Crypto World

21Shares Hyperliquid ETF Hits $14M Volume Days After Debut

TLDR

- The 21Shares Hyperliquid ETF recorded a rapid increase in daily trading volume within days of its launch.

- The ETF’s turnover rose from about $1.8 million on its first day to nearly $14.08 million.

- The surge represents a 682% increase in trading activity over a short period.

- Bloomberg analyst Eric Balchunas said the growth reflects strong organic investor demand.

- The ETF’s share price has climbed more than 20% since its launch, rising above $28.

- The fund provides direct exposure to the Hyperliquid ecosystem through HYPE token backing.

The 21Shares, Hyperliquid ETF has recorded a sharp rise in trading activity within days of its debut. Daily turnover climbed to about $14.08 million, up from roughly $1.8 million on launch day. The ETF has also posted a price gain of over 20% since it began trading.

21Shares, Hyperliquid ETF Trading Volume Jumps After Launch

Bloomberg ETF analyst Eric Balchunas highlighted the rapid growth in trading volume in a recent post. He said the increase reflects strong organic demand from market participants.

The ETF launched on May 12 with an opening-day volume of about $1.8 million. Trading activity has since risen to around $14.08 million per day.

This represents a 682% increase in turnover over a short period. The rise shows continued investor engagement rather than a short-term spike.

Balchunas stated that higher volume supports improved liquidity for the ETF. He added that sustained trading activity often indicates stable investor interest.

The ETF initially trailed other crypto-linked launches in early volume. Bitwise’s Solana Staking ETF recorded about $56 million on its first day.

Despite this gap, market participants viewed the debut as a solid start. Volume growth in the following days has strengthened that view.

The ETF’s share price has also moved higher since launch. It rose 20.39% from about $23.49 to above $28.28.

Hyperliquid Ecosystem Gains Attention as Institutional Interest Grows

The 21Shares Hyperliquid ETF provides exposure to the Hyperliquid ecosystem. Each share is backed by HYPE tokens held by the issuer.

21Shares set the ETF’s management fee at 0.30%. This rate is slightly lower than Bitwise’s competing product at 0.34%.

Hyperliquid has gained traction in the crypto derivatives market. The platform leads in on-chain perpetual futures trading activity.

The HYPE token currently ranks among the top cryptocurrencies by market value. It holds an estimated valuation of $12.95 billion.

Institutional interest has also expanded in the ecosystem. Goldman Sachs recently disclosed a position linked to Hyperliquid.

The bank acquired 654,630 shares of Hyperliquid Strategies Inc. The purchase was valued at about $3.3 million at the time.

Hyperliquid Strategies is a Nasdaq-listed digital asset treasury firm. It focuses on investments tied to the Hyperliquid ecosystem.

Goldman Sachs reduced exposure to XRP and Solana before this move. The filing shows a shift toward assets linked to Hyperliquid. At the time of writing, the ETF continues to record daily trading volumes near $14 million.

AI Financial, formerly known as Alt5 Sigma, wants the market to know that it’s more than just its token holdings, and calling it a WLFI treasury company isn’t the right way to describe it.

“AiFi continues to operate an active fintech and digital payments business while executing on a broader long-term strategy across digital assets, settlement infrastructure, tokenization, and next-generation financial technologies,” a company spokesperson told CoinDesk in an email. “Characterizing the company solely as a ‘treasury company’ does not accurately reflect the breadth of AiFi’s operating business.”

AI Financial operates ALT5 Pay, its crypto payments platform, and ALT5 Prime, its over-the-counter digital asset trading business. Since quarter-end, it has also announced the acquisition of tokenization and ICO infrastructure firm Block Street, signed a commercial agreement with SuperQ Quantum, and outlined broader expansion into digital financial infrastructure.

The response from the spokesperson comes after AI Financial’s latest SEC filing painted a starkly different picture of its current financial profile.

The Nasdaq-listed company disclosed in this filing that it held 7.28 billion WLFI tokens, worth $706.4 million at the end of March, down from an acquisition cost of roughly $1.46 billion. By comparison, its operating fintech business generated just $4.7 million in quarterly revenue.

AI Financial also warned in this filing that recurring losses and a $5.5 million working capital deficit raise “substantial doubt” about the company’s ability to continue as a going concern within one year after the financial statements were issued.

Complicating the picture further, the company’s WLFI holdings remain contractually locked, limiting its ability to convert its largest asset into cash. AI Financial ended the quarter with just $10.5 million in cash.

AI Financial’s relationship with WLFI goes far beyond ownership. World Liberty CEO Zach Witkoff serves as the company’s chairman. Co-founder Zachary Folkman sits on its board; WLFI has lent it $15 million, secured by WLFI tokens, and WLFI holds rights equivalent to roughly 46% of its fully diluted equity.

But the question is, can investors see past WLFI when looking at AI Financial as a whole?

AI Financial may be building a broader fintech and digital infrastructure platform, but its SEC filing suggests WLFI remains the asset defining its financial story.

Unlike a typical digital asset treasury company holding bitcoin or another liquid asset, AI Financial’s relationship with WLFI is more complex: the issuer of its core treasury asset also has deep governance, lending and equity ties to the company itself.

The Digital Asset Market Clarity Act just cleared its hardest committee test. If it becomes law, it ends the single most damaging fact of life for American crypto: not knowing who is in charge. But the version that reaches President Trump’s desk will be shaped by three fights still being waged in the Senate, and the outcome of those fights decides who wins and who loses.

Summary

- The Senate Banking Committee advanced the CLARITY Act in a 15 to 9 vote, moving the crypto market structure bill closer to a full Senate vote.

- The proposal would divide digital assets into categories overseen by the SEC and CFTC, while also creating a separate framework for payment stablecoins.

- Ethics rules tied to President Donald Trump’s crypto connections, stablecoin yield limits, and anti-money laundering provisions remain among the biggest unresolved issues before the bill can reach the White House.

The restaurant with two inspectors

Imagine running a restaurant where the health inspector and the fire marshal both insist your kitchen is theirs to police. Neither will put their rules in writing. And if you guess wrong about whose instructions to follow, the penalty is that they shut you down and sue you.

