Crypto World

X Head of Product Teases New Launch to Address Crypto’s Rough Year

X Head of Product Nikita Bier suggested the platform could launch a crypto-focused product, posting that “crypto has had a rough year” and that X should “launch something to fix it.”

While nothing has been officially confirmed, the post quickly drew responses from prominent community members pitching specific integration ideas. Fred Krueger responded to Bier’s post, calling for native Bitcoin (BTC) support on X.

Another user argued that paying creators in USDC stablecoin would improve the experience for both content producers and the platform.

These responses reflect a growing appetite among X’s crypto-native user base for deeper digital asset functionality.

Smart Cashtags and Trading Infrastructure

X has already taken concrete steps toward crypto-adjacent features. On February 14, Bier announced Smart Cashtags. This tool would let users trade stocks and crypto directly from the X timeline. The feature builds on X’s existing cashtag indexing system.

Previously, there was growing speculation that crypto functionality could be integrated into the X Money service, but the platform has not yet confirmed any such plans.

Furthermore, X appointed Benji Taylor as its new Design Lead in March. Taylor previously served as Chief Product Officer at Aave Labs and as the lead designer at Coinbase’s Base network.

His blockchain-heavy background has been widely interpreted as a signal that X is preparing to integrate crypto more deeply into its product stack.

Whether Bier’s post was a genuine product tease or simply community engagement, the convergence of Smart Cashtags, Taylor’s hire, and X Money’s development suggests the platform’s crypto ambitions may be advancing on multiple fronts.

The post X Head of Product Teases New Launch to Address Crypto’s Rough Year appeared first on BeInCrypto.

Bitcoin (BTC) has slipped about 6.5% from a recent peak that briefly topped $82,000, as a confluence of bearish technical signals, waning demand and rising selling pressure clouds the short-term outlook. Traders and analysts say the pullback comes after BTC failed to sustain momentum beyond the key level near $82k, with price action trapped within a price channel that has guided moves since February.

Key takeaways:

- BTC faces a risk of sliding toward $72,000 as momentum remains negative on higher timeframes.

- BTC inflows into Binance have risen for multiple consecutive days, signaling mounting selling pressure and cooling investor confidence.

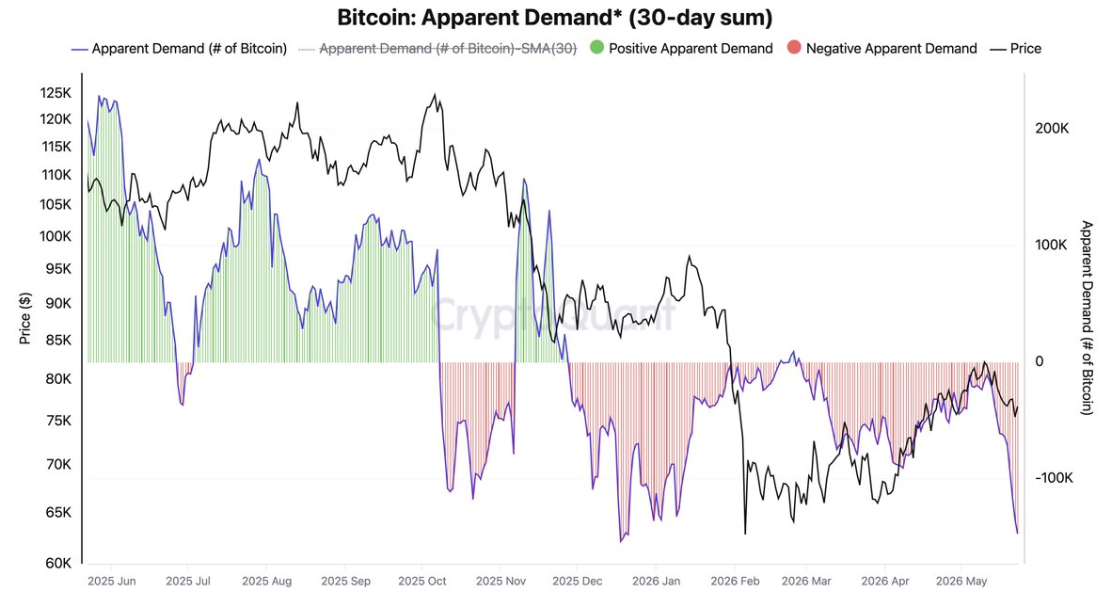

- Bitcoin’s apparent demand has weakened to its 2026 lows, suggesting downside risk unless spot demand recovers in the coming weeks.

