Crypto World

Trump earned $1B from crypto. What he holds

The headline number is income, not a wallet balance. Trump’s disclosure shows more than a billion dollars in crypto earnings, but what he holds today is a smaller and more specific story worth reading carefully.

Summary

- President Trump’s annual financial disclosure, released June 30, 2026, reports more than $1 billion in crypto-related income for 2025, with some outlets totaling the figure near $1.4 billion.

- The largest single line is about $635 million in royalties tied to the $TRUMP meme coin, paid through CIC Digital LLC under a licensing arrangement described as Celebration Coins.

- World Liberty Financial, the Trump-linked venture that issues the WLFI token and the USD1 stablecoin, accounts for the bulk of the rest, roughly $515 million to $592 million across token sales and an equity sale.

- Income is not the same as holdings: the filing lists current cold-wallet positions of over $50 million in Bitcoin and a smaller Ethereum position, plus staking rewards, figures far below the headline earnings number.

- The disclosure has drawn conflict-of-interest criticism, which the White House denies, and it lands as crypto market-structure legislation remains stalled in the Senate.

The number everyone repeated was “more than a billion dollars,” and it is accurate. But it answers a different question from the one most readers think they are asking. Trump’s disclosure reports crypto income, the money his ventures earned and distributed over the year, not a snapshot of a wallet. What he actually holds today is a separate and smaller figure, and the gap between the two is the most important thing in the filing.

This piece separates the earnings from the holdings, walks through where each number comes from, explains the vehicles behind them, and covers the conflict question honestly, with the criticism and the denial both on the page. The goal is the real picture, not the headline. Trump’s crypto ventures were extraordinarily lucrative in 2025, but that does not mean the disclosure shows a billion-dollar crypto wallet. It shows a much more specific mix of licensing income, token-sale proceeds, Bitcoin holdings, Ethereum exposure, staking rewards, and Trump-linked token businesses.

What the disclosure is

The document is a routine but revealing instrument: the annual public financial disclosure that federal officials must file, submitted on the Office of Government Ethics Form 278e and covering the 2025 reporting year, the first full year of Trump’s second term. It was released on June 30, 2026, after a 45-day extension, and it is enormous, running to roughly 900 pages by most counts, with one tally at 847. For comparison, recent predecessors filed forms in the single or low double digits of pages. That scale alone explains why the first wave of headlines focused on the biggest and easiest number to repeat.

Two features of the format matter for reading it correctly. First, values are reported in dollar ranges, or brackets, not exact amounts, which is standard for government ethics filings. When the disclosure says a holding is worth “over $50 million,” that is the top bracket on the form, and the true figure could be higher. Second, the filing mixes income and assets throughout, listing what ventures earned alongside what the filer holds.

Conflating the two is the single most common error in the coverage, and avoiding it is the whole point of reading the document carefully. Income tells you what flowed in during the year. Holdings tell you what remained as assets at the reporting date. The filing contains both, and the difference between them changes the story.

The income: where the billion-plus came from

The earnings side is where the large numbers live, and it breaks into two main sources. The single biggest line on the entire filing is roughly $635 million in royalties tied to the $TRUMP meme coin, paid through CIC Digital LLC under a licensing arrangement the filing describes as Celebration Coins. That one item accounts for more than half of the crypto income by itself. It is also why the TRUMP meme coin category matters here: the biggest number in the disclosure came from a politically branded token business, not from ordinary trading gains.

The second major source is World Liberty Financial. Across the filing, WLF-linked proceeds run to roughly $515 million to $592 million, depending on how the line items are grouped. That total includes general token-sale distributions in the low hundreds of millions, an equity sale of about $65 million tied to a Trump-affiliated entity that held a 38.25% stake in the venture, and a wallet-by-wallet breakdown of token proceeds. That breakdown is unusually granular: Ethereum proceeds of about $150.6 million, Bitcoin proceeds of about $33.5 million, USDC proceeds of about $56 million, and smaller distributions in tokens including Link, Aave, ENA, Move, and Ondo.

Add the two sources together and the crypto income clears $1 billion, with some outlets putting the full-year figure near $1.4 billion. The key word across all of this is income. These are proceeds from selling tokens and licensing a brand, realized and distributed over the year. They describe money that came in, not a pile of assets sitting in a wallet today.

The holdings: what he actually owns now

This is the part the headlines skip. Separate from the income, the disclosure lists current crypto holdings, and they are far smaller than the earnings. The filing shows a cold-wallet Bitcoin position valued at over $50 million, the top bracket on the form, and a smaller Ethereum position, reported in a multimillion-dollar range that varies across readings of the filing’s line items. It also notes ether staked through a Coinbase arrangement that produced about $1.8 million in validator rewards, meaning some of the Ethereum is generating yield.

The contrast is the story. More than a billion dollars flowed through Trump’s crypto ventures as income, but the disclosed holdings amount to a Bitcoin stake above $50 million and a smaller Ethereum stake, plus whatever exposure runs through the WLFI token and USD1 stablecoin tied to World Liberty Financial. In other words, the ventures earned enormously, but the reported end-of-period crypto assets are a fraction of that, consistent with income being distributed or moved rather than accumulated as a growing on-chain balance. Anyone picturing a billion-dollar wallet is misreading the filing.

That does not make the holdings trivial. A cold-wallet Bitcoin position above $50 million is still a large disclosed crypto asset for any public official, and it sits inside a much wider portfolio. But it is not the same thing as the income number. The more accurate read is that the crypto businesses generated the headline money, while the disclosed direct crypto holdings show a smaller ongoing exposure led by Bitcoin.

Income versus holdings: why the distinction matters

The gap between the two numbers is not a technicality. It changes what the disclosure actually tells you. Income measures the flow of money a venture generated and paid out over a period. Holdings measure the stock of assets held at a point in time. A licensing deal can generate $635 million in royalty income without any of it remaining as a crypto holding, because royalties are paid in cash or converted, not held as tokens.

Token sales generate proceeds precisely by selling the tokens, which reduces holdings even as it produces income. That is why a venture can produce hundreds of millions of dollars in crypto-related income while the end-of-period balance sheet shows a much smaller direct crypto position. The same logic applies to staking rewards: a reward is income, while the staked ether is a holding. Mixing those categories makes the disclosure look like a single giant pile of crypto, when it is actually a set of different flows and assets.

So the honest framing is this: Trump’s crypto ventures were extraordinarily lucrative in 2025, and his disclosed crypto holdings at the end of the period were comparatively modest, led by a Bitcoin position above $50 million. Both facts are true, and reporting only the first inflates the picture. The holdings figure is the better guide to ongoing exposure, while the income figure is the better guide to how much the ventures earned. Reading them as one number, a billion-dollar hoard, is simply wrong.

