Crypto World

How the GENIUS Act made USDC wall street’s stablecoin

The GENIUS Act, signed into law on July 18, 2025, established the first comprehensive federal framework for stablecoins in the United States.

Summary

- USDC’s reserve structure already matched the GENIUS Act’s core requirements before the law passed.

- Circle’s banking, custody, and reserve-management links helped push USDC toward Wall Street infrastructure.

- Broker-dealer capital treatment and FIS integration made USDC more useful for regulated financial firms.

- Circle’s CRCL listing validated the stablecoin business model, but reserve-income dependence remains a risk.

Circle’s USDC was already operationally aligned with what the law required: 98.9 percent of reserves in short-dated US Treasuries and cash equivalents, custodied at BNY Mellon, with BlackRock managing the reserve fund, full monthly attestations, and a regulated US issuer structure. Three subsequent developments accelerated USDC’s institutional positioning.

The SEC quietly amended its broker-dealer guidance to apply only a 2 percent haircut for USDC holdings used as regulatory capital, putting the stablecoin on the same footing as money market funds. Circle’s July 2025 partnership with FIS integrated USDC into the Money Movement Hub serving banks across 46 US states and Europe, connecting it directly to ACH and FedNow rails.

Circle’s June 2025 IPO on the NYSE under ticker CRCL surged to a peak market cap above $77 billion, briefly exceeding the value of USDC in circulation and signaling public-market conviction that the stablecoin business model is durable. Combined, these developments did something subtle but structurally important.

USDC stopped being a crypto-native stablecoin used by institutions and started becoming an institutional financial instrument that happens to be a stablecoin. This is what changed, why it matters more than most coverage acknowledges, and what it means for the broader stablecoin competitive landscape going forward.

What the GENIUS Act actually requires

The mechanics of the GENIUS Act matter because they determine which stablecoins are structurally positioned to capture institutional adoption and which are not. Most coverage treats the law as generic regulatory clarity. The specific provisions are more consequential than that.

The GENIUS Act (Guiding and Establishing National Innovation for US Stablecoins) was signed into law on July 18, 2025, after months of bipartisan negotiation in Congress. The law establishes the category of “Permitted Payment Stablecoin Issuer” (PPSI), defines the requirements for entities seeking that status, and creates a federal regulatory framework that preempts the patchwork of state-level approaches that had previously governed stablecoins.

The core requirements are structural. A PPSI must back its stablecoin 1:1 with high-quality liquid assets, primarily short-term US Treasuries (T-bills), cash, and Treasury repurchase agreements. The reserve composition is specified, and the law requires monthly attestations of reserve composition from independent accounting firms.

The issuer must comply with strict anti-money laundering and sanctions screening requirements equivalent to those applied to federal financial institutions. Larger issuers (those with stablecoin issuance above a specified threshold) fall under direct federal supervision by the OCC. Smaller issuers can elect state supervision through approved state programs.

The most significant structural provision is the seniority of stablecoin holders’ claims if an issuer fails. Under the GENIUS Act, stablecoin holders have senior rights to the reserve assets backing their tokens. This means in the event of issuer bankruptcy or insolvency, stablecoin holders get paid back from reserves before other creditors. This provision is what turns stablecoins from “tokens with reserves” into “regulated financial instruments with bankruptcy-remote backing.” It is the legal architecture making institutional adoption viable at scale.

The law’s effective date is January 18, 2027, or 120 days after regulators issue final regulations, whichever comes later. This means the formal compliance period extends through 2026 and into 2027, but the practical effect on institutional behavior began immediately upon enactment in July 2025. Banks, broker-dealers, and other regulated entities began incorporating USDC into their operational planning as soon as the law passed, even though formal compliance is still being phased in.

The federal preemption matters because it eliminates the regulatory uncertainty that had previously constrained institutional adoption. Before the GENIUS Act, an institution wanting to use a stablecoin had to navigate state-by-state regulations, varying compliance requirements, and unclear federal positioning. After the GENIUS Act, the federal framework provides a single set of rules applying nationally, with clear pathways for both federal and state supervision.

What this means in practice is institutions can now treat compliant stablecoins as standard financial instruments rather than as exotic crypto assets requiring special handling. The legal foundation for treasury management, settlement operations, payment processing, and other institutional use cases is established. The question is no longer whether stablecoins can be used institutionally. The question is which specific stablecoins are positioned to capture the adoption.

Why USDC was structurally aligned before the law passed

The reason USDC captured the institutional positioning the GENIUS Act enabled is Circle had built the company specifically around the regulatory architecture the law eventually mandated. This was not coincidental. It was strategic positioning over a multi-year period.

Circle’s reserve composition has been Treasury-dominated since the company’s early years. As of mid-2025, approximately 98.9 percent of USDC reserves were held in short-dated US Treasuries and cash equivalents. The Circle Reserve Fund is custodied at The Bank of New York Mellon (BNY Mellon), one of the largest custody banks in the world. The fund is managed by BlackRock, the world’s largest asset manager. The reserve composition is published in detailed monthly attestations.

This structure is operationally identical to what the GENIUS Act requires for PPSI status. The 1:1 backing in T-bills and cash equivalents, the institutional custody, the monthly attestations, the regulated US issuer. Circle had built all of it before the law established the formal requirements. When the GENIUS Act passed in July 2025, USDC was already compliant in substance, requiring only the formal application process to achieve PPSI designation.

The contrast with the broader stablecoin landscape is sharp. Tether’s USDT runs through Tether Operations, which is not a US-licensed entity and was not structured to comply with the GENIUS Act framework. Tether eventually launched USAT in January 2026 as a separate US-compliant stablecoin issued by Anchorage Digital Bank, but the global USDT product stays structurally outside the GENIUS framework. Smaller stablecoin issuers face the choice of restructuring to meet PPSI requirements or accepting institutional adoption pathways will not be available to them.

USDC’s pre-existing institutional relationships also matter. The BlackRock partnership for reserve management provides institutional-grade credibility that is difficult for newer entrants to replicate. BNY Mellon custody is the same custody framework used by major asset managers, mutual funds, and institutional pools. Circle’s audit relationships with major accounting firms (rather than just attestation relationships) provide additional institutional confidence. The combined effect is institutional treasurers, compliance officers, and risk managers can review USDC’s operational structure and find it familiar rather than alien.

The Coinbase relationship is the third pillar. Coinbase is the largest distributor of USDC, and the two companies have a revenue-sharing arrangement on the interest income USDC reserves generate. This creates aligned incentives for both companies to scale USDC adoption. Coinbase’s institutional client base (Coinbase Prime serves major institutional investors) becomes a natural distribution channel for USDC into traditional finance.

What Circle built over multiple years was not just a stablecoin. It was the institutional infrastructure stack around the stablecoin: regulated issuer, institutional custody, top-tier asset manager, major exchange distributor, comprehensive compliance program. The GENIUS Act validated this architecture as the regulatory standard. Other stablecoins now have to retrofit themselves to match what USDC was already doing.

The SEC broker-dealer rule that quietly changed everything

One of the most consequential developments for USDC’s institutional positioning happened with relatively little fanfare in early 2026: the SEC adjusted its guidance for broker-dealers using stablecoins as regulatory capital. The change is technical but the impact is structural.

Broker-dealers under SEC oversight are required to maintain specific levels of regulatory capital to ensure they can meet client obligations. The capital requirements include detailed rules about which assets qualify and how much of each asset’s value can be counted toward the capital requirement. Historically, stablecoins have been treated unfavorably under these rules, often with a 100 percent haircut (meaning the stablecoin holdings did not count toward capital at all) or with substantial discounts.

The early 2026 SEC guidance change instructs broker-dealers to apply only a 2 percent haircut when using qualified stablecoins (essentially GENIUS-compliant stablecoins like USDC) as regulatory capital. This means a firm holding $100 million in USDC can now count $98 million toward its capital requirements. The previous treatment would have counted zero. The change puts USDC on the same regulatory footing as money market funds, which have historically been the standard near-cash regulatory capital instrument.

The practical implications are enormous. Broker-dealers can now hold USDC as part of their regulatory capital cushion, which means they can use USDC for client settlements, intraday liquidity management, and other operational purposes without the capital penalty that previously made it economically unattractive. The combined regulatory capital held by US broker-dealers exceeds $500 billion. Even a small percentage shift toward USDC would represent meaningful additional demand for the stablecoin.

