Business

Tribe Property Technologies Inc. (TRBE:CA) Q1 2026 Earnings Call Transcript

Operator

Thank you, everyone, for joining us. My name is [ Hitin Sanny ], and I’ll be the operator for today’s call. Welcome to Tribe Property Technology Fiscal First Quarter 2026 Financial Results Conference Call. This call is being recorded. We will be having a question-and-answer session at the end of the call. On our call today, we have Tribe’s CEO, Joseph Nakhla; and the company’s CFO, Scott Ullrich.

I trust that everyone has received a copy of our financial results press release that was issued earlier today. Listeners are also encouraged to download a copy of our financial statements and management discussion analysis from SEDAR+. Please note portions of today’s call, other than historical performance, include statements of forward-looking information within the meaning of applicable securities laws. These statements are made under the safe harbor provisions of those laws. Forward-looking statements are based on management’s current views and assumptions. Please review our press release and Tribe’s reports filed on SEDAR+ for various risk factors that could cause actual results to differ materially from our projections.

We use terms such as gross profit, gross margin, adjusted EBITDA and recurring revenue on this conference call, which are non-IFRS and non-GAAP measures. For more information on how we define these terms, please refer to the definition set out in our management discussion analysis. In addition, reconciliations between any adjusted EBITDA and net income is included in the press release this morning. Please note that all financial information is provided in Canadian dollars unless otherwise noted. With that, I will now turn the call over to Tribe’s CEO, Joseph Nakhla.

Donny DBM/iStock via Getty Images

After a strong start in January the market corrected largely due to the Strait of Hormuz crisis. Technology was the quarter’s worst-performing S&P 500 sector, especially software-related companies which suffered from AI disruption fears, excessive stock-based compensation and high valuations. Adding to that were monetization concerns over a sizable increase in “hyperscaler” capital expenditures in excess of $660 billion. The conflict in Iran and resulting Strait of Hormuz shutdown effectively halted shipping of 20.5-21 million barrels per day of crude oil and refined products that pass through what is one of the world’s most critical commodity corridors. This boosted energy, the best performing sector. Value outperformed growth with the Russell 1000 Value Index advancing 2.10% compared to a decline of 9.78% for the Russell 1000 Growth Index.

Defense Spending on the Rise

Geopolitical uncertainties over the last several years have brought about steadily increasing defense budgets, particularly in the United States which saw an increase from $715 billion in 2020 to just under $850 billion in 2025. For the first time ever, the 2026 budget exceeds $1 trillion. These increases have been driven by events like the Russia-Ukraine conflict as well as the war in Israel. Most recently, the US proposed a $1.5 trillion defense budget for 2027, citing factors like increasing global threats and the need for more domestic defense infrastructure. Lockheed Martin (LMT), Northrop Grumman (NOC) and RTX (RTX) stand to be among the largest beneficiaries of rising defense budgets, as all three are prime contractors for the US’s proposed $185 billion “Golden Dome” nationwide missile defense system. General Dynamics (GD), meanwhile, serves as the prime contractor for the nation’s $65.8 billion naval modernization effort. Boeing (BA) should see consistent revenue following their award of the F-47 next-generation aircraft contract, which is particularly attractive as aircraft programs typically run for decades. The previous generation F-35 first delivered in 2011 is still in production. Outside of traditional defense companies, we also see some tech names as beneficiaries of higher military spending with Nvidia (NVDA), Intel (INTC) and Qualcomm (QCOM) providing processing and compute for current and future autonomous vehicle and drone programs.

Growing Risk in Private Equity and Private Capital

The private equity and credit markets have exploded in growth over the last decade and are among the fastest-growing alternative asset classes. S&P Global estimated that private market assets under management totaled $15 trillion in 2024, up from $10.89 trillion in 2022. They project that those markets could reach more than $18 trillion by 2027. Private equity investments account for over half of the market. This lightly regulated industry is now facing headwinds. Payment-in-Kind loans have flourished as borrowers struggle to meet cash interest payments. Private equity funds are unable to exit their mid-market companies and investors are questioning valuation parameters. The opaque nature of these funds has further damaged investor confidence.

AI Disruption Fears Hit Software Companies Hard

The Software as a Service (SaaS) industry was one of the hardest hit areas of the market during the first quarter as investors have increasingly become uncertain over AI’s potential for disruption that could commoditize the industry and compress profit margins. Forbes reported that the software sector’s price-to-earnings ratio fell to 20 times during the first quarter compared to around 35 at the end of 2025, the lowest level since 2014. Companies like Intuit (INTU), Adobe (ADBE), Salesforce (CRM) and FICO (FICO) saw their shares fall 30%-37% during the first quarter despite reporting strong earnings. Investors fear that AI agents could replace much of the work currently performed by software companies for a fraction of the cost. Intuit has been working to counter the fears by heavily investing in their AI agent platform, bringing it to all their existing products. Adobe has been doing the same and both companies have seen strong support for AI features with around 90% of users taking advantage of the new capabilities. On the commodity risk side, these companies possess an advantage over popular general purpose AI models as they have access to specialized proprietary data they can use to train their own models. Adobe owns hundreds of licensed images they use for training and provides protection from litigation. Intuit instills confidence that taxes and business operations will comply with laws and regulations. AI models training only on public general data have a history of hallucinating false information and presenting it as fact which could be incredibly costly when dealing with important financial information. Proprietary data and the promise of security is something that we see as an advantage for long-standing SaaS companies that could help them better compete with growing AI players. It is amazing to see the P/E compression of these stocks since Covid. Fiserv (FI)—an unglamorous back-office processor for banks—was valued at over 100x earnings four years ago and now trades at just 7x, despite delivering 39 consecutive years of double-digit earnings-per-share growth.

Contributors

Bank of New York Mellon (BK) reached all-time highs following their first quarter earnings report of a 42% increase in year-over-year earnings per share along with an 18% increase in interest income resulting from higher yields. Assets under management grew 12% to a record $59.4 trillion. AI initiatives have been paying off as AI agents led to 20% faster client onboarding and 80% faster settlement inquiry investigation; agents are now writing 40% of all code. They returned $1.4 billion through repurchases and dividends and authorized a new $10 billion share repurchase program. CEO Robin Vince has done an exceptional job since taking over four years ago. Major US banks as a whole are aggressively retiring stock in 2026 due to recent deregulation, with a record $33 billion bought back in the first quarter alone—up 35% from the prior year quarter. This is the type of “double play” return we seek; an undervalued, vital, dull business with inspired management improving operating results leading to a sixfold return on our investment.