Bearish setup tightens around key levels

Analysts note that Bitcoin’s failure to hold above crucial support levels points to difficulty in sustaining an upturn. As one observer put it, BTC has “officially lost the 100 and 50-day EMA,” signaling that the local market structure has shifted back toward a bearish configuration. The broader commentary emphasizes that macro conditions have deteriorated, helping to sap momentum and leaving any bounce unconfirmed as of now.

The rejection at the $82,000 zone aligns with the upper boundary of an ascending parallel channel that has defined price action since early in the year. Historical patterns suggest that each time BTC hits this trend line and fails to penetrate it, the price has tended to pull back meaningfully, often to the channel’s lower boundary. If that dynamic repeats, a target near $72,000—roughly 13% below the upper boundary—remains on the near-term radar, with the lower edge providing a potential support zone around that level.

Several prominent voices highlighted the risk. One analyst noted that the market’s impulse faded as macro conditions worsened, describing the current environment as risk-off and remarking that every bounce needs additional confirmation. Another trader pointed to a pattern where losses can accelerate if key support fails to hold, underscoring the potential for renewed downside toward the mid-$70,000s and below.

Beyond the price channel, a broader view places emphasis on the importance of a critical zone around $75,000–$76,000. According to market participants, losing this neighborhood could open the door to a test of the next defensive levels at approximately $74,000 and $71,400, with some forecasting the possibility of revisiting the 2026 lows around $60,000 if downside pressure intensifies and selling accelerates.

There is also a contingent view that a renewed push above the $80,000 mark could occur if geopolitical headlines shift quickly and a “peaceful” development emerges in the Middle East. Such a narrative would be a stark contrast to the current risk-off mood but remains contingent on fresh catalysts and observer sentiment.

Demand signals point to a tougher road for a durable rally

Bitcoin’s demand signals have deteriorated as on-chain metrics align with a more cautious stance among market participants. The risk index tracked by Swissblock recently re-entered a “high-risk” territory, a sign that selling pressure is increasingly challenging to absorb, though it does not by itself confirm a breakdown. The takeaway for traders is that a sustained rally would require stronger immediate demand to absorb supply at current and near-term price levels.

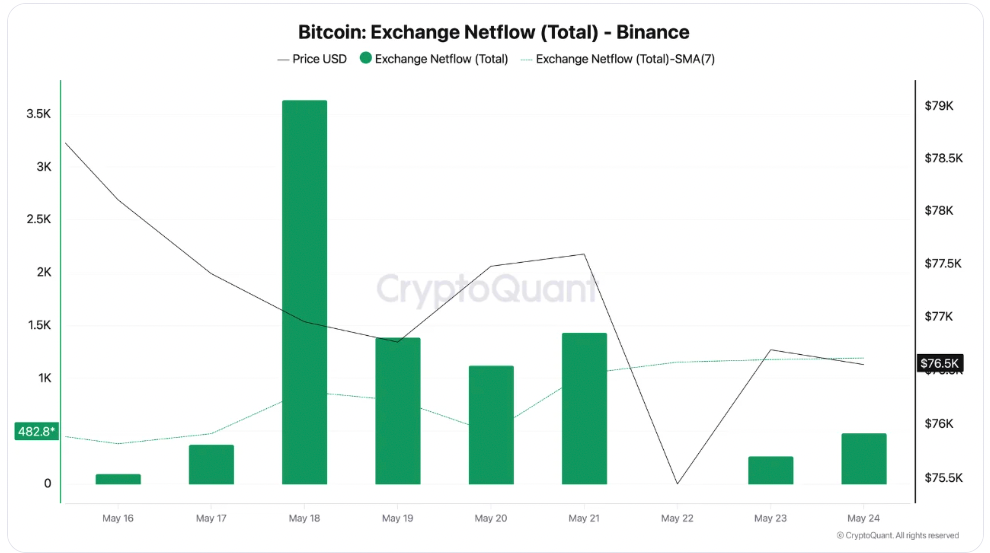

Demand dynamics are further echoed by exchange flow data. Net BTC inflows into Binance have persisted for nearly a week, with the weekly average rising to around 1,190 BTC from roughly 378 BTC just two weeks earlier. CryptoQuant analysts caution that persistent inflows can be interpreted as a seller-ready signal—advancing the notion that holders may be transferring BTC to exchanges in preparation for profit-taking, reducing exposure, or repositioning portfolios in a risk-off environment.