The strategic implications go beyond immediate adoption. Once broker-dealers integrate USDC into their capital management workflows, the operational lock-in becomes substantial. Switching costs for established financial infrastructure are high. The institutions adopting USDC first establish operational patterns competitors then have to displace, which creates structural advantage for the early movers.

The contrast with Tether is again instructive. Tether’s USDT was not eligible for the favorable broker-dealer treatment because Tether Operations is not a GENIUS-compliant issuer. USAT, the Anchorage Digital-issued GENIUS-compliant alternative from Tether, is theoretically eligible, but its small scale (approximately $20 million market cap in early 2026 versus USDC’s $73-77 billion) means it cannot meaningfully compete for broker-dealer integration in the near term.

The SEC rule change is also a signal about the broader regulatory direction. The agency under Chair Paul Atkins has consistently moved to make regulated crypto activities easier rather than harder, in contrast to the prior administration’s enforcement-first approach. The broker-dealer haircut change is one of multiple regulatory adjustments collectively favoring institutional crypto adoption through compliant frameworks. USDC’s positioning as the most clearly compliant major stablecoin makes it the primary beneficiary of these adjustments.

The FIS partnership and the banking integration

The Circle-FIS partnership announced on July 10, 2025 (eight days before the GENIUS Act was signed) deserves dedicated attention because it represents the operational mechanism through which USDC enters mainstream US banking infrastructure.

FIS (formerly Fidelity National Information Services) is one of the largest financial technology companies in the world, providing core banking technology, payment processing, and operational infrastructure to thousands of banks and financial institutions globally. FIS’s “Money Movement Hub” is the platform that connects bank operational systems to established payment networks like ACH (Automated Clearing House) and FedNow (the Federal Reserve’s instant payment system).

The Circle-FIS integration lets US banks offer their customers domestic and cross-border payments using USDC through the same operational interfaces they already use for traditional payments. From the bank’s perspective, USDC payments look operationally similar to ACH or FedNow payments. From the customer’s perspective, sending USDC through a participating bank’s interface is similar to sending any other payment. The complexity of blockchain settlement is abstracted away by the FIS infrastructure layer.

This is structurally important because it removes the operational barriers that have historically kept US banks from offering stablecoin services. A bank that wanted to offer USDC payments previously had to either build its own blockchain infrastructure, integrate with multiple wallet providers, or partner with a crypto-native company running outside the bank’s normal compliance and operational framework. The FIS integration provides USDC services through the same operational infrastructure the bank already uses, with the same compliance frameworks and risk management procedures.

The scale is meaningful. FIS serves banks across 46 US states and has substantial European presence. The platform processes payment volumes measured in trillions of dollars annually. Even partial USDC integration across the FIS bank network would represent enormous transaction volume flowing through the stablecoin.

The competitive implications are also substantial. If FIS becomes the dominant infrastructure for bank-issued stablecoin services and USDC is the default stablecoin within that infrastructure, the bank-channel adoption of USDC becomes self-reinforcing. Banks using FIS for traditional payments adopt USDC services through the same infrastructure. The integration cost for switching to alternative stablecoins becomes substantial. The structural lock-in builds over time.

The combined effect of the FIS partnership and the SEC broker-dealer rule is USDC is being integrated into the operational infrastructure of US banking and securities markets simultaneously. Banks use it through FIS for payments. Broker-dealers use it as regulatory capital and for client settlements. Asset managers use the Circle Payments Network for institutional flows. Each integration reinforces the others, creating compound institutional adoption that is difficult for competitors to disrupt.

The IPO verdict and public-market validation

Circle’s June 2025 IPO on the NYSE under ticker CRCL is the public-market expression of the institutional positioning USDC has built. The price action since the IPO tells a story about both the opportunity and the challenges of the stablecoin business model.

Circle priced the IPO at $31 per share, implying a valuation of approximately $6.8-6.9 billion at debut. The stock surged dramatically in the months following, peaking at $298.99 in early 2026. At the peak, Circle’s market capitalization exceeded $77 billion, which briefly exceeded the value of USDC in circulation (approximately $73-74 billion at the time). This was unusual: a company valued at more than the assets it manages on behalf of its product holders.

The market interpretation of the peak valuation was Circle’s business represents more than just a stablecoin issuer. The company is becoming the infrastructure provider for the broader internet financial system, with Arc blockchain development, the Circle Payments Network, USYC tokenized money market fund, EURC euro stablecoin, and various other adjacent products. The peak valuation priced in the full strategic vision rather than just the current stablecoin revenue.

The pullback from the peak (CRCL was trading around $61.92 in February 2026, down approximately 80 percent from the high) reflects the structural challenges of the stablecoin business model under sustained scrutiny. Circle’s revenue is heavily dependent on interest income from Treasury reserves. H1 2026 revenue was approximately $1.25 billion, with 95.5 percent from interest income. This concentration creates two specific vulnerabilities: interest rate risk (if Treasury yields fall, revenue compresses) and competitive risk (if USDC market share grows more slowly than expected, the revenue base does not expand).

Q1 2026 results showed the dynamic in action. Net income declined 15 percent to $55 million despite USDC reaching $77 billion in circulation. The decline reflected rising costs as Circle invested in Arc blockchain development, Circle Payments Network expansion, and other strategic infrastructure. The market’s interpretation was the investment phase is real but the path to scaled profitability requires sustained execution that has not yet been shown.

For analysts and investors, the CRCL story is the public-market test of whether stablecoin issuers can build durable, scaled businesses or whether they are structurally constrained by the interest-rate dynamics of their reserve income. The early read is mixed. The business model works at scale (Circle is meaningfully profitable). The growth trajectory is real (USDC supply keeps expanding). But the valuation pricing in the full strategic vision (the $77 billion peak) requires execution that has not yet been shown, while the more conservative valuation pricing in just the current stablecoin business (the $29 billion current range) implies more modest growth assumptions.

The structural takeaway from CRCL is the public-market verdict on regulated stablecoin businesses is they are real and meaningfully valuable, but the upside scenarios require execution on adjacent products (Arc, CPN, USYC) and continued favorable regulatory environment. The institutional positioning USDC has captured is necessary but not sufficient for the most bullish CRCL scenarios.

The competitive picture and what could change

The combined effect of GENIUS Act alignment, SEC broker-dealer rules, FIS partnership, and IPO validation is USDC has established structural advantages in US institutional adoption that competitors are now scrambling to address. The competitive picture deserves honest engagement.

Tether’s USDT remains the dominant stablecoin globally by market capitalization (approximately $186 billion versus USDC’s $73-77 billion), but the institutional adoption picture has been shifting. USDT’s offshore structure and lack of US regulatory compliance excludes it from the GENIUS Act framework. Tether’s January 2026 launch of USAT through Anchorage Digital was the strategic response, but USAT’s small scale (approximately $20 million market cap in early February 2026) means it cannot meaningfully compete with USDC for institutional adoption in the near term. The MiCA delistings in Europe further constrained USDT’s regulated market access.

Newer compliant stablecoin entrants face similar challenges to USAT. Ripple’s RLUSD launched in late 2024 and has been building distribution through Ripple’s existing institutional relationships, but its market cap is still measured in the low single-digit billions. PayPal’s PYUSD has institutional reach through PayPal’s payment network but limited adoption beyond PayPal’s ecosystem. Bank-issued stablecoins are emerging but generally have institutional-specific use cases rather than competing for broad market share.

The structural advantage USDC has is what economists call “first-mover advantage in a network industry.” Once major institutional infrastructure (FIS, broker-dealer capital management, asset manager treasury operations) integrates USDC, the switching costs for alternatives become substantial. The competitive moat builds over time rather than eroding. Even if alternatives offer better economics or features, the operational disruption of switching makes the alternatives less attractive in practice.

What could change the picture is regulatory shifts, technical failures, or major competitive disruption. The current SEC under Chair Atkins is unlikely to reverse the broker-dealer haircut rule or other USDC-favorable changes, but future administrations could. A significant USDC operational failure (depeg event, reserve transparency issue, custody failure) could damage institutional confidence in ways competitors could exploit. A major competitive disruption (a stablecoin from a tier-one financial institution like JPMorgan, Goldman Sachs, or BlackRock entering at meaningful scale) could fragment the market.

