBS plans, though speculation includes potential streaming projects or a return to more flexible formats.

As the calendar turns to May 22, CBS affiliates will debut the new comedy block. Byron Allen’s “Comics Unleashed” will lead, followed by “Funny You Should Ask.” The arrangement covers at least the 2026-27 season, with options for renewal depending on performance.

Letterman’s blunt assessment has reignited conversations about the future of broadcast television. In an era of cord-cutting and digital disruption, networks face difficult choices between prestige programming and bottom-line stability. His words — “They don’t wanna spend any money” — have become a succinct summary of the tension playing out behind the scenes at CBS and across the industry.

For a franchise that once defined late-night comedy, the transition to a syndicated time-buy represents a stark departure. Whether Allen’s panel format can capture lightning in a bottle or simply fill the hour profitably will determine if this experiment becomes a template for other networks or a cautionary tale.

In the meantime, fans of traditional late-night talk shows may find themselves flipping channels or turning to streaming replays of Letterman and Colbert classics. The desert of 11:35 p.m. is about to look very different, and the man who once ruled it has made clear he is not impressed with the new tenant.

While a sharp market correction has brought valuations down to fair levels, institutional desks are not yet signaling a “compelling buy.” Instead, a sense of urgency has taken hold as the math for dollar-based investors fundamentally breaks.

Market data from Elara Securities shows that India remains an outlier in emerging markets as it saw outflows extend to the fifth consecutive week while other EMs saw flows stabilizing.

Here are the seven brutal truths driving the great FII retreat:

1) The Ceasefire Mirage

The two-week truce in the Iran-US conflict gave markets a brief bounce, but institutional investors are not treating it as a turning point. FIIs view the pause as tactical, not diplomatic. With a blockade still looming and the threat of a “Phase 2” escalation firmly on the table, global funds are staying on the sidelines until a long-term settlement is actually signed. In the language of markets, this has been a dead cat bounce and sophisticated money knows it.

Also Read | Is Nifty’s cheap-looking valuation a mirage? Why $100 oil could trap value hunters

2) Crude Oil: The Twin Deficit Time Bomb

Brent crude hovering near $100 a barrel is not just an energy story for India but a macro-stability threat. FIIs are acutely conscious of the twin deficit trap: elevated oil prices simultaneously widen the current account deficit and stoke domestic inflation, creating pressure on the Reserve Bank of India to raise interest rates precisely when the economy needs relief.

3) The Yield Spread Has Flipped Against India

The arithmetic for foreign investors has fundamentally shifted. As US 10-year Treasury yields climb toward 4.5%, the risk premium for holding Indian equities has compressed sharply. Compounding the problem is the rupee, which recently breached the ₹95 mark for the first time. For dollar-based investors, currency depreciation acts as a silent tax on returns. And when risk-free USD assets are yielding meaningfully, the case for enduring emerging market volatility weakens considerably.

4) Better Returns Are Available Elsewhere

India is losing the capital allocation argument to its regional peers. Markets like South Korea and Taiwan are considered significantly more attractive from an FII perspective, with expectations of far superior earnings growth compared to the modest outlook for India in FY27. When global funds run relative value screens, India is no longer automatically at the top.

5) India’s Tax Regime Has Become a Competitive Disadvantage

India’s evolving tax landscape is increasingly being cited as a structural deterrent. The 2024 Union Budget raised short-term capital gains tax from 15% to 20% and pushed long-term capital gains tax from 10% to 12.5%. Combined with tweaks to the LTCG/STCG structure and a hike in Securities Transaction Tax (STT) from FY27, the cost of entry and exit for global funds has risen materially. When benchmarked against tax-friendly regimes in competing destinations like Vietnam or Indonesia, India’s framework is no longer the draw it once was.

6) Four and a Half Years of Zero Returns

Perhaps the most haunting statistic circulating in global investment banks is this: measured in US dollar terms, the Nifty has delivered almost zero CAGR since late 2021. For a global fund manager who held Indian stocks for four-plus years only to watch currency depreciation erase every capital gain, making the case for re-entry to an investment committee is an exceptionally difficult conversation.

7) The Earnings Shock

Beyond the immediate geopolitical crisis, a deeper fear is building: a structural earnings downgrade for India Inc. War-induced supply chain disruptions and elevated input costs are expected to weigh heavily on the Q1 and Q2 margins of India’s manufacturing and FMCG sectors. FIIs appear to be front-running this earnings shock by exiting before official numbers confirm what the macro data already suggests.