Industrials were the best performing sector during the quarter relative to the overall Fund, due in part from strong reshoring thanks to low domestic natural gas prices, legislation like the CHIPS and Inflation Reduction Acts as well as geopolitical risks that incentivize companies to return manufacturing to the US. Last year’s massive increase in hyperscaler capital expenditures continues, projected to be over $650 billion this year and may account for up to half of US GDP growth. Strong performers in the Fund included Gates (GTES), Caterpillar (CAT), Corning (GLW), and FedEx (FDX). Corning has seen strong demand for their optical connectivity products used in AI-focused data centers. Corning CEO Wendell Weeks is impressive in his ability to execute.

Defense and aerospace companies Boeing, Parker-Hannifin (PH), General Dynamics and RTX have reaped the benefits of a massive increase in global defense spending in response to rising conflicts.

Skilled labor educators Lincoln Educational (LINC) and Universal Technical Institute (UTI) have reported strong growth in student starts as demand for trades continues to rise. The expansion of data centers has led to high demand for electricians, HVAC technicians, welders and CNC machining engineers. AI automation is expected to impact many professional industries, driving interest in trades that are viewed as more resistant to disruption. Reshoring trends in the US specifically in the semiconductor and defense industries are also contributing to strong student starts.

Energy refiners Valero (VLO) and Phillips 66 (PSX) outperformed with diesel and Jet A fuel prices soaring. The crack spread hit a record $88.25 per barrel of oil in March. Chevron (CVX) has been a major beneficiary of years of diligent investments in oil and gas production.

Detractors

UnitedHealth (UNH) has been a major laggard for the past quarter and year. However, since CEO Stephen Hemsley’s return last May operating performance has been improving. We made over a fivefold return under his previous tenure from 2006-2017 and are confident that he can navigate a successful turnaround going forward. The recent medical cost ratio (MCR) of 83.9% is the lowest in two years and combined with a 2.48% CMS rate increase this spring has been a big boost. The lower amount spent on patient medical claims follows the company’s late 2025 shift to focus on higher margin patients over aggressive membership growth. Total membership has fallen by about 700,000 since the end of 2025. Management cited their higher margins as the reason for raising their full year adjusted earnings per share guidance to over $18.25, up from their previous guidance of $17.75 in January and consensus estimates of $17.86. Going forward, management also announced at least $1.5 billion in spending on artificial intelligence technology in 2026. This technology will be focused on areas like helping members understand their coverage and automating some administrative tasks and claims processing.

Software-related stocks in the portfolio have been hit hard due to the threat of margin compression from artificial intelligence. Microsoft (MSFT)’s 21.9% drop in the quarter was the worst decline since the 2008 financial crisis. They are spending $190 billion on AI-related capital expenditures in 2026 yet their AI Copilot product has failed to scale, with less than 15 million total paid seats. Google Gemini has successfully integrated their AI and captured the largest share of casual AI users with 2 billion people interacting with “Gemini-powered AI overviews” in Google Search every month. Microsoft has a large installed base with Fortune 500 companies. They have over $88 billion in cash on the balance sheet which is a huge competitive advantage. It is hard to bet against CEO Satya Nadella who took over in February 2014 and has a great record with the stock up over elevenfold.

First Quarter 2026 Performance Update

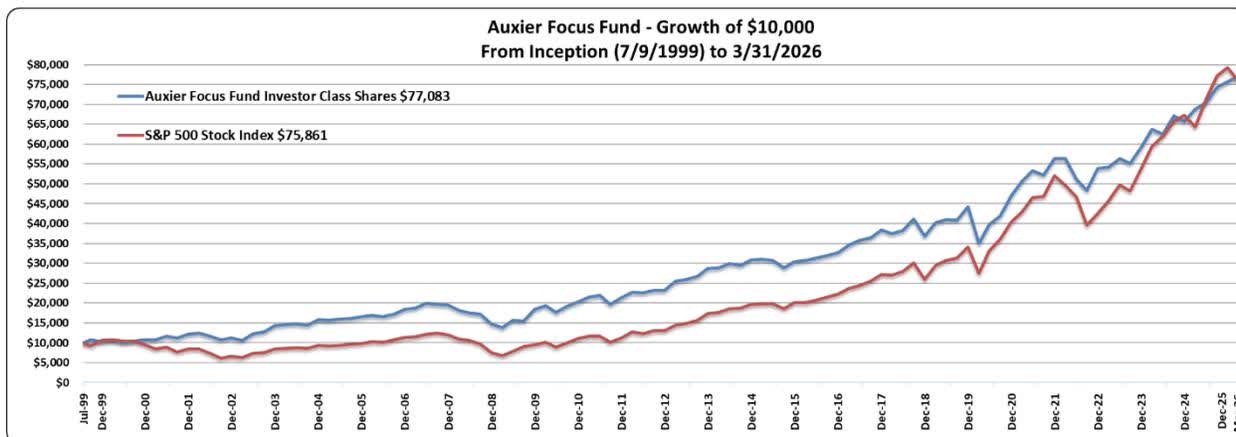

Auxier Focus Fund’s Investor Class gained 1.73% in the first quarter of 2026 with stocks up 2.00%. For the same period the S&P 500 cap-weighted index declined 4.33% and the equal weight returned 0.67%. The Russell 1000 Value was up 2.10%. For the quarter, fixed income investments as measured by the S&P US Aggregate Bond Index returned 0.04% and the longer-dated ICE US Treasury 20+ Year Index was up 0.11%. Stocks in the Fund comprised 92% of the portfolio. The breakdown was 82.5% domestic and 9.5% foreign, with 8.0% in short-term debt instruments. A hypothetical $10,000 investment in the Fund from inception on July 9, 1999 to March 31, 2026 is now worth $77,083 vs $75,861 for the S&P 500 and $65,542.76 for the Russell 1000 Value Index. During the same period, equities in the Fund (entire portfolio, not share class specific) have had a gross cumulative return of 1,323.34% vs 658.61% for the S&P. The Fund had an average exposure to the market of 82% over the entire period. Our results are unleveraged.