None of these scenarios are imminent, but they are the conditions under which USDC’s institutional positioning could erode. The honest read is USDC’s current advantage is real and substantial, but it is not absolute or permanent. The competitive landscape will keep evolving, and Circle needs to keep executing on the broader infrastructure vision (Arc, CPN, USYC) to maintain the positioning the GENIUS Act enabled.

For institutional users specifically, the practical implication is USDC has become the default stablecoin for new US institutional integrations, but the market is not monolithic. Specific use cases (cross-border remittance, crypto trading, emerging market dollar access) may still favor USDT or other alternatives. The institutional default is USDC, but the broader stablecoin market keeps having multiple legitimate options for different use cases.

What this means for the broader market

The structural shift of USDC into Wall Street infrastructure has implications beyond Circle and USDC specifically, and the broader market effects deserve honest engagement.

For the stablecoin sector generally, the implication is the GENIUS Act creates a clear distinction between compliant and non-compliant issuers, and the compliant issuers are positioned to capture the institutional adoption that the broader stablecoin growth depends on. The total stablecoin market is projected to grow substantially over the next several years (some projections reach $1+ trillion by 2030), but the growth will disproportionately flow to issuers who can integrate into traditional financial infrastructure. USDC is positioned to capture more than its current market share would suggest.

For traditional finance institutions, the implication is the operational pathway to using stablecoins is now clear and accessible. Banks can integrate USDC through FIS. Broker-dealers can hold USDC as regulatory capital. Asset managers can use the Circle Payments Network for institutional flows. The infrastructure barriers that previously constrained institutional stablecoin adoption have been substantially reduced. The pace of institutional adoption over the next 24 months will be determined by institutional risk appetite and competitive pressure rather than by infrastructure availability.

For the US dollar’s global position, the institutional USDC adoption matters because it creates new mechanisms for dollar usage in regulated international finance. Cross-border payments through bank channels using USDC settlement extend dollar reach into transaction flows that previously used either traditional correspondent banking (slow, expensive) or unregulated stablecoin transfers (compliance-questionable). The aggregate effect is reinforcing dollar dominance through new regulated channels.

For the US Treasury market specifically, USDC’s growth creates additional demand for the T-bills backing the stablecoin reserves. This is similar to the dynamic discussed in the context of Tether’s Treasury holdings, but the USDC channel is more institutionally integrated and more directly visible to traditional financial market participants. If USDC scales to $200+ billion in circulation over the next few years, the additional Treasury demand from USDC alone could be $150+ billion, with similar dynamics to the Tether Treasury holdings analysis.

For competing financial infrastructure (SWIFT, traditional correspondent banking, payment networks), the USDC adoption represents both threat and opportunity. The threat is stablecoin rails can offer faster, cheaper alternatives for specific use cases. The opportunity is integrating with stablecoin infrastructure (like SWIFT has done with Chainlink) extends the existing infrastructure’s relevance rather than replacing it. The likely outcome is hybrid models where stablecoins and traditional infrastructure coexist and integrate rather than competing directly.

The bottom line

The GENIUS Act did not create USDC’s institutional positioning. Circle had built that positioning over multiple years through deliberate strategic choices: Treasury-dominated reserves, BNY Mellon custody, BlackRock asset management, comprehensive attestations, regulated US issuer structure. What the GENIUS Act did was validate this architecture as the regulatory standard and unlock the institutional adoption pathways that the pre-existing infrastructure had been built to enable.

The three subsequent developments (SEC broker-dealer rule, FIS partnership, IPO) compounded the structural advantage. The broker-dealer haircut change made USDC usable as regulatory capital for securities firms. The FIS partnership integrated USDC into the operational infrastructure of US banking. The IPO created public-market validation and provided Circle with capital to execute on the broader infrastructure vision. Together, these developments transformed USDC from “the regulated stablecoin alternative” into “the institutional default for new US stablecoin integrations.”

The competitive picture is favorable for USDC but not without risks. Tether’s USDT remains dominant globally and keeps growing in absolute terms despite losing market share percentage. USAT, RLUSD, PYUSD, and other compliant alternatives are positioned to compete in specific segments. Bank-issued stablecoins may emerge from major institutions in ways that fragment the market. The institutional advantage USDC has built is real and substantial but not absolute or permanent.

For Circle as a company, the structural positioning creates both opportunity and risk. The opportunity is becoming the infrastructure provider for the internet financial system, with USDC as the foundation and Arc, CPN, USYC, and other products building the broader stack. The risk is the business model’s heavy dependence on interest income from Treasury reserves creates vulnerability to rate environment changes and competitive pressure on the reserve-yield revenue stream. The CRCL stock trajectory (peak above $77 billion market cap, pullback to roughly $29 billion) reflects the market’s ongoing assessment of these dynamics.

For institutional users specifically, the practical implication is USDC has become the default stablecoin for new US institutional integrations. The combination of GENIUS Act compliance, broker-dealer capital eligibility, banking infrastructure integration through FIS, institutional custody at BNY Mellon, and BlackRock-managed reserves provides the operational and regulatory foundation institutional risk and compliance teams require. Choosing USDC for new institutional use cases is the path of least resistance in 2026, and the operational lock-in builds over time.

For the broader US dollar story, USDC’s institutional adoption creates new mechanisms for dollar usage in regulated international finance and creates additional structural demand for US Treasury bills. The aggregate effect is reinforcing US dollar dominance through new regulated channels, complementing the dynamic visible through Tether’s Treasury holdings but running through different distribution channels and reaching different user segments.

For the broader crypto sector, the USDC story is one of the clearest examples of how regulated crypto infrastructure can integrate into traditional finance at institutional scale. The integration is not happening through dramatic announcements or speculative narratives. It is happening through the boring infrastructure of SEC rule changes, banking system partnerships, custodial relationships, and reserve management arrangements. The compounding effect over the next several years will likely make USDC structurally important to US financial infrastructure in ways current market cap figures do not fully capture.

The GENIUS Act did not invent any of this. It codified what Circle had already built and unlocked institutional adoption pathways the pre-existing infrastructure was designed to enable. The result is USDC has become Wall Street’s stablecoin not through marketing or promotion but through the slow, deliberate work of building institutional infrastructure that regulated financial institutions actually need.

The implications go beyond Circle. They reach into how the US financial system integrates stablecoins, how the US dollar keeps its global position through new mechanisms, and how the broader crypto-traditional finance integration actually happens at scale. Those are conversations the broader financial world is now having seriously rather than dismissively.

USDC’s position as the institutional default is the structural fact making most of these conversations possible. The next phase will be determined by whether Circle can execute on the broader infrastructure vision (Arc, CPN, USYC) and whether competitive pressure or regulatory shifts disrupt the current trajectory. The answer arrives over the coming years through specific operational milestones rather than through any single defining event.

Wall Street’s stablecoin is USDC. The structural reasons why are now in place. The implications keep unfolding.

This article is for informational purposes and does not constitute financial or investment advice. Stablecoin regulations, institutional adoption patterns, and competitive dynamics evolve quickly; the figures and milestones described reflect reporting available as of late May 2026. Always do your own research.

