Crypto World

Hong Kong’s HKDAP Stablecoin Passes Ethereum Mainnet Test Ahead of Q2 2026 Launch

TLDR:

- Anchorpoint Financial completed HKDAP’s Ethereum mainnet transfer test with OSL and PantherTrade in May 2026.

- Every minted HKDAP token was fully backed by reserve assets and redeemed after the transfer test concluded.

- OSL Group will leverage StableHub, BizPay, and Banxa infrastructure to support phased HKDAP issuance.

- HKDAP phased issuance is set to begin by end of Q2 2026, targeting payments and cross-border capital flows.

Hong Kong’s first officially licensed stablecoin, HKDAP, has cleared a major milestone. Anchorpoint Financial, OSL Group, and Futu Holdings-backed PantherTrade completed a transfer test on the Ethereum mainnet.

The test covered converting statutory Hong Kong dollar funds into reserve assets. All minted tokens were fully redeemed after the test concluded. A phased official issuance is planned before the end of Q2 2026.

HKDAP Transfer Test Marks a Regulated Step Forward

Anchorpoint Financial received its stablecoin issuer license from the Hong Kong Monetary Authority earlier this month.

The company is a joint venture backed by Standard Chartered Hong Kong, Hong Kong Telecom under PCCW, and Animoca Brands.

These institutional partners bring both banking infrastructure and Web3 expertise to the project. Together, they form a foundation built on compliance and regulatory trust.

Standard Chartered’s infrastructure and institutional trust services backed the entire testing process. Every minted and transferred HKDAP token was fully supported by reserve assets throughout the test.

This bank-grade backing is central to what separates HKDAP from unregulated alternatives. The structure ensures that holders have full confidence in the token’s peg to the Hong Kong dollar.

OSL Group confirmed its role in supporting the test and ongoing issuance preparations. Kevin Cui, CEO of OSL Group, stated that “OSL has established a comprehensive stablecoin trading infrastructure, including OSL StableHub for smooth stablecoin and forex trading, OSL BizPay for B2B cross-border payments, and Banxa, a stablecoin deposit and withdrawal channel.”

He added that this product portfolio provides better services to OSL customers and partners. The infrastructure supports the sustainable development of the broader stablecoin ecosystem.

PantherTrade, fully owned by Futu Holdings, also participated in the Ethereum mainnet transfer test. Zhu Guyi, Global Head of Digital Assets at Futu Group, stated that the company “continues to promote qualified investors to deploy in compliant digital assets.”

He added that the collaboration will provide Futu’s extensive investor and institutional network with stable and efficient HKD stablecoin solutions. The partnership reflects growing demand for regulated digital asset products among mainstream investors.

Phased Issuance Plans Support Hong Kong’s Digital Asset Vision

Dominic Maffei, CEO and co-founder of Anchorpoint Financial, described the test as a critical first step. He stated that “completing the minting and transfer testing of HKDAP in collaboration with OSL is the first step toward Anchor Financial’s goal.”

He confirmed that HKDAP will begin phased issuance later in 2026 to support payments and capital flows. The rollout is designed to benefit the real economy, not just digital asset markets.

Maffei further noted that “Anchor Point Finance focuses on creating a safe, convenient, and regulated tokenized currency for Hong Kong.”

He added that achieving a more efficient tokenized financial asset market is a key part of Hong Kong’s vision. This vision positions the city as a global digital asset hub. Reaching that goal requires close collaboration with industry players like Futu and PantherTrade.

OSL confirmed it will continue supporting Anchorpoint Financial and its ecosystem partners in issuance preparations. The platform plans to develop a robust, regulated Hong Kong dollar stablecoin and digital asset ecosystem.

Deep integration with HKDAP is expected to provide users with secure fiat and digital asset exchange channels. It will also support efficient cross-border payment solutions and wider adoption of tokenized financial products.

The successful Ethereum mainnet test signals that Hong Kong’s stablecoin framework is becoming fully operational. Regulatory clarity, institutional backing, and tested infrastructure are now aligned for the next phase.

As issuance begins, market participants will watch how HKDAP performs in live payment environments. The project could set a template for other regulated stablecoin initiatives across the region.

Ripple’s cross-border token has tracked the broader crypto downturn, sliding roughly 24% over the past month to its current level of $1.12.

Despite unfavorable conditions and fears of a deeper decline, several key factors suggest that a much-needed recovery could be on the horizon.

The Potential Catalysts

The first bullish sign was disclosed by the renowned analyst Ali Martinez. He revealed on X that the Tom DeMark Sequential indicator has flashed a buy signal on XRP, suggesting a possible rebound is imminent.

It is important to note that his post was met with mixed feelings, as some users claimed that the technical analysis tool has not been quite accurate in the past.

Earlier this month, Martinez touched on XRP again, saying he has been closely monitoring $0.90 and arguing that a plunge to that level could present “a compelling long-term buying opportunity.”

The second factor on the list is the asset’s Relative Strength Index (RSI). The ratio recently slipped well below 30 and now hovers around that mark, suggesting the token remains oversold and may be on the verge of a short-term rally. The index ranges from 0 to 100, and conversely, anything above 70 is interpreted as a bearish signal.

Third comes the declining amount of XRP tokens stored on Binance. CryptoQuant’s data shows that the figure has dropped to a four-month low of around 2.68 billion. The development indicates that some investors have moved their holdings from the world’s largest crypto exchange to self-custody solutions, thereby reducing immediate selling pressure.

Bonus: The ETFs

The solid institutional interest in Ripple’s native cryptocurrency should also be mentioned. Over the past several weeks, inflows into spot XRP exchange-traded funds (ETFs) have exceeded outflows, suggesting that more conservative players, including pension funds and hedge funds, have increased their exposure to the coin.

As a result, financial giants such as Bitwise, Canary Capital, Franklin Templeton, 21Shares, and Grayscale were required to purchase real XRP to properly back the acquired shares. The first such products popped up towards the end of 2025, and since their launch, they have generated a cumulative total net inflow of almost $1.45 billion.

Meanwhile, spot BTC and ETH ETFs have been bleeding lately, suggesting that institutional investors have reduced their exposure to the two biggest cryptocurrencies.

The post 3 Reasons Why Ripple (XRP) Could Be Ready to Pump appeared first on CryptoPotato.

Crypto World

Trump “Loves the Inflation,” as Crypto Keeps Getting Butchered: Geopolitical Tensions vs. Crypto

Bitcoin is holding above $62,000, but barely. The crypto market shed by 20% in a month, with Ethereum breaching the psychologically huge $2,000 level and XRP going down fast. Meanwhile, a new political narrative is hardening on Crypto Twitter. The crypto president, Donald Trump, openly welcomes inflation if it torches incumbent credibility and pumps hard assets.

The macro backdrop has turned genuinely hostile. Hotter-than-expected inflation prints have markets reluctantly pricing in a “higher for longer” rate environment. This has acted as a direct headwind for Bitcoin and risk assets, regardless of what political soundbites suggest.