In Closing

We continue to seek businesses and managements displaying a strong culture with a heart and soul. Great leadership combined with enduring business models purchased in periods of fear and uncertainty have generated most of our returns over the past three decades. We have had good luck

with gritty founder CEOs who love their business. There is however a shortage of great operators. The key is to identify these managers and businesses ahead of time and do vigorous daily research to determine the sustainable earnings power of each entity. While we are aggressively monitoring the risks of a continued Strait of Hormuz shutdown, we remain mindful that many opportunities can be missed by focusing too much on macro headlines and not enough on micro details of improving operating fundamentals with exceptional leaders. Program trading dominates the investment landscape, but we firmly believe that investing is still the craft of the specific and knowing what you own is crucial to mitigating risk and improving investment odds.

Finally, during this time of global turmoil Warren Buffett said it best: “What we learn from history is that people do not learn from history. You can count on fear, greed and folly to be ever present in the marketplace. Their sequence is unpredictable; their duration is unpredictable; and their effects are unpredictable. But their presence is certain. ” Emotional and psychological responses to money often lead to substantial misappraisals in auction markets, creating new opportunities.

We appreciate your trust.

Jeff Auxier

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Rocket Pharmaceuticals CEO Shah sells $171,840 in stock

ismagilov/iStock via Getty Images

Dear Baron First Principles ETF ® Shareholder,

Performance

Baron First Principles ETF ® ((the Fund)) had a disappointing start to 2026, with a decline of 8.51% (NAV) compared with a 9.54% loss for the Russell 3000 Growth Index ((the Benchmark)). The declines were due to continued concerns about the effects of AI on many businesses throughout the portfolio as well as worries about the impact of the Iran war on inflation, interest rates, and consumer spending. These declines were partially offset by Space Exploration Technologies Corp. (SPACE) (SpaceX) and its deal to acquire X. AI Holdings Corp. (X.AI) (xAI), which resulted in the revaluation of the combined business at a significantly higher enterprise value.

While we are disappointed with the start of the year, we continue to see opportunities throughout the portfolio. Our portfolio companies continue to do quite well and are generating strong growth and cash flow for additional investments in their businesses to accelerate growth further with excess cash being returned to shareholders through share buybacks and dividends.

Our companies all have strong balance sheets with many operating with financial leverage below their targeted levels, giving them additional liquidity to lever up and buy back more stock should they desire.

Many stocks in the portfolio are now trading at historically low valuations, and we believe there is a disconnect between where these businesses trade today and what they can become over time. As a result, this past quarter we saw an accelerated rate of insider purchases from executives and directors at Verisk Analytics, Inc. (VRSK) , Birkenstock Holdings plc, Vail Resorts, Inc. (MTN) , FactSet Research Systems Inc. (FDS) , and MSCI Inc. (MSCI) When we see these insider purchases, it gives us further confidence in our investment theses for these growth businesses and reinforces our belief that valuations are attractive. As a result, during the quarter we increased our positions in many of these stocks while adding a couple of new names as well. We are continuing to make sure the portfolio remains focused while being cognizant that positions are appropriately sized for risk in this concentrated Fund.

Cumulative performance (%) for periods ended March 31, 2026

.

We believe this combination of strong revenue growth with well-positioned balance sheets and attractive valuations offers multiple avenues for potential returns for investors. As a result, we view the portfolio as compelling, with a favorable risk/reward profile.

Further, we believe there is still a ton of capital remaining on the sidelines waiting to be invested, including private equity firms who continue to raise new funds. We believe as rates continue to move lower over the next year, public to private transactions and strategic acquisitions should accelerate, which should further support valuations and our investments.

We continue to believe these businesses have strong competitive advantages with underpenetrated growth opportunities ahead of them and robust balance sheets to finance their growth.

While it is only the Fund’s first full quarter of performance, we believe the Fund should generate significant excess returns over time with much less than market risk. This is due to the balanced nature of the portfolio with approximately 35% invested in high-growth disruptive investments that can generate revenue growth of as much as 20% to 30%; between 15% and 20% of the portfolio in real irreplaceable assets that trade at significant discounts to replacement cost and where they would sell to private equity or another strategic buyer; between 20% and 25% in financials businesses, many of which are financial data providers that have recurring revenue and earnings given the embedded nature of their products in the workflow of their customers; and the balance in core double-digit revenue growing businesses that are more mature in their lifecycle and generate earnings growth while using excess cash for dividend increases, share buybacks, and additional investments in the business to accelerate growth further.

Total returns by investment type for the quarter

Total returns by investment type for the quarter

Aside from two of our private investments, SpaceX and xAI successfully completing their combination at a valuation significantly higher than previous marks, performance in the first quarter was hurt by continued concerns about the introduction of AI into the economy and those businesses that could be impacted most from the new competition. These included our subscription-based software and platform investments such as Spotify Technology S. A. , FactSet, and Guidewire Software, Inc. However, while the increased competition hurt the valuation of these stocks in the quarter, it has not impacted financials, and these companies continue to generate strong revenue growth and margins in line with company and investor expectations.

Further losses were seen in our exposure to consumer-focused investments given worries about the escalation of the war in Iran and what that could mean for inflation, interest rates, and consumer spending. These included companies such as Red Rock Resorts, Inc. , Hyatt Hotels Corporation , and On Holding AG . However, despite worries about the war and its impact on the consumer, these companies continue to do quite well as the consumer remains resilient despite macro concerns.

Global digital music streaming platform Spotify declined by 17.4% in the first quarter and detracted 77 bps from performance as investors were concerned about the impact AI music could have on the conversion of free subscribers to paying subscribers as well as how it could impact time on the platform. In addition, further concerns about the timing of price increases and resulting margin expansion also frustrated investors. However, the company continues to institute price increases across multiple regions and complete negotiations with major record labels. User growth remains strong growing at a double-digit rate with high engagement and low churn even with price increases. The company remains on a path to increase gross margins through its high-margin artist promotions marketplace, growing podcast contribution, and ongoing investments in advertising where revenue growth is expected to accelerate this year. We continue to view Spotify as a long-term winner in music streaming with potential to reach 1 billion-plus subscribers by 2030.