Key Takeaways

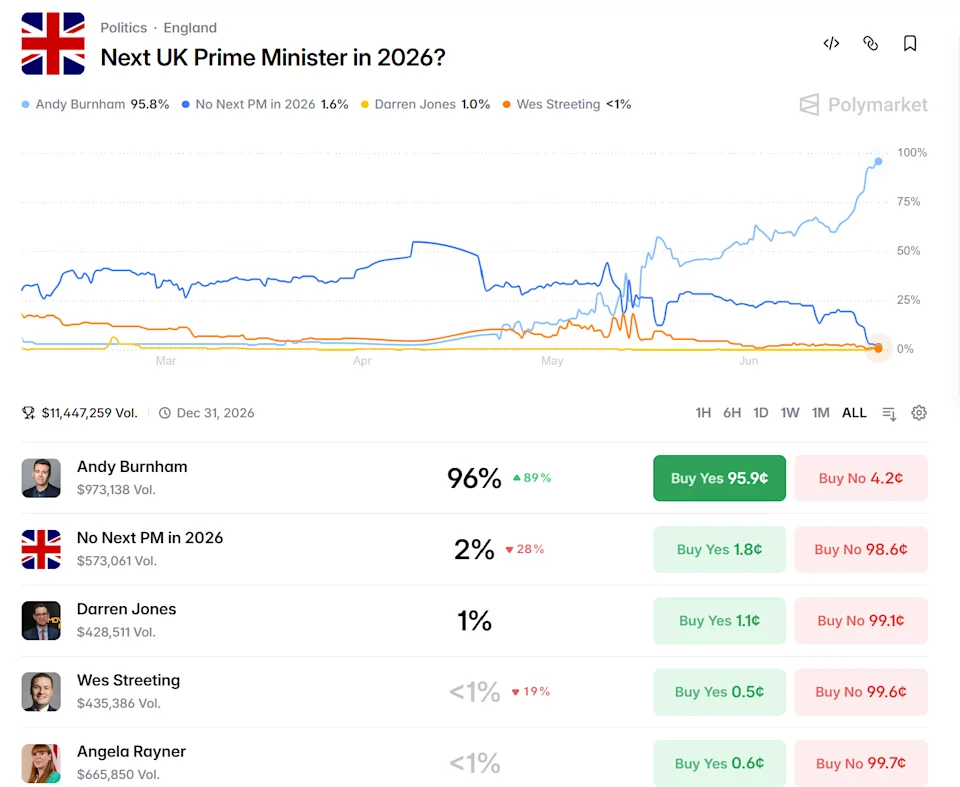

- Andy Burnham secured Makerfield constituency on June 18 with 54.8% of votes, positioning himself for Labour party leadership

- Prime Minister Keir Starmer anticipated to reveal resignation timeline on June 22, 2026

- Burnham has publicly expressed strong support for cryptocurrency, telling Web3 entrepreneurs he is fully committed to digital assets

- Current government implemented prohibition on cryptocurrency political donations in March 2026

- Over $11 million wagered on Polymarket regarding UK leadership transition, with Burnham leading predictions

By-elections rarely trigger immediate shifts in national governance. This particular contest may prove exceptional.

Andy Burnham, serving as Greater Manchester’s Mayor, captured the Makerfield parliamentary seat on June 18 with a commanding 54.8% majority. His margin over Reform UK exceeded 9,200 votes, with participation reaching nearly 59%—significantly higher than typical by-election engagement levels.

This electoral success eliminated the final procedural obstacle preventing a Labour leadership campaign. Almost immediately, speculation emerged that Prime Minister Keir Starmer was considering his position. While his office dismissed suggestions of an immediate departure, reports indicate cabinet members, union representatives, and party financiers have begun discussing transition arrangements.

Current expectations point toward Starmer announcing a departure schedule on June 22, 2026.

Implications for the Digital Asset Sector

The potential leadership change carries significant ramifications for the digital assets sector.

Starmer’s administration enacted a provisional prohibition on cryptocurrency contributions to political organizations in March 2026. This decision stemmed from recommendations in the independent Rycroft Review, which identified cryptocurrency’s pseudonymous nature as a potential conduit for foreign interference in British electoral politics.

Burnham has articulated a markedly different position. Addressing approximately 100 Web3 entrepreneurs at a Stand With Crypto gathering, he declared himself completely committed to the technology. He has consistently positioned Manchester as an emerging center for Web3 development, connecting this vision to the city’s manufacturing heritage.

Should Burnham assume the Prime Minister role, reconsideration of the cryptocurrency donation restriction appears probable. His tenure as Manchester’s mayor demonstrates consistent support for nascent technologies as economic catalysts.

Financial Markets Respond to Political Developments

Prediction platforms have registered rapid movement. Polymarket, the cryptocurrency-based forecasting platform, has seen over $11 million in positions taken on Britain’s leadership succession, with Burnham dominating as the anticipated successor.

Additionally, more than $2 million entered contracts specifically focused on Starmer’s exit timeline.

Traditional fixed-income markets have also demonstrated sensitivity. Britain’s 10-year government bond yield climbed to approximately 4.8% on Friday. Market participants appear more focused on Burnham’s anticipated fiscal stance than his cryptocurrency positioning.

The pound sterling declined in tandem with government bonds.

Bitcoin hovered around $63,900 during this timeframe, registering less than 1% daily appreciation. The cryptocurrency has declined roughly 17% over the previous month and 38% year-to-date, trading substantially below its October peak near $126,000. The political turbulence has not prompted a defensive rotation into cryptocurrency assets.

Digital asset adoption in the UK has also contracted. Financial Conduct Authority research indicates approximately 8% of British adults currently possess digital assets, declining from 12% in the prior year.

Burnham’s parliamentary induction and potential leadership declaration this week will establish the immediate trajectory for UK cryptocurrency regulation.