World Liberty Financial and the token machine

Understanding the income requires understanding the vehicle behind most of it. World Liberty Financial is the Trump-linked crypto venture, co-founded by family members including Eric Trump and Donald Trump Jr., that issues the WLFI governance token and the USD1 stablecoin. It is the engine that produced the bulk of the non-meme-coin crypto income in the disclosure, through token sales and the equity stake held by an affiliated entity. For readers trying to parse the structure, the WLFI governance token and the USD1 stablecoin are different instruments with different economics.

WLF matters beyond the 2025 figures because it is an ongoing business, not a one-time event. A governance token and a stablecoin are products that keep generating activity, fees, and potential proceeds, which means the venture is a recurring source of income rather than a closed chapter. For anyone tracking the crypto-market implications, WLFI and USD1 are the live instruments to watch, since their adoption and trading are where the venture’s future value, and the associated exposure, will show up. The disclosure quantifies what WLF generated in one year; the tokens are how the story continues.

That is also why the WLF portion of the filing is politically and commercially important. It is not merely a passive investment line. It is a live Trump-linked crypto business operating in the same sector the administration is regulating. The financial disclosure does not settle the ethics question, but it gives the market a clearer picture of how large the business has already become.

The $TRUMP meme coin

The largest single income line deserves its own look. The $TRUMP meme coin launched on the Solana network just days before Trump returned to office in January 2025, and the roughly $635 million in the filing came almost entirely from royalties on a licensing agreement, routed through CIC Digital LLC and described as Celebration Coins. This is a licensing structure: the earnings are royalty income from the use of the brand and the coin, not proceeds from Trump trading the token himself. That distinction matters because it explains why the line can be so large without matching a current token balance.

The meme coin is also the clearest illustration of the income-versus-holdings point. A licensing royalty of $635 million is a payment for the use of a name and a product, and it does not imply a corresponding crypto holding. It is cash income generated by the coin’s existence and trading, flowing to the licensor. The meme coin made a great deal of money as a business line, which is a separate fact from whether the president holds a large position in the token today.

It also carries the heaviest headline risk. A politically branded meme coin is not just a crypto product; it is a financial instrument tied to a public officeholder’s name and political identity. That makes it commercially powerful and ethically sensitive at the same time. The disclosure confirms the scale of the income, but it does not make the token safer, less volatile, or less politically exposed.

The conflict-of-interest question

No honest account of this disclosure can skip the controversy, and no fair one can take a side on it. The scale of a sitting president earning more than a billion dollars from crypto ventures, while his administration pursues favorable crypto policy, has drawn sharp conflict-of-interest criticism, including from lawmakers. Some Democrats opposing crypto market-structure legislation have argued it should not pass without ethics language barring the president and his family from crypto businesses. Critics frame the overlap between Trump’s crypto income and his crypto policy as the core problem.

The White House rejects the framing. A spokesperson has said neither the president nor his family has engaged or will engage in conflicts of interest, and the Trump Organization says the assets are managed by third-party institutions with trades executed through automated technology, meaning the president does not direct the investments. The administration casts its crypto stance as promoting American innovation and economic growth rather than personal benefit. Both positions are part of the record.

The disclosure documents the numbers; whether they represent an improper conflict is a contested judgment, and this article reports the dispute without resolving it. The market implication is that the Trump-linked tokens now sit at the center of both commercial opportunity and legislative scrutiny. That scrutiny matters because the market-structure legislation remains part of the broader policy backdrop for every major crypto business in the U.S. The more directly presidential crypto interests enter that debate, the harder the politics become.

What it means for the Trump-linked tokens

For the crypto market specifically, the disclosure sharpens attention on the instruments tied to Trump: the $TRUMP meme coin, the WLFI governance token, and the USD1 stablecoin. Quantifying how much these ventures earned confirms they are significant, active businesses instead of novelties, which is relevant context for anyone assessing the tokens. Heavy political attention, regulatory debate, and the ongoing legislative fight over crypto rules all bear on how these assets trade. They now carry both market risk and political risk in a way few crypto assets do.

None of that is a reason to buy or avoid them, and this is not advice. It is a note that the tokens now carry a documented commercial and political weight that will keep them in the headlines, and that headline risk cuts both ways, drawing interest and scrutiny in equal measure. The disclosure is a data point about the ventures behind the tokens, not a signal about where their prices go. It proves the businesses generated enormous income; it does not prove the tokens are good investments.

The distinction matters most for the meme coin. A meme coin can generate royalty income for a brand owner while still being volatile, speculative, and structurally risky for traders. A stablecoin can grow as a payments product while its token remains designed to hold a dollar peg. A governance token can represent influence over a protocol without automatically producing cash flows for every buyer. The disclosure makes the businesses legible, not the token outcomes predictable.

The stocks alongside the crypto

Crypto was the headline, but it sat inside a much larger portfolio that the filing also details, and that context matters for reading the crypto numbers correctly. The disclosure lists hundreds of individual company stocks, including large purchases of Apple, Microsoft, and Nvidia, each recorded in a bracket between $5 million and $25 million, among the biggest single transactions in the document. It also follows an earlier disclosure that covered stock trades made in the first part of the year, including crypto-adjacent names such as Robinhood and Coinbase, and it references investment-account activity in companies including the private-prison operator GEO Group. The filing is not a crypto-only document; it is a broad financial map.

The timing of some trades drew attention. One reading noted that a large Nvidia purchase came shortly after an announcement affecting the company’s China revenue, the kind of overlap that fuels the conflict questions covered above. The Trump Organization has said the president does not direct these trades, which are handled by third-party managers through automated technology, a point the White House emphasizes when the timing is raised. Those denials are part of the same record as the critics’ concerns.

The broader portfolio is relevant to the crypto story because it shows the crypto income and holdings as one slice of a diversified balance sheet, not the entirety of it. The meme-coin royalty was the largest single line, but the disclosure describes a wide spread of assets, which is part of why the crypto holdings, at over $50 million in Bitcoin, look modest against the income figures and against the rest of the portfolio. For market context, the Bitcoin market context is separate from the disclosure itself: Trump’s reported Bitcoin holding is an exposure line, not a forecast for BTC.

How the picture has changed in a year

The disclosure also marks a trajectory, and the trajectory is as striking as any single number. Trump’s estimated net worth has climbed to roughly $6 billion, up from about $2.3 billion a year earlier, according to Forbes, and crypto is a central reason for the jump. In the space of a single reporting year, digital-asset ventures moved from a smaller part of the picture to among the largest income lines on the entire filing, driven by the meme-coin licensing and the World Liberty Financial token sales. That speed is the real story.