Property and casualty (P&C) insurance software vendor Guidewire declined 24.7% in the first quarter and detracted 84 bps from performance. The declines were due to continued AI concerns and potential future competition. However, the company continues to do quite well and after a multi-year transition period, the company’s cloud transition is substantially complete, and insurers are upgrading to the cloud at an accelerated rate. We believe that cloud will be the sole path forward, with annual recurring revenue (ARR) benefiting from new customer wins and migrations of the existing customer base to the company’s Insurance Suite Cloud. We also expect the company to shift R&D resources to product development from infrastructure investment, which should help drive cross-sales into its sticky installed base and potentially accelerate ARR over time. We are encouraged by Guidewire’s subscription gross margin expansion, which improved by approximately 580 bps in its most recently reported quarter. We believe Guidewire will be the critical software vendor for the global P&C insurance industry, capturing 30% to 50% of its $15 billion to $30 billion total addressable market and generating margins above 40%.

Shares of global hotelier Hyatt declined 8.6% and hurt performance by 34 bps in the first quarter as investors were concerned with a potential deceleration in revenue per available room (RevPAR) growth due to the Middle East conflict as well as cartel uprisings in Mexico that could hurt travel to those parts of the world. However, according to Hyatt management, the Middle East is only 3% of total fees and Mexico, while it represents approximately 7% of global rooms, is seeing travelers switch and rebook for other places including its Caribbean properties. There has been no impact on unit growth, and the company still expects to grow units between 6% and 7% this year. We believe this growth combined with low single-digit RevPAR growth and slight margin improvement should lead to double-digit EBITDA growth this year. This should generate strong free cash flow, which the company can use for further share buybacks and reinvestment back into the business. The company still has a strong investment grade balance sheet with 90% of the business coming through fees that should allow them to overcome any short-term outside disruptions to its business. Hyatt trades at a discount to peers despite a similar growth and mix of business. We believe this discount should narrow over time as investors see the continued growth and resilience of its business model.

Shares of Las Vegas Local casino operator, Red Rock Resorts, declined 11.2% in the first quarter and hurt performance by 44 bps as investors were concerned with a potential slowdown in Las Vegas gaming revenue brought about by the macro uncertainty from the war in Iran. Combine this slowdown with construction disruption due to many renovation and expansion projects occurring at its properties and current earnings could decelerate. However, the company continues to spend at its resorts as management sees further opportunities for growth from continued population growth and a higher net worth individual coming to Las Vegas. The company continues to generate strong cash flow that should produce accelerated growth in the coming years. We continue to believe the stock remains attractively valued as the company’s founders recently bought stock at current levels giving us further confidence in the company’s accelerated growth prospects.

Top contributors to performance for the quarter

Space Exploration Technologies Corp. (SpaceX) is a high-profile private company founded by Elon Musk. The company’s primary focus is on developing and launching advanced rockets, satellites, and spacecrafts, with the ambitious long-term goal of making life multi-planetary. SpaceX is generating significant value with the rapid expansion of its Starlink broadband service. The company is successfully deploying a vast constellation of Starlink satellites in Earth’s orbit, reporting substantial growth in active users, and regularly deploying new and more efficient hardware technology. Furthermore, SpaceX has established itself as a leading launch provider by offering highly reliable and cost-effective launches, leveraging the company’s reusable launch technology. SpaceX capabilities extend to strategic services such as human spaceflight missions. Moreover, SpaceX is making tremendous progress on its newest rocket, Starship, which is the largest, most powerful rocket ever flown. This next-generation vehicle represents a significant leap forward in reusability and space exploration capabilities. We value SpaceX using prices of recent financing transactions.

FIGS, Inc. designs and sells scrubwear for health care professionals through a digitally native, direct-to-consumer strategy. Shares rose following robust fourth-quarter results and upbeat 2026 guidance. Revenue expanded 33% to $201.9 million, reflecting broad-based momentum across categories and geographies and exceeding expectations. Holiday demand was strong throughout the season and remained elevated through quarter-end. U. S. revenue rose 28.7% to $164.2 million, while international revenue accelerated 55% to $37.7 million, with scrubs and non-scrubwear contributing gains of 35% and 26%, respectively. This topline strength translated to profitability, with EBITDA rising 29.8% to $26.7 million. Building on this momentum, revenue is expected to grow in the low-20% range in the first quarter and 10% to 12% for the full year. Additional drivers include accelerating international expansion, new store openings (both the ramping 2025 cohort and four locations planned for 2026), and continued traction in TEAMS (FIGS’ enterprise and group ordering business). The company maintains a strong balance sheet, with no debt and roughly $300 million in cash and marketable securities.

Global hotel franchisor Choice Hotels International, Inc. contributed to performance during the quarter as the company saw a slight acceleration in revenue per available room across its portfolio. Choice continues to grow units at a low-single-digit rate and is benefiting from higher royalty rates on new franchise contracts, driving mid-single-digit growth in earnings and free cash flow. The company is using this cashflow to return capital through share repurchases. We continue to believe the stock offers compelling value, trading at a roughly five multiple-point discount to its historical average. Choice maintains a strong balance sheet, providing flexibility for additional share buybacks, particularly when the stock trades below the company’s view of intrinsic value. Choice’s steady growth profile, both domestically and internationally, should further support attractive shareholder returns over time.

Top detractors from performance for the quarter

Tesla, Inc. designs, manufactures, and sells fully electric vehicles (EVs), solar products, and energy storage solutions, while developing advanced real-world AI technologies. Following robust gains in late 2025, shares fell as investors awaited progress on robotaxis and assessed the company’s sizable investments in manufacturing and AI. Operationally, Tesla delivered strong quarterly results amid a challenging EV environment. Automotive gross margins improved sequentially and beat expectations, the energy storage business maintained robust momentum with best-in-class margins, and battery cell production ramped. The company continues to advance its AI and autonomous driving initiatives at a rapid pace. Management anticipates meaningful robotaxi expansion in 2026 and continues to finalize the Optimus Gen 3 design and build out large-scale manufacturing capacity for humanoid robots. Tesla is also releasing major Full Self-Driving enhancements, scaling AI training compute, and deepening vertical integration in semiconductor design and production. These initiatives, while increasing near-term capital spending, underscore Tesla’s pivot toward becoming a leader in physical AI.