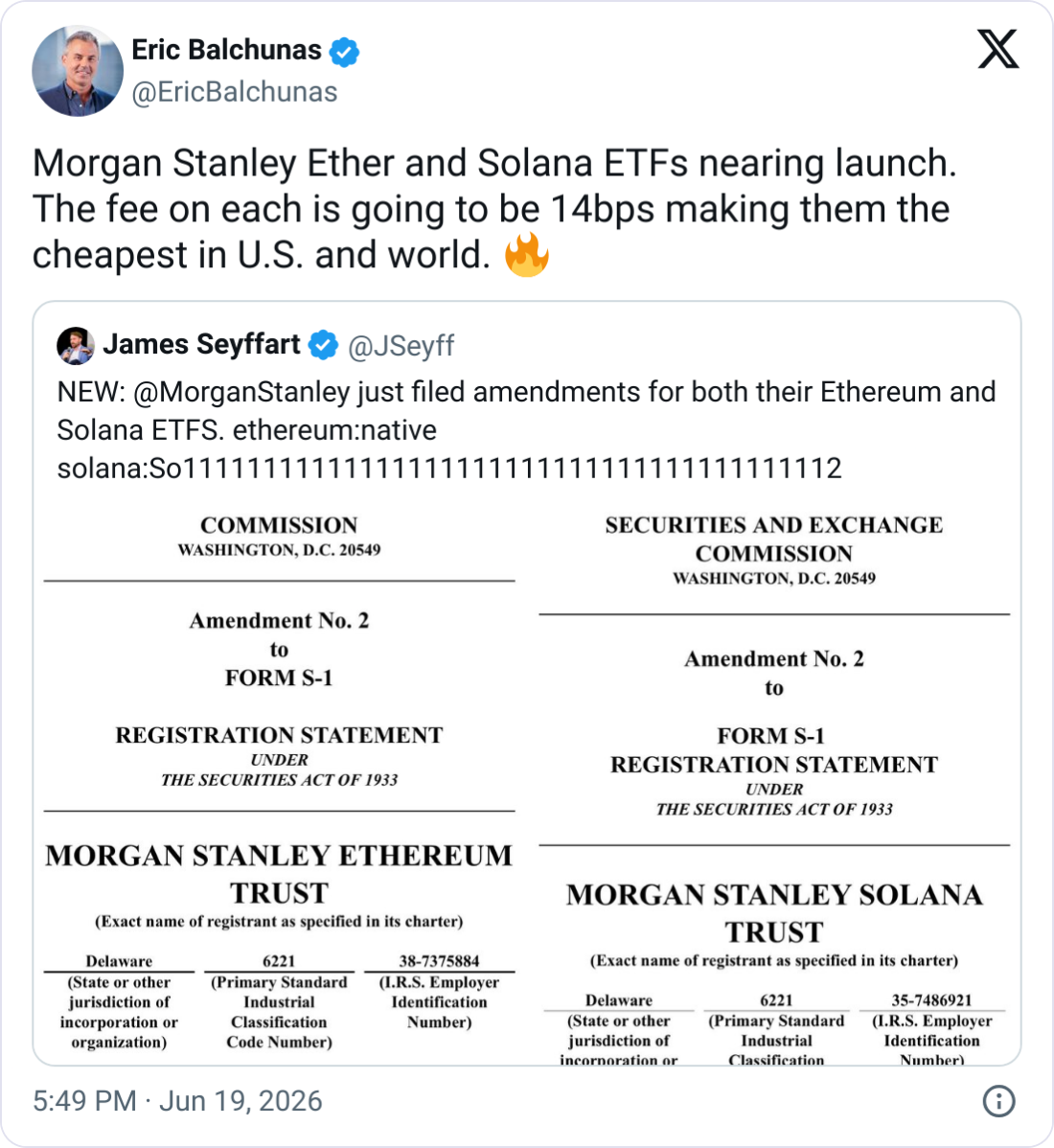

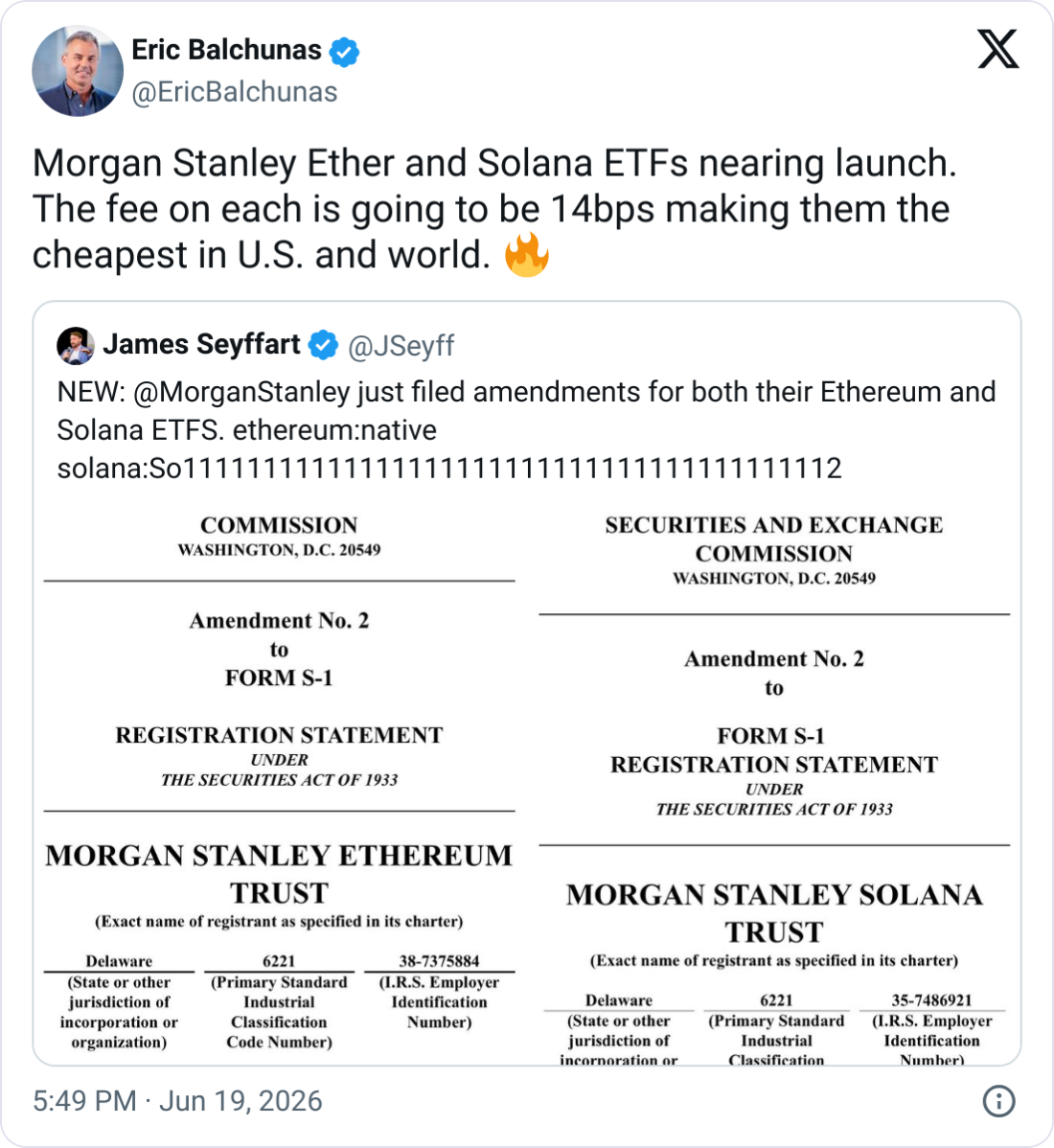

Morgan Stanley has updated its filings for its Ether and Solana exchange-traded funds, revealing that it plans to charge the lowest fees among its rivals.

The company filed amended Form S-1 statements with the Securities and Exchange Commission for each ETF on Thursday, showing it plans to undercut the current market offerings and charge fees of 0.14% for each of its products.

The current lowest-fee spot Ether (ETH) ETF in the US is the Grayscale Ethereum Staking Mini ETF (ETH) at 0.15%, while Franklin Templeton’s spot Solana (SOL) ETF, the Franklin Solana ETF (SOEZ), charges the lowest fee among its competitors at 0.19%, according to Farside Investors.

It is the second time that Morgan Stanley has updated its ETF filings since it first filed for the ETFs in January, with amendments typically a signal that the SEC is close to approving the products for trading, which would make them the 11th spot Ether ETF and seventh spot Solana ETF to launch in the US.

Bloomberg ETF analyst Eric Balchunas posted to X on Friday that the fees make them “the cheapest in [the] US and [the] world.”

Source: Eric Balchunas

Low fees have been a tactic for Morgan Stanley as it looks to make a late entry into the spot crypto ETF market dominated by issuers such as BlackRock and Fidelity. Its Bitcoin (BTC) ETF, which launched in April, set its fees at 0.14%, below Grayscale’s 0.15% fee on its mini Bitcoin ETF.

Related: Grayscale HYPE ETF ‘likely imminent’ as new update shows competitive fee: Analyst

That fee likely helped Morgan Stanley’s Bitcoin fund to record a respectable first-day inflow of $30.6 million. The ETF has since seen total inflows of $331 million, surpassing ETFs from Invesco, Franklin Templeton and CoinShares, which all launched in January 2024.

Morgan Stanley’s latest filings also show that Figment, Galaxy Blockchain Infrastructure and Coinbase Canada will provide the staking services for each of the ETFs, with each fund having a 5% staking fee for the rewards earned by the product.

The Ethereum ETF, called the Morgan Stanley Ethereum Trust, will feature the ticker “MSSE,” while the Solana ETF, dubbed the Morgan Stanley Solana Trust, will trade under MSOL.

Magazine: Does ‘Paper Bitcoin’ mean there’s an unlimited supply of BTC?

Morgan Stanley has amended its filings for spot Ether and spot Solana exchange-traded funds, setting fees it says are designed to be the lowest available in the US market for comparable products. The updates—made via amended Form S-1 statements—signal the firm is continuing to move toward an SEC decision that would allow the funds to begin trading.

According to the SEC filings lodged Thursday, Morgan Stanley plans to charge a fee of 0.14% for each ETF. If approved, the funds would expand Morgan Stanley’s presence in the fast-growing US spot crypto ETF lineup.

Key takeaways

- Morgan Stanley amended its SEC filings for both a spot Ether and a spot Solana ETF, targeting 0.14% fees.

- Farside Investors data cited in the article indicates existing lowest-fee spot products currently charge 0.15% for Ether and 0.19% for Solana.

- Amendments to Form S-1 have often been interpreted by the market as a sign of advancing SEC review and potential approval.

- Earlier, Morgan Stanley’s spot Bitcoin ETF launched with a 0.14% fee—matching its approach to undercut peers.

- Staking services for the proposed funds are set to involve Figment, Galaxy Blockchain Infrastructure, and Coinbase Canada, with a 5% staking fee on rewards.

Fees take center stage as SEC review advances

The core detail in Morgan Stanley’s latest updates is pricing. In the amended filings for each fund, the company states it intends to charge 0.14% annually. The move is particularly notable because it would place Morgan Stanley’s products at the low end of the fee spectrum for spot crypto ETFs in the US.

As background, Farside Investors data referenced in the article shows the current lowest-fee spot Ether ETF in the US is the Grayscale Ethereum Staking Mini ETF at 0.15%. For Solana, the lowest-fee spot offering cited is Franklin Templeton’s Franklin Solana ETF (SOEZ) at 0.19%, also based on Farside Investors’ figures.

Market watchers typically treat fee positioning as a proxy for how actively an issuer expects to compete for new assets. Lower expense ratios can make a fund more appealing to long-term allocators, especially when multiple spot crypto vehicles aim to track the same underlying assets.

Spot Ether and Solana proposals: what Morgan Stanley filed

The firm submitted amended Form S-1 statements for both proposed products on Thursday, as linked in the filings. The updates are the second set of amendments since Morgan Stanley first filed for the ETFs in January.

In practice, amendments are often read by the market as progress in negotiations and technical review—particularly because they generally appear closer to the moments when an issuer moves from preliminary review toward potential approval.