Pro-Trump influencers on X are circulating the line that he “loves the inflation,” framing persistent CPI as a weapon against the current administration. Macro analysts push back hard: real yields drive crypto flows, not campaign rhetoric.

ETF inflows into US spot Bitcoin products have become the clearest short-term directional signal, and those flows have been wavering amid escalating geopolitical flashpoints across the Middle East and Eastern Europe.

Discover: The Best Crypto to Diversify Your Portfolio

Can Crypto President Donald Trump Reverse Bitcoin to $70,000?

Bitcoin is trading in a weekly range of $59,000–$64,000, with that band acting as both short-term support and resistance. The current $62,800 print sits uncomfortably in the middle of that channel, a no man’s land for directional traders.

The technical structure is mixed at best. Analyst video breakdowns identify ascending trendline support clustering around $60,000 on higher timeframes, while the critical resistance zone sits between $67,500 and $70,000. A clean breakout above $71,500–$73,000 would flip the short-term bias decisively bullish.

Ethereum at $1,600 is tracking BTC’s indecision rather than generating its own momentum. XRP remains range-bound at low with no breakout catalyst in sight. The collapse in corporate buying pressure adds another layer of bearish overhang.

Discover: The Best Token Presales

Bitcoin Hyper Targets Early-Mover Upside as BTC Tests Critical Support

Here’s the uncomfortable truth for spot BTC holders: even in the extreme bull case, a move from here to an all-time high will just give traders $1k for $1k initial. For traders who missed the cycle lows, that’s a thin margin against macro risk. That calculus is exactly why early-stage infrastructure plays are drawing attention from allocation-aware investors rotating out of range-bound majors.

Bitcoin Hyper ($HYPER) is positioning itself as the first-ever Bitcoin Layer 2 with Solana Virtual Machine (SVM) integration, a technical combination that, if it delivers, addresses Bitcoin’s three core limitations simultaneously: slow transactions, high fees, and the near-total absence of programmability.

The project has raised a verified $32 million in presale at a current token price of $0.0136814, with high-APY staking already live for early participants. The SVM integration theoretically enables smart contract execution faster than Solana’s mainnet, while the Decentralized Canonical Bridge handles BTC transfers without custodial risk.

The post Trump “Loves the Inflation,” as Crypto Keeps Getting Butchered: Geopolitical Tensions vs. Crypto appeared first on Cryptonews.

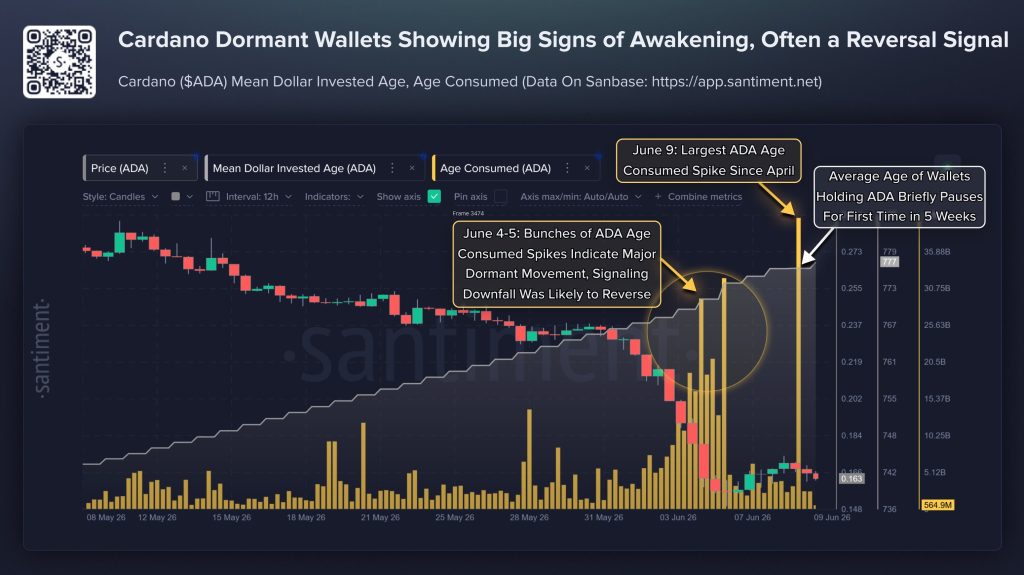

Cardano News: ADA price is sitting at $0.1665, down 42% over the past month and trading at its lowest level since December 2020, a level that has effectively unwound the entire speculative premium from Cardano’s Alonzo-era rally.

A whale sell-off is pressing the asset deeper into a zone most traders hoped they would never revisit, while a speculative cross-chain catalyst from Flare Network is generating just enough noise to complicate the bearish read.

The question is whether that noise becomes signal, or whether the selling simply overwhelms it.

Discover: The Best Crypto to Diversify Your Portfolio

Cardano News: What the Whale Data and On-Chain Pressure Actually Show

On-chain analytics firm Santiment flagged a sharp spike in Cardano’s Age Consumed metric and a simultaneous flattening of Mean Dollar Invested Age as ADA printed a low near $0.1485, signals interpreted as long-dormant holders suddenly moving coins, consistent with capitulation or major redistribution rather than routine churn.

Separately, large-holder cohorts have been repeatedly offloading: wallets holding 10–100 million ADA sold roughly 180 million tokens over just a few days, while wallets in the 1–10 million ADA range shed over 560 million tokens in a prior four-day window.

That selling pressure is compounded by a broader crypto bear market environment, ETF outflows, treasury-level de-risking, and geopolitical risk-off have hit the entire altcoin complex, meaning ADA’s breakdown is not purely project-specific.

Technically, the 50-, 100-, and 200-day EMAs are clustered between $0.23 and $0.33, all sitting well above current price, the kind of stacked moving average compression that confirms a structurally broken trend rather than a temporary dip.

Cardano Price Prediction: Where Can ADA go From Here?

Cardano (ADA/USD) has experienced a dramatic boom-and-bust cycle over the past two years on the weekly timeframe.After trading in a relatively subdued range around $0.35–$0.50 through mid-2024, ADA exploded higher in late 2024, surging to a major peak near $1.35–$1.40 in early 2025.

This parabolic move was followed by intense volatility and a series of lower highs throughout 2025. Since the second half of 2025, the token has been in a sustained and steep downtrend, shedding the majority of its gains and recently breaking to fresh lows around $0.1666.As of June 11, 2026, ADA is trading at approximately $0.1666 (up ~0.85% on the week), sitting near the bottom of a multi-month descending channel.

The RSI (14) is deeply oversold at 27.83, suggesting the asset is technically exhausted to the downside and potentially due for a relief bounce or consolidation, though the broader trend remains firmly bearish. The price is now trading at levels last seen in the 2024 bear market lows, indicating significant long-term value erosion for holders who bought near the 2025 highs.

Discover: The Best Token Presales

The post Cardano News: ADA Hits Multi-Year Low as Whales Sell, Can this be The End of Cardano? appeared first on Cryptonews.