The double-digit earnings growth that was supposed to define FY27 is now at serious risk. If the geopolitical storm persists, that growth could be downgraded to single digits, delayed by at least two quarters, and potentially reset structurally lower.

The Bottom Line

The correction has brought Indian valuations down from stretched to fair. But fair is not a buy signal for investors who can find better risk-reward elsewhere, who are staring at a zero-return track record, and who face a macro backdrop that could deteriorate further before it improves. Until crude stabilises, the ceasefire holds credibly, and earnings guidance provides a floor, the $18 billion exodus may be the beginning of a longer reckoning.

The taxpayer-backed Sydney to Busselton Jetstar flights have been suspended as fallout from the Middle East war forces Qantas Airways to scale back services and flag a fuel cost blowout.

SYDNEY — WiseTech Global Ltd shares climbed 4.66% to close at $38.89 on Tuesday, adding $1.73 amid renewed investor enthusiasm for the Australian logistics software provider’s aggressive push into artificial intelligence and steady progress integrating its major e2open acquisition.

The move came on solid trading volume as the company, known for its flagship CargoWise platform, continues to navigate a transformative period marked by workforce restructuring, strong half-year results and reaffirmed full-year guidance. With a market capitalization hovering near A$12.5 billion to A$13 billion, WiseTech remains one of Australia’s most prominent technology success stories in the supply chain sector.

WiseTech Global, headquartered in Sydney, develops cloud-based software that powers international freight forwarding, customs compliance, logistics execution and trade management. Its CargoWise suite serves thousands of customers worldwide, handling complex global supply chains with integrated tools for visibility, automation and compliance. The August 2025 acquisition of U.S.-based e2open significantly expanded its footprint, adding scale in transportation management systems and broadening its addressable market across shippers, carriers and manufacturers.

In its first-half FY2026 results released February 25, the company reported total revenue of US$672 million, a 76% increase from the prior corresponding period. The jump was largely driven by the inclusion of e2open, though organic growth stood at 7%. Core CargoWise revenue rose 12% to US$372.4 million, with 9% organic expansion. Recurring revenue within CargoWise remained exceptionally high at 99%, underscoring the platform’s sticky, subscription-like model.

EBITDA climbed 31% to US$252.1 million, delivering a reported margin of 38%. On an organic basis excluding e2open, the EBITDA margin held steady near 51%, reflecting operational efficiency in the legacy business. Underlying net profit after tax increased 2% to US$114.5 million, while free cash flow rose 24% to US$153.6 million. The board declared an interim dividend of US$0.068 per share, up 1% on the previous period and representing a 20% payout ratio of underlying NPAT.

Management reaffirmed full-year FY2026 guidance, targeting total revenue between US$1.39 billion and US$1.44 billion — implying 79% to 85% growth — and EBITDA of US$550 million to US$585 million. CargoWise revenue growth is expected in the 14% to 21% range. Guidance incorporates one-off integration and restructuring costs but excludes any material net impact from the AI-driven job reductions announced alongside the results.

The most attention-grabbing element of the February update was WiseTech’s accelerated AI transformation. The company plans to cut up to 2,000 positions — roughly one-third of its global workforce — over FY2026 and FY2027, with initial reductions of up to 50% in product development and customer service teams. CEO Zubin Appoo and executives framed the move as a strategic pivot to embed AI deeply into the platform, creating agentic workflows, enhancing automation and strengthening the company’s data and integration moat.

An Australian union sought urgent talks following the announcement, highlighting broader concerns about AI-driven job displacement in the technology sector. WiseTech has emphasized that the restructuring aims to reposition resources toward higher-value innovation while delivering long-term efficiency gains. Analysts noted that the cost savings, combined with new commercial models such as CargoWise Value Packs, could support margin expansion and price uplifts in the second half.

The e2open integration has progressed ahead of plan in several areas, contributing meaningfully to first-half revenue. e2open, recognized as a leader in Gartner’s Magic Quadrant for Transportation Management Systems for the fourth consecutive year, adds complementary capabilities in cloud-based trade and supply chain execution. WiseTech expects the deal to be earnings-accretive in its first full year, funded through debt rather than equity issuance.

Additional strategic moves have bolstered the company’s position. In January 2026, WiseTech acquired the Centre for Customs and Excise Studies to enhance global customs education and compliance training. It also completed smaller tuck-in acquisitions and signed memoranda of understanding, including one with Saudi Arabia’s Elm Company to explore technology applications for logistics efficiency.