While the final SEC outcome is not guaranteed, the article notes that approval would add to the already expanding shelf of spot crypto products in the US, potentially bringing Morgan Stanley’s spot Ether ETF count to the 11th and spot Solana ETF count to the 7th among similar offerings, as described in the original coverage.

The specific fund naming and trading targets outlined in the article include:

- Morgan Stanley Ethereum Trust with ticker MSSE

- Morgan Stanley Solana Trust with ticker MSOL

Why “cheap” matters: Morgan Stanley’s Bitcoin playbook

Morgan Stanley has already used low fees as a market entry strategy in spot Bitcoin. Its Bitcoin ETF, launched in April, set its fee level at 0.14%, positioned below Grayscale’s 0.15% fee on its mini Bitcoin product, as noted in the article.

That fee decision appears to have been part of the firm’s early traction. The article references Cointelegraph coverage stating the fund recorded first-day inflows of $30.6 million and that total inflows have since reached $331 million, outpacing ETFs from Invesco, Franklin Templeton, and CoinShares that launched in January 2024.

Importantly, while inflow performance can be affected by many variables beyond fees—such as distribution reach, investor base, and timing—the repetition of a 0.14% expense ratio suggests Morgan Stanley is intentionally carrying forward a “competitive cost” approach across its crypto ETF expansion.

Staking services and the 5% reward fee

Morgan Stanley’s amended filings also address operational details tied to staking. The article says the filings indicate Figment, Galaxy Blockchain Infrastructure, and Coinbase Canada will provide staking services for each of the ETFs.

Under the structure described, each fund would apply a 5% staking fee to rewards earned by the product. This matters for investors because staking-related fees can change the effective return experienced by shareholders, particularly for spot products where staking can influence yield dynamics compared with a simple spot exposure approach.

Even with a low base expense ratio, staking economics can differ from the headline management fee. Investors generally look at both the fund’s stated expense level and any additional costs associated with custody, network participation, and reward allocation.

What to watch next

With Morgan Stanley’s spot Ether and Solana ETFs moving through an active amendment cycle—and with fees positioned at the low end versus currently available rivals—the next steps for investors are to monitor SEC feedback and any further filing updates that often precede approval decisions. The open question remains whether the SEC’s review will conclude in a timeframe that brings these products to market, and how staking-related costs ultimately shape investor outcomes versus existing offerings.

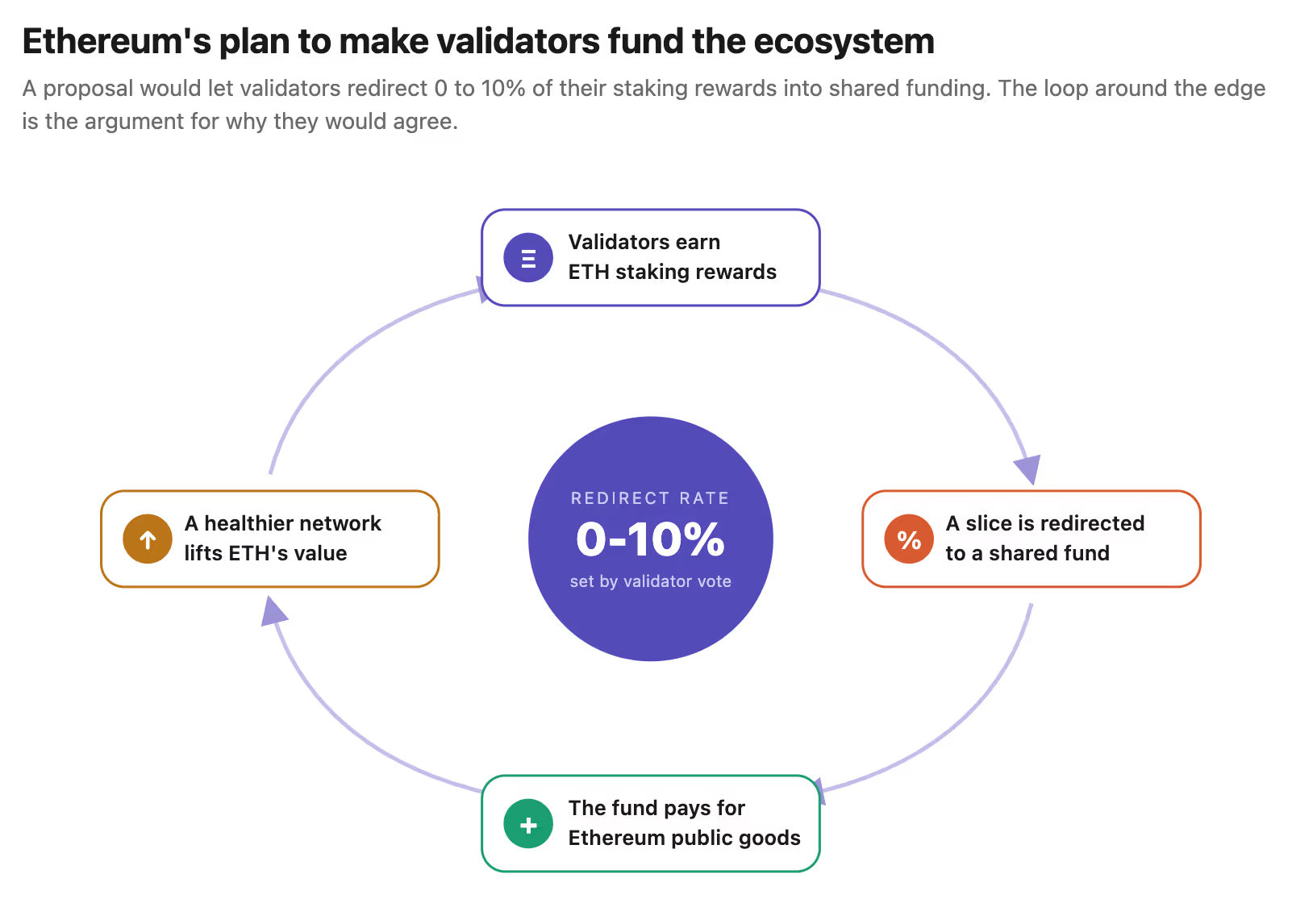

Validators are entities that keep Ethereum running by locking up ether (ETH), checking transactions and earning staking rewards for doing so. Funding, in this context, means paying for the shared work Ethereum relies on, such as developer tools, security research, public infrastructure and other projects that help the network but do not always have a direct business model.

The proposal seeks to shift that burden toward validators, who earn ETH rewards for securing the network and benefit when Ethereum becomes more valuable.

It argued that validators are natural long-term stakeholders because better ecosystem funding can increase network activity, ETH burn and the value of staked ETH.

Validators could also select preferred funding recipients under the proposal. Those preferences would be combined into a ‘splitter’ contract that distributes redirected funds among chosen addresses. The design is meant to let validators “set and forget” their preferences rather than vote on every grant.

At current staking levels, the post estimated that validators receive roughly 700,000 ETH a year in rewards. A 5% to 10% redirect could send about 50,000 to 70,000 ETH a year toward ecosystem funding. That equates to about $120 million at ether’s current market prices.

The idea is likely to be controversial, however.

For years, users looking to speed up their transactions on the Bitcoin blockchain relied on a handy optional feature that essentially says, “I might want to replace this transaction with a higher fee.”

But what started as a helpful tool has become redundant and a small privacy issue, prompting some developers to discuss possible ways to do away with it.

Let’s first take a look at the so-called replace-by-fee (RBF) signaling, then discuss the developers’ proposals.

Replace by fee (RBF) signaling

Imagine sending a paper check through the mail, but the postal system is stretched and congested. To ensure your payment doesn’t get stuck, the check has a small checkbox that says, “I reserve the right to cancel this check and write a new one with a higher rush fee if it gets delayed.” (The higher fee, of course, is an incentive for the postal system to prioritize your transaction.)

Such a feature is called Replace-by-Fee (RBF) in the Bitcoin ecosystem. For years, when you sent bitcoin, your wallet let you flip a switch, signaling to the network that you might want to “fee-bump” to speed up your transaction later.

Crypto World

Ethereum Layer 2 Taiko Urges Users to Withdraw Funds From Bridges, Confirms Security Breach

Taiko, the Ethereum layer 2 blockchain, has urged users to withdraw their funds from all bridges deployed on the network immediately.