That, more or less, has been the experience of building a crypto company in the United States since around 2017. The Securities and Exchange Commission and the Commodity Futures Trading Commission have spent the better part of a decade in an unresolved turf war over digital assets, and the industry has lived in the gap between them. Tens of billions of dollars in fines have been paid. Founders have spent years in litigation just to extract an answer that regulators could have written down in advance. Most builders simply gave up and left, for Dubai, Singapore, Switzerland, anywhere a straight answer arrived in less than three years.

The Digital Asset Market Clarity Act, universally shortened to the CLARITY Act, is Washington’s most serious attempt to end that era. And after months of stalemate, it just took its biggest step forward yet. On May 14, 2026, the Senate Banking Committee voted 15-9 to advance the bill to the Senate floor, with two Democrats crossing party lines to join every Republican on the panel.

That vote was not the finish line. It was the moment the bill stopped being a wishlist and became real legislation with a credible path to law. For anyone who trades, builds, invests in, or simply holds digital assets, the question is no longer whether to pay attention. It’s what, concretely, changes if this thing passes, and what the unresolved fights still being waged in the Senate will mean for the version that actually becomes law.

This is a long answer to that question.

What the bill actually does: three boxes, two regulators

Strip away the acronyms and the 270-plus pages, and the CLARITY Act does one structurally simple thing. It sorts every digital asset into one of three categories and assigns each category to a regulator.

Digital commodities. A token whose value comes from a functioning, sufficiently decentralized blockchain, where the network does something real and the token is the fuel that powers it. Bitcoin and Ether are the obvious cases, and both are widely expected to land here, formalizing what has been their de facto treatment for years. Digital commodities fall under the CFTC.

Investment contract assets. A token is sold the way startup equity is sold, where a centralized team raises money from the public and promises to build something with it. These stay with the SEC, which is where that agency has always had its firmest legal footing.

Permitted payment stablecoins. Dollar-pegged tokens designed to actually move money. These get a separate category with joint SEC and CFTC oversight, building on the GENIUS Act stablecoin framework that passed earlier.

Three boxes. Two regulators. The biggest reduction in legal fog the American crypto industry has ever been offered.

The mechanics behind that simple structure are what make the bill consequential. The CLARITY Act gives the CFTC exclusive jurisdiction over the spot and cash markets for digital commodities, which is a dramatic expansion for an agency that has historically referred to derivatives rather than the underlying assets themselves. Exchanges, brokers, and dealers handling digital commodities would register with the CFTC through a new, purpose-built pathway, instead of trying to force themselves into securities rules written in 1933 and 1934 for a very different kind of asset.

The SEC, in turn, keeps authority over genuine securities offerings. The bill draws a line, in federal statute, between the moment a token is being sold as a fundraising instrument by a centralized team and the moment the underlying network has matured enough that the token trades as a commodity. That maturation test, the question of when a project becomes “decentralized” enough to graduate from SEC to CFTC oversight, is one of the most legally intricate parts of the bill, and one of the most important.

For developers, there’s a provision that may matter more than the jurisdictional sorting itself: protection for people who write open-source code but never have custody of user funds. Under the CLARITY Act, publishing a smart contract would stop being treated as the legal equivalent of running an unlicensed money-transmitting business. For a corner of the industry that has watched developers face personal legal exposure simply for shipping code, this is foundational.

What approval would mean, by who you are

A regulatory framework is not an abstraction. It lands differently depending on where you sit in the ecosystem. Here is the concrete picture.

If you are a developer or founder

The immediate change is the disappearance of a specific, paralyzing fear: that building in the open is itself a legal risk. A clear registration pathway means a US-based project can launch knowing which agency it answers to and what compliance looks like, rather than discovering the answer through an enforcement action two years later.

The decentralization maturity test gives projects something they have never had, which is a roadmap. A token can begin its life under SEC oversight as an investment contract asset and, as its network decentralizes, move into the digital commodity category. That transition used to be a matter of speeches, blog posts, and hope. Putting it into statute means a founder can plan around it.

The likely practical effect is repatriation. A meaningful share of the talent and capital that decamped to friendlier jurisdictions did so for one reason: those places offered a straight answer. Remove that disadvantage, and the math on building in the US changes.

If you are an exchange, broker, or custodian

For the largest US platforms, the bill turns an existential ambiguity into an operational task. Instead of litigating whether the assets they list are securities, exchanges would register with the CFTC and operate under a defined rulebook. The bill includes an expedited registration process and provisional status, so platforms are not frozen out while the CFTC builds its full framework.

This is a double-edged outcome. Clarity is not the same as leniency. A registered exchange will face real, enumerated obligations: custody standards, disclosure requirements, conduct rules, and capital expectations. The era of regulatory vapor ends, but so does the era of regulatory absence. Compliance will have a cost. The industry’s bet is that a known, payable cost beats an unknowable, unbounded legal risk. For most serious operators, that bet is obviously correct.

If you are a retail investor or token holder

The benefits here are real but slower and less glamorous. Defined disclosure requirements for token issuers mean better information before you buy. Custody and conduct rules for registered intermediaries mean more protection for assets you hold on a platform. The legal status of the assets in your wallet becomes a settled question rather than an open one.

There’s also a subtler consequence. A credible US framework is the precondition for the next wave of institutional products, and for traditional financial institutions to offer crypto services to ordinary customers without regulatory peril. Approval doesn’t put crypto in your bank tomorrow. It removes the biggest single obstacle standing between today and that future.

If you hold or use stablecoins

This is where the bill’s politics get sharp, and the detail matters. The compromise negotiated by Senators Thom Tillis and Angela Alsobrooks draws a careful line. Intermediaries, exchanges, for instance, would be prohibited from paying yield on a customer’s idle, passive stablecoin holdings. The intent is explicit: a passive stablecoin balance must not be allowed to function like an interest-bearing bank deposit. But the same provision permits rewards tied to activity, meaning incentives connected to actually spending or using a stablecoin, as long as they don’t resemble passive interest.

If that distinction sounds narrow, it is. It’s also the fault line over which this entire bill nearly collapsed, and it explains a fight covered in the next section.

The three fights that will shape the final bill

The version of the CLARITY Act that passed committee is not the version that will become law. Three contested issues remain open, and each one will shape who benefits and by how much. Anyone trying to understand what approval “means” has to watch these, because the answer is still being written.