On-chain demand metrics show a more sobering picture. BTC’s apparent demand has hovered around negative territory, roughly -147,000 BTC, marking its weakest reading since late 2025. Analysts note that such a deterioration in demand, if not offset by a meaningful rebound in spot buying, makes a durable rally harder to sustain. As one strategist observed, the absence of a strong demand recovery in the spot market complicates the possibility of a sustainable upside breakout.

These patterns come amid ongoing discussions about external demand drivers, including the broader ETF landscape. In recent coverage, Cointelegraph highlighted that weakness in spot demand, combined with rising ETF outflows, compounds the risk of prolonged consolidation or a slide toward the mid-$60,000s in a downside scenario. While ETF flows can shift rapidly with new product launches or regulatory developments, the current trajectory adds a layer of caution for bulls hoping for a swift, durable revival.

What investors should watch next

The immediate line in the sand remains the $75,000–$76,000 region. A daily close below that zone keeps the risk of a deeper pullback intact, potentially inviting a test of the channel’s lower boundary near $72,000 and even lower if selling accelerates. Conversely, a sustained hold above the zone could set the stage for a cautious re-entry into bulls’ territory, though confirmation would likely require a combination of firmer demand signals and a respite in exchange inflows.

Analysts are also watching how macro news and geopolitical developments might tilt the balance. A major complicating factor is the potential influence of external events on risk appetite, which can either reinforce the current bearish tilt or catalyze a renewed bout of buying if headlines shift favorably and liquidity conditions improve.

In the near term, traders should be prepared for continued volatility as BTC negotiates the crosscurrents of technical resistance, fading on-chain demand and persistent exchange flows. The balance of risk is skewed toward downside unless a meaningful demand pickup materializes and sellers step back from the market.

What happens next will hinge on a mix of price action around the key support and resistance levels, the evolution of on-chain demand, and the trajectory of exchange inflows. As always in crypto markets, the landscape can shift quickly—making close attention to the unfolding data essential for readers navigating this evolving chapter of Bitcoin’s price journey.

Readers should stay tuned for any shift in the demand picture, a decisive move at or above the $76,000 level, or a reduction in exchange selling pressure, as these variables will likely dictate whether BTC can sustain a meaningful recovery or extend its consolidation in the coming weeks.

Bitcoin (BTC) has fallen 6.5% from its recent high above $82,000, as a bearish technical structure, weakening demand, and increasing sell pressure now point to the risk of further losses ahead.

Key takeaways:

- BTC price risks a drop toward $72,000 as bearish momentum strengthens on higher time frames.

- Binance BTC inflows tripled in under two weeks, signaling rising sell pressure and weaker investor confidence in the market.

- Bitcoin’s apparent demand fell to 2026 lows, raising risks of deeper losses if spot demand fails to recover in the coming weeks.

Bitcoin bears eye BTC price drop to $72,000

Bitcoin’s failure to hold above key support levels suggested buyers were unable to sustain the upward momentum.

“$BTC has officially lost the 100 & 50d EMA,” analyst CryptoJelleNL said in a recent post on X, adding:

“The local market structure is back to bearish.”

“Bitcoin lost its bullish impulse exactly when macro sharply deteriorated,” fellow analyst Axel Adler Jr said in a Sunday X post, adding:

“The market looks risk-off, and every BTC bounce remains unconfirmed.”

The rejection at $82,000 coincided with the upper trend line of an ascending parallel channel, which has capped BTC’s price action since early February.

The chart below shows that every time the price has been rejected from this trend line, it has lost between 11%-14% of its value, dropping toward the lower support trend line.

If this price behaviour continues, Bitcoin will fall toward the lower boundary of the channel at $72,000, which is 13% below the upper boundary and a 7% drop from the current price.

BTC/USD daily chart. Source: Cointelegraph/TradingView

Meanwhile, the relative strength index has dropped to 48 from near overbought conditions at 69 on May 6, suggesting increasing downward momentum.

“Bitcoin briefly dipped as low as $74.1K, sweeping the May VCPR liquidity zone before seeing a quick reaction,” trader and analyst Anup Dhungana said in his latest analysis on X, adding:

“Losing this support area could send $BTC swiftly back toward the $70K region, while holding it keeps the door open for another recovery attempt.”

MN Capital founder Michael van de Poppe shared a chart showing that if the “crucial” support zone between $75,000 and $76,000 is lost, the price could retreat toward the next lines of defense at $74,000 and $71,400, before potentially retesting the 2026 lows at $60,000.