Recent share price action reflects a volatile but resilient trajectory. After a challenging start to 2026 that saw the stock trade as low as $35.54, Tuesday’s 4.66% gain builds on intermittent rallies tied to AI optimism and results reaffirmation. The 52-week range has been wide, stretching from that recent low to highs above $120 in prior periods, illustrating the stock’s sensitivity to guidance, acquisition news and broader technology sector sentiment.

Analysts remain generally constructive. Some brokers highlight WiseTech’s data moat, ecosystem integrations and potential for AI to drive deeper customer stickiness and new revenue streams. UBS, for instance, maintained a Buy rating post-results, citing positive indicators around large freight forwarder rollouts and the shift to value-based pricing. Consensus price targets have varied, with some projecting significant upside if execution on AI and integration remains smooth.

Challenges persist. Integration of e2open involves managing a larger, more diverse cost base, including higher proportions of professional services revenue. Non-CargoWise revenue streams from earlier acquisitions continue to decline as expected. Broader macroeconomic pressures on global trade volumes, currency fluctuations and potential delays in large customer implementations could affect growth.

Yet the underlying business fundamentals appear solid. CargoWise continues to win new customers and expand with existing ones, with 1,060 product enhancements delivered in the first half alone. High gross margins near 79% to 84% in the core platform support investment in research and development.

For investors, the AI narrative has become central. While job cuts raise short-term human and reputational considerations, many view them as necessary for WiseTech to remain competitive in a rapidly evolving logistics technology landscape where automation and predictive capabilities are increasingly table stakes.

Tuesday’s trading likely reflects a combination of bargain hunting after recent softness, positive rotation back into technology names and confidence that reaffirmed guidance provides visibility through the remainder of FY2026. Full-year results are scheduled for late August, with the annual general meeting in November.

WiseTech’s journey illustrates the opportunities and disruptions facing software companies in the age of AI. From its roots as a founder-led Australian business to a global player with thousands of employees and billions in revenue potential, the company is betting that bold transformation today will secure leadership in supply chain technology tomorrow.

As global trade grows more complex amid geopolitical shifts, sustainability demands and e-commerce expansion, platforms like CargoWise and the expanded e2open suite position WiseTech at the center of digital logistics. Whether the current share price momentum sustains will hinge on tangible proof of AI-driven efficiencies, margin improvement and accelerated organic growth in coming quarters.

For now, the 4.66% daily lift signals market willingness to reward a company embracing change at scale in one of the world’s most critical industries.

primeimages/E+ via Getty Images

Beware of noise, hurry and crowds

In his book Celebration of Discipline, American theologian Richard Foster warned that noise, hurry and crowds were the most significant obstacles to a vibrant spiritual life. The same could be said of successful value investing. When it comes to investing, ignoring the noise, exhibiting patience and being indifferent to the prevailing sentiment of the crowds sounds like the right thing to do. Most people would not argue with these principles, yet behavior suggests otherwise.