It is not just that a sitting president earned a great deal from crypto; it is how quickly crypto became a dominant contributor to a rapidly growing fortune. The pace raises the stakes of the conflict debate, because the larger and faster-growing the crypto income, the sharper the questions about the overlap with crypto policy, and the firmer the White House denials in response. It also signals that the ventures behind the numbers, the $TRUMP meme coin and World Liberty Financial, are likely to keep generating income and attention, since they are active businesses instead of one-year events. For the crypto market, the takeaway is that these instruments are now tied to a high-profile, fast-growing financial story that will keep them in the spotlight.

The year-over-year change, more than any single figure, is what makes this disclosure a marker instead of a footnote. Crypto is no longer a side interest in the financial picture. It is one of the central engines of the reported income and wealth expansion. That makes the next filings, and the policy fights around them, worth watching.

Why the disclosure matters beyond the numbers

Strip away the specific figures and the document still marks something without a clear precedent: a sitting president whose personal fortune is now deeply entangled with an industry his administration actively regulates. Historians reviewing the filing have noted that no modern president has had financial interests of comparable scale and complexity, and the crypto ventures are the sharpest example, because they sit at the intersection of the president’s private income and his public policy. That intersection is what makes the disclosure consequential regardless of where any single number lands. The size of the income turns an ethics debate into a market-structure issue.

The two readings of that fact are both worth stating plainly, because the debate is not going away. One view holds that the entanglement is a structural conflict: when the person setting crypto policy also earns enormously from crypto, the incentives are compromised no matter how the assets are managed, and disclosure alone does not cure it. The other view holds that transparency is the safeguard the system asks for, that the assets are handled by third parties without the president’s direction, and that pro-crypto policy reflects a genuine economic strategy instead of self-dealing. The Trump Organization frames the nearly thousand-page filing itself as evidence of transparency.

Critics frame the same length as evidence of how tangled the interests have become. Both can point to the same document. For the crypto industry specifically, the disclosure is a double-edged moment: it confirms that crypto has reached the highest levels of American wealth and power, while also tying the industry’s public image to a politically charged figure and an unresolved ethics fight. That scrutiny could shape the very legislation the sector is watching.

The stalled market-structure bill, and the push by some lawmakers to attach ethics language limiting presidential crypto involvement, shows how directly the president’s holdings feed back into the rules the whole industry will operate under. That feedback loop, personal holdings shaping policy that shapes the market, is the real reason this filing matters beyond its dollar figures. It is why the crypto market will keep watching how the conflict debate resolves. The filing is not only about what Trump earned; it is about how crypto money, political power, and market rules now overlap.

Frequently asked questions

How much did Trump earn from crypto in 2025?

His annual financial disclosure, released June 30, 2026, reports more than $1 billion in crypto-related income for 2025, with some outlets totaling it near $1.4 billion. The largest piece is about $635 million in meme-coin licensing royalties, and most of the rest comes from World Liberty Financial token sales and an equity sale. These are earnings figures, not a wallet balance. That distinction is the main point: the disclosure shows very large crypto income, but not a billion-dollar crypto holding.

What crypto does Trump actually hold?

The disclosure lists current holdings far smaller than the income. It shows a cold-wallet Bitcoin position valued at over $50 million, the top bracket on the form, and a smaller multimillion-dollar Ethereum position, plus ether staked through Coinbase that produced about $1.8 million in rewards. He also has exposure through the WLFI token and USD1 stablecoin tied to World Liberty Financial. The filing therefore shows a meaningful direct crypto position, but one led by Bitcoin and far below the headline income figure.

Why is the income number so much bigger than the holdings?

Because income and holdings measure different things. Income is money the ventures earned and distributed over the year, such as licensing royalties and proceeds from selling tokens. Holdings are the assets still held at period end. Selling tokens produces income while reducing holdings, and royalties are paid in cash, not held as crypto, so large earnings can leave modest holdings.

What is the $635 million meme-coin figure?

It is royalty income from a licensing agreement tied to the $TRUMP meme coin, paid through CIC Digital LLC and described in the filing as Celebration Coins. The meme coin launched on Solana just days before Trump returned to office in January 2025. The $635 million is a licensing payment for the brand and coin, the single largest line item on the entire disclosure. It is not the same as saying Trump holds $635 million of the token today.

What is World Liberty Financial?

World Liberty Financial is the Trump-linked crypto venture, co-founded by family members including Eric Trump and Donald Trump Jr., that issues the WLFI governance token and the USD1 stablecoin. It produced most of the non-meme-coin crypto income in the disclosure, roughly $515 million to $592 million across token sales and an equity sale by an affiliated entity that held a 38.25% stake. It matters because it is an ongoing token and stablecoin business, not just a one-time income line. Future WLFI and USD1 activity will shape how the story develops.

Are the disclosed figures exact?

No. Government ethics filings report values in ranges, or brackets, not exact amounts. A holding listed as “over $50 million” reflects the top bracket on the form, and the actual figure could be higher. Income line items are more specific, but the holdings figures in particular should be read as bracketed ranges instead of precise balances. That is why exact wallet-style claims should be treated carefully.

Why is the disclosure controversial?

Because a sitting president earning more than a billion dollars from crypto while his administration pursues favorable crypto policy has drawn conflict-of-interest criticism, including from lawmakers seeking ethics limits in crypto legislation. The White House denies any conflict, says the assets are managed by third parties with automated trades, and casts its crypto policy as pro-innovation. Both positions are part of the public record. The disclosure provides the numbers, while the ethics judgment remains contested.

What does this mean for the Trump-linked tokens?

It confirms that the $TRUMP meme coin, the WLFI token, and the USD1 stablecoin sit behind real, sizable businesses, which is relevant context for assessing them. It also means they carry heavy political and regulatory attention that can move sentiment in either direction. This is context, not investment advice, and the disclosure is a data point about the ventures instead of a signal about token prices. The businesses may be significant even if the tokens remain volatile and politically exposed.

Disclaimer: This article is for information purposes only and does not constitute financial, investment, or trading advice, and it takes no political position. Figures are drawn from public reporting on a government disclosure that uses bracketed ranges, and details may be revised as the filing is analyzed further. Nothing here is a recommendation to buy or sell any asset. Always do your own research and consider consulting a licensed professional before making financial decisions. Information is accurate as of July 1, 2026, and will change.

Circle co-founder and CEO Jeremy Allaire published a lengthy rebuttal on X on July 1 to the pitch behind OUSD, the stablecoin launched by the Open Standard consortium, arguing that USDC's advantages in distribution, liquidity and regulatory licensing are not easily replicated. "We've had lots of… Read the full story at The Defiant

K Wave Media has sold its remaining Bitcoin holdings, ending a short-lived treasury push that once aimed to turn the Nasdaq-listed Korean media company into a major corporate BTC holder.