TLDR

- Philippines central bank said Binance and BlockShoals do not hold required VASP licenses.

- Authorities clarified that BSP licensing is separate from SEC sandbox approval rules.

- Binance previously faced restrictions in 2023 for operating without proper authorization.

- SEC allowed BlockShoals entry under the StratBox sandbox for controlled fintech testing.

- Regulators require integration with a licensed domestic VASP before user onboarding begins.

The Philippines’ central bank confirmed Binance and its partner lack the required VASP licenses today. Securities and Exchange Commission records show prior warnings against Binance operations in the country. Officials said licensing rules under BSP remain separate from SEC sandbox approval process requirements.

Binance Faces Licensing Gap in Philippine Market

Bangko Sentral ng Pilipinas said neither entity holds a valid VASP license authorization. The regulator stressed that crypto payment operations require separate approval frameworks under BSP.

Binance previously faced restrictions after the SEC flagged unlicensed activity in a 2023 public notice. Authorities ordered internet providers and app stores to block the exchange nationwide.

BlockShoals Technologies entered a partnership with Binance under a regulatory sandbox framework program. The sandbox allows firms to test financial services under supervision rules in a controlled environment.

SEC granted initial clearance to BlockShoals under its StratBox program framework pilot phase. Clearance does not replace central bank licensing requirements for operations in Philippines market.

BlockShoals Partnership Under Regulatory Scrutiny

Reports say the SEC revised language describing the Binance crypto-asset service provider classification change. This description differs from earlier references that labeled Binance as a VASP designation status.

New terms require BlockShoals to integrate systems with a licensed domestic VASP by the deadline. Integration must occur before any Binance-powered user onboarding begins according to regulatory terms.

The requirement sets a 90-day timeline for compliance action from the approval stage. Authorities say the rule ensures separation between sandbox and licensing framework requirements.

BlockShoals must meet conditions before onboarding users via the Binance infrastructure system integration stage. The central bank confirmed licensing remains mandatory for all VASP operations nationwide.

BitPinas reported that the central bank clarified sandbox participation limits for crypto firms locally. The clarification highlights regulatory separation between test environments and licensing compliance structure rules.

Binance continues discussions with local partners to enter the Philippine market on the regulatory approval path. Officials maintain that all exchanges must follow dual licensing rules under BSP SEC.

StratBox sandbox continues to evaluate fintech and crypto applications under the supervision of the review process. Participation requires integration testing with regulated financial service providers before the production use stage.

The SEC adjusted sandbox terms describing the Binance crypto service entity classification update. Updated terms also require integration with licensed domestic operators within the regulatory window period.

BlockShoals must complete integration within the 90-day compliance requirement set by the regulators’ framework. No Binance user onboarding can proceed without full licensing approval from authorities process.

Bitcoin rose Thursday, and its share of the total crypto market, its dominance rate, gained alongside a meteoric rise in a lesser-known cryptocurrency.

The BTC price advanced 2.4% in 24 hours to trade recently around $62,800. The CoinDesk 20 Index (CD20) added 2.3% to 1,690 and the CoinDesk Memecoin Index (CDMEME) led gains with a 2.7% increase.

BTC’s dominance rate has risen to 59% from last week’s low of 57.9%, a sign of renewed capital flowing into the largest cryptocurrency as major altcoins struggle. The bitcoin price has held its 200-week average even as other majors such as XRP, ether (ETH) and solana (SOL) trade below the key technical line, suggesting strengthening bearish momentum in altcoins.

In the wider market, Audiera’s BEAT token jumped another 57%, taking the seven-day gain to over 500%. Audiera is a Web3 entertainment and rhythm gaming platform built on BNB Chain that treats AI characters and virtual idols as economic participants.

The protocol announced on X that onchain activity is surging, driven by consistent token burns and rising wallet participation. However, some users on social media have voiced concerns about concentrated token ownership and potential pump-and-dump risks.

The other big gainer is Velvet’s VELVET token, which has surged roughly 800% in 30 days.

Derivatives positioning

- Bullish crypto futures bets continue to get squeezed. Over the past 24 hours, exchanges liquidated $378 million, with more than $207 million coming from long positions.

- Open interest (OI) in bitcoin and ether futures has remained largely stable, indicating little appetite for fresh leverage. In zcash (ZEC), open interest has fallen to 2.28 million tokens, extending its pullback from recent highs above 2.5 million. This reflects a lightening of positioning as ZEC’s recovery from Friday’s sub-$300 low has stalled. The token has retreated from $480 to around $430 in just two days.

- The 24-hour OI-adjusted cumulative volume delta (CVD) presents a mixed picture. Tokens like BTC, XMR, ETH, HBAR, and SHIB recorded positive CVDs, showing buyers lifting offers. Meanwhile, TON, XLM, HYPE, TRX, XRP, and several others saw negative readings.

- BTC’s 30-day implied volatility index (BVIV) remains steady below 50%, suggesting traders don’t expect volatility related to tomorrow’s SpaceX IPO to spill over into crypto. Ether’s volatility index (EVIV) is also easing from Friday’s peak.

- On Deribit, bitcoin and ether puts continue trading at a premium to calls across all major expiries. The $58,000 BTC put expiring June 13 was the most actively traded contract in the past 24 hours.

Token Talk

- Velvet’s VELVET token has surged roughly 800% in 30 days, more than doubling in the past 24 hours alone.

- The token is riding the rush into pre-IPO perpetual futures, synthetic contracts that let traders bet on the valuations of SpaceX, OpenAI and Anthropic before the shares start trading. The timing tracks SpaceX’s expected June 12 debut at a reported $1.75 trillion valuation.

- DefiLlama now tracks 14 similar markets across SpaceX, OpenAI, Anthropic and Quantinuum on venues including Injective, Hyperliquid and Crypto.com, and Velvet reaches them by routing through outside platforms TradeXYZ and Ventuals rather than building its own. Injective launched the format back in October 2025.

- The contracts carry real risk. They are synthetic derivatives that convey no shares, dividends or voting rights, and their prices come from data feeds that can be thin and can drift far from actual funding rounds or any eventual IPO price. A synthetic SpaceX contract on Hyperliquid flash-crashed about 45% on Thursday.

- The VELVET token itself is drawing scrutiny. Lookonchain flagged concerns over the linkage between its spot and futures markets and heavy selling pressure after the spike, and the price whipsawed between $0.29 and $1.07 in a single day.

- The protocol holds about $653,000 in deposits against a $339 million market cap, a wide gap between the token’s valuation and the money actually using the platform.