CoStar Group, Inc. is the leading provider of information and marketing services to the commercial and residential real estate industries. Shares fell due to multiple compression driven by rising AI fears. The market has come to view AI as an existential risk for a growing number of industries—including software, business services, information services, and video games—despite no evidence of any fundamental impact to these sectors. This “shoot first and ask questions later” dynamic has resulted in meaningful share price declines. We continue to own CoStar given its differentiated data assets and significant growth opportunities in providing enhanced real estate information, analytics, and marketplace offerings. CoStar boasts an enviable business model with high levels of recurring revenue and meaningful cash flow generation potential. While near-term cash flow is obscured by elevated investment in Homes. com, we expect spending to moderate and cash flow to improve over the next several years. The company also maintains a substantial cash balance, which we are hopeful will be used to aggressively repurchase shares at current depressed valuation levels.

Syndicated research provider Gartner, Inc. detracted from performance as valuation multiples compressed amid rising concerns around AI. Investors have increasingly viewed AI as a potential existential risk across a widening range of industries—including software, business services, information services, and video games—despite no evidence of any fundamental impact to these sectors. This “shoot first and ask questions later” dynamic has driven meaningful share price declines across the group. Against this backdrop, shares of Gartner came under pressure after the company reported contract value growth that was just 0.5% below expectations, underscoring the dramatic valuation compression at play. We continue to own Gartner given its large addressable market, significant competitive advantages, and robust free cash flow generation, which we expect management to deploy toward share repurchases at depressed valuation levels. We also view Gartner as an AI beneficiary, as it can leverage emerging tools to extract deeper insights from its vast trove of proprietary data and deliver it to customers in chatbot-type formats that meaningfully enhance its value proposition.

Portfolio Structure

We are steadfast in our commitment to long-term investing in competitively advantaged, growth businesses. We run a balanced portfolio of uncorrelated businesses to help reduce portfolio risk. We believe this portfolio strategy is an effective way to mitigate risk and increase the purchasing power of your savings. While there will always be market volatility, we believe we can reduce that volatility via this portfolio due to its balanced nature.

As of March 31, 2026, the Fund owned 24 investments. From a quality standpoint, the Fund’s investments have generally strong long-term sales growth and margins with the ability to possibly double earnings and cash flow over the next four to five years. Many of our portfolio companies generate recurring earnings and cash flow with low churn rates giving them enhanced visibility into growth and significant pricing power. Many of our portfolio companies continue to invest in their businesses to accelerate growth further. While this hurts current margins, we believe they should generate strong returns on invested capital, and the investments will accelerate further growth in the future.

While focused, the Fund is diversified by sector. The Fund’s weightings are significantly different than those of the Benchmark. For example, the Fund is heavily weighted to Consumer Discretionary businesses with 35.6% of its net assets in this sector versus 12.9% for the Benchmark. The Fund has no exposure to Energy, Materials, or Utilities. We believe companies in these sectors can be cyclical, linked to commodity prices, and/or have little if any competitive advantage. The Fund also has lower exposure to Health Care stocks at 1.9% versus 8.4% for the Benchmark. The performance of many stocks in the Health Care sector can change quickly due to exogenous events or binary outcomes (e. g. , biotechnology and pharmaceuticals). As a result, we do not invest a large amount in these stocks in this focused portfolio. In Health Care, we invest in competitively advantaged companies that are leaders in their industries such as IDEXX Laboratories, Inc. , the leading provider of diagnostics to the veterinary industry and who is benefiting from the increase in pets that people acquired during the COVID pandemic, especially as these pets age. The Fund is further diversified by investments in businesses at different stages of growth and development.

Disruptive Growth Companies

Disruptive Growth firms accounted for 35.8% of the Fund’s net assets. On current metrics, these businesses may appear expensive; however, we think they will continue to grow significantly and, if we are correct, they have the potential to generate exceptional returns over time. Examples of these companies include EV leader Tesla, Inc. , commercial satellite and launch company, Space Exploration Technologies Corp. , and audio streaming service provider Spotify Technology S. A. These companies all have large underpenetrated addressable markets and are well financed with significant equity stakes by these founder-led companies, giving us further conviction in our investment.

Core Growth Investments

Core Growth investments, steady growers that continually invest in their businesses for growth and return excess cash-flow to shareholders, represented 24.7% of net assets. An example would be FIGS, Inc. , the largest provider of scrubs and other attire to health care workers. The company continues to add new customers and increase the level of spending per customer as they add new articles of clothing and open new stores both domestically and abroad. This has allowed them to grow their addressable market and improve client retention and cash flow. FIGS continues to invest its cash flow in its business to accelerate growth further, which we believe should generate strong returns over time.

Financials Investments

Financials investments accounted for 23.9% of the Fund’s net assets. These businesses generate strong recurring earnings through subscriptions and premiums that generate highly predictable earnings and cash flow. These businesses use cash flows to continue to invest in new products and services, while returning capital to shareholders through share buybacks and dividends. These companies include Arch Capital Group Ltd. , FactSet Research Systems Inc. , and MSCI Inc.

Investments with Real/Irreplaceable Assets

Companies that own what we believe are Real/Irreplaceable Assets represent 15.5% of net assets. Vail Resorts, Inc. , owner of the premier ski resort portfolio in the world, upscale lodging brand Hyatt Hotels Corporation , and Red Rock Resorts, Inc. , the largest player in the Las Vegas Locals casino gaming market, are examples of companies we believe possess meaningful brand equity and barriers to entry that equate to pricing power over time.

Portfolio Holdings

As of March 31, 2026, the Fund’s top 10 holdings represented 64.9% of net assets. We have a long history of investing in many of these businesses across the Firm and believe they continue to offer significant appreciation potential, although we cannot guarantee that will be the case.

The top five positions in the portfolio, Tesla, Inc. , Space Exploration Technologies Corp. , MSCI Inc. , Shopify Inc. , and Verisk Analytics, Inc. , all have, in our view, significant competitive advantages due to strong brand awareness, technologically superior industry expertise, or exclusive data that is integral to their operations. We think these businesses cannot be easily duplicated and have large market opportunities to penetrate further, which enhances their potential for superior earnings growth and shareholder returns.

Top 10 holdings

Thank you for investing in the Baron First Principles ETF®. We continue to work hard to justify your confidence and trust in our stewardship of your family’s hard-earned savings. We also continue to try to provide you with information we would like to have if our roles were reversed. This is so you can make an informed judgment about whether the Fund remains an appropriate investment for your family.