On the other hand, Van de Poppe said BTC/USD could break to “higher grounds” above $80,000 if “there’s going to be a peace deal in the Middle East” in the coming days.

BTC/USD daily chart. Source: X/Michael van de Poppe

As Cointelegraph reported, the $76,000 level is the critical level to watch, as a close below it would increase the risk of a drop to the multi-month support line around $72,000.

Bitcoin apparent demand hits 2026 lows

Bitcoin’s “warning is flashing” after its Risk Index re-entered “high-risk” territory, according to private wealth manager Swissblock.

“That doesn’t confirm breakdown yet,” Swissblock said in a recent X post, adding:

“But it confirms that selling pressure is no longer being fully absorbed.”

Bitcoin risk index. Source: Swissblock

That high-risk signal also aligns with increasing selling pressure on exchanges, with Binance recording nearly 10 straight days of net BTC inflows. The weekly average inflows rose to 1,190 BTC from 378 BTC on May 16, marking a more than threefold increase in less than two weeks.

“When inflows become dominant and consistent on a platform like Binance, this is traditionally interpreted as a potential sell signal,” CryptoQuant analyst Darkfost said in a QuickTake note on Monday, adding:

“Holders transferring their BTC to an exchange most often do so with the intent to sell, whether it be profit taking, reducing exposure, or a more defensive repositioning.”

Binance exchange’s Bitcoin net flow. Source: CryptoQuant

Meanwhile, Bitcoin’s apparent demand has fallen to around -147,000 BTC, its most negative level since the start of the year and the weakest reading since December 2025.

“This development suggests that demand continues to gradually contract,” Darkfost said in an X post on Sunday, adding:

“Without a meaningful recovery in spot demand, it becomes difficult to imagine Bitcoin sustaining a durable rally.”

Bitcoin’s apparent demand. Source: CryptoQuant

The last time this metric was this low was in December 2025, before another 33% drop to multi-year lows below $60,000 was reached on Feb. 6.

As Cointelegraph reported, Bitcoin’s weakening demand and increasing spot ETF outflows have raised the risk of prolonged consolidation or a drop toward $65,000 in the short to medium term.

Stablecoin issuer Tether and the government of Georgia are pursuing a new digital asset initiative: GELT, a stablecoin pegged to the Georgian lari that would operate under Georgia’s evolving digital asset regulatory framework. The collaboration aims to facilitate cross-border commerce and digital payments within the country, though key details—such as legal issuance arrangements, reserve custodians, and redemption rights—remain to be disclosed as the program unfolds.

On Monday, Tether stated that GELT’s structure, rollout plan, and regulatory implementation would be announced at a later stage. The announcement comes as Georgia advances a regulatory regime for digital assets, including stablecoins, with an emphasis on reserve management, redemption rights, issuer oversight, and anti-money laundering compliance. In March, the National Bank of Georgia signaled it had developed rules governing the initial offering of so‑called “stable virtual assets,” including requirements for full reserve backing, the provision of offering documents, and external auditor verification. According to authorities, the framework is designed to bolster consumer protection, strengthen risk management, and align with international standards.

Georgian Prime Minister Irakli Kobakhidze described the GELT partnership as a step toward a more connected and transparent financial system. Natia Turnava, president of the National Bank of Georgia, welcomed the collaboration as part of the central bank’s broader plan to advance digital financial infrastructure. The announcement did not specify who would legally issue GELT, where reserves would be held, or whether holders would have direct redemption rights. Tether did not provide a definite launch timeline. The company confirmed it had received Cointelegraph’s inquiry but did not offer additional details at publication time.

Key takeaways

- GELT represents a formal collaboration between Tether and the Georgian government to issue a lari‑pegged stablecoin under Georgia’s digital asset rules, with cross-border payments and digital commerce as primary use cases.

- Georgia’s March framework for stablecoins requires prior written consent from the National Bank, mandates full reserve backing with liquidity‑quality assets, and obliges issuers to prepare offering documents verified by external auditors. Non‑VASPs must register before offering stablecoins.

- Specifics about GELT’s issuer identity, reserve custody, and whether holders would have direct redemption rights remain undisclosed; no launch timeline has been announced.

- GELT would extend Tether’s non‑dollar stablecoin portfolio, which already includes MXNT (Mexican peso) and CNHT (offshore Chinese yuan), with plans for a UAE dirham‑pegged token and the recently launched USAT (federally regulated US‑dollar stablecoin). Earlier tokens such as EURT have been wound down or moved toward non‑redeemable status.