Crypto World

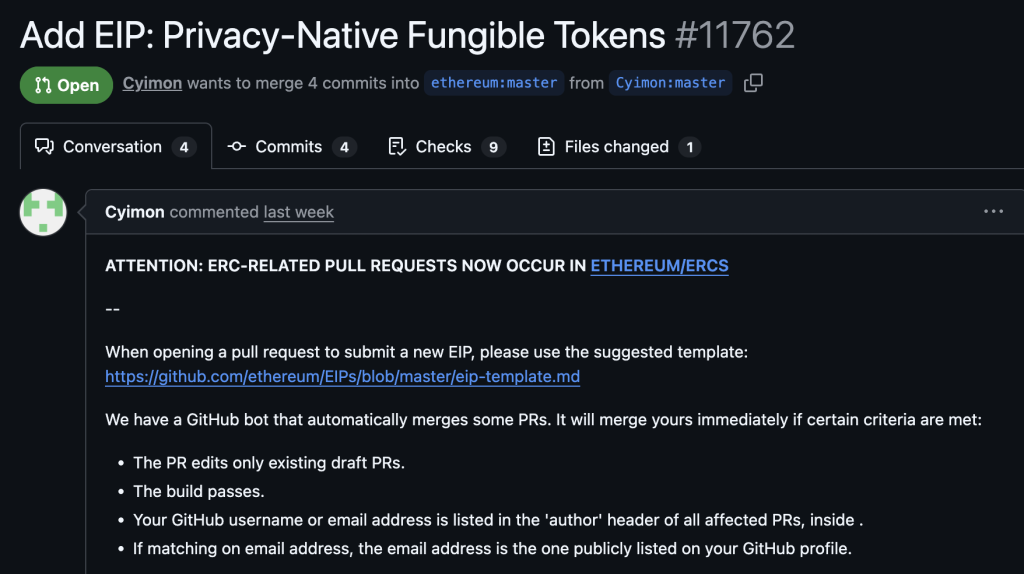

Ethereum News: Ethereum’s pERC-20 Proposal Would Make Token Transfers Private by Default

Ethereum News: A draft Ethereum token standard called pERC-20, formally tracked as ERC-7605, proposes making token transfers private by default, hiding balances, transaction amounts, and counterparties using zero-knowledge proofs baked directly into the token contract.

It is not a wrapper around existing ERC-20 tokens. It is a replacement interface: privacy-native from mint to transfer, designed so encrypted balances never exist in public state at any point in a token’s lifecycle.

The mechanism draws heavily on ZK-UTXO architecture pioneered by Zcash, specifically the Groth16 proof system and Orchard-style note commitments, and adapts them for EVM-native deployment. MetaMask-compatible. No new precompile required.

Tokens exist as cryptographic notes, not public account balances.

The proposal also includes a compliance blacklist mechanism, a deliberate architectural choice that positions pERC-20 not as a privacy-maximalist tool but as regulation-aware infrastructure. That framing matters given the regulatory climate that buried Ethereum privacy work for the better part of three years.

Discover: The Best Crypto to Diversify Your Portfolio

Ethereum News: How pERC-20 Actually Works, The UTXO Model Comes to Ethereum Tokens

Under the current ERC-20 standard, every wallet holding tokens has a publicly readable balance; anyone can query balanceOf on any address and see exactly how many tokens it holds, where they came from, and where they went. pERC-20 removes that interface entirely.

There is no balanceOf, no approve, no allowance, no transferFrom. Instead, the standard introduces a new IPERC20 interface built around mint, burn, and transfer operations, each requiring a valid zero-knowledge proof.

The underlying model is UTXO-style and note-based, the same conceptual architecture behind Zcash Orchard.

A token balance does not live at an address in the traditional sense. It exists as one or more encrypted cryptographic notes, each representing a discrete amount, owned by a key pair, and spendable exactly once. Ownership is proven via standard ECDSA signatures, which is what makes the standard EVM-native and wallet-compatible without requiring custom hardware or new browser extensions.

New EIP! — ethresearchbot (@ethresearchbot) June 4, 2026

pERC20 – Privacy-Native Fungible Tokens https://t.co/gi69qSed0M

https://t.co/gi69qSed0M

Highlights:

– Not ERC-20 compatible by design: pERC20 removes public balance/allowance concepts (no balanceOf/approve/allowance/transferFrom) and replaces transfers with a ZK note-based interface…

Transaction validity is verified using Groth16 zero-knowledge proofs, the same proof system Zcash has used at scale.

A Groth16 proof lets the network confirm that a transfer is mathematically sound, that inputs equal outputs, that the spender owns the notes being consumed, without revealing any of the underlying values.

Poseidon hash commitments are used for note construction, optimized for ZK circuit efficiency. Spent-note tracking happens in O(1) with configurable epoch cleanup, preventing the unbounded state growth that plagued earlier on-chain privacy experiments.

One thing the VOSA design does preserve publicly: the transfer graph, which addresses interacted with which. Amounts are hidden; the linkage between Virtual One-time Sub-Accounts is not. That is a deliberate tradeoff, and a significant one for anyone treating pERC-20 as equivalent to full transaction graph privacy.

pERC-20 is still a draft, it must survive the full ERC review process before any widespread deployment, and no mainnet changes are required for it to launch as an application-level standard.

The first real test is whether it advances from forum discussion to a stable interface with a reference implementation. If it does, the question of whether Ethereum’s default token layer should be transparent or private by default becomes a live design choice rather than a theoretical one.

Discover: The Best Token Presales

The post Ethereum News: Ethereum’s pERC-20 Proposal Would Make Token Transfers Private by Default appeared first on Cryptonews.

Digital Asset Holdings LLC, best known as the entity behind the Canton Network, has raised another $355 million in a new funding round led by Andreessen Horowitz’s main crypto fund.

The US-based privately held venture capital firm, founded by Marc Andreessen and Ben Horowitz, contributed $100 million. Other notable names that participated in the funding round include heavyweights like Citadel Securities, Apollo, BNP Paribas, CME Ventures, Coinbase Ventures, and HSBC.

Digital Asset Holding built the Canton Network, a layer-1 smart-contract blockchain with configurable privacy and controls. It aims to become a household name in the rapidly growing sectors of Real-World Assets (RWA) and TradFi institutions.

It uses a two-tier consensus mechanism that allows unlimited horizontal scalability of the network. It also maintains full smart contract interoperability.

According to reports, the Canton Network has already supported $6 trillion in tokenized issuance, while the proceeds from the latest funding round will be channeled toward partnerships, M&A, and ecosystem expansion.

It’s worth noting that this is the second major funding round closed by Digital Asset Holdings. In the previous round, announced a month ago, the entity raised $300 million at a near-$2 billion valuation, and a16z was once again at the forefront.

In 2025, it raised $50 million from major backers such as Nasdaq and Bank of New York Mellon.

The post Digital Asset Holdings Secures Another $355 Million in Funding Round Led by a16z appeared first on CryptoPotato.

A federal bank charter, a European passport, a growing stablecoin, and a ledger upgrade cycle in full swing. The company has never looked stronger. The token is down nearly half this year. The gap between those sentences is the most important question in the XRP market.

Summary

- Ripple’s regulatory and stablecoin wins strengthen the company, but they do not automatically create XRP token demand.