Summary

- K Wave Media sold its remaining 88 BTC to repay $6 million in debt obligations.

- The company once said it wanted to expand Bitcoin holdings toward 10,000 BTC quickly afterward.

- K Wave’s filing shows it halted Bitcoin strategy while shifting focus toward AI infrastructure investments.

The sale came less than a year after the company said it had access to up to $1 billion in financing for its Bitcoin strategy.

K Wave sells 88 BTC to repay debt

In a June 30 SEC filing, K Wave said it liquidated 88 Bitcoin held in its treasury and used the proceeds to repay $6 million of Initial Notes. The transaction was tied to an April 29 amendment to its securities purchase agreement with Anson Funds.

The same filing says K Wave sold all of its Bitcoin holdings on May 6. It also says the company has not abandoned its treasury strategy, but has decided to halt it and focus on AI infrastructure. That shift puts its Bitcoin balance at zero after it once marketed itself as a Korean media company with a Bitcoin-backed treasury model.

Company once aimed for 10,000 BTC

K Wave’s exit marks a sharp turn from its July 2025 announcement. At the time, the company said it had secured $1 billion in total capital capacity through a $500 million convertible note agreement with Anson Funds and a $500 million standby equity purchase deal with Bitcoin Strategic Reserve.

The company said it had completed an initial purchase of 88 BTC and planned to scale its holdings.

“Our objective is clear: to scale our holdings toward 10,000 Bitcoin as soon as possible,” said CEO Ted Kim.

The company also said at least 80% of net proceeds from the first Anson tranche had to be used to buy Bitcoin.

AI strategy replaces Bitcoin plan

K Wave later changed course. As previously reported, K Wave redirected up to $485 million from its Bitcoin treasury plan toward AI infrastructure, including data centers, GPU compute operations, and possible acquisitions. Its shares fell about 25% after that update.

The SEC filing adds more detail to that pivot. K Wave said it has started a strategic transformation toward AI infrastructure and is pursuing data centers, GPU clusters, AI cloud platforms, power systems, cooling systems, and related technology assets. The company also expects shareholders to consider the planned sale of Play Company and the disposal of its Solaire stake.

K Wave is also dealing with Nasdaq compliance issues. The filing says Nasdaq notified the company in January that its shares failed to meet the $1 minimum bid rule. Nasdaq sent another notice in June after the company failed to meet the required $15 million market value of publicly held shares.

Treasury firms face wider pressure

K Wave’s move adds to stress across the digital asset treasury sector. As crypto.news reported, Sequans sold half of its Bitcoin as debt pressure tested its treasury plan. That report also cited K Wave’s earlier Bitcoin-to-AI shift as another case of public firms rethinking BTC reserves.

The wider model has also come under review. Crypto.news explained that Bitcoin treasury companies often depend on investor demand, share premiums, and access to fresh capital. When those conditions weaken, debt and dilution can make the structure harder to maintain.

Previously, crypto.news reported that Strive’s Ben Werkman warned that a long Bitcoin downturn could force some treasury firms to restructure, especially those that relied on convertible debt. K Wave’s sale shows how a company can move from an aggressive BTC target to debt repayment and a new business focus within one year.

Bitcoin ended June at $58,526, sliding 20.5% over the month and recording its weakest monthly performance since June 2022. The retreat left the flagship cryptocurrency trading below its 200-week moving average near $62,000, but still above a key on-chain valuation metric known as realized price (around $52,000), a configuration that some analysts interpret as a warning that the market may not have reached a full bear-market bottom.

Crypto analyst PlanB, creator of the stock-to-flow pricing model, argued that this price positioning matters because previous bear-market troughs occurred below realized price. In a post shared this week, PlanB said the setup suggests Bitcoin’s downside could continue, potentially revisiting the realized-price area and beyond.

Key takeaways

- Bitcoin’s June close at $58,526 placed it below the 200-week moving average (about $62,000) while remaining above realized price (~$52,000).

- PlanB says earlier bear-market bottoms formed below realized price, implying the market may still be searching for its bottom.

- Analysts at Bitrue Research Institute and Bitget Wallet both described the June-to-$60,000 region as a developing bottom zone, but with risk of further drawdowns.

- Benjamin Cowen suggested Bitcoin may see a cycle-bottom window tied to the US midterm election year, historically aligning with accumulation phases in 2018 and 2022.

Why June’s “in-between” level is drawing attention

PlanB’s argument centers on what he views as the relationship between price and realized price during bear markets. According to the stock-to-flow analyst, Bitcoin’s historical bear-market bottoms have not simply arrived after price fell below major moving averages; they also tended to appear after price moved to levels beneath realized price.

In earlier posts, PlanB highlighted that if Bitcoin breaks down below realized price, it would align with that prior pattern. He referenced the possibility that Bitcoin could fall to $52,000, which would correspond closely with realized price.

From an investor perspective, this distinction can be important because realized price is often used as an on-chain proxy for the average cost basis of coins in circulation. When market price trades above realized price, the market may still be able to bounce; when it slips below, the distribution of holders’ costs versus current valuations tends to become more unfavorable, which can prolong bearish conditions.

Realized price explained—and what it signals

Realized price is calculated by valuing all Bitcoin outputs (typically discussed in terms of unspent transaction output or UTXO cohorts) at the price when each coin last moved on-chain. The result is an aggregate measure of the average acquisition price for the existing supply.

Because realized price reflects holder cost basis, it is frequently used to identify potential support areas during downtrends. The idea is that when price is substantially below realized levels, the market is effectively pricing Bitcoin below what many holders paid when they last moved coins, which can coincide with capitulation phases and supply shakeouts.

Against that backdrop, June’s outcome—still above realized price but no longer above the 200-week moving average—has led analysts to frame the current range as transitional rather than conclusive.

Analysts see a bottom developing, but not confirmed

Andri Fauzan Adziima, research lead at Bitrue Research Institute, told Cointelegraph that Bitcoin’s June close carried a signal consistent with prior cycles. He said the month’s finish above realized price but below the 200-week moving average “signals the bear bottom is still ahead per prior cycles.”

Adziima added that he is watching for a potential capitulation period in late 2026 before a subsequent move higher—while also arguing that the decline could be shallower this cycle due to the role of institutions.

Meanwhile, Lacie Zhang, research analyst at Bitget Wallet, characterized the current consolidation around $60,000 as an area that may be approaching a bottom. She told Cointelegraph that if further downside occurs, the market could build “strong historical and technical support” around $55,000.