This follows a confirmation of a security breach involving the network’s chain state verification mechanism.

We have confirmed a compromise of Taiko’s chain state verification mechanism. As a result, the security assumptions of all bridges deployed on Taiko can no longer be relied upon.

The team confirmed they are actively working with the Security Council and various ecosystem partners to contain the incident, pause the affected system wherever possible, and take both technical and legal actions.

So far, there’s no information on the amount of funds in jeopardy or if something has been stolen.

According to data from PeckShield, the exploit resulted in a loss of $1.7 million, while the attacker has already transferred 1.99 million TAIKO tokens, worth slightly less than $200K, to MEXC.

#PeckShieldAlert @taikoxyz has been exploited for ~$1.7M.

The exploiter has already transferred 1.99M $TAIKO (~$189.12K) to #MEXChttps://t.co/uJhqTYrqHH pic.twitter.com/Sl9kesSSUM

— PeckShieldAlert (@PeckShieldAlert) June 22, 2026

The post Ethereum Layer 2 Taiko Urges Users to Withdraw Funds From Bridges, Confirms Security Breach appeared first on CryptoPotato.

Altura will begin winding down its stablecoin yield vault after a sharp rise in withdrawal requests over the weekend.

Summary

- Altura processed more than 8.5m USDT in instant redemptions before announcing the stablecoin vault wind-down.

- Withdrawal pressure followed Main Street’s msUSD depeg, though Altura said it had no direct exposure.

- Some portfolio positions need standard settlement periods, so redemptions will continue as underlying capital returns.

CEO Ranveer Arora said the protocol processed more than 8.5 million USDT in instant redemptions over 24 hours before deciding to close the vault in an orderly way.

Arora said the team made the move because of “sustained withdrawal demand and current market sentiment.” He added that Altura’s priority was user capital and that the team wanted all redemptions completed in a “fair, transparent, and efficient manner.” The announcement marks a sharp change for a vault built around stablecoin yield on HyperEVM.

Altura stablecoin vault positions now being unwound

Altura has notified counterparties and partners about the decision and started unwinding positions across the vault portfolio. Arora said those positions include allocations held on exchanges, private credit opportunities and real-world asset strategies.

Some positions can return capital quickly, while others need standard settlement and redemption periods. Arora said the team is working with counterparties to speed up the process where possible, and that capital will return to users as underlying positions are redeemed. He said the team will keep posting updates as more liquidity becomes available.

Main Street depeg fuels market concern

The wind-down followed wider concern across yield-bearing stablecoin markets after Main Street’s MSUSD lost its peg. The token fell sharply after Accountable, its proof-of-solvency provider, ended its service agreement with MainStreet and said the project was “unable to meet our verification standards.”

MainStreet later said its assets remained fully backed and blamed the market stress on the shutdown of a third-party proof-of-reserves dashboard. As previously reported by crypto.news, MSUSD traded far below its intended $1 peg while lending liquidity on the Morpho msY/USDC market tightened.

Altura blames misinformation and speculation

Altura said earlier that it had no direct exposure to Main Street or its strategies. It also said its HyperEVM lending vault, Alpha USDT Prime, the related USDT/AVLT market and borrowers using its Ethereum vault remained unaffected by the Main Street event.

Arora said Altura had worked around the clock through the weekend to process withdrawals and speak with partners and users. He criticized what he called “misinformation and speculation,” saying unfounded narratives had added to market fear and withdrawal pressure.

Stablecoin vault risks return to focus

DefiLlama data showed Altura with about $32.36 million in total value locked on Hyperliquid L1, with one tracked yield pool and an average APY near 17.49%. The vault had reached a peak total value locked of about $39 million on HyperEVM.

The case comes as demand for tokenized real-world asset and stablecoin yield products grows. Crypto.news recently reported that Plume and Ether.fi launched a $100 million yield-bearing RWA vault, while separate coverage of MSUSD showed how a proof-of-reserves dispute can quickly move into wider liquidity concerns.

Altura said it will keep giving updates as redemptions progress and new liquidity becomes available. For users, the main questions now are the speed of settlements, how much capital returns in each stage and whether the process can avoid rushed sales of slower portfolio positions. The protocol has not set a final completion date, leaving the redemption timeline tied to each position’s settlement terms.

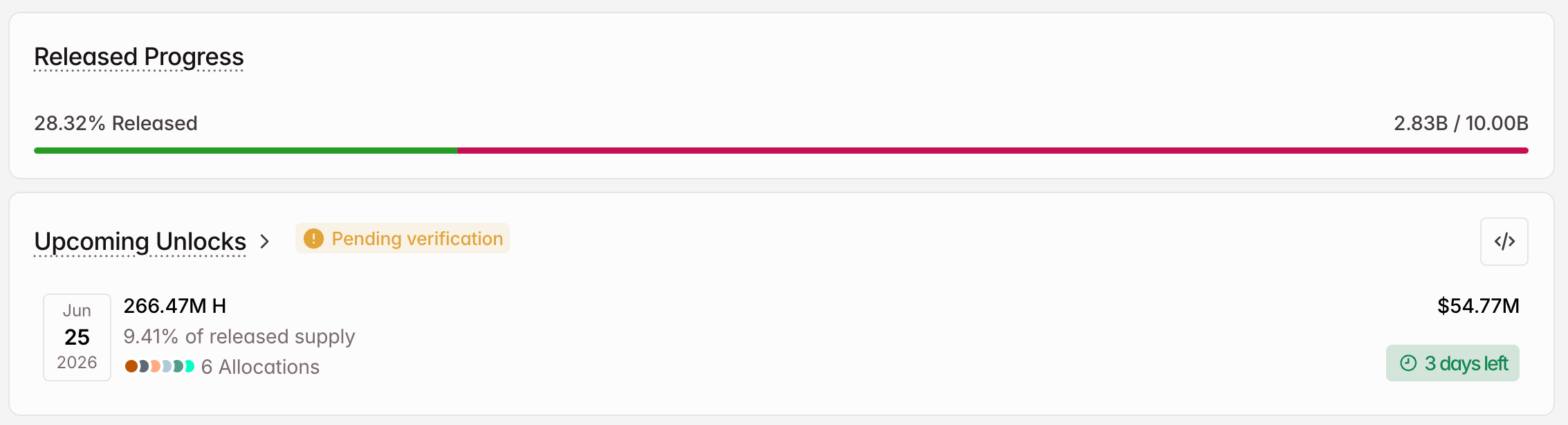

The crypto market will welcome tokens worth more than $735 million in the final week of June 2026. Major projects, including Humanity (H), MegaETH (MEGA), and Sahara AI (SAHARA), will release significant new token supplies.

These unlocks could introduce market volatility and influence short-term price movements. So, here’s a breakdown of what to watch.

1. Humanity (H)

- Unlock Date: June 25

- Number of Tokens to be Unlocked: 266.47 million H

- Released Supply: 2.8 billion H

- Total supply: 10 billion H

Humanity (H) is a decentralized identity protocol that utilizes biometric palm recognition, zero-knowledge proofs, and blockchain to verify the authenticity of real human users without exposing their personal data. It features a native Proof of Humanity (PoH) consensus mechanism.

On June 25, the protocol will unlock 266.47 million tokens. The tokens are worth $54.77 million and account for 9.41% of the released supply.

The unlock comes after the protocol suffered an exploit that resulted in losses exceeding $30 million. The H token plunged sharply following the incident. Although it recorded a notable recovery in the days that followed, the downtrend has since resumed amid growing macroeconomic and geopolitical pressures.

The team will split the released supply six ways. The ecosystem fund will receive 50 million H. Furthermore, Humanity will allocate 42.86 million altcoins to identity verification rewards and 12.50 million to the foundation operations treasury.

Additionally, early contributors will receive 79.17 million H. Investors will gain 55.56 million tokens. Finally, the Human Human Institute Strategic Reserve will receive 26.39 million H.

2. MegaETH (MEGA)

- Unlock Date: June 23

- Number of Tokens to be Unlocked: 250 million MEGA

- Released Supply: 757.5 million MEGA

- Total supply: 10 billion MEGA

MegaETH is an Ethereum Layer 2 network built for high-speed transaction processing. The network uses mini-blocks produced roughly every 10 milliseconds and targets over 100,000 transactions per second.