- XRP’s supply pressure, escrow releases, whale selling, and weak ETF demand have kept the chart under pressure.

- RLUSD supports Ripple’s payments business but narrows XRP’s original bridge-asset narrative.

- XRP’s next durable rally likely depends on mechanical demand channels such as lending, burn, escrow reform, and ETF flow recovery.

Picture two screens side by side. On the left, Ripple’s 2026: conditional approval for a national trust bank from the OCC, a stablecoin passport covering 30 European countries, regulatory wins from London to Abu Dhabi, a lending protocol moving through ledger governance, transaction counts on the XRP Ledger at a two-year high, and a quantum-security roadmap stretching confidently to 2028.

On the right, XRP’s 2026: a token that opened the year near $2.10, touched multi-year highs in the spring, and now trades around $1.10 after a week in which it lost roughly 17%, sitting below its 50-day moving average near $1.38 and its 200-day near $1.62.

Six years ago, the explanation would have been easy: the SEC lawsuit was strangling the company, so of course the token suffered.

The lawsuit’s shadow has mostly lifted, the regulatory environment is the friendliest in the asset’s history, and the divergence has only widened.

Holders are asking the question with increasing irritation, and they deserve a better answer than market manipulation memes or bagholder cope.

There is a real answer. It has several parts, none of them flattering to the simple thesis that corporate success must eventually pull the token upward, and a few of them hopeful in ways the frustrated crowd is currently ignoring.

The answer, compressed

Five forces explain the gap, and the rest of this piece unpacks them in order.

First, Ripple’s wins accrue to Ripple’s equity, and XRP is not equity; nothing in a bank charter or a license buys the token.

Second, supply runs on its own clock: the escrow drips up to a billion XRP a month into the market while large early holders have spent the spring selling into every bounce.

Third, the company’s flagship product now competes with the token’s original thesis, because RLUSD does the bridge-asset job without the volatility.

Fourth, the ETF demand channel turned out to be cyclical, chasing strength instead of creating it.

Fifth, a market-wide crash hit a high-beta token with extra sell pressure attached harder than most.

None of these forces is mysterious. What they share is that no press release fixes any of them, and the channels that could—lending, burn, escrow reform—are still under construction.

The win column, taken seriously

Start by giving the left screen its due, because the corporate run is real and remarkable.

In December 2025, the OCC conditionally approved Ripple National Trust Bank, putting a crypto-native company inside the federal banking perimeter and opening a path toward reserves held directly with the Federal Reserve.

In late January 2026, the U.K.’s Financial Conduct Authority granted an electronic money license; days later, Luxembourg finalized an EMI license that passports RLUSD issuance across the entire European Economic Area under MiCA.

Swiss approval reached advanced review in March. Gulf regulators in Abu Dhabi, Dubai, and Bahrain signed off on RLUSD for regulated use.

The stablecoin itself crossed $1 billion within 11 months of launch and now holds around $1.5 billion with reserves attested above the float.

The ledger side has been just as busy.

The XLS-65 and XLS-66 amendments, which would build native vaults and fixed-rate lending into the protocol, entered validator voting in January after a $200,000 security Attackathon.

The EVM sidechain has grown to roughly $180 million in locked value.

The core software is being rebranded from Rippled to XRPLd with a major performance release attached, RippleX has begun threading AI through the development pipeline, and a four-phase plan aims to make the ledger quantum-resistant by 2028.

Transactions recently touched their highest levels in two years. Central bank pilots continue to run on Ripple infrastructure. Any one of these items would have produced a double-digit rally in 2021.

In 2026, the market shrugged at all of them. That is not because the market is broken. It is because the market is answering a different question than the one holders are asking.

The question the market is actually answering

The core of it is uncomfortable. Ripple’s wins accrue, first and most directly, to Ripple, a private company whose equity captures the value of its licenses, stablecoin business, and enterprise relationships.

XRP is not equity.

Holding the token gives no claim on Ripple’s revenue, no share of RLUSD’s reserve interest, and no dividend from the trust bank.

The token’s value rests on demand for the token itself: as bridge liquidity, as the ledger’s native asset, as collateral, and as a speculative vehicle.

The implicit thesis behind the divergence frustration is that corporate success must convert into token demand.

Sometimes it does, through real channels this piece will get to.

But the conversion is neither automatic nor proportional, and 2026 has made the gap brutally visible because the corporate wins have come faster than the token-demand channels can absorb.

A bank charter does not buy XRP. A stablecoin passport does not buy XRP. A quantum roadmap does not buy XRP.

Each one makes the company more valuable and the ecosystem more durable, and each one leaves the token’s daily demand-supply balance where it was.

Equity markets understood this distinction long ago, which is why the perennial Ripple IPO chatter cuts deeper than it first appears.

If Ripple ever lists, investors will finally have a direct way to own the win column, and the market will be forced to price, openly, how much of the company’s success the token was ever going to capture. The realistic range of answers starts at less than holders hope.

The announcement rally died of overuse

Some market history explains why the win column stopped working. Half of crypto Twitter still trades as if the old regime were alive, so the story bears retelling in full. From 2017 through 2021, XRP was the announcement-rally token par excellence.

A bank partnership, a new RippleNet corridor, a MoneyGram deal, or an exchange listing in a new country: each headline produced a pop, because the holder base was overwhelmingly retail, the float available on exchanges was thinner, and the surrounding market treated every institutional gesture as confirmation of the bridge-asset destiny.

Traders learned to buy rumors of announcements, then to buy rumors of rumors. The reflex was so reliable that it became infrastructure; entire accounts existed to catalog Ripple partnership hints. Regimes like that die in a specific way.

Each announcement that fails to change the underlying demand for the token teaches a cohort of traders that the pop is for selling, and the selling arrives a little earlier each cycle, until the pop stops forming at all.

The MoneyGram partnership was the canonical lesson: a flagship deal, celebrated for two years, that ended with the disclosure that the partner had been selling the XRP it received as fast as it arrived.

By the time the 2026 win column began stacking up, the market had a decade of training data showing that Ripple’s corporate milestones convert to token demand weakly and slowly when they convert at all.

The OCC charter announcement in December produced barely a candle. That was not apathy. That was memory.

The practical implication runs against instinct: the next durable XRP rally will almost certainly not begin with a Ripple announcement, and a trader waiting for the catalyst headline is watching the wrong screen.

It will begin, if it begins, in the boring data series this piece keeps returning to: vault deposits, burn rates, flow tables, where changes compound quietly long before they trend.

The supply side never sleeps

Demand is only half of any price, and XRP’s supply side runs on a schedule that no corporate achievement alters.

Every month, Ripple’s escrow releases up to one billion XRP, with the unused portion re-locked into new contracts.

In practice only a fraction enters circulation, but the headline figure is what traders price, and the mechanism guarantees a steady drip of potential supply from a single large holder into a market that must absorb it.

Years of debate have not changed the basic optics: the largest beneficiary of XRP sales is the company whose successes holders are waiting to be paid for.