Fight one: ethics, and the shadow of the Trump family

This is the single biggest political wedge between the bill and final passage. Many Senate Democrats are demanding an ethics provision barring senior government officials from holding business ties to the crypto industry, a demand driven, unambiguously, by President Trump’s family’s extensive crypto ventures, including the World Liberty Financial project.

Republicans on the Banking Committee declined to include such language in the committee bill, arguing that ethics sits outside the committee’s remit and can be added later by floor amendment. The committee specifically voted down a Democratic ethics amendment. That rejection is the most direct explanation for why most Democrats voted no.

The arithmetic makes this unavoidable. On the Senate floor, the bill needs 60 votes. Assuming every Republican supports it, that means roughly seven Democrats have to come along. Crypto-friendly Democrats, including Senators Kirsten Gillibrand and Ruben Gallego, have stated plainly that they won’t provide those votes without an ethics provision. Industry advocates now describe some form of ethics language as “almost all but guaranteed” to be added before a floor vote.

But there’s a counter-pressure pulling the other way. Senator Cynthia Lummis, a key negotiator, warned that the President himself has to sign off, and that if the bill becomes, in her words, a cudgel aimed specifically at him, he’ll veto it without hesitation. The realistic landing zone is therefore an ethics provision strong enough to win seven Democratic votes but weak enough to survive a presidential signature. That’s a narrow target, and where exactly the language lands will tell you a great deal about how seriously the final law treats conflicts of interest.

Fight two: illicit finance and law enforcement

A coalition of law enforcement groups argues the bill doesn’t do enough to stop digital assets from being used in financial crime, and would make catching bad actors harder. The concern gained urgency from a Treasury FinCEN advisory flagging crypto platforms and stablecoins as a channel for sanctioned actors to launder illicit proceeds.

Senators have filed amendments to strengthen anti-money-laundering and sanctions provisions. Backers of the bill counter that it actually strengthens AML and sanctions rules and gives law enforcement better tools. How this gets resolved affects the compliance burden on every registered intermediary, and the bill’s credibility with the national-security-minded senators whose votes are in play.

Fight three: the banks

America’s banking industry is the bill’s most powerful organized opponent, and its objection is

fundamentally about deposits. If stablecoins can pay anything resembling yield, banks fear money will drain out of deposit accounts, the same deposits that fund lending. In the days before the committee vote, bank trade groups reportedly sent more than 8,000 letters to senators demanding revisions. Even after the Tillis-Alsobrooks compromise, banking groups complain the activity-rewards language leaves room for workarounds.

This is not a sideshow. It’s a genuine clash between two financial industries over the future shape of money, and the banks have decades of lobbying infrastructure behind them. The final stablecoin language will be one of the most negotiated paragraphs in the entire bill.

The road from here

Even on an optimistic reading, the CLARITY Act has several gates left to clear.

First, the Senate Banking Committee bill has to be merged with a parallel version produced by the Senate Agriculture Committee, since the two panels share jurisdiction over digital assets, into a single unified text. Industry insiders expect intense negotiation over the next several weeks, and this is the most likely vehicle for inserting the ethics compromise.

Second, the merged bill faces a full Senate floor vote requiring 60 senators.

Third, because the House passed its own version of the CLARITY Act back in July 2025, any Senate- passed bill containing new components, such as the stablecoin yield language, the DeFi provisions, or ethics rules, has to be reconciled with, or accepted by, the House before it can go to the President.

The timeline is genuinely tight. White House officials have floated a target of a signing on or around July 4, 2026. Industry advocates describe an effective “drop-dead deadline” before the August recess, after which the midterm elections and a potentially less crypto-friendly Congress raise the degree of difficulty considerably. Prediction markets have put the odds of passage in 2026 in the rough vicinity of two-in- three, while at least one Wall Street analyst has been more cautious, calling a successful floor vote “in play but not the expected outcome.”

In other words: reachable, not guaranteed.

What it means, in the end

It’s worth being precise about the nature of what is on offer here, because both boosters and skeptics tend to overstate it.

The CLARITY Act is not a gift to the crypto industry. It’s a rulebook. It hands the industry the thing it has asked for over and over, a definitive answer to “who regulates this?”, and the price of that answer is a genuine, enforceable obligation. Exchanges will register. Issuers will disclose. Intermediaries will be examined. For an industry that has at times romanticized its own lawlessness, the deepest meaning of approval is that the era of operating in the absence of rules ends, and the era of operating under them begins.

For the United States as a whole, the bill is a bet that a clear domestic framework will pull

Builders, capital, and talent back home, and that the alternative, ceding the next decade of financial infrastructure to other jurisdictions, is the worst outcome.

And for the ordinary participant, the developer shipping code, the trader on an exchange, the person holding a stablecoin, the change is less a single dramatic event than the removal of a decade-long background hum of uncertainty. The legal status of the asset in your wallet becomes a settled fact. The platform you use answers to a named regulator. The developer who wrote the protocol is not a criminal for having written it.

That’s what crypto purgatory ending actually looks like. Not paradise. Just, finally, a map.

The committee’s vote on May 14 was the moment the map stopped being a rumor. The next two months, the merged text, the ethics deal, the floor math, and the House vote will decide what the map actually says. Watch the floor math. Watch the ethics negotiations. And when the merged text lands, read it. The details are the story now.

This article is for informational purposes and does not constitute legal, financial, or investment advice. Legislative situations evolve quickly; the status described reflects developments as of mid-May 2026.

Bitcoin has hit resistance at its 200-day moving average and is showing signs of a trend reversal, according to CryptoQuant on Wednesday. The move closely mirrors a March 2022 pattern where a 43% rally stalled at the same level before prices declined further.

“Overall, Bitcoin demand has flipped into contraction,” the analyst wrote.

The platform’s “Bull Score Index” has declined from 40 back to extreme bearish territory at 20, “as stalling stablecoin liquidity, and negative price momentum simultaneously eroded the composite signal.”

This score is consistent with the deep bear market readings of February and March, when prices declined to $60,000, and historically “has preceded either further price weakness or extended consolidation,” they added.

Bitcoin Correction Likely to Continue

If the correction continues, the $70,000 level represents the primary on-chain support target, the traders’ on-chain realized price. The analysts noted that this level has functioned as a “precise inflection point” throughout the current bear market cycle.