- The development sits within a broader regulatory and policy context, reflecting ongoing efforts to harmonize cross‑border crypto activities with established financial regulation and to align with international standards, including potential parallels to MiCA outside the EU framework.

Georgia’s stablecoin regime and the GELT initiative

The March 2024 framework released by the National Bank of Georgia establishes the guardrails for stablecoin issuance within the country. The central bank’s guidance makes clear that stablecoins may not be offered without prior written consent from the regulator, signaling a strict supervisory posture for digital asset offerings. The framework covers virtual asset service providers (VASPs) registered with the central bank; issuers not registered as VASPs must obtain registration before launching any stablecoin offering or related services. Importantly, the rules require that circulating stablecoins be fully backed by reserve assets that satisfy predefined liquidity and credit quality requirements. This emphasis on reserve integrity reflects a broader global regulatory concern around reserve adequacy and risk management for stablecoins serving as payment rails or settlement vehicles.

Additionally, the central bank requires issuers to prepare documentation for the initial issuance and submit these materials for external auditor verification. The regulator said the goal is to strengthen consumer protection, reinforce risk controls, and ensure alignment with international standards. For institutions and market participants, the regime signals a formal path to licensing, ongoing oversight, and heightened due‑diligence requirements for entities seeking to operate stablecoins in Georgia.

GELT’s architecture, governance, and regulatory questions

The public statement outlining GELT’s plans stops short of disclosing critical operational specifics. Notably absent are details about who would legally issue the GELT token, where any reserves would be held, and whether GELT holders would have direct redemption rights or access to reserves. The lack of a launch timeline further underscores the project’s early stage and the regulatory conditioning embedded in Georgia’s framework. As authorities emphasize, any stablecoin formation under the regime would require compliance with reserve standards, disclosure obligations, and independent verification, all of which would shape GELT’s risk profile and usability in commercial contexts.

From a policy and enforcement standpoint, the GELT initiative highlights several compliance considerations for financial institutions, banks, and technology providers operating in Georgia. First, the necessity of obtaining NBG consent points to a formal licensure process that would likely involve ongoing oversight of reserve management practices and governance. Second, the requirement for robust AML/KYC controls and external audit verification aligns GELT with internationally recognized controls that regulators monitor in cross-border payments ecosystems. Finally, the framework’s emphasis on consumer protection and risk management suggests that any GELT‑related products would be evaluated for compliance with disclosure standards, redress mechanisms, and governance transparency, which are critical for institutional confidence and retail trust alike.

Tether’s broader non‑dollar stablecoin strategy and regulatory alignment

GELT would extend Tether’s multi‑currency stablecoin lineup beyond its flagship USDT. The issuer has previously launched MXNT, a peso‑pegged token introduced in 2022 with initial support on Ethereum, Tron, and Polygon. It also operates CNHT, a yuan‑pegged token issued offshore, which has been expanded to multiple networks, and has announced a planned UAE dirham‑pegged token with backing from UAE‑based liquidity. In 2026, Tether launched USAT, a US‑regulated dollar stablecoin designed for the American market, reflecting the company’s strategic pivot toward compliance‑driven, regulator‑friendly offerings. At the same time, Tether has wound down some earlier non‑US‑dollar stablecoins; EURT’s minting was halted, and CNHT is slated to become non‑redeemable in February 2027. These moves illustrate a broader pattern: Tether is diversifying its product suite while tightening compliance and governance around its non‑USD assets.

The GELT development sits within this broader strategic arc, where Tether seeks to provide currency‑specific stablecoins that may appeal to regional economies and financial ecosystems seeking faster, cheaper cross‑border settlement options. For Georgia, the GELT plan could create a new interface between digital assets and traditional financial infrastructure, potentially enabling smoother cross‑border payments, remittances, and digital commerce—subject to the regulatory guardrails and the stability and transparency of reserve arrangements. From a regulatory standpoint, GELT also raises questions about how non‑dollar stablecoins will be treated in Georgia’s licensing framework, how cross‑border activities will be monitored, and how such instruments will interact with global AML/KYC standards and correspondent banking relationships.