Watchers have pressed for a more transparent release regime, and the CLARITY Act’s progress has revived speculation that disclosure standards might force one.

Until then, every rally runs into the same arithmetic. The nearer-term pressure has come from whales.

On-chain trackers through late spring flagged sustained distribution from large wallets, with sizeable cohorts selling into every bounce, and the past week’s slide came with whale selling named repeatedly as the proximate cause.

Some of that is profit-taking from addresses that accumulated in 2024 at a fraction of current prices, behavior that is rational, predictable, and indifferent to press releases.

Distribution of this kind ends in one of two ways: sellers exhaust, or demand arrives that absorbs them. The win column produces neither directly. A caution on reading all this.

A falling price during heavy distribution tells you about the sellers’ positioning, not about the asset’s prospects, and conflating the two is how investors talk themselves out of positions at lows and into them at highs.

The current chart is ugly. The current chart is also exactly what a transfer from early large holders to a wider base looks like, when it is that. The data cannot yet say which it is.

The IPO wildcard cuts both ways

Hovering over all of this is the listing question, which resurfaces every quarter and usually gets argued with less precision than it needs.

An eventual Ripple IPO would be a genuine event for the token, in two opposite directions at once. The supportive direction runs through disclosure.

A public Ripple must publish audited financials, and audited financials would put hard numbers on things the XRP market has guessed about for a decade: the size and pace of XRP sales, the carrying value of the company’s holdings, the actual revenue contribution of products that use the token versus products that bypass it.

Forced transparency would close the trust discount that escrow opacity built, and a successful listing would carry validation effects no private milestone can match, with the equity’s reception telling the world how serious institutions price the whole Ripple complex.

The adverse direction runs through substitution. Every investor who wanted exposure to Ripple’s regulatory empire and bought XRP for lack of an alternative would suddenly have the real thing.

The token’s role as a proxy for the company, always analytically wrong but behaviorally real, would end on listing day, and demand built on that proxy logic would migrate to the stock.

Circle’s market history offers the template: its IPO gave investors a direct claim on stablecoin economics, and nobody needed to hold a token to participate.

The likeliest net effect is a repricing in which XRP trades more purely on its own mechanical demand, which is healthy in the long run and could be violent in the short run, in either direction, depending on what the disclosures reveal.

No filing exists, and post-CLARITY rules would shape the timing.

But the scenario belongs in any serious map of the divergence, because it is the one event that would force the market to answer, in public and with money, exactly how much of the win column the token was ever entitled to.

The stablecoin ate the story

There is a deeper, slower force underneath the supply mechanics, and it is the one the XRP community least enjoys discussing. RLUSD competes with the original XRP thesis.

The bridge-asset argument that powered every XRP bull case since 2017 held that institutions moving money across borders would prefer a fast, neutral intermediary asset over pre-funded foreign accounts.

The argument was sound. What it did not anticipate was that the winning intermediary might be a stablecoin: an asset with the same settlement speed, on the same ledger, with none of the volatility that makes treasurers flinch.

Ripple built that asset itself, wrapped it in more licenses than any competitor, and now leads its corporate communication with it.

Inside Ripple’s payment flows, the two assets do cooperate, with XRP providing bridge liquidity in thin corridors while RLUSD provides the stable leg.

But at the level of narrative, the company’s regulatory triumphs of 2026 are stablecoin triumphs, and every one of them strengthens the case that regulated tokenized dollars, not volatile bridge assets, are what institutional payments were waiting for.

The market is not stupid. It watched the company’s center of gravity move and repriced the token’s role accordingly.

This, more than any single sale or unlock, explains why announcements that would once have ignited the chart now pass through it.

The announcements are about a future in which XRP’s job description has narrowed. The token keeps the ledger’s fee and anti-spam functions, its DEX and collateral roles, and its bridge niche in exotic corridors.

Those are real. They are simply smaller than the world-reserve-bridge dream that old prices were built on, and markets reprice dreams without sentimentality.

The ETF era arrived, and it was not enough

Spot XRP ETFs were supposed to be the demand channel that finally connected institutional interest to the token itself, and their story this year is a microcosm of the whole divergence.

The products exist now, after the post-lawsuit regulatory thaw turned filings into listings.

Flows through their first stretch have been positive but modest, a topic this publication has covered in depth, and nothing close to the Bitcoin ETF tidal wave that the most excited projections borrowed their math from.

The shortfall is informative. Bitcoin ETFs succeeded because they let a vast, pre-existing pool of fiduciary money express a view it already held.

XRP ETFs offer access to a view that institutions, evidently, hold with less conviction, and access without conviction produces shelf space, not flows.

Spring’s price action made the problem circular. ETF allocators chase strength and momentum. A token down sharply on the year with visible whale distribution gives a portfolio committee every reason to wait, and their waiting removes the bid that would have stopped the slide.

None of this makes the ETF channel worthless. It makes it cyclical, a demand amplifier that will matter enormously in the next genuine uptrend and contributes little during a markdown.

The steady institutional bid arrives when the price story improves, which is backwards from what holders hoped ETFs would do.

The macro made everything worse

Fairness requires the context that XRP’s slide did not happen in a vacuum.

The broader crypto market has spent recent weeks in a brutal selloff, with hundreds of billions wiped from total capitalization, Ethereum dragged toward levels not seen in years, and Bitcoin well off its highs even as equity markets sat near records.

The decoupling of crypto from stocks has been one of the stranger features of the season, and it has hit high-beta large caps like XRP harder than the leaders.

XRP’s relationship with Bitcoin this year has been its own study in decoupling.

Through the spring, the token traded its own calendar of legal and regulatory catalysts, sometimes rallying against a flat market, which felt like strength.

The same independence cuts the other way in a downturn: idiosyncratic supply pressure means XRP can fall harder than its beta predicts, and the past month delivered it, with the token breaking the $1.20 to $1.25 support zone that had held through earlier scares and probing toward the $1.05 to $1.10 region that technicians flag as the next meaningful floor.

The concentration of XRP’s spot volume on Asian retail venues, particularly in South Korea and Japan, adds a final amplifier.

Retail-heavy order books are momentum machines in both directions, quick to chase highs and quick to abandon support, and they make XRP’s drawdowns sharper than its institutional-era story would suggest.

The microstructure of who actually trades this token has changed far less than the company behind it.

What Ripple itself could do tomorrow

One actor in this story has tools nobody else holds, and the discussion rarely puts them on the table plainly.

Ripple could publish a binding, transparent escrow release policy: fixed schedules, advance disclosure of intended sales, and reporting that lets the market price supply instead of fearing it.

The cost would be flexibility; the benefit would be retiring the single oldest discount on the asset.

Hyperliquid showed the opposite lever in 2025, showing the whole industry how mechanically routing protocol revenue into open-market token purchases can re-anchor a price to a business.

While Ripple’s corporate structure makes a direct copy awkward, nothing prevents the company from committing a defined slice of payments or stablecoin revenue to programmatic XRP acquisition for operational reserves.