A break below this back into the $60k zone could result in new bear market lows, however. Meanwhile, Glassnode reported on Wednesday that Bitcoin has reclaimed the True Market Mean at $78,300 but failed to sustain above it. However, it also noted that the correction from recent highs is likely to continue if previous cycle patterns repeat.

“Any deeper correction from current levels would therefore reframe the recent rally as a local top within the ongoing bear market, a structure that has recurred multiple times in prior cycles and remains the higher probability outcome until price demonstrates sustained follow-through.”

Bitcoin momentum has faded from full max momentum, reported Swissblock on Thursday. It remained cautiously bullish, stating that as long as momentum does not degrade significantly, “the base case is consolidation, not breakdown.”

Bitcoin momentum has faded from full max momentum.

But as long as it does not fall below -0.5, this does not imply breakdown.

What usually follows is consolidation.

The key reference is June–July 2025.

Momentum faded from full strength, but the indicator never broke below… https://t.co/QkVFmMTReb pic.twitter.com/ZarKY77Bx3

— Swissblock (@swissblock__) May 21, 2026

Crypto Market Outlook

Bitcoin has climbed steadily over the past 24 hours, gaining 1.7% from $76,600 to tap $78,000 twice during the Thursday morning Asian trading session.

However, this level is also a resistance zone that needs to be overcome quickly for BTC to reach $80,000 again. Volumes and sentiment suggest it will be thwarted here again.

Ether prices have mirrored the move, but it remains bearish under $2,150 at the time of writing, while the altcoins were notching larger gains. Hyperliquid and Zcash had exploded with double-digit gains on the day.

The post Bitcoin’s Key Resistance Stall Could Send it Tumbling Much Lower: Analysts appeared first on CryptoPotato.

Anthropic is on track to generate $10.9 billion in second-quarter revenue, more than doubling its first-quarter haul.

The figure puts the artificial intelligence (AI) company on track for its first quarterly operating profit.

Anthropic Q2 Revenue Set To Double

According to The Wall Street Journal, Anthropic shared the numbers with investors as part of an ongoing funding round that could lift its valuation past OpenAI’s.

“The projections, which were reviewed by The Wall Street Journal, provide a window into the meteoric rise of a startup that was once a laggard in the artificial-intelligence race, and defy the conventional wisdom that AI companies’ huge spending needs hamper near-term profitability,” the report read.

The Claude maker expects to post an operating profit of $559 million in the June quarter. First-quarter revenue reached $4.8 billion, meaning sales more than doubled within months.

Follow us on X to get the latest news as it happens

The firm has posted strong gains this year, and investor talks are underway on a funding round pegged at a $900 billion valuation. That price would lift Anthropic above OpenAI, which was last valued at $852 billion during a March funding round.

Meanwhile, rival OpenAI has faced setbacks this year. The maker of ChatGPT missed internal revenue and weekly user targets in early 2026.

Even so, the company has pushed ahead with its IPO plans. OpenAI is working with Goldman Sachs and Morgan Stanley on a confidential S-1 filing that could land as early as Friday. Anthropic itself is weighing a public listing as soon as October.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Anthropic Eyes First Profitable Quarter on $10.9 Billion Q2 Revenue Projection appeared first on BeInCrypto.

Ontop has partnered with OpenTrade to launch a ~3% APR rewards product on USD balances for thousands of global workers, converting idle payroll funds into yield in under a month.

Summary

- Ontop launches ~3% APR rewards on USD balances for global workers

- OpenTrade provides plug-and-play institutional-grade yield and infrastructure

- Pilot hit $1m in two weeks, now $3m+ in user funds under management

The move shifts Ontop from a pure payroll and payments provider toward a broader financial platform for distributed teams worldwide.

Global workforce platform Ontop has rolled out a ~3% APR rewards program on USD balances held in its Global Account, powered by OpenTrade’s stablecoin and fiat yield infrastructure, after processing more than $1 billion in payroll to workers across 150+ countries in 2025. The new product targets one of the largest pools of idle capital in fintech — uninvested payroll sitting between pay cycles — by allowing Ontop’s global users to earn rewards on their USD while mitigating inflation, currency devaluation, and repatriation risk, regardless of jurisdiction.

The partnership is explicitly designed to be plug-and-play for Ontop’s existing stack. OpenTrade handled legal structuring, portfolio management, and automated reporting, enabling Ontop to bring the ~3% APR rewards product from concept to launch in under a month with “no material operational lift.” According to the companies, the program is fully embedded into the Ontop Global Account, so users experience it as a native feature rather than a separate investment product or external platform.

Turning idle balances into yield and revenue

The initial pilot for the rewards product went live in December 2025 with 1,300 users and reached $1 million in user-provided funds in less than two weeks, before scaling to Ontop’s full customer base. Total user-provided funds now exceed $3 million, with OpenTrade’s APIs wired directly into Ontop’s reporting systems to provide real-time, daily visibility into balances and performance. All activity takes place within the existing Global Account, positioning it as a single financial home where remote workers can get paid, store capital, move it, and now earn yield.

For Ontop, the integration also opens a new revenue line beyond subscription and payroll processing fees. The company now captures a margin on the balances it allocates to OpenTrade’s infrastructure, effectively evolving from a pure payroll and payments platform into a financial operating system for global teams — without building an in-house treasury stack or taking on additional operational overhead. Fixed-term products, which would likely offer different yield and duration profiles, are already in development and scheduled to launch in the coming weeks.

OpenTrade COO Jeff Handler framed the partnership as an example of how fintechs still reliant on legacy rails can access institutional-grade yield without re-architecting their core systems. In comments to crypto.news, he said: “the majority of the fintech world still runs on dollars in traditional bank accounts that moves on traditional banking rails, but that shouldn’t be a barrier to accessing plug-and-play institutional-grade yield,” Handler said. “Our ability to meet Ontop where they’re at operationally, without requiring them to rebuild their infrastructure, is exactly what OpenTrade was designed to do.”

Building a financial OS for global workers

Ontop co-founder Julian Torres positioned the rewards launch as central to the company’s broader thesis that financial infrastructure has failed to keep pace with the globalisation of work. “At Ontop, we’re building the financial infrastructure for the global workforce. The future of work is global, but financial systems haven’t caught up,” Torres said. “Through our Global Account, we’re not just helping workers get paid, we’re giving them a place to store, move, and grow their money. Our partnership with OpenTrade is a key step in turning idle balances into real financial opportunity anywhere in the world.”