Implications for banks, VASPs, and cross‑border settlement

The Georgian framework appears to be designed with a structured approach to licensing, oversight, and risk management. For banks and VASPs operating in or with Georgia, GELT could entail new compliance channels, including enhanced customer due diligence, ongoing monitoring of reserve holdings, and transparent audit reporting. The requirement for reserve backing and external audits would necessitate robust third‑party verification and clear disclosure to customers and counterparties. In cross‑border contexts, GELT could become part of a wider network of currency‑specific tokens that facilitate cross‑border payments, provided jurisdictions recognize and harmonize stability, governance, and regulatory compliance standards. Policymakers and industry participants alike will be watching how Georgia’s approach harmonizes with international standards and how it aligns with broader regional efforts to standardize stablecoin oversight.

From a historical and policy perspective, Georgia’s approach reflects a growing trend toward formalizing stablecoins within national financial architectures. The regime’s emphasis on consent, reserve adequacy, disclosure, and external audit mirrors requirements that have gained traction globally as jurisdictions reconcile innovation with investor protection and systemic risk mitigation. For institutional readers, this case underscores the importance of regulatory calendars, licensing pathways, and cross‑border compliance considerations when engaging with regional digital asset programs and payment rails.

Closing perspective

Georgia’s GELT plan emblemizes a cautious but ambitious avenue for integrating stablecoins into a regulated financial system. While many details remain to be announced, the initiative signals a clear intent to bridge digital assets with traditional monetary infrastructure under formal supervision. As regulators refine reserve and disclosure standards and as Tether outlines governance and issuance details, GELT’s trajectory will likely influence regional discussions on stablecoin licensing, cross‑border settlement, and the resilience of digital asset ecosystems in transitioning economies.

The coming week appears to be macro-led, with U.S. economic data carrying the main calendar risk. Inflation, growth, jobless claims and housing numbers all land before the open, giving markets insight on whether the Fed has room to cut rates.

Prediction markets and the CME’s FedWatch tool currently point to rates remaining unchanged in June’s meeting.

The data comes amid the ongoing Middle East war, which keeps oil prices and inflation risk in focus. Any move higher in energy costs could make softer inflation harder to sustain and weigh on risk assets.

What to Watch

(All times ET)

- Crypto

- May 26–June 1: Kevin Warsh officially begins his first week as Federal Reserve Chair following his confirmation.

- Macro

- May 26, 08:00 a.m.: U.S. S&P/Case-Shiller Home Price YoY for March est. 1.1% (Prev. 0.9%)

- May 26, 08:00 a.m.: U.S. House Price Index YoY for March est. 1.8% (Prev. 1.7%)

- May 26, 09:00 a.m.: U.S. CB Consumer Confidence for May est. 92 (Prev. 92.8)

- May 26, 08:30 p.m.: Australia Consumer Price Index YoY for April est. 4.4% (Prev. 4.6%)

- May 27, 08:00 p.m.: Bank of Korea Interest Rate Decision (Prev. 2.5%)

- May 28, 04:00 a.m.: Eurozone Economic Sentiment for May est. 92 (Prev. 93)

- May 28, 07:30 a.m.: U.S. PCE Price Index YoY for April (Prev. 3.5%); Core PCE (Prev. 3.2%)

- May 28, 07:30 a.m.: U.S. Initial Jobless Claims for period ending May 23 est. 212K (Prev. 209K)

- May 28, 08:00 a.m.: South Africa Reserve Bank Interest Rate Decision est. 7.0% (Prev. 6.75%)

- May 28, 09:00 a.m.: U.S. New Home Sales for April est. 0.67M (Prev. 0.682M)

- May 28, 03:30 p.m.: U.S. Fed Balance Sheet for period ending May 27 (Prev. $6.713T)

- May 28, 06:30 p.m.: Japan Tokyo Consumer Price Index YoY Prel for May (Prev. 1.5%)

- May 29, 07:30 a.m.: Canada GDP Growth Rate Annualized for Q1 (Prev. -0.6%); QoQ (Prev. -0.2%)

- May 29, 08:45 a.m.: U.S. Chicago PMI for May est. 49.5 (Prev. 49.2)

- May 30, 08:30 p.m.: China NBS Manufacturing PMI for May est. 50.5 (Prev. 50.3)

- Earnings

- Governance Votes & Calls

- Compound DAO is voting on a proposal to update Compound III supply caps for USDC, USDT, and WETH across Optimism, Polygon, and Unichain. Voting ends on May 25.

- Aave DAO is voting on a proposal to establish a 3-of-4 rewards operations multisig to manage third-party incentive funding for growth campaigns. Voting ends on May 25.

- Instadapp DAO is voting on a proposal to rebalance wstUSR vaults, withdraw 750,000 FLUID to fund rewards, configure PST launch limits, and consolidate InstaConnectorsV2 administrative controls to the Team Multisig. Voting ends on May 26.