Sincerely,

Ronald Baron, CEO, Portfolio Manager

David Baron, Co-President, Portfolio Manager

Michael Baron, Co-President, Portfolio Manager

References

- The Russell 3000® Index measures the performance of the largest 3,000 U. S. companies representing approximately 98% of the investable U. S. equity market. The Russell 3000® Growth Index measures the performance of the broad growth segment of the U. S. equity universe.

- The performance data in the table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemptions of Fund shares.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Form 144 Spotify Technology S.A. For: 26 May

A household using a typical amount of gas and electricity is forecast to pay about £200 more a year.

Vertiv CEO Giordano Albertazzi discusses his company’s support for tech giants in A.I. infrastructure on ‘The Claman Countdown.’

Meta’s artificial intelligence overhaul is now hitting one of the country’s largest tech corridors, with the Facebook parent company preparing to cut nearly 1,400 workers across Washington state.

New filings submitted to Washington state officials show Meta will begin terminating employees in Seattle, Bellevue, Redmond and remote positions starting July 22 as the company restructures operations around AI initiatives.

The filings provide one of the clearest looks yet at how Meta’s broader workforce overhaul is affecting employees on the ground after the company announced plans last week to eliminate roughly 10% of its workforce while shifting thousands of workers into AI-focused roles.

META THREATENS TO PULL FACEBOOK AND INSTAGRAM FROM NEW MEXICO OVER CHILD SAFETY TRIAL REQUIREMENTS

In this photo illustration, the app icons of Facebook, Messenger, Instagram, WhatsApp and Oculus VR are displayed on a smartphone screen with a Meta logo in the background. (Photo Illustration by Onur Dogman/SOPA Images/LightRocket via Getty Images / Getty Images)

Bellevue will take the largest hit, with 699 workers affected, according to the WARN notice filed Friday with the Washington State Employment Security Department. The cuts also include 259 employees across two Seattle offices, 206 workers in Redmond and another 231 remote employees statewide.

The layoffs affect a broad range of positions, including software engineers, data scientists, content designers and IT staff, underscoring how deeply Meta’s restructuring effort is reaching into its technical workforce.

“The changes we are implementing vary by team and include layoffs, open role closures, and moving thousands of employees to business critical priorities across the company,” a spokesperson for Meta said in a statement shared with FOX Business.

ZUCKERBERG SAYS META LAYOFFS TIED TO AI SPENDING, WON’T RULE OUT FUTURE CUTS

Meta is weighing significant workforce reductions as the tech giant ramps up spending on artificial intelligence infrastructure. (Getty Images / Getty Images)

Meta has emerged as one of Silicon Valley’s biggest spenders in the AI race, committing billions toward data centers, advanced chips and internal AI tools as competition intensifies with OpenAI, Microsoft and Google.

CEO Mark Zuckerberg has increasingly positioned artificial intelligence as central to the company’s future business strategy, while Meta simultaneously reduces headcount and reshapes internal teams around automation and AI-focused development.

Mark Zuckerberg, chief executive officer of Meta Platforms Inc., appears during the Meta Connect event in Menlo Park, California, on Sept. 17, 2025. (David Paul Morris/Bloomberg via Getty Images / Getty Images)

GET FOX BUSINESS ON THE GO BY CLICKING HERE

The company employed nearly 78,000 workers globally at the end of March, according to securities filings.

Workers affected by the Washington layoffs were notified May 20 and will continue receiving pay and benefits through their termination dates, according to the filing signed by Meta Chief People Officer Janelle Gale.

Fox Business’ Bradford Betz contributed to this report.

TUCSON, Ariz. — Nancy Guthrie’s disappearance remains under active investigation more than three months after she was reported missing, with the FBI and Pima County authorities continuing to review DNA evidence, surveillance footage and public tips in a case that has drawn sustained attention in Arizona and beyond.

Guthrie, the 84-year-old mother of NBC anchor Savannah Guthrie, was last seen in late January 2026 and reported missing on Feb. 1, according to earlier reporting on the case. Investigators have said they are treating the matter as a suspected abduction, but no arrest has been announced and no suspect has been publicly named.

The case has remained in the public eye because of Guthrie’s family connection and the absence of a clear resolution. Officials have continued to ask anyone with information to come forward, while investigators work through evidence collected from Guthrie’s home and the surrounding neighborhood.

Reports over the past several weeks have described a broad investigative effort that includes video analysis, DNA testing and continued follow-up on leads from the public. Authorities have said the FBI is involved in the case, and published reports indicate that forensic material recovered during the investigation has been sent for analysis.

The search has unfolded in phases. In the weeks after Guthrie disappeared, investigators canvassed the neighborhood, collected surveillance footage from nearby homes and businesses and interviewed potential witnesses. As the inquiry continued, authorities broadened the scope of the investigation to include digital records, additional video review and forensic work.

Officials have not publicly detailed every piece of evidence, but reporting has indicated that investigators are examining material from multiple cameras in the area and trying to reconstruct Guthrie’s movements before she went missing. The case has also involved DNA analysis, including data that has been received by the FBI, according to published accounts.

Law enforcement has described the investigation as active and ongoing. That means detectives and federal agents continue to review tips and compare evidence, even as the public waits for clearer answers. So far, authorities have not announced any charges or identified anyone publicly as a suspect.

The lack of a public breakthrough has fueled concern and speculation online. But officials have not confirmed the theory that a specific attack scenario has been established, and there has been no public evidence supporting claims that the case has been solved or that a particular person is responsible.

That uncertainty has created a difficult environment for Guthrie’s family and for investigators. High-profile missing-person cases often generate intense public interest, and this one has been no exception. Social media commentary and online theories have circulated widely, but authorities have continued to emphasize the importance of verified information and credible tips.

The FBI’s involvement reflects the seriousness of the case and the resources being used to try to find answers. Federal support in missing-person investigations can help with digital forensics, database checks and additional evidence review, especially when local authorities are working through a large amount of data.

As the case enters another month, the central facts remain unchanged: Nancy Guthrie is still missing, investigators are still searching for her, and no arrest has been announced. The case remains open, and authorities continue to ask the public for information that could help move the investigation forward.

One reason the case has remained so closely watched is Guthrie’s connection to Savannah Guthrie, who is one of NBC’s best-known anchors. That has brought greater media attention to the investigation and intensified public interest in developments, even when little new information has been released by law enforcement.