OpenTrade, backed by Circle and a16z Crypto, describes itself as institutional-grade yield infrastructure for fintechs, neobanks, and payroll providers, with more than $268 million in transaction volume processed to date and asset management operations overseen by Five Sigma Finance, a UK-regulated manager supervising over $6 billion for institutional clients. Ontop, meanwhile, positions its Global Account and payroll stack as a comprehensive solution for companies hiring and paying distributed teams, using the new rewards layer to deepen engagement and differentiate in an increasingly crowded global employment and contractor-payments market.

Morgan Stanley has resubmitted a spot Solana ETF application that would hold and stake SOL under the ticker MSOL, extending the bank’s push deeper into U.S. crypto exchange-traded products.

Summary

- Morgan Stanley’s revised S-1 says the trust will hold SOL directly and reflect staking rewards in net asset value.

- The filing places Solana alongside the bank’s expanding crypto ETF lineup, including its recently launched MSBT Bitcoin ETF.

- Solana was priced at $84.91 on crypto.news at the time of reporting.

Morgan Stanley has filed a revised registration statement for a spot Solana (SOL) exchange-traded fund, a product that would trade under the ticker MSOL and hold SOL directly while staking part of the fund’s assets through third-party providers. The filing shows the bank is not merely seeking passive price exposure but wants staking rewards to accrue inside the product itself, a structure that could differentiate it from simpler spot vehicles.

The fund is formally structured as the Morgan Stanley Solana Trust, and the preliminary prospectus says its investment objective is to track the performance of SOL in U.S. dollars, adjusted for expenses and liabilities, while also reflecting rewards from staking a portion of the trust’s SOL. The same filing says the sponsor plans to choose staking providers based on “performance, reliability, and reputation,” including “uptime and slashing history.”

Morgan Stanley’s earlier crypto ETF expansion gives the filing broader significance. In a previous crypto.news story, the bank’s move into Bitcoin and Solana ETFs was described as evidence that digital assets had gone “from compliance headache to boardroom strategy” as regulatory guardrails tightened.

Filing details

The prospectus states that the trust is a passive investment vehicle and “will not utilize leverage, derivatives or any similar arrangements” in pursuing its objective. It also says the trust intends to hold SOL in custody with regulated third-party custodians and may distribute staking rewards at least quarterly when required under current Internal Revenue Service guidance.

Morgan Stanley’s language is unusually explicit about why investors might want the structure. The filing says the trust is meant to provide access to SOL “through a traditional brokerage account without the potential barriers to entry or risks involved with holding or transferring SOL directly.” That is the pitch in plain English: exposure without private keys, wallets, or direct on-chain handling.

The filing also includes a notable market data point. As of Dec. 20, 2025, SOL had a total market capitalization of about $70.54 billion and ranked as the seventh-largest digital asset by market capitalization, according to CoinMarketCap data cited in the prospectus.

Broader push

The Solana filing follows Morgan Stanley’s broader push into crypto-linked products. Another crypto.news story reported that the bank’s spot Bitcoin ETF, MSBT, was set to begin trading on NYSE Arca on April 8 with a 0.14% fee, entering a market where BlackRock’s IBIT and Fidelity’s FBTC had already pulled in more than $74.3 billion in net inflows since launch.

That matters because MSOL is not an isolated filing but part of a coordinated buildout across spot crypto products. Crypto.news also reported in another story that Morgan Stanley had expanded crypto investment access across all clients and account types, reinforcing the idea that the bank now sees digital assets as a mainstream wealth product rather than a niche alternative.

At the time reflected on crypto.news pricing pages, Bitcoin (BTC) traded at $77,450.00 and Ethereum (ETH) at $2,130.03, while Solana changed hands at $84.91. If approved, MSOL would give Morgan Stanley a direct way to package that Solana exposure into a regulated, exchange-traded wrapper built for traditional investors.

Bitcoin’s recovery from February lows, which had begun to look like a new bull run, hit a wall last week at the 200-day simple moving average (SMA) positioned just above $82,000. Since then, prices have pulled back to $77,500 in a move reminiscent of 2022 when a 43% relief rally failed at the same indicator before bitcoin resumed its decline.

Analytics firm CryptoQuant’s latest report offers a compelling explanation for why the rally failed to break through the critical average, a long-term trend line traders often treat as the dividing line between a bear-market bounce and a real recovery.

The bigger issue is demand.

CryptoQuant says the April and early May rally had been supported by three things: leveraged futures buying, spot demand, and U.S. ETF inflows. All three have now weakened. The firm’s Bull Score Index has fallen from 40 to 20, a level the firm calls “extremely bearish” and one that matched the February-March period when bitcoin traded between $60,000 and $66,000.

The clearest cross-check is the Coinbase bitcoin premium, which has remained negative through much of the May rally and the subsequent correction, CryptoQuant points out in the report.

The premium measures whether bitcoin is trading higher on Coinbase than on offshore venues; a positive reading is treated as a sign of relatively stronger U.S. demand, a negative reading as evidence that U.S. investors aren’t paying up for exposure.

U.S. spot bitcoin ETFs have flipped into sellers to match. Weekly data from SoSoValue shows the products lost about $979.7 million in the week ended May 19, on top of roughly $1 billion of outflows the prior week. The reversal follows six straight weeks of inflows that helped fuel the rally.

Is there any demand at all?

Korea’s kimchi premium, which measures demand for BTC on Korean exchanges, has dropped below zero, according to CryptoQuant data, meaning there’s no above-normal demand on exchanges in the country.

Elsewhere in Asia, Hong Kong’s three spot bitcoin ETFs, run by ChinaAMC, Bosera Hashkey, and Harvest, have rarely cleared a few million dollars in combined daily volume through May.

If the correction deepens, CryptoQuant identifies $70,000, the traders’ on-chain realized price, as the next major on-chain support. That level capped rallies in October and January. This time, it would have to hold them up.

Terraform Labs’ liquidators have accused Jane Street of insider trading that allegedly netted $134 million during the May 2022 Terra/LUNA implosion, claiming the trading giant front‑ran the depeg using non‑public information while retail investors were wiped out.