- Bancor DAO is voting on a proposal to increase the vortex MaxSaleAmount parameter from 100 to 100,000 for the TAC and IOTA EVM blockchains. Voting ends on May 27.

- Arbitrum DAO is voting on an amended proposal to transfer 30,765.66 frozen ETH, tied to the rsETH incident, to an Aave LLC-controlled wallet. Voting ends on May 29.

- Unlock DAO is voting on a proposal to process the May constant payment roll, compensating contributors David Moderator, Ceci Sakura, and Trigs for their roles. Voting ends on May 30.

- Uniswap DAO is voting on proposals to expand protocol fee infrastructure to BNB Chain, Polygon, and Celo, and to recall 12.5M delegated UNI from the Franchiser system to the Governance Timelock. Voting ends on May 30.

- Unlocks

- May 26: Plasma (XPL) to unlock 3.38% of its circulating supply worth $7.39 million.

- May 26: Huma Finance (HUMA) to unlock 20.04% of its circulating supply worth $11.76 million

- May 29: Grass (GRASS) to unlock 3.55% of its circulating supply worth $11.29 million.

- May 30: Falcon Finance (FF) to unlock 4.06% of its circulating supply worth $8.26 million.

- June 1: EigenCloud (EIGEN) to unlock 4.99% of its circulating supply worth $8.48 million.

- Token Launches

Big Tech’s $2 trillion AI gold rush is hiding a structural flaw. Critics say the giants are quietly paying themselves through their own cloud bills, igniting fresh AI bubble fears that increasingly echo the dot-com era.

Latest corporate filings show OpenAI and Anthropic alone anchor over half of the roughly $2 trillion in future cloud commitments held by Microsoft, Amazon, Google, and Oracle. This leaves four trillion-dollar companies leaning on two unprofitable startups.

The Cloud Loop That Pays Itself

Critics call the mechanism a round-trip funding loop. A tech giant writes a billion-dollar check to an AI startup. The contract then forces that same money straight back, in the form of cloud rent. The cash never leaves the building.

Microsoft’s $13 billion stake in OpenAI is the textbook case. The investment landed largely as Azure cloud credits. OpenAI fed those credits into training models, and Microsoft turned around and booked the consumption as fresh commercial revenue.

OpenAI’s annual cloud bill has reportedly ballooned past $60 billion. The company’s actual revenue sits closer to $25 billion.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

Anthropic plays the same hand with Amazon. The Claude developer spent $2.66 billion on Amazon Web Services in nine months, roughly every dollar it earned.

“The entire AI boom might be built on fake revenue,” remarked analyst Bull Theory.

The pattern echoes 2001, when Global Crossing and Qwest Communications swapped fiber-optic capacity to fabricate sales.

Qwest eventually erased $1.4 billion in fictitious income, and Global Crossing went bankrupt. The 2026 version stays fully legal under current accounting rules.

Paper Profits Are Doing the Heavy Lifting

The second leg of the loop sits on the income statement. Every fresh funding round for an AI startup lets its Big Tech backer mark up the investment and drop the paper gain straight into net income.

Alphabet posted a record $62.6 billion profit in Q1 2026. About $28.7 billion of that figure came from a markup on its Anthropic stake, according to its filing.

Amazon mirrored the trick. Roughly $16.8 billion of its $30.3 billion in net income tracked back to the same Anthropic revenue story, according to Fortune’s analysis.

Behind the headline profit, Amazon’s free cash flow cratered 95% to $1.2 billion. The company poured $44.2 billion into physical data centers in the same quarter.

Microsoft now carries 49% of its $627 billion future backlog tied to OpenAI alone. Oracle leans harder still, with 54% of its $553 billion pipeline riding on that same single customer.

Real Companies Are Already Hitting the Wall

The bigger problem starts the moment AI leaves the protected loop and lands in a budget meeting. Ordinary companies cannot recycle infrastructure spending into their own revenue, and the invoices are arriving fast.

Uber torched its full 2026 AI coding budget by April after handing Anthropic’s Claude Code and Cursor to thousands of engineers. Some staff burned $500 to $2,000 in monthly API charges each.

Microsoft, despite a multi-billion Anthropic partnership, ordered its own employees to stop using Claude Code internally after token consumption had become unsustainable, according to Fortune’s report.

Nvidia’s vice president of applied deep learning Bryan Catanzaro admitted his team now spends more on compute than on human salaries.