Taken together, these views reflect a common tension in market bottoms: technical indicators and on-chain benchmarks can both suggest stabilization, yet neither can confirm capitulation has fully played out. In this case, the “middle” positioning—between the 200-week moving average and realized price—is leaving room for additional volatility before a more durable floor forms.

Cycle-bottom theory tied to US midterms

Beyond on-chain valuation levels, some analysts are also looking at macro calendar effects. ITC Crypto founder Benjamin Cowen speculated that Bitcoin may see a cycle bottom this year, pointing to the fact that it is a US midterm election year.

Cowen argued that the second half of midterm years often marks an accumulation zone and a market cycle bottom, noting that such timing previously coincided with bear market bottoms in 2018 and 2022. The next US midterms are scheduled for Nov. 3, with all House of Representatives seats and about a third of Senate seats up for election.

While this framing is not the same as a realized-price breakdown model, it can influence how traders time risk—particularly when they treat the calendar as a factor that shapes liquidity and positioning. Investors watching this thesis would likely focus on whether Bitcoin’s downtrend stabilizes into accumulation rather than continuing to grind toward or below realized price.

For now, the key takeaway from all perspectives is that June’s close did not neatly resolve the debate. Bitcoin is weak enough to be below its long-term trend proxy, but it has not yet fallen to the on-chain valuation zone that PlanB says has marked prior trough formation.

Traders and long-term holders will likely watch whether Bitcoin can hold above realized price around $52,000 and whether weakness extends toward $55,000 support. The market’s next step—whether it stabilizes into accumulation or breaks below realized valuation—may determine if this is merely consolidation or the start of a more complete bear-market bottom.

Crypto World

ENS Community Member Proposes Dissolving DAO After Founder Blocks Security Council Renewal

Christoph Jentzsch proposed on X that ENS DAO dissolve itself rather than continue operating under what he called a broken governance structure. "As it seems, the ENS DAO is broken," he wrote. "I would propose turning this into a win, by actually dissolving it. Its goals have been accomplished, the… Read the full story at The Defiant

Solana Foundation has introduced Solana Governance Proposals, a new onchain process for validators to move major network questions into stake-weighted votes.

Summary

- Solana validators can now move core governance questions into stake-weighted onchain votes through SGPs directly.

- A proposal needs 15% active stake support before it can enter formal network voting period.

- Validators need at least 100,000 SOL delegated to take an SGP onchain under current rules.

The system gives validators a formal route to submit, support, and decide governance items that may shape Solana’s future protocol direction.

Meanwhile, the Solana Governance Proposals repo says SGPs are documents proposed by Solana validators for stake-weighted, onchain voting through the svmgov program. The process is for high-level questions that ask whether the network should move in a certain direction, rather than detailed technical changes. This keeps SGPs focused on broad network direction only.

A validator vote account needs at least 100,000 SOL staked to take an SGP onchain. The proposal then needs support from at least 15% of active stake before it can enter voting. The Solana Governance documentation says validators create proposals, other validators support them, and voting weight is proven through Merkle proofs against an onchain stake snapshot.

The process separates signals from code

The SGP process sits beside Solana Improvement Documents, which cover detailed protocol design. In simple terms, SGPs ask whether Solana should pursue a direction, while SIMDs explain how a change would be built. The repo says, “A ‘yes’ on an SGP is a mandate to proceed.”

The lifecycle moves from idea to draft, support, voting, acceptance, and activation. Once a proposal reaches the 15% support threshold, it enters a fixed 11-epoch process. That includes seven epochs for discussion, one epoch for a Node Consensus Network snapshot, and three epochs for voting.

There is no quorum rule. A proposal passes only if “For” votes reach at least 66.67% of “For” plus “Against” stake. The repo also says SGPs are not mandatory for every technical change. If validators do not reach support, developers can continue through normal SIMD review.

Governance arrives as upgrades continue

The launch comes as Solana continues to test large infrastructure changes. As previously reported, the Alpenglow upgrade entered community validator testing in May. Alpenglow aims to cut confirmation times to about 150 milliseconds and remove Proof of History and onchain vote transactions from Solana’s core process.

The new SGP route could give validators a clearer way to request network-wide direction before developers prepare technical work. The GitHub repo uses Alpenglow as an example of a proposal that could have first taken a directional vote before later SIMDs defined the build path. That example shows how Solana may use SGPs when validator input is needed before engineering details are complete.

Recent Solana activity adds context

Solana’s validator set has also been tied to other recent network tools. As crypto.news reported, DoubleZero launched Edge in April with 379 validators publishing shreds and about 43% of Solana’s total stake covered at launch. The project aims to deliver Solana block data through private fiber paths.

Solana has also seen renewed market activity around network use. Crypto.news reported that Solana’s tokenized stock activity helped drive an 18% weekly SOL rebound in late June. Earlier, crypto.news reported that Galaxy Digital proposed a voting model for Solana inflation, showing that validator voting design has already been part of the network’s policy debate.

Türkiye-based digital asset platform Paribu has launched DeFi access inside its main app, adding DEX trading, perpetual contracts through Hyperliquid, and Polymarket-linked option markets.

Summary

- Paribu now offers Hyperliquid perpetuals and Polymarket markets through its main self-custodial DeFi app section.

- The platform opened a waitlist for NYSE, Nasdaq, and Borsa Istanbul stock trading access soon.

- Paribu says users can trade DeFi products without separate wallet apps, seed phrases, or transfers.

The company also opened a waitlist for stock trading as it works to combine crypto, DeFi, yield products, and equities in one app.

Paribu said it is the first regulated exchange to offer both Hyperliquid perpetuals and Polymarket option markets through a centralized exchange interface. Users can access the DeFi section with their existing balance, without a separate wallet app, seed phrase, or new account. The company said each DeFi position remains self-custodial, while trades settle onchain through linked protocols.

DeFi access targets Türkiye’s retail market

Paribu framed the launch around Türkiye’s active crypto market. The company cited TRM Labs data showing Türkiye ranked fifth globally in retail crypto activity, with $40 billion in volume in Q1 2026. The figure rose 7% year over year while global retail crypto volume fell 11%.

The company said many local retail users keep their main crypto holdings inside one app and have not used DeFi wallet tools. Paribu’s DeFi access is designed to let these users reach onchain markets without switching platforms. Its blog post on DeFi access says the wallet setup uses passkeys and recovery tools instead of seed phrases.

Hyperliquid and Polymarket enter the app

The Hyperliquid integration lets Paribu users trade perpetual contracts from the DeFi section of the app. Trades route to Hyperliquid’s decentralized blockchain, while positions remain in users’ self-custodial wallets. Paribu said Hyperliquid has processed more than $4 trillion in cumulative trading volume.