Summary

- The court-appointed administrator says Jane Street used confidential data and private Telegram coordination to dump UST ahead of the collapse.

- The lawsuit alleges roughly $134 million in illicit profit from trades executed during a “death spiral” that erased around $40 billion in market value.

- Jane Street has moved to dismiss the case, calling the complaint “self‑defeating” and a “desperate effort” to shift blame for Terraform’s fraud.

The administrator winding down Do Kwon’s Terraform Labs has filed a federal lawsuit accusing Jane Street, its co‑founder Robert Granieri, and traders Bryce Pratt and Michael Huang of insider trading tied to the May 2022 Terra collapse.

Terraform liquidator targets Jane Street over May 2022 trades

According to the complaint, filed in the Southern District of New York and reviewed by the Financial Times, Jane Street “used material, non‑public information obtained from Terraform insiders to front‑run market‑moving events” and exit positions while ordinary investors were left holding collapsing UST and LUNA.

The complaint alleges that Jane Street coordinated its UST trades “through a private Telegram chat” and executed an “85 million UST” sale on May 7, 2022, minutes after confidential instructions were given to withdraw liquidity from a key pool. Terraform’s plan administrator claims those trades formed part of a broader scheme that generated “approximately $134 million in unlawful profits” as Terra’s algorithmic stablecoin lost its peg and the ecosystem unraveled in a matter of days.

In detailing the fallout, the lawsuit places Jane Street’s trading squarely inside one of crypto’s most destructive episodes, describing Terra’s failure as a “$40 billion collapse” that triggered cascading liquidations and contributed to a wider credit crunch across digital asset markets. Crypto.news has previously reported on the long legal afterlife of that implosion, including civil and criminal actions targeting Terraform, Do Kwon and other actors that helped reshape the regulatory conversation around so‑called algorithmic stablecoins.

Jane Street hits back, calls complaint ‘self‑defeating’

Jane Street has categorically denied the allegations and asked a Manhattan court to throw out the case with prejudice. In its motion to dismiss, the firm argues that the administrator “does not identify any material, nonpublic information Jane Street supposedly received” and that the complaint “concedes Jane Street’s single largest UST sale occurred ten minutes after the supposed material non‑public information was visible to the market,” making it “self‑defeating on its own terms.”

The trading firm also frames the lawsuit as an attempt to plug Terra’s hole with someone else’s balance sheet.

“This lawsuit is a desperate effort to pursue funds where none are owed,” a Jane Street spokesperson said, adding that “losses suffered by LUNA and UST holders were the direct result of the multibillion‑dollar fraud perpetrated by Terraform Labs’ leadership, not the actions of Jane Street.”

Coverage in the Wall Street Journal notes that the plaintiff is seeking to claw back the alleged $134 million plus additional damages from Jane Street and its executives, arguing that their trades “hastened the downfall” of Terraform by draining liquidity and accelerating panic. In a separate analysis, DL News reported that Jane Street told the court it simply “sold a deteriorating investment” as public signs of Terra’s failure mounted, insisting that sophisticated firms and retail traders were reacting to the same information as the peg broke.

The case now sits at the intersection of market‑structure reality and post‑crash scapegoating: a high‑frequency trading firm that profited by moving fast, and a liquidator trying to reframe that speed as illicit access to inside information. Whatever the outcome, the lawsuit ensures that the forensic fight over who really accelerated Terra’s $40 billion destruction—Terraform itself, Jane Street, or a combination of both—will play out in open court rather than just in crypto’s collective memory.

Missouri has filed a civil lawsuit against GPD Holdings, the operator behind CoinFlip’s network of crypto ATMs, accusing the company of knowingly facilitating fraudulent transactions and profiting from them. The action represents one of the most prominent state-level efforts to police crypto kiosks as regulators widen scrutiny over how digital-asset services interact with everyday consumers, including seniors and veterans who may be particularly vulnerable to scams.

The Missouri Attorney General’s Office, in a filing disclosed this week, seeks a wide-ranging remedy under the Missouri Merchandising Practices Act. The petition asks the court to declare CoinFlip’s practices unlawful, to enjoin the company from operating within Missouri, to impose civil penalties of $1,000 per violation for the past five years (potentially up to $1.826 million), and to award restitution to affected consumers. The office framed the case as part of a broader concern about the integrity of crypto kiosks and the protection of Missouri residents from fraudulent activity.

CoinFlip’s footprint in Missouri, according to the company’s own disclosures, includes 136 crypto kiosks in the state and a national network of 4,229 kiosks across the United States. The Missouri action comes amid a wider wave of regulatory interest in crypto ATM operators that has included investigations and local ordinances aimed at restricting or banning kiosk activity in several jurisdictions. The state’s inquiry first emerged last December as part of a broader probe into multiple crypto ATM operators, including Bitcoin Depot, which has faced its own regulatory and financial pressures in recent months.

Key takeaways

- The Missouri Attorney General filed a civil lawsuit against CoinFlip’s operator, alleging violations of the Missouri Merchandising Practices Act and seeking a court order to halt operations in Missouri, plus civil penalties and consumer restitution.

- CoinFlip reports 136 kiosks in Missouri and more than 4,200 nationwide, illustrating the scale of crypto ATM access in the United States and the potential exposure for consumers to fraud if operators fail to comply with consumer protections.

- The case is part of a broader regulatory push in the United States, where multiple states have scrutinized crypto kiosks and passed or considered laws restricting their use amid concerns about scams and fraudulent activity.

- In a related development, Bitcoin Depot disclosed material going-concern risk in an SEC filing ahead of its Chapter 11 filing, underscoring rising financial and legal pressures on major kiosk operators.

Broader regulatory momentum and the cited concerns

The Missouri action does not stand alone. The attorney general’s filing notes that the enforcement action is tied to a broader investigation launched in December into several crypto ATM operators. While the Missouri case centers on CoinFlip, it sits within a pattern of local and state authorities moving to constrain or regulate crypto kiosks as cases of alleged fraud or consumer harm come to light. This pattern has included other operators and, in some cases, actions aimed at specific practices or business models within the sector.