Even a modest, audited program would invert the market’s core assumption that the company is a permanent net seller of the asset its community holds.

The fact that none of this has happened is itself information. Ripple’s incentives point toward funding the regulatory land grab, and selling escrowed XRP remains the cheapest funding desk on earth.

Holders waiting for the company to defend the chart are waiting for it to act against its own treasury logic, which companies do rarely and only when the asset’s weakness starts costing them something they value more: ecosystem credibility, validator goodwill, or an IPO narrative.

Watch for that pain threshold. The day defending XRP becomes cheaper for Ripple than ignoring it is the day the win column finally gets a direct conduit to the price, and that day is more likely to be chosen in a boardroom than discovered on a chart.

The channels that could reconnect company and token

Diagnosis without prognosis is just complaint. The constructive version is a list of specific, watchable channels through which the win column could start paying the chart.

The first is the lending protocol. If XLS-65 and XLS-66 activate and vault deposits grow, XRP gains its first native yield and its first protocol-level supply sink.

Locked tokens earning underwritten credit yield are tokens off the order books, and the analyst threshold of $500 million in vault value is a reasonable line for when the effect becomes visible.

The second is fee burn at scale. Every XRPL transaction destroys a sliver of XRP; transaction counts at two-year highs make the burn real but still tiny, and only an order-of-magnitude rise in ledger activity, of the kind tokenization and lending could bring, turns it into a pricing factor.

The third is escrow reform. A credible move to a transparent, rules-based release schedule, whether volunteered or regulation-forced, would remove the single largest standing discount on the asset.

The fourth is the ETF flywheel reversing polarity, which requires a price uptrend to start it but compounds once started.

The four channels share one trait. Each converts ecosystem activity into token demand mechanically, without requiring anyone to believe a narrative.

That is the actual lesson of 2026 for XRP: narrative channels are exhausted, mechanical channels are under construction, and the chart will reconnect with the company when the mechanics, not the press releases, say so.

Reading the divergence honestly

The divergence supports two readings: a broken token attached to a thriving company, or a mispriced one.

The bearish reading is coherent. The company’s success has migrated to assets and business lines that holders do not own, supply pressure is structural and scheduled, the flagship demand thesis was partially cannibalized in-house, and the token now trades as a high-beta large cap with extra sell pressure attached.

Under this reading, the divergence is not an anomaly to be corrected but a discovery of how things always were, and rallies are for selling until a mechanical demand channel proves itself at scale.

The bullish reading is also coherent, and it is not cope.

Ripple is constructing the most heavily regulated financial stack in crypto, every layer of it runs on a ledger whose native asset is XRP, and the conversion channels—lending, burn, collateral, ETF flows—are months rather than years from testable.

Prices set during indiscriminate whale distribution and a market-wide crash are the worst possible estimate of what a demand structure will look like after those channels open.

Under this reading, 2026 is the year the market punished XRP for the gap between announcement and mechanism, and the punishment is creating the entry that the mechanism era will reward.

What a careful observer cannot do is split the difference lazily.

The two readings make different predictions on visible timelines: vault deposit growth, burn rates, escrow policy, ETF flow direction.

Within two or three quarters, the data will start choosing between them.

Until then, the only defensible position is the uncomfortable one: the company’s win column is real, the chart’s verdict is real, and the bridge between them is under construction with no completion date on the permit.

As of June 11, 2026. Prices and on-chain figures move quickly; verify current data before trading. This article is information, not investment advice.

The debate over Strategy’s (MSTR) recent dilutive transaction resurfaced, this time featuring Strategy Executive Chairman Michael Saylor and Strike and Twenty One Capital (XXI) CEO Jack Mallers, on Wednesday at BTC Prague, as the two weighed in on how investors should assess the company’s increasingly complex capital structure.

Mallers asked Saylor how he defines multiple-to-net asset value (mNAV), noting that some investors include out-of-the-money securities in their calculations and asking whether he agrees with that approach. (Strategy currently has $6.7 billion of convertible debt that is out of the money, meaning the securities are not expected to convert into equity at the current $115 share price).

Mallers also challenged Saylor’s view on dilution, asking for an example of a dilutive transaction if issuing equity for cash is not considered dilutive.

Saylor responded that mNAV can be calculated by including the notional value of convertible debt, common equity and preferred equity. However, he argued that mNAV is only one valuation framework. Investors can also evaluate gross assets per share and net assets per share, which may exclude preferred equity or convertible debt from the calculation. According to Saylor, the distinction matters less when debt and preferred equity represent only a small portion of the company’s overall asset base.

On dilution, Saylor argued that issuing equity for cash is not inherently dilutive because shareholders receive a tangible asset in return, whether cash or bitcoin. He said raising capital strengthens the balance sheet, expands the capital base and improves creditworthiness. As an example, Saylor pointed to Strategy’s recent addition of approximately $100 million to its U.S. dollar reserves, bringing the total to roughly $1 billion.

AI agents are crypto’s strongest story in 2026, but DeFAI projects now have to prove they can handle user capital safely once money is moving in live markets.

DeFAI projects pitch automated trading, portfolio management, and AI-assisted token launches to users who may not fully understand the risks. Singularry is one of those projects, working on non-custodial automation, risk controls, and smart-wallet permissions.

In an exclusive interview with BeInCrypto, Singularry explained how its AI trading agent works, which dApp features are already live, and what the project needs to prove before traders treat it as a serious DeFi product.

Singularry’s AI Agent Is Built Around Portfolio Automation

Singularry’s dApp currently includes a fully autonomous, non-custodial AI trading agent designed to manage a diversified portfolio of strategies around the clock.

The platform also offers a library of 17 strategies, ranging from conservative approaches such as dollar-cost averaging, index exposure, and stablecoin vaults to more advanced delta-neutral and market-neutral strategies.

The company said the agent is designed to act as an always-on portfolio manager rather than a single-trade execution tool.

“You set the guardrails, how much it can deploy, how aggressive it should be, and which strategies it is allowed to use, and it does the rest: continuously reading the market, sizing positions to your risk profile, entering and exiting across DeFi and CEX venues, and rebalancing as conditions shift,” Singularry said.

The company added that the agent “thinks in portfolios, not one-off trades,” weighing eligible strategies, allocating capital to stronger opportunities, and learning from each outcome over time.

Permissions Are Scoped, Revocable, and Risk-Capped

A major concern around AI trading agents is permission risk. If users give an agent too much control, a faulty strategy, compromised integration, or malicious execution path can quickly become dangerous.

Singularry said its system is designed around narrow, revocable permissions rather than open-ended access.

“Users never hand over open-ended control. Permissions are scoped on four levels,” the company said.

Those levels include on-chain capability controls, approval thresholds, risk caps, and revocable signing.

In practice, the smart wallet only lets the agent interact with protocols the user has enabled, while larger trades require explicit approval. Sensitive actions such as withdrawals remain manual.