The launch follows wider activity around Hyperliquid. As reported by crypto.news, Kalshi launched CFTC-regulated HYPE perpetual futures, lifting HYPE futures open interest to $2.48 billion. Moreover, crypto.news reported thatHyperliquid added validator-settled outcome markets under HIP-4, expanding beyond perpetual futures.

Paribu also added access to Polymarket markets through the same DeFi section. The company said it will list curated markets only, with each contract reviewed for integrity, liquidity, and risk profile before appearing in the app. Paribu serves as the interface, while execution and settlement happen onchain through Polymarket infrastructure.

The rollout comes as prediction markets face closer review in several jurisdictions. As crypto.news reported, the CFTC is preparing new rules that could affect Polymarket and Kalshi. Crypto.news also reported that the CFTC sued Kentucky to block state action against Kalshi, Polymarket, and related partners.

Stock trading remains pending

Paribu is also preparing to offer equities. Its brokerage arm has received establishment authorization from Türkiye’s Capital Markets Board and is waiting for an operating license. The company said NYSE, Nasdaq, and Borsa Istanbul stocks will become tradable after the license process is complete.

For now, users can view real-time market data for U.S. and Turkish stocks inside the app. Paribu said the stock waitlist is open before trading goes live. Founder and CEO Yasin Oral said, “Paribu is becoming a single app for all of finance: crypto, DeFi, equities, and yield.”

The expansion follows other Paribu moves. Previously, crypto.news reported that Paribu’s $240 million CoinMENA acquisition led a weekly crypto funding period in December 2025. The company has also said Clave joined Paribu in 2026 to support passkey-based account abstraction and self-custody tools.

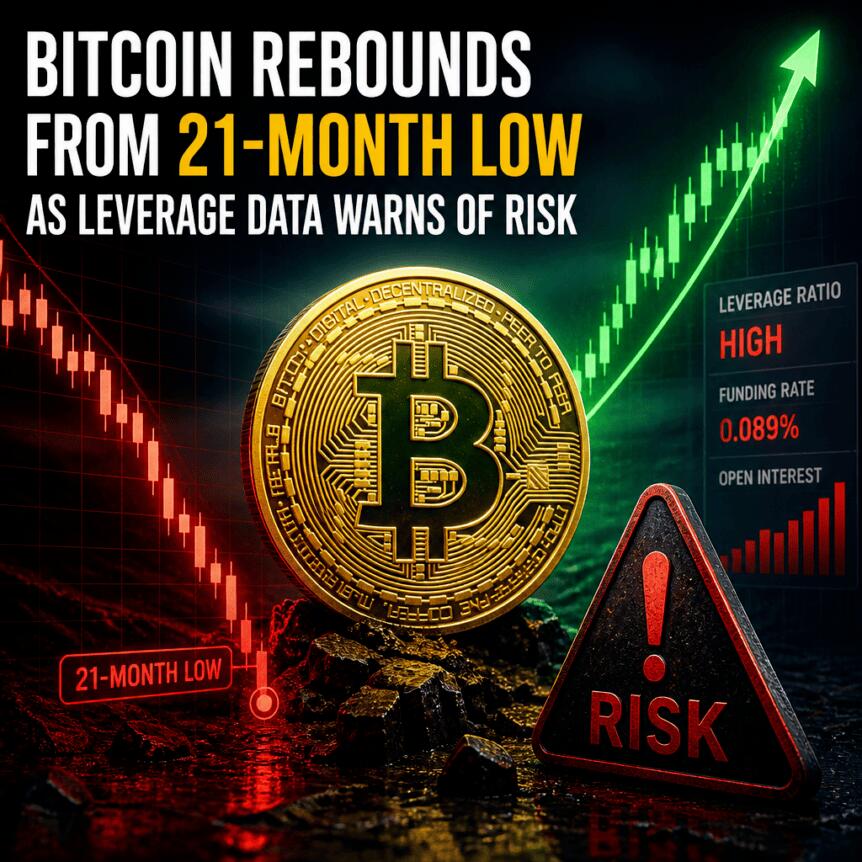

Bitcoin rebounded on Wednesday after tagging a 21-month low, with BTC rising as high as $60,200 and gaining roughly 2.7% over the past 24 hours from earlier losses. The bounce lifted major alternatives as well: Ether (ETH) rose about 3%, while Solana (SOL) climbed roughly 4.85%.

Still, the recovery is happening against a backdrop of persistent caution. According to the Crypto Fear & Greed Index maintained by Alternative.me, sentiment is around 11 out of 100—an “Extreme Fear” reading—suggesting many market participants remain nervous about what comes next. Even with today’s uptick, Bitcoin is still down about a third since the start of the year.

Key takeaways

- Bitcoin’s intraday bounce followed a fresh 21-month low near $57,737, but broader confidence remains weak with the Fear & Greed Index in “Extreme Fear.”

- US spot Bitcoin ETF flows have been net negative recently, including a reported $4.5 billion outflow in June—the largest since the funds launched—indicating cautious institutional positioning.

- On-chain data points to strength from long-term holders, with an estimated addition of roughly 270,000 BTC over the past two weeks.

- Funding rates have stayed positive for three straight days, implying leverage is still leaning toward long exposure even as price remains under pressure.

- Liquidation risk appears heaviest in the $57,000 to $60,500 band, meaning sustained moves beyond roughly $61,000 or below $56,000 could accelerate volatility.

Fear remains elevated even after the rebound

Market pricing today reflects a tug-of-war between dip-buyers and the fear of further downside. The latest sentiment readings underline that many traders are still operating defensively, despite Bitcoin’s recovery attempt from the yearly low area.

This matters because fear can shape how quickly the market absorbs negative news. When sentiment is extremely negative, rebounds often face selling pressure not just from those who missed the decline, but from participants who are using rallies to reduce risk. The result is a market that can rally sharply—then struggle to build follow-through.

ETF outflows versus long-term accumulation

One of the clearest contrasts in the data is between institutional product flows and on-chain holder behavior.

US spot Bitcoin exchange-traded funds (ETFs) have seen more money leaving than entering in recent weeks, including a reported total outflow of $4.5 billion in June, described as the largest since the funds began launching. That pattern typically suggests that, at least for now, some traditional investors are not convinced enough to add exposure during a drawdown.

At the same time, on-chain indicators show long-term holders accumulating. According to the on-chain data referenced in the analysis, long-term wallets added about 270,000 BTC over the past two weeks. In crypto market interpretation, that kind of accumulation is often read as evidence that bigger investors view the recent decline as an opportunity rather than a prompt to sell.