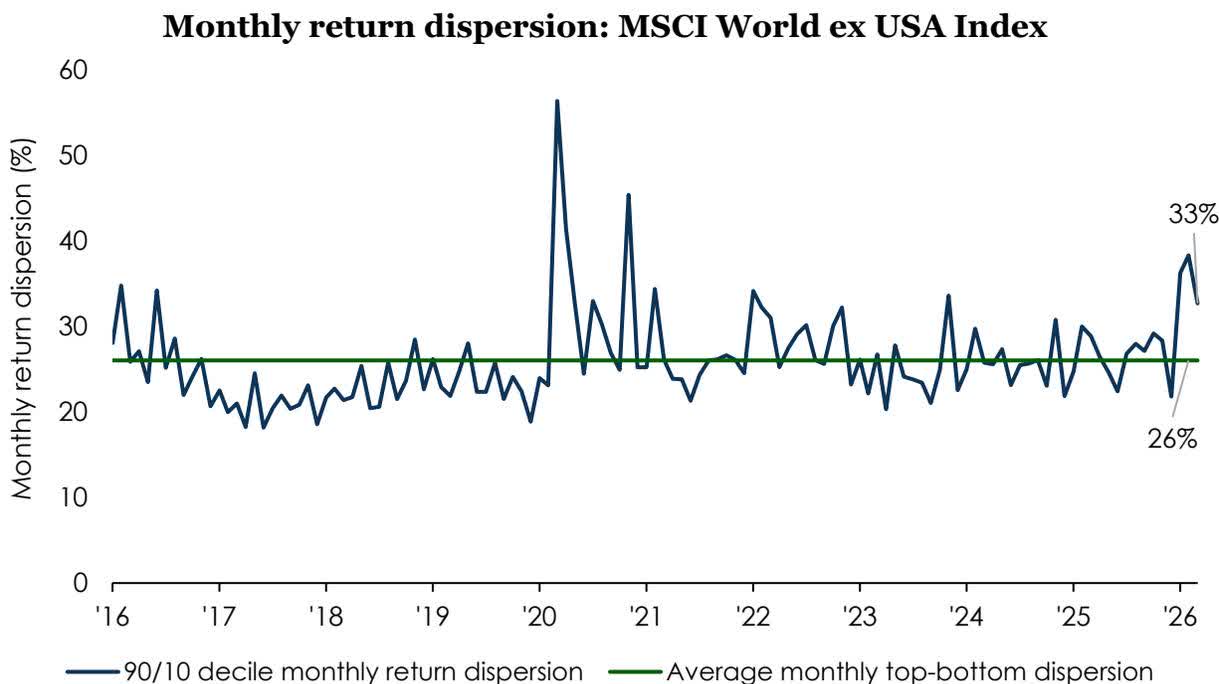

If there ever were a quarter of noise, this may have been it. The first 90 days of 2026 experienced near-record stock dispersion—that is, an unusually wide spread between the best- and worst-performing stocks—based on whatever company or industry the market happened to view that day as an AI winner or loser. For instance, the difference between the highest- and lowest-return stocks in the MSCI World ex-USA Index has been well above average, with a gap in performance of over 80 percentage points in the quarter, as investors debated the impact of AI. Then, in the last month of the quarter, bombs started falling in Iran and oil ran up well past $100 per barrel. As I write today, trying to make a deadline for publication with something timely and relevant, the White House announced progress toward a de-escalation. Noise galore.

Source: FactSet. Monthly data from 12/31/2015 through 3/31/2026. Returns represent the average performance of top and bottom decile stocks within the MSCI World ex USA Index; spreads are calculated as top decile minus bottom decile. Charts are for informational purposes only and do not depict the performance of any Harris | Oakmark strategy or product.

We aren’t technology neophytes; we believe AI is for real and is changing the way many of us work, and there will be winners and losers. However, we do believe the market has been too eager to declare victory and defeat. Where there is a real threat of change, we lower our estimate of value by reflecting a higher risk of disruption. In the case of large, deeply embedded enterprise software companies such as SAP, we think the market has skewed too negative on the risks introduced by AI, when in fact, there is a real possibility that AI is additive. We do not pretend to know how the Iran conflict is going to end, but there have been scores of these conflicts over my nearly 27 years at Harris | Oakmark and the world keeps turning. Remember, WTI (West Texas Intermediate) oil futures have both been in the triple digits and negative over the past six years. Meanwhile, population and incomes grow and the global economic pie along with them. We see the same bewildering headlines you do, but remain focused on the clarity of business values, which are far more stable than daily headlines.

The only way to really hurry your way to success in the equity markets is to have insight into the next tick and the ability to act before it moves. This requires an advantage in physics, not insight. At Harris | Oakmark, we estimate the intrinsic value of a business. There is an identifiable reason (or reasons) why the market price and our estimate differ. Often it boils down to our time horizon being longer than the marginal market participant. It takes time for value to be realized. Fixed income investors seem to understand this better than equity investors. In the bond world, one typically starts the conversation with duration—in other words, the desired time horizon for the securities you are looking to own. Equities are perpetual in duration, which means their theoretical time horizon is longer than that of even the longest bonds. Yet much of the market coverage focuses on one-minute charts, and the financial press seems to like or dislike a company based on how well it performed over the last quarter relative to broader expectations, with almost no airtime given to the long-term outlook for the business. Today, an estimated 60% of index options tied to the S&P 500 have same-day expirations and there are even new 5- and 10-minute option contracts being marketed for indices and cryptocurrencies. This short-termism reflects investors losing touch with the actual duration of the assets they own. Just because you can trade a stock one minute at a time (or less) doesn’t mean you should. At Harris | Oakmark, we think of equities as proportionate interests in real businesses that have real value based on the total future cash flows of the business. We have more insight into what the business ought to look like over time than where the stock will go over the next day, quarter or year. Don’t get me wrong, we would love the value gap to close the second we buy a stock, but unfortunately that is not how markets function.