Meanwhile, Bitcoin Depot—another major crypto ATM operator—has faced a separate set of challenges. In a May filing with the U.S. Securities and Exchange Commission, Bitcoin Depot warned that substantial doubt existed about the company’s ability to continue as a going concern. The filing highlighted looming legal judgments and ongoing litigation as part of a broader risk profile. Days later, Bitcoin Depot proceeded with a voluntary Chapter 11 filing in Texas, underscoring how even the largest kiosk networks are navigating a high-stakes legal and financial environment.

These developments come as municipalities and states weigh concrete regulatory measures. Earlier reporting documented efforts in several jurisdictions to restrict or ban crypto kiosks, with Minnesota cited as considering a ban in the wake of scam-related incidents. The cumulative effect is a climate in which operators must contend with evolving compliance requirements, potential consumer redress obligations, and the financial strain that litigation and reorganizations can place on business models built around high-volume, low-margin ATM operations.

For investors and users, the implications extend beyond individual lawsuits. The Missouri action underscores the ongoing risk that state-level regulators will deploy consumer-protection tools to shape how crypto services operate at the kiosk level. As regulators demand higher standards for disclosures, transaction disclosures, and possibly Know-Your-Customer (KYC) controls, operators may need to accelerate compliance investments. In parallel, high-profile bankruptcies and insolvency risk among large operators remind the market that the sector remains exposed to liquidity pressures and legal headwinds even as demand for easy crypto access persists.

Operational and market implications for the crypto ATM sector

From an operator’s perspective, the Missouri suit serves as a practical case study in how consumer protection statutes can be leveraged to challenge business practices perceived as deceptive or unfair. The Missouri filing emphasizes the act at issue—the Missouri Merchandising Practices Act—as the vehicle for relief, signaling that consumer protection frameworks will be a major battleground as states refine their oversight of crypto kiosks. Operators may need to reassess marketing claims, fee structures, and the clarity of disclosures to avoid dispute over what constitutes deceptive practices.

For users, the proceedings highlight the ongoing need for diligence when using crypto kiosks. While these machines offer convenient on-ramps to digital assets, they carry risks related to scams, chargebacks, and potential misrepresentation of fees or operational limits. Consumer protection actions (and the potential for restitution) may become more common if regulators perceive that kiosk operators are not meeting established standards for safe, transparent transactions.

From a market dynamics standpoint, the regulatory actions could influence the pace and pattern of kiosk deployment. If states pursue stricter enforcement or impose additional operating constraints, operators might slow expansion plans or shift toward jurisdictions with clearer compliance pathways. Conversely, a more predictable regulatory framework could support broader consumer adoption by reducing scam-related incidents and building trust in crypto-enabled cash-in and cash-out channels.

The contrast between ongoing enforcement actions and the sector’s growth trajectory also feeds into an important question for the market: how sustainable is a model that relies heavily on quick, low-friction access to digital assets through physical kiosks? The answer may hinge on how effectively operators implement robust fraud-detection tools, user protections, and transparent fee structures, all of which regulators are likely to scrutinize closely in the months ahead.

As for the Missouri case specifically, observers will be watching how the court handles the arguments about deceptive practices, the scope of the relief requested, and what this could mean for other operators facing similar inquiries. The outcome could set a precedent for whether consumer protection statutes will play a decisive role in shaping the day-to-day realities of crypto kiosks across the country.

CoinFlip did not provide an immediate comment in response to the filing. The company’s disclosures show a national footprint that dwarfs its Missouri presence, but the case illustrates how state-level actions can affect even widely adopted platforms. In parallel, the sector’s consolidation and legal scrutiny continue to unfold, with major operators forced to navigate both courtroom risk and market volatility.

Readers should monitor further developments from the Missouri case as well as the broader regulatory responses across states. As more courts weigh questions of consumer protection versus innovation, the next steps will reveal not only how these kiosks operate within law but also how accessible and trustworthy they remain to the general public.

Looking ahead, the sector’s trajectory will depend on the balance between enforcement actions, corporate compliance upgrades, and consumer demand for easy on-ramps to digital assets. The Missouri suit is a reminder that regulatory clarity—and the willingness of courts to enforce it—will shape the practical accessibility of crypto services at the street level in the coming months.

Bitcoin (BTC) is down roughly 40% from its October 2025 record high, but a long-term valuation model suggests the cryptocurrency could erase the entire decline and rally to as high as $255,000 by year-end.

Key takeaways:

- Bitcoin Decay Channel puts BTC’s conservative year-end range at $90,000–$255,000, with its 2027 range extending to $128,000–$308,000.

- Bearish HODL Waves suggest a possible higher bottom in the $65,900–$70,500 range.

Bitcoin model puts BTC’s year-end target in the $90,000–$255,000 range

The Bitcoin Decay Channel is a logarithmic price model that tracks BTC’s long-term uptrend while adjusting for smaller gains in each new cycle.

The cryptocurrency’s major tops in 2013, 2017 and 2021 formed near the model’s upper valuation bands, while bear-market lows repeatedly moved back toward its lower support zone.

BTC/USD price performance to date. Source: Sminston/TradingView

Bitcoin’s latest rebound also began near the lower end of the Decay Channel in March-April, showing that buyers stepped in around a zone the model has historically treated as long-term support, or bottom.

That keeps the bullish case alive, according to analyst Sminston.

“Bitcoin Decay Channel gives a pretty reasonable range—conservative case—of $90k–$255k, by the end of this year. $128k – $308k for end of ’27,” he said in a Wednesday post, adding:

“For comparison, Bitcoin was $43k in December 2023.”

Sminston’s $90,000–$255,000 Bitcoin target range fits multiple predictions calling for BTC to reach a new all-time high in 2026.

Earlier, Bernstein analysts maintained a $150,000 Bitcoin target for 2026, while pushing their $200,000 peak forecast into 2027, citing a longer institutional adoption cycle led by BTC ETFs and public companies.

Related: Bitcoin price history suggests 77% odds of new all-time high within a year

BitMEX co-founder Arthur Hayes expected Bitcoin to reclaim $126,000 this year, citing US war spending in Iran, AI infrastructure demand and the resulting pressure for more fiat liquidity.

Bear flag and other indicators hint at persistent BTC sell-off risks

Bitcoin continues facing selloff warnings from a slew of bearish indicators, including a multi-month bear flag.

A bear flag typically resolves when the price drops by as much as the previous downtrend’s height. BTC risks plunging under $56,000, down about 30% from current prices, if the classic breakdown setup plays out as intended.