Still, the public record remains limited. Authorities have not confirmed a suspect, have not announced a motive and have not said whether the evidence recovered so far points conclusively to one explanation over another. In the absence of those details, investigators appear to be proceeding carefully, building the case piece by piece.

The timeline remains important. Guthrie was last seen in late January and reported missing on Feb. 1. Since then, investigators have continued to examine the home, the surrounding area and digital evidence in an effort to identify what happened in the hours before her disappearance. As time passes, investigators often face the challenge of narrowing down large volumes of footage and tip information while preserving the integrity of the case.

That process can be slow, but authorities have not indicated that the investigation has stalled. On the contrary, reporting has continued to show active evidence review, continued federal support and ongoing public outreach. In cases like this, progress often comes through small developments rather than one dramatic announcement.

Family members and supporters have also remained focused on answers. The Guthrie case has prompted sympathy, concern and renewed discussion about how long missing-person investigations can remain unresolved when there is little public evidence to share. It has also highlighted how families in the public eye can become the subject of speculation even when law enforcement has not identified wrongdoing.

For now, the status of the case is clear: Nancy Guthrie remains missing, the investigation remains open and authorities are still working through forensic and video evidence. Until investigators announce a suspect, make an arrest or release more details, the case will continue to stand as an active but unresolved missing-person investigation.

Anyone with information related to Guthrie’s disappearance has been urged to contact investigators. Officials say even small details can matter, particularly in cases where evidence is still being assembled and reviewed.

The public is likely to continue following the case closely until there is a confirmed development. For now, though, authorities have offered no public indication that the investigation is complete or that a final conclusion has been reached.

Nancy Guthrie’s disappearance remains one of the more closely watched unresolved missing-person cases in Arizona. With the FBI involved, DNA evidence under review and surveillance footage still being analyzed, investigators are continuing to search for answers while her family and the public await a breakthrough.

LOS ANGELES — Luka Doncic received his sixth career All-NBA First Team selection Monday, cementing his place among the NBA’s all-time greats at just 27 years old and marking his first such honor as a member of the Los Angeles Lakers.

The Slovenian superstar led the league in scoring during the 2025-26 season with 33.5 points per game while adding 8.3 assists and 7.7 rebounds. He shot 47.6% from the field and 36.6% from three-point range, attempting a high volume of threes that ranked second only to Stephen Curry. His selection places him in rare historical company as just the fifth player in NBA history to earn at least six First Team nods by age 27, joining Tim Duncan, LeBron James, Oscar Robertson and Bob Pettit.

Doncic received 91 First Team votes and nine Second Team votes for a total of 482 points, the fourth-highest total among all players. The honor comes in his first full season with the Lakers after a high-profile trade that paired him with James in one of the league’s most anticipated partnerships.

The 2025-26 campaign represented a career peak for Doncic in several statistical categories. He joined an exclusive group of five players — Giannis Antetokounmpo, Jaylen Brown, Luka Dončić, Nikola Jokić and Shai Gilgeous-Alexander — to average at least 25 points, 5 rebounds and 4 assists. His scoring title and consistent production made him a frequent topic in MVP discussions throughout the season, though he ultimately finished outside the top three.

This marks the latest milestone in a career defined by rapid ascent and record-breaking efficiency. Doncic has now averaged at least 25 points per game in each of his past 17 seasons played, second only to LeBron James. He also climbed the NBA’s all-time scoring list this season, further solidifying his legacy as one of the most prolific scorers in league history.

The Lakers acquired Doncic ahead of the 2024-25 season in a move designed to create a championship window around two generational talents. While the team fell short in the Western Conference semifinals this year due in part to injuries, Doncic’s individual brilliance remained undeniable. His ability to carry the offense as the primary option while sharing the court with James demonstrated his adaptability and elite basketball IQ.

Doncic’s impact extends beyond raw numbers. His playmaking vision, step-back shooting and competitive fire have drawn comparisons to some of the game’s greatest players. At 27, he already boasts a résumé that includes multiple deep playoff runs, including a trip to the NBA Finals with the Dallas Mavericks in 2024.

The All-NBA First Team this season also included Victor Wembanyama, Nikola Jokić, Shai Gilgeous-Alexander and Cade Cunningham. The selections reflect a league transitioning toward a new generation of superstars while still featuring established veterans like James and Durant.

For the Lakers, Doncic’s recognition validates the strategic decision to build around him. The franchise, which has navigated challenges in recent years, sees him as the cornerstone of future contention. His chemistry with James has shown flashes of brilliance, though injuries and roster construction have prevented sustained success so far.

League officials praised the voting results as a reflection of fan and media appreciation for consistent excellence. The All-NBA teams are selected by a global panel of 100 voters, balancing statistical dominance with overall impact on winning.

Doncic’s efficiency at high volume sets him apart. Few players in NBA history have matched his combination of scoring output and shooting accuracy over sustained periods. His eight seasons of averaging 25-plus points on 50% field goal shooting and 40% from three-point range remain unmatched in league annals.

Off the court, Doncic has embraced his role as a global ambassador for the game. His popularity spans continents, with strong followings in Europe and among international fans. The move to Los Angeles has only amplified his visibility and marketability.

Looking ahead, Doncic’s focus remains on chasing an NBA championship. While individual accolades continue to accumulate, he has repeatedly emphasized team success as his ultimate goal. The Lakers will look to bolster the roster around him and James in the upcoming offseason to create a more complete contender.

The 2025-26 season presented both opportunities and obstacles for Doncic. He shouldered a heavy workload as the Lakers’ primary offensive engine, often playing through minor injuries to keep the team competitive. His leadership and resilience earned praise from teammates and coaches.

NBA history is filled with players who achieved early greatness only to fade. Doncic’s trajectory suggests a different path. His basketball intelligence, work ethic and physical tools position him for sustained excellence well into his 30s, much like the legends he now joins in the record books.

The All-NBA selection also carries financial implications. Players on the First Team receive the maximum allowable raise under the collective bargaining agreement, providing significant long-term security.

As the league prepares for the 2026 draft and free agency, Doncic’s latest honor serves as a benchmark for excellence. Few players have matched his production at such a young age while carrying the expectations of a major market franchise.

For Lakers fans, the recognition reinforces belief in the team’s direction. Pairing two of the game’s most accomplished players creates a foundation for future success, even if the immediate results have not yet matched the hype.