Following the crowd is the easier—but more dangerous—path. I’m sure I’m not the only one who pleaded with my parents that, “everyone else was doing it” to which they replied, “if everyone else jumped off a cliff would you?” In markets, it is generally cause for concern when everyone seems to believe the same thing. Market participants make markets and markets price assets. Crowding occurs when there is more than typical agreement between market participants. That “agreement” gets priced into the asset such that there is little room for different outcomes without the stock getting pummeled. Beyond that, crowding introduces endogenous (or self-inflicted) risks that go beyond fundamentals, such as distorting liquidity dynamics on a security such that the distribution of future price outcomes skews negatively. By nature, as value investors we seek mispriced stocks—specifically, stocks selling well below their intrinsic value. Often this means going against the “crowd”. In our view, if everyone seems to believe something, you should assume a good portion of that belief is priced into the security. Meaning, if you and the crowds are right, there is little to no excess return and if wrong, painfully below average returns are likely. When a stock is undervalued, investors can afford to be wrong given the stock is unlikely priced to perfection. This is the essence of the “margin of safety” concept and the reason we require a significant discount before investing in any company.

We cannot promise much as regulated investment advisors but know that we are truly committed to a disciplined process that ignores the noise, exhibits patience, and is indifferent to the crowd.

Thank you for your partnership with us in our international equity portfolios.

We are eager to hear from you, so please do not be shy.

Tony Coniaris, CFA, Portfolio Manager

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Over 25 Lakh Students Await Results Expected Any Day

Why is Crypto Up? Ether, HYPE, and Solana Lead Following US Grand Deal

The Trump Family’s Business Expansion Could Reshape Presidency

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Alan Cumming Brands Baftas Ceremony A ‘Triggering S**tshow’

Forza Horizon 5 Money Glitch: TOP 3 METHODS to GET MONEY FAST in FH5 (PS5/XBOX/PC)

Iran Just Used Bitcoin To Break US Sanctions! (Here’s What Nobody Told You)

XRP- DTCC = $100T Flip Of The Switch? – The Clarity Act & Crypto Tax? – AI XRP Price Target?

-

Politics4 days ago

Politics4 days agoUS brings back mandatory military draft registration

-

Sports4 days ago

Sports4 days agoMan United discover Nico Schlotterbeck transfer fee as defender reaches Dortmund agreement

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Veronica Beard

-

Tech7 days ago

Tech7 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Politics4 days ago

Politics4 days agoMalcolm In The Middle OG Turned Down ‘Buckets Of Money’ To Appear In Reboot

-

Politics2 days ago

Politics2 days agoWorld Cup exit makes Italy enter crisis mode

-

Crypto World5 days ago

Crypto World5 days agoCanary Capital Files SEC Registration for PEPE ETF

-

Business4 days ago

Business4 days agoTesla Model Y Tops China Auto Sales in March 2026 With 39,827 Registrations, Beating Cheaper EVs and Gas Cars

-

Fashion7 days ago

Fashion7 days agoLet’s Discuss: DEI in 2026

-

Crypto World6 days ago

Crypto World6 days agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Crypto World15 hours ago

Crypto World15 hours agoThe SEC Conditionalises DeFi Platforms to Be Avoided for Broker Registration

-

NewsBeat1 day ago

NewsBeat1 day agoPep Guardiola and Gary Neville agree over Arsenal title problem that benefits Man City

-

Crypto World12 hours ago

Crypto World12 hours agoSEC Signals Exemption for Crypto Interfaces From Broker Registration

-

Business4 days ago

Business4 days agoOpenAI Halts Stargate UK Data Centre Project Over Energy Costs and Copyright Row

-

Business3 days ago

Business3 days agoIreland Fuel Protests Enter Day 5 as Blockades Spark Shortages and Government Prepares Support Package

-

Politics4 days ago

Politics4 days agoLBC Presenter Mocks Trump Over Iran War Failures

-

Crypto World3 days ago

Crypto World3 days agoFederal judge blocks Arizona from bringing criminal charges against Kalshi

-

Tech4 days ago

Tech4 days agoA version of Windows 10 released a decade ago is now eligible for additional security patches

-

NewsBeat2 days ago

NewsBeat2 days agoJD Vance announces ‘no agreement’ with Iran over nuclear weapons fear

-

Business3 days ago

Business3 days agoIMF retains floor for precautionary balances at SDR 20 billion

You must be logged in to post a comment Login