BTC/USDT daily chart. Source: TradingView

Onchain data suggests Bitcoin may not need to fall as far as the bear-flag target.

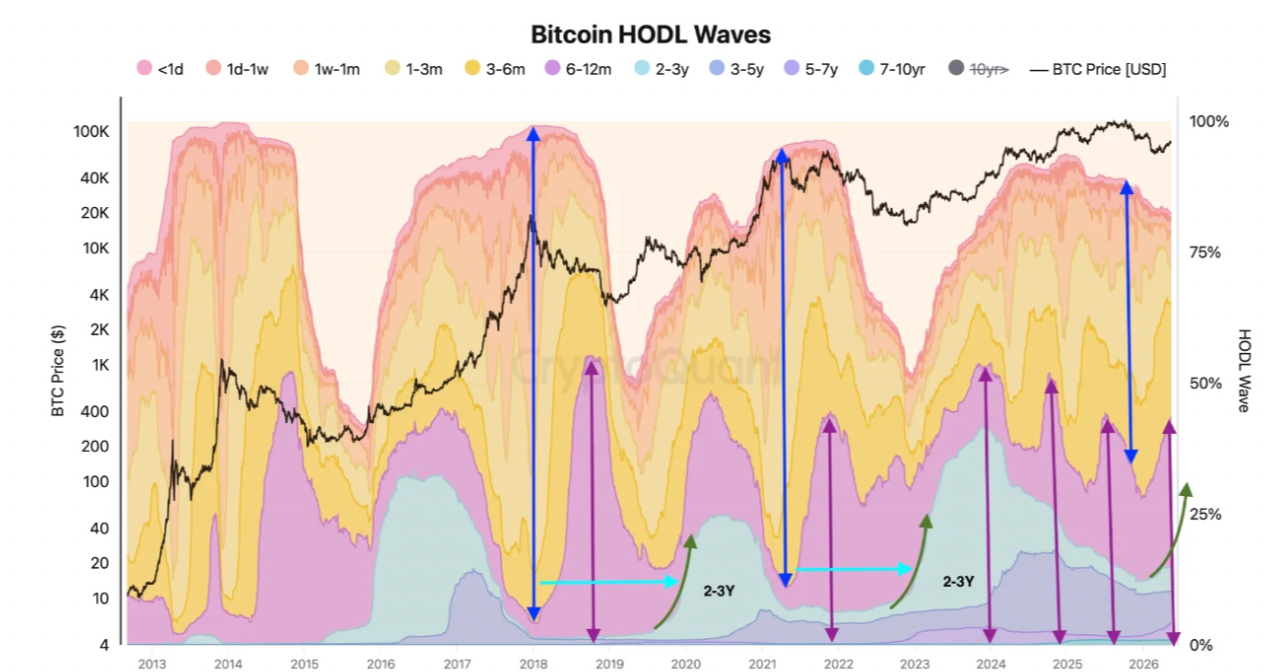

The Bitcoin HODL Waves indicator, which tracks how long BTC remains unmoved in wallets, suggests a possible bottom in the $65,900–$70,500 range if the weakness continues.

Bitcoin HODL wave indicator. Source: CryptoQuant

In a Tuesday post, CryptoQuant analyst Sunny Mom said a stronger long-term holder base may help BTC form a higher, slower bottom this cycle, with $70,500 as the key level to hold.

RIPPLE XRP: They Scared You Out of Crypto Then Bought in at a Discount!?

HMRC confirms full list of legal side hustles you must declare and those you don’t

Rinehart-backed Arafura green lights Nolans rare earths mine construction

-

Crypto World5 days ago

Crypto World5 days agoBloFin War of Whales 2026 Grand Prix opens registration for $5M trading championship

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Theory – Corporette.com

-

Crypto World5 days ago

Crypto World5 days agoE-Estate Announces 1 Year Live: Washington DC Summit as Real Estate Tokenization Enters Its Next Phase

-

Tech6 days ago

Tech6 days agoTech Moves: Microsoft AI leader jumps to OpenAI; former AI2 exec joins Meta; and more

-

Tech5 days ago

Tech5 days agoGoogle reimburses Register sources who were victims of API fraud

-

Crypto World7 days ago

Crypto World7 days agoGoogle’s Gemini AI Predicts Incredible Solana Price by the End of 2026

-

Business6 days ago

Business6 days agoH&R Real Estate Investment Trust (HR.UN:CA) Q1 2026 Earnings Call Transcript

-

Entertainment7 days ago

Entertainment7 days agoZara Larsson Has Blunt Response To Chris Brown Diss

-

Sports5 days ago

Sports5 days agoNapoleonic enters 2026 Doomben 10,000 field via Abounding withdrawal

-

Crypto World5 days ago

Crypto World5 days agoBeInCrypto 100 Institutional Awards Nomination: KAST for Best Digital Assets Neobank and Best Digital Assets Fintech

-

Crypto World5 days ago

Crypto World5 days agoBitcoin Battles US Bond Nerves With BTC Price Dip Toward New May Lows

-

Fashion4 days ago

Fashion4 days agoOn the Scene at Gucci’s Cruise Show in New York City: Mariah Carey, Kim Kardashian, Lindsay Lohan, Iman, and More!

-

Crypto World5 days ago

Crypto World5 days agoWall Street’s Boldest Gold Prediction Has Russians Rushing to Buy

-

Crypto World5 days ago

Crypto World5 days agoICE and CME urge US regulators to curb Hyperliquid energy trading

-

Fashion5 days ago

Fashion5 days agoTrending Western Style Vests Perfect for Summer

-

Politics6 days ago

Politics6 days agoDWP PIP Timms review continues to be an absolute farce

-

Entertainment6 days ago

Entertainment6 days agoDavid Letterman Returns to Late Show, Blasts Cancellation

-

Crypto World5 days ago

Crypto World5 days agoIREN closes $3 billion convertible notes deal amid AI infrastructure expansion

-

Fashion4 days ago

Fashion4 days agoAmazon Sundays: Memorial Day Hosting

-

Crypto World6 days ago

Lido Finance Selects Chainlink CCIP as the Official Cross-Chain Infrastructure for wstETH Security

You must be logged in to post a comment Login