The network will release 250 million tokens on June 23, worth approximately $13.54 million. The unlock accounts for 32.8% of the released supply.

The team will direct the entire unlocked supply toward the Mainnet Campaign (Terminal).

3. Sahara AI (SAHARA)

- Unlock Date: June 26

- Number of Tokens to be Unlocked: 1.03 billion SAHARA

- Released Supply: 3.41 billion SAHARA

- Total supply: 10 billion SAHARA

Sahara AI is a full-stack, AI-native blockchain platform built to democratize the development and monetization of artificial intelligence. The network combines data services, AI tools, and a marketplace into one ecosystem.

On June 26, Sahara AI will unlock 1.03 billion SAHARA. The supply is worth $14.75 million. The tokens represent 30.10% of the released supply.

Sahara AI will direct 534.9 million tokens to early backers. The core team and contributors will get 406.25 million SAHARA. In addition, the team will allocate 53.02 million altcoins to ecosystem development and 31.25 million tokens for community incentives.

The unlock follows the token’s drop of over 50% earlier this month. The network said a “futures-led liquidation cascade” caused the price volatility.

In addition to these, other prominent unlocks that investors can look out for in the final week of June include Plasma (XPL), Soon (SOON), Newton Protocol (NEWT), and more.

The post 3 Token Unlocks to Watch in the Final Week of June 2026 appeared first on BeInCrypto.

Taiko has urged users to withdraw funds from all bridges deployed on its network after confirming a compromise of its chain state verification mechanism.

Summary

- Taiko urged users to withdraw bridge funds after confirming a chain verification mechanism compromise.

- Blockaid said flawed source-signal proof checks enabled unauthorized releases from Taiko’s ERC20 Vault on Ethereum.

- Taiko also stopped proposers from producing blocks and asked exchanges to suspend TAIKO deposits immediately.

The Ethereum Layer 2 project said the security assumptions behind its bridge system could no longer be relied upon.

The notice followed alerts from blockchain security firm Blockaid, which said its exploit detection system found an ongoing attack on Taiko’s ERC20 Vault on Ethereum. Blockaid put losses at more than $1 million and shared the victim contract, attacker wallet and exploit transactions.

Blockaid points to Taiko proof validation flaw

Blockaid said the likely root cause was a flaw in Taiko bridge source-signal proof validation. The firm said crafted message proofs were accepted as valid on Ethereum L1 even though there were no matching legitimate “MessageSent” events on the Taiko source chain.

That allowed the attacker to register and later retrieve fraudulent bridge messages, leading to unauthorized asset releases from the ERC20 vault. Taiko later confirmed a broader verification problem and said it was working with the Security Council and ecosystem partners.

Moreover, Taiko also said all proposers had temporarily stopped producing new blocks while the team investigates and resolves the issue. The project asked centralized exchanges to suspend TAIKO deposits immediately and said deposits should resume only after an official notice.

The team published several attacker addresses as part of its update. It said it would take technical and legal steps where needed, but did not give a timeline for restoring bridge security or restarting block production.

Bridge risks remain in focus

Taiko is a Type 1 Ethereum-equivalent ZK-EVM rollup designed as a based rollup, where Ethereum L1 validators are expected to help order transactions. The network launched mainnet in May 2024 and supports Ethereum-compatible smart contracts and tools.

Meanwhile, crypto.news recently reported that cross-chain bridge exploits caused $28.6 million in May losses, or about 42% of that month’s total reported by CertiK.

The incident comes after other cross-chain security failures this year. As previously reported by crypto.news, Verus Protocol’s Ethereum bridge lost more than $11.5 million in a forged-transfer exploit, while Axelar disabled Secret Network bridge routes after a $4.7 million exploit.

Moreover, as crypto.news earlier reported, an old Aztec Connect contract lost about $2.1 million after a verification mismatch let unbacked balances move through Ethereum settlement records.

Venture capital funds have poured $12.3 billion into defense technology startups since the start of 2026, nearly double the amount raised over the same stretch last year.

Conflicts in Ukraine and the Middle East have exposed an urgent demand for weapons systems that are cheaper and faster to build. That demand has turned military hardware into one of the year’s most sought-after bets.

VC Funds Pour $12.3 Billion Into Defence Tech in 2026

According to the Financial Times, the figure already exceeds the $9.95 billion the sector attracted across all of 2025. This signals how quickly investor appetite for drones, autonomous vessels, and battlefield artificial intelligence has grown.

The capital is concentrated among a small group of active investors. According to PitchBook, Gaingels, Alumni Ventures, and Andreessen Horowitz ranked among the most prolific check writers in the first quarter.

Daniel Rudnicki Schlumberger, head of JPMorgan’s security and resiliency initiative for Europe, the Middle East, and Asia, noted that the surging valuations come as funds increasingly treat defense as a lasting opportunity.

“We’re seeing the most important change in the way wars are being fought arguably ever,” Schlumberger said.

Follow us on X to get the latest news as it happens

Crypto Venture Funding Moves the Other Way

The defense rush stands in contrast to crypto, where venture investment has cooled sharply. Galaxy Research found that VCs deployed about $4 billion across 355 crypto deals in the first quarter.

That marked a 50% drop in capital from the prior quarter, though deal count fell only 16%.

“The decline from Q4’s spike was driven primarily by a drop in very large, later-stage financings. The number of completed deals fell much less than the amount of capital invested, indicating that smaller early-stage and seed rounds continued to get done even as Q1 lacked Q4’s concentration of mega-rounds,” Galaxy Research wrote.

Annualized, the pace implies roughly $16 billion in 2026, below last year’s near-$20 billion total. Meanwhile, new fund formation also stalled.

Crypto-focused venture funds drew about $1.1 billion in the first quarter, spread across just eight vehicles. That count marked the slowest quarter for new fund launches since the third quarter of 2020.

Galaxy attributed part of the shift to spot exchange-traded products and digital asset treasury firms, which now compete with venture funds for allocator capital. Still, the firm affirmed that “crypto venture activity remains relatively healthy overall.”

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Wars Have Driven $12.3 Billion in VC Investment Into This Sector appeared first on BeInCrypto.

Keir Starmer ‘to announce resignation this morning’ – here’s everything we know | News Politics

TYG: This Aptly Named Fund Can Be Safely Avoided

Andy Burnham’s Path to Prime Minister Could Transform UK Crypto Policy

-

Crypto World7 days ago

Crypto World7 days agoCrude Oil Plunges Over 4% as US-Iran Agreement Reopens Hormuz Strait

-

Tech6 days ago

Tech6 days agoThe Adder At The Heart Of Intel’s 8087 FPU

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Miami – Corporette.com

-

Business2 days ago

Business2 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Crypto World2 days ago

Crypto World2 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Sports3 days ago

Sports3 days agoFIFA World Cup 2026: Canada beat 9-men Qatar 6-0 to register first ever win | FIFA World Cup 2026

-

Crypto World2 days ago

Crypto World2 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Business1 day ago

Business1 day agoMHP SE 2026 Q1 – Results – Earnings Call Presentation (OTCMKTS:MHPSY) 2026-06-20

-

Crypto World4 days ago

Crypto World4 days agoAnthropic’s Dario Amodei Urged AI Unity at G7, Even as US Banned His Models

-

Business3 days ago

Business3 days agoBrexit cost 6% of UK economy, Bank of England company data suggests

-

Business1 day ago

Business1 day agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Crypto World2 days ago

Crypto World2 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Tech4 days ago

Tech4 days agoWeeks Of In-The-Field Testing And A Verdict

-

Tech4 days ago

Tech4 days agoAdobe adds its AI assistant to Premiere, Illustrator and InDesign

-

Politics2 days ago

Politics2 days agoAndy Burnham and the meaning of Makerfield

-

Crypto World4 days ago

Crypto World4 days agoIren (IREN) Stock Surges on Jefferies Buy Rating: AI Infrastructure Play Gains Momentum

-

Entertainment1 day ago

Entertainment1 day agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Tech3 days ago

Tech3 days agoInstagram Now Lets You Add A Unique Caption To Each Carousel Slide

-

Politics3 days ago

Politics3 days agoBBC Reporter Discusses Cross Party Criticism Of Trumps Iran Deal

-

News Videos3 days ago

News Videos3 days agoNightcore – MONEY ON THE DASH (Soft Rock Version) (Lyrics)

You must be logged in to post a comment Login