Doncic’s journey from European prodigy to NBA superstar continues to inspire. His story resonates with global audiences and highlights the league’s growing international appeal. As he enters the prime of his career, the basketball world watches with anticipation for what comes next.

The 2026 All-NBA teams reflect the depth of talent across the league. With multiple superstars sharing the spotlight, individual recognition becomes even more meaningful. Doncic’s sixth First Team nod at 27 places him on a path previously traveled only by the game’s immortals.

As summer workouts begin and teams regroup, Doncic will use this latest achievement as motivation. His competitive drive and desire to win remain as strong as ever, fueling expectations for an even stronger 2026-27 campaign.

The NBA landscape continues evolving, but certain constants remain. Elite scoring, playmaking and leadership will always be prized. In Luka Doncic, the league has one of its finest current examples of those qualities, now officially recognized once again among the very best.

Business

Electricity Generating Public Company Limited (EYGPF) Presents at SET Digital roadshow Q1/2026 – Slideshow

Electricity Generating Public Company Limited (EYGPF) Presents at SET Digital roadshow Q1/2026 – Slideshow

Thailand and China have significantly boosted cooperation in trade, investment, transport, and security. Key discussions in 2025 included high-speed rail and EVs. This intensified partnership follows their golden jubilee, with a royal visit underscoring China’s strategic importance.

Key Points

- Thailand and China have strengthened cooperation across trade, investment, transport, and security.

- Key areas of focus include high-speed rail, the digital economy, EVs, and combating scam networks, reflecting an expanded bilateral relationship.

- This renewed momentum follows the 50th anniversary of diplomatic ties in 2025 and a significant royal visit to China, underscoring Beijing’s strategic importance.

Deepening Bilateral Engagement

Thailand and China have significantly intensified their cooperation across a broad spectrum of areas in recent years. Beyond traditional diplomatic channels, the two nations have prioritized advancements in trade, investment, and transport connectivity. Key discussions in 2025, for instance, focused on ambitious projects such as high-speed rail, the burgeoning digital economy, and the promotion of electric vehicles. Furthermore, a critical aspect of this strengthened partnership involves collaborative efforts to combat transnational scam networks, demonstrating a shared commitment to addressing contemporary global challenges. This multifaceted approach underscores the evolving and comprehensive nature of the bilateral relationship.

Catalysts for Enhanced Cooperation

The robust engagement between Thailand and China in 2025 has been propelled by a period of heightened symbolic and political interactions. The 50th anniversary of diplomatic ties, celebrated in 2025, served as a significant milestone, underscoring the long-standing relationship. This was further amplified by a historic royal visit from Thailand to China later that same year. This royal delegation underscored China’s strategic importance within Thailand’s foreign policy and its integral role in the nation’s economic strategy, providing substantial impetus for the deepening of bilateral ties and collaborative initiatives.

Expanding Horizons of Partnership

The burgeoning relationship between Thailand and China extends far beyond conventional diplomatic exchanges, reflecting a shared vision for future development and security. The focus on infrastructure projects like high-speed rail is poised to revolutionize connectivity, facilitating greater economic integration and people-to-people exchange. Moreover, the concerted efforts in the digital economy and electric vehicles signal a mutual commitment to embracing technological innovation and sustainable growth. The joint endeavors to dismantle transnational scam networks highlight a pragmatic and proactive approach to maintaining regional stability and protecting citizens. This diverse and expanding cooperation is setting a new paradigm for bilateral relations.

Other People are Reading

Violence erupts as police intervene in clash before Conference League final

Auxier Spring 2026 Market Commentary (Mutual Fund:AUXFX)

ETF Flows, Institutions Accelerate Crypto Adoption

-

Crypto World5 days ago

Crypto World5 days agoBlockchain.com files with SEC for U.S. IPO

-

Fashion4 days ago

Fashion4 days agoHoliday Weekend Open Thread – Corporette.com

-

Business4 days ago

Business4 days agoDell Technologies DELL Stock Surges 15% on AI Server Momentum and Analyst Upgrades in 2026

-

Crypto World5 days ago

Crypto World5 days agoBitcoin Accumulation Weakens as BTC Realized Losses Hit $600M

-

Crypto World4 days ago

Crypto World4 days agoRobinhood crypto COO Tanya Denisova exits

-

Crypto World4 days ago

Crypto World4 days agoSpace X IPO Is ‘Bad News’ for Tech Stocks: But What About Bitcoin?

-

Politics4 days ago

Politics4 days agoMakerfield: a tale of two social-media histories

-

Business2 days ago

Business2 days agoNYT Strands Answers May 24 2026 Revealed for Puzzle No. 812 Theme Summer Essentials

-

Tech1 day ago

Tech1 day agoMicrosoft’s quiet Claude Code retreat and the real cost of enterprise AI

-

Crypto World5 days ago

Crypto World5 days agoMicroStrategy’s Saylor Says Miners No Longer Set Bitcoin Price, Another Force Has Taken Over

-

Tech5 days ago

Tech5 days agoWhatsApp ads could make Irish debut after discussions with DPC

-

Tech4 days ago

Tech4 days agoA 0.12% parameter add-on gives AI agents the working memory RAG can’t

-

Crypto World4 days ago

Crypto World4 days agoAI infrastructure race heats up as IREN pitches full-stack strategy, WhiteFiber lands $160M deal

-

Tech5 days ago

Tech5 days agoYou Can Now Add ChatGPT To PowerPoint

-

NewsBeat5 days ago

NewsBeat5 days agoCharity run by Reform leader Malcolm Offord accused of ‘law breaking’ over Scottish registration

-

Business5 days ago

Business5 days agoTrump Invests $1M-$5M in Kura Sushi USA Chain With 27 California Locations

-

Crypto World2 days ago

Crypto World2 days agoNvidia (NVDA) CEO Calls on Super Micro to Strengthen Export Controls Amid Smuggling Probe

-

Sports5 days ago

Sports5 days ago2026 CJ Cup Byron Nelson leaderboard: Brooks Koepka finds putting stroke in Round 1

-

Tech1 day ago

Tech1 day agoWestone Audio and Etymotic Acquired by Fidelity Collective in Major IEM Market Move

-

Crypto World6 days ago

Crypto World6 days agoExa Labs raises $250 million in funding led by a16z

You must be logged in to post a comment Login