The tension between these two signals—net outflows from ETFs versus accumulation by long-term holders—helps explain why the market can bounce without fully transitioning into a sustained uptrend. Flows may stay cautious while deeper capital continues to build positions more quietly.

Funding rates stay positive as leverage crowds in

Another point to watch is leverage. The analysis highlights that Bitcoin’s funding rate has remained positive for three consecutive days. In practical terms, that means the prevailing derivatives positioning has continued to lean toward bets that prices will rise.

Positive funding while spot prices are weak can be a volatility risk. When one side of the market becomes overcrowded with leveraged longs, a further downside move can force liquidations that amplify the drop—especially if price breaks key support levels. Conversely, if the market stabilizes or turns upward while longs remain funded, the same mechanism can also support rallies through short-covering and stop-trigger effects.

As of now, the key point is that leverage appears active, but price confirmation has not yet clearly followed through in a way that would suggest the market has fully flipped from fear to conviction.

Liquidations cluster around current trading levels

Where liquidation risk sits is often central to understanding how quickly price can move during stressful periods. Using a three-exchange, three-day liquidation heatmap (as cited in the analysis, sourced from Hyblock), the highest concentration of leveraged positioning appears roughly between $57,000 and $60,500. That zone closely overlaps with the trading range Bitcoin has held since late June.

Above that area, the density of liquidation risk thins out noticeably between approximately $61,000 to $62,000. Below, a similar reduction appears around $55,000 to $56,000. This distribution suggests that a move breaking out of the present range could encounter less immediate “magnet” pressure from nearby liquidations—while a move that stays within or slightly beyond the clustered zone could lead to sharper, more abrupt price reactions.

In the near term, the analysis argues that most forced unwind potential sits close to current prices rather than far away. That is why decisive movement beyond roughly $61,000 to the upside—or below about $56,000 on the downside—could create room for accelerated liquidation-driven volatility.

Looking ahead to the next 24 hours, the outlook described here is neutral. A meaningful change would likely require stronger evidence that leveraged positioning is both rising and aligning with a rising spot price—an interaction the analysis notes has not clearly emerged yet.

Traders and investors should monitor whether ETF flow weakness persists alongside continued long-term accumulation, and whether derivatives conditions evolve—particularly funding rate direction and liquidation clustering—as these factors together will determine whether this bounce becomes a trend or fades back into range-bound action.

Venice AI, the privacy-focused AI platform founded by Erik Voorhees, has raised $65 million in Series A funding at a $1 billion valuation, bringing the company to “unicorn” status. The round—led by Dragonfly and backed by Coinbase Ventures, F-Prime, North Island Ventures, Morgan Creek and others—was announced on Wednesday, and represents Venice AI’s first outside capital raise since it launched in 2024.

The funding arrives as privacy concerns around mainstream AI services are drawing renewed attention. Earlier this month, Anthropic cut off foreign access to two of its latest models, and in the broader public debate over AI data handling, a class-action lawsuit recently accused OpenAI of sharing ChatGPT data with third parties. Against that backdrop, Venice AI positions itself as a layer between users and model providers, designed to reduce what third parties can see about user activity.

Key takeaways

- Venice AI reached unicorn status after closing a $65 million Series A round at a $1 billion valuation, led by Dragonfly.

- The platform claims 3.5 million users and routes traffic through a proxy that can obscure IP address and user/account/session data from model providers.

- Venice AI says the new capital will fund more of its own infrastructure, including owning GPUs via data center expansion rather than relying entirely on rental capacity.

- The announcement lands amid heightened scrutiny of AI data privacy, including legal claims involving tracking technologies and alleged sharing of user information.

Unicorn funding for a privacy-first AI delivery layer

Venice AI’s Series A funding was announced by the company in a blog post published Wednesday, with Erik Voorhees describing the company’s mission in constitutional terms in a separate X post. Voorhees said the funding will be used to uphold the First and Fourth Amendments “as they relate to mankind’s interaction with AI.” In the U.S. legal framework, the First Amendment protects core freedoms including speech, while the Fourth Amendment restricts unreasonable government searches and seizures.

While the fundraising headlines focus on valuation and total capital, the more meaningful detail for potential users is the product model: Venice AI’s platform is built to act as an intermediary between a user and over 200 AI models. According to the company, users can choose the level of privacy they want, with different models routed through different privacy protections.

How Venice AI says it protects user data

Venice AI claims it has 3.5 million users. For models associated with OpenAI, Anthropic, xAI and Google, Venice AI says its proxy obscures users’ IP address as well as account and session data. The company also claims “other models offer higher levels of privacy,” indicating that its approach is not one-size-fits-all and may vary depending on which model is being accessed.

The core premise is that owning (or controlling) the “delivery stack” matters: if the intermediary is the part that can see traffic patterns and data flows, then that component can potentially reduce exposure to outside entities that operate the underlying model endpoints. Dragonfly managing partner Haseeb Qureshi framed the strategic stakes in those terms, arguing that whoever runs the AI delivery layer can see more about users’ behavior and ultimately influences the conditions under which users get access to powerful systems.

Where the $65 million will go

Voorhees said the Series A funding will be used to continue building Venice AI’s data center infrastructure. A central element of that plan is ownership of the compute resources—specifically, owning GPUs that power the platform—rather than renting them at higher costs.

Beyond infrastructure, Voorhees said remaining capital will support growth initiatives including expanding the customer base, entering new markets, hiring talent, and acquiring what he described as “additive businesses.” The acquisition language suggests Venice AI may be looking to broaden capabilities around its platform, though no specific targets were named in the materials provided.

Privacy scrutiny pushes privacy-focused AI into focus

Venice AI’s funding timing underscores how quickly privacy questions have become a defining topic for AI adoption. Earlier coverage from Cointelegraph reported that a user who consults an AI for legal matters could face the risk of chat logs being used against them in court. The broader theme is that AI interactions can generate sensitive records—even if users are not providing personal data intentionally.

In parallel, researchers and industry figures have proposed technical approaches to limit exposure. For example, the Ethereum Foundation’s AI lead Davide Crapis and Ethereum co-founder Vitalik Buterin proposed using zero-knowledge proofs and other techniques to help ensure that a user’s interactions with large language models are kept private.

Legal concerns have also intensified. In May, a proposed class action was filed in California federal court accusing OpenAI of disclosing private ChatGPT user data to third parties including Google and Meta. The complaint alleged that Meta Pixel and Google Analytics were embedded into ChatGPT.com, so that when users send queries, duplicate data is allegedly sent to Meta and Google along with advertising cookies and personally identifiable information—information that could then be used for targeted advertising.

These developments highlight a tension for users: modern AI platforms often involve multiple layers of data collection, analytics, and third-party integration, which can be difficult to disentangle from “model inference” itself. Venice AI’s proxy concept is an attempt to restructure that data path by introducing a dedicated intermediary that can obscure certain identifiers from model providers.