The platform also allows users to define maximum position size, the number of concurrent positions, and daily spending limits. Execution authority can be revoked on-chain at any time.

“You grant narrow, revocable permissions. Not the keys to your funds,” Singularry said.

Security Goes Beyond Audits

Singularry said its security model relies on several safeguards beyond formal audits. These include pre-trade simulation, stale-data protection, circuit breakers, integration safeguards, and restricted custody flows.

Transactions are simulated before being broadcast. If they cannot be safely validated, they are blocked. Price and market data that exceed freshness thresholds are flagged, and the agent refuses to trade on degraded inputs.

Circuit breakers can halt activity when daily-loss limits or drawdown thresholds are reached. Singularry also said that if a connected service or signing path behaves unexpectedly, the system locks execution rather than attempting to continue.

“Keys are never held in the open; signing happens in a secure delegated environment, and destinations are restricted,” the company said.

Singularry also said its smart contracts have been audited by Fairyproof, and that all known issues have been remediated.

Risk Profiles Are Designed for Different User Types

Singularry’s risk profiles come in three presets: conservative, balanced, and aggressive. Each preset defines how capital is split across risk tiers, position limits, and approval thresholds.

The company said the agent reacts to changing market conditions through market-regime detection, volatility-aware position sizing, automatic drawdown pauses, and daily-loss breakers. It also continuously re-ranks strategies based on real outcomes.

Still, Singularry acknowledged that its system is built for disciplined portfolio management rather than ultra-fast trading.

“One honest note: the agent operates on a regular evaluation cycle, so it is built for disciplined risk management, not millisecond reaction,” the company said.

The platform currently appears most suited to intermediate DeFi users: people who already understand wallets, self-custody, and risk settings, but want to automate portfolio execution.

“Today, Singularry naturally resonates most with intermediate DeFi users: those confident enough to define their own risk parameters, smart enough to value automation, and looking for exposure to proven, conservative strategies without unnecessary complexity,” Singularry said.

Over time, the company wants beginners to grow into more advanced strategies while experienced traders use Singularry alongside existing trading systems.

The AI Launchpad Needs Quality Controls

Alongside its managed-strategy product, Singularry also has an AI Launchpad for AI-assisted token creation and bonding-curve launches. This introduces a separate challenge: preventing the launchpad from becoming a low-quality token factory.

Singularry gave a direct answer on this point.

“A bonding-curve launchpad with AI generation is structurally a memecoin factory unless quality gates are deliberately added,” the company said.

According to Singularry, better controls would include token-security screening at launch, graduation requirements based on liquidity and holder thresholds, creator reputation tied to on-chain identity.

And also a clear separation between the speculative launchpad and the audited managed-strategy product.

The company also said teams should avoid marketing quality controls before those controls are actually built.

The Market Will Judge DeFAI by Live Performance

For Singularry, the next six months will ultimately be judged by real product metrics: live capital deployed by agents, funded active users, net ecosystem growth, risk-adjusted returns, retention, re-funding behavior, fund safety, and the long-term survival rate of launchpad projects.

The company believes autonomous DeFi agents must prove they can operate safely, intelligently, and economically under real market conditions. Not just in theory, but at scale and over time.

“Narratives alone are easy in crypto. Sustainable execution is not” Singularry said. “At the end of the day, live performance, user trust, and continuous execution will determine who survives this market cycle. We believe the future of DeFi will be increasingly managed by autonomous AI agents interacting directly on-chain, optimizing strategies, allocating capital, and operating across ecosystems in real time.”

The post Singularry Says DeFAI Must Prove Itself in Live Markets appeared first on BeInCrypto.

3 Reasons Why Ripple (XRP) Could Be Ready to Pump

Where to watch all World Cup games in El Paso at Dome, Elmont

The Blood Money System (the 1st homicide, sacrifice, & conjured power) w/Dr. Francis Myles

HarrisX Poll Found 52% of Registered Voters Support the CLARITY Act

BloFin War of Whales 2026 Grand Prix opens registration for $5M trading championship

Blockchain.com files with SEC for U.S. IPO

The Blood Money System (the 1st homicide, sacrifice, & conjured power) w/Dr. Francis Myles

Every Bitcoin Investor Should Do This Before It Gets Worse

Only a true car enthusiast can understand #mindset #money #car #success #rich #wrongtalk

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Evereve – Corporette.com

-

Crypto World6 days ago

Crypto World6 days agoJensen Huang Approves Samsung, SK Hynix, and Micron for NVIDIA (NVDA) HBM4 Memory Supply

-

Entertainment4 days ago

Entertainment4 days agoThe Best Mystery Series of All Time Is Surging on Streaming 30 Years After It Ended

-

Crypto World3 days ago

Crypto World3 days agoAnatomy of the June crypto crash: Fed, Iran, Saylor

-

NewsBeat4 days ago

NewsBeat4 days agoAlexander Zverev wins the French Open to finally earn a 1st Grand Slam title

-

Tech5 days ago

Tech5 days agoSuspicious Polyfill login prompts pop up on Toshiba, Muji websites

-

Crypto World5 days ago

Senator Cynthia Lummis Calls CLARITY Act the Most Consequential Financial Legislation of This Generation

-

Tech4 days ago

Tech4 days agoMicrosoft unveils seven homegrown AI models in new bid for ‘long term self-sufficiency’

-

Tech6 days ago

Tech6 days agoMicrosoft launches MXC, an OS-level sandbox for AI agents, with OpenAI and Nvidia already on board

-

Business6 days ago

Business6 days ago(VIDEO) Justin Bieber Delivers Surprise Happy Birthday Serenade to Diners at Los Angeles Mexican Restaurant

-

Business4 days ago

Business4 days agoThe Pain Points Taking a Fragile Tech Rally Down a Notch

-

Business3 days ago

Business3 days agoHigh Stakes for Wembanyama as New York Pushes for 3-0 Lead

-

Crypto World3 days ago

Crypto World3 days agoEli Lilly (LLY) Stock Surges 4% Following Breakthrough Sleep Apnea Trial Results

-

Tech5 days ago

Tech5 days agoVon der Leyen’s AI envoy pick draws conflict-of-interest fire

-

Crypto World6 days ago

LBank Surpasses 25 Million Users Worldwide as AFA Partnership Continues to Drive Global Growth

-

Tech6 days ago

Tech6 days agoMeta steals a tactic from Tesla and builds data centers in tents

-

Tech5 days ago

Tech5 days agoHackers now exploit SolarWinds Serv-U flaw to crash servers

-

Crypto World4 days ago

Crypto World4 days agoTrump’s AI Ownership Plan Could Benefit Anthropic at OpenAI’s Expense

-

Sports2 days ago

Sports2 days agoBangladesh beat Australia after 20 years in ODIs, register only their second win over six-time world champions | Cricket News

-

NewsBeat4 days ago

NewsBeat4 days agoAlexander Zverev conquers demons and outlasts Flavio Cobolli to win French Open for first major title

You must be logged in to post a comment Login