The recent industry shifts also reinforce why an intermediary approach is gaining attention. Anthropic’s sudden reduction in foreign access to two of its latest AI models earlier this month served as another reminder that availability and access controls can change quickly—while privacy-focused architectures aim to give users more predictable control over how their data is handled.

What to watch next

With Venice AI scaling its infrastructure and expanding adoption, the key question for investors and users will be how effectively its proxy-based design delivers measurable privacy protections across a wide set of models and real-world integrations. Readers should watch for more transparency around which metadata is obscured under each privacy mode, and whether Venice AI’s compute buildout translates into faster, more consistent performance without sacrificing its stated privacy goals.

The Erik Voorhees-founded Venice AI has achieved unicorn status after raising $65 million in Series A funding at a $1 billion valuation.

Led by Dragonfly and with backing from Coinbase Ventures, F-Prime, North Island Ventures, Morgan Creek and others, the funding round announced on Wednesday marks the company’s first external capital raise since launching in 2024.

The fundraising came in the same month Anthropic was forced to suddenly cut foreign access to two of its latest AI models, and comes just weeks after OpenAI was accused in a class-action lawsuit for sharing ChatGPT data with third parties, highlighting the potential appeal of privacy-focused AI platforms.

“This capital will be used to uphold the First and Fourth Amendments to the Constitution as they relate to mankind’s interaction with AI,” Voorhees said in an X post on Wednesday.

The First Amendment is part of the United States Constitution protecting five essential freedoms including the freedom of speech. The Fourth Amendment protects people from unreasonable searches and seizures by the government.

Venice AI courts privacy-focused users

Venice AI, which claims to have 3.5 million users, offers access to over 200 AI models but adds a proxy between the user and the models and allows users to choose the level of privacy they want.

For models from OpenAI, Anthropic, xAI and Google, the proxy obscures users’ IP address, account and session data. Other models offer higher levels of privacy.

Source: Erik Voorhees

“Control over intelligence is the defining fight of the coming decade,” Haseeb Qureshi, managing partner at Dragonfly, said on Wednesday.

“Whoever owns the AI delivery stack owns a direct window into your interior life. They log all your chats, train on them, and will hand them over when asked. And in the end, they decide the terms on which you’ll get to access the most powerful systems humankind has ever built.”

Voorhees said the capital will be used to further build out its own data center infrastructure, owning the GPUs that power its platform rather than being forced to rent them at higher costs.

The remaining capital will be used to grow its customer base, enter new markets, hire talent and acquire “additive businesses,” he added.

Venice Token rose 6% on Wednesday. Source: X

AI privacy concerns in spotlight

The capital raise comes amid mounting concerns over user privacy when using AI models.

Earlier this year, lawyers told Cointelegraph that a user consulting an AI for legal matters could have their chat logs used against them in court.

Related: AI’s power crunch turns Bitcoin miners’ grid access into an asset

In February, Ethereum Foundation AI lead Davide Crapis and Ethereum co-founder Vitalik Buterin proposed a way to use zero-knowledge proofs and other methods to ensure that a user’s interactions with large language models are private.

Conversations about privacy when using AI were stirred again in May, when a proposed class action was filed in California federal court accusing OpenAI of disclosing private ChatGPT user data to Google and Meta.

The complaint alleged that OpenAI embedded Meta Pixel and Google Analytics into the ChatGPT.com website, so that when a user sends a query, the website allegedly sends duplicate data to Meta and Google alongside advertising cookies and personally identifiable information, which is then used to target advertisements to the user.

Magazine: Bitcoin slides to $58K, XRP hits $1 but onchain data promising: Market Moves

Meta’s plan to sell surplus computing power hit chip stocks hard on Wall Street. Meta’s own shares climbed nearly 9% on the news.

The announcement flipped years of assumed AI compute scarcity into a supply warning. It erased billions in semiconductor and neocloud value in a single session.

A Supply Signal Rattles Wall Street

Meta is building a business called Meta Compute. The unit will lease idle data center capacity to outside clients. The approach mirrors SpaceX’s model. SpaceX has rented spare capacity to firms including Anthropic.

For years, investors rewarded chip suppliers on one premise. They believed AI demand always outstripped supply. Meta’s admission of excess capacity broke that premise. Recent Nvidia institutional money flow data already show large investors pulling back.

Micron sank more than 10% on July 1. SanDisk, Intel and AMD each lost between 6.9% and 10.6%. Nvidia slipped just 1.25%, a modest decline that stood out against the broader rout.

Neoclouds and Big Tech Diverge

CoreWeave and Nebius rent GPU capacity to AI developers and saw their stocks fall 14% and 17% respectively on fears that Meta will undercut their pricing.

Meta has paid for similar cloud services before, but its shift into the same business now puts it in direct competition with its own vendors.

Other Magnificent 7 members gained ground. Apple, Microsoft, Amazon, Alphabet and Tesla all closed higher as some strategists link the split to AI spending cycle winners rotating away from pure hardware plays.

South Korea Feels the Spillover

The sell-off spread to Asia as Samsung and SK Hynix memory stocks fell more than 7% and 9% respectively in early trading and the KOSPI triggered another trading halt. The move extended a pattern from a prior Big Tech selloff spillover that hit Asian chipmakers earlier this year.

The post Meta Compute Launch Sends AI Compute Stocks Tumbling Globally appeared first on BeInCrypto.

Insiders Made $100 Million on China Brokerage Crackdown, Trading Firm Alleges

Circle CEO Rebuts OUSD Pitch, Defends USDC's Network Effects After Stock Slide

Taylor Frankie Paul ‘Trying to Avoid Pain’ Amid Dakota Drama

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics6 days ago

Politics6 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World2 days ago

Crypto World2 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics6 days ago

Politics6 days agoPotential 2028er World Cup attendee leaderboard

-

Business6 days ago

Business6 days agoAsia stock markets slide as tech shares slump

-

News Videos3 days ago

News Videos3 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech6 days ago

Tech6 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World6 days ago

Crypto World6 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World5 days ago

Crypto World5 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business2 days ago

Business2 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World5 days ago

Crypto World5 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports5 days ago

Sports5 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World6 days ago

Crypto World6 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech4 days ago

Tech4 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech2 days ago

Tech2 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Tech5 days ago

Tech5 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World6 days ago

Crypto World6 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World6 days ago

Crypto World6 days agoRTX holders must register wallets before token distribution begins

-

Sports16 hours ago

Sports16 hours agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Business2 days ago

Business2 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

You must be logged in to post a comment Login