“For my team, the cost of compute is far beyond the costs of the employees,” Catanzaro recently told Axios.

Cheaper chips may not rescue the math. Lower token prices tend to invite heavier agentic workloads, and enterprise AI spending may keep climbing even if hardware costs fall sharply.

The AI Bubble Enters Its Prove-It Phase

The market is no longer asking whether AI can grow. It is asking whether AI can pay for itself.

“The first companies to actually use AI at scale are not able to afford it,” one analyst remarked.

Index funds and retirement accounts have been dragged deeper into a tight cluster of trillion-dollar names whose AI-linked profits hinge on a handful of unprofitable startups.

Crypto investors hold a direct stake. Bitcoin (BTC) hit a correlation with Nasdaq of 0.75 in January 2026,

This means any unwind of the Nvidia and OpenAI trade likely ripples straight into digital assets. AI tokens, already volatile, would feel the first blow.

The falling chip prices, agentic adoption, or cold accounting math winning the next round is now in the balance, with the AI boom officially entering its prove-it phase.

Notably, mainstream finance has already taken notice, with Fidelity’s own AI bubble framework listing five warning checks.

“We think 5 indicators may offer directional insights into future AI-driven market and economic trends,” Fidelity listed.

- The rate of aggregate earnings growth

- Aggregate earnings quality

- Valuations vs. history

- The affordability/sustainability of corporate capex spending, and

- The interest-rate cycle

Big Tech’s Q1 filings already trip two of them, earnings quality and capex affordability.

The boom may not get the chance to prove anything if the warning lights keep multiplying.

The post AI Bubble Fears Grow as Big Tech Allegedly Pays Itself in Cloud Loop appeared first on BeInCrypto.

Crypto World

Bitcoin News Today: Saylor Moves to MicroStrategy 2.0 with Treasury Bonds as the Company Stops Buying BTC

In Bitcoin News today, Strategy has paused its BTC purchases this week to repurchase $1.5 billion in face value of its 0% convertible senior notes due 2029 for approximately $1.38 billion in cash. Michael Saylor confirmed it himself on X with a single line: “This week we bought bonds, not bitcoin. The ₿itVac is charging.”

This is no longer a one-way accumulation machine. Strategy is now actively managing its capital structure, retiring debt at a discount, recycling capacity, and integrating US Treasury instruments as a yield-generating funding leg. The company that pioneered corporate Bitcoin accumulation is evolving into something closer to a macro carry trade vehicle.

Discover: The Best Crypto to Diversify Your Portfolio

Treasury Yield Leg Could Work

The mechanics are straightforward, with Strategy raising capital through equity sales, convertible notes, and perpetual preferred shares like STRC. A portion of the capital gets parked in short-duration US Treasuries and money-market instruments, generating yield while BTC accumulation conditions are evaluated.

That yield becomes the “safe leg” of a macro barbell as Treasuries generate cash flow that can service dividends on STRC, fund opportunistic buybacks of discounted convertibles, and eventually recycle into BTC purchases when the entry is right.

The Carry Trade logic here is that Strategy borrows or issues at ultra-low cost (0% coupon on the 2029 notes, fixed dividends on STRC) and earns spread against Treasury returns and BTC appreciation.

The $1.38 billion bond repurchase this week is a direct expression of that logic. Strategy is retiring debt at a discount to face value ($1.38B cash for $1.5B face), which immediately improves its balance sheet, reduces future share dilution (fewer notes means fewer potential conversion events into MSTR equity), and increases Bitcoin per share for existing holders.

Strategy currently holds 843,738 BTC, worth $65.25 billion, against an acquisition cost of $63.88 billion, for approximately $1.50 billion in unrealized profit. No Bitcoin was sold to fund this bond repurchase. The BitVac, as Saylor frames it, is recharging. It is not liquidating.

Bitcoin News Today: What the Carry Trade Structure Does to MSTR’s Risk Profile

MSTR is no longer a clean Bitcoin proxy. It is a layered instrument: BTC price exposure stacked on top of rate sensitivity stacked on top of equity volatility. Institutional desks now need to model three variables simultaneously, and that changes how the stock behaves in different macro regimes.

The clearest structural risk is the 2028 liquidity window. Strategy carries around $3 billion in convertible notes with put rights that allow holders to demand cash repayment beginning June 2028. If capital markets are closed, or MSTR is trading poorly relative to conversion prices, those obligations could force Bitcoin sales at the worst possible time. That is precisely why Strategy is front-loading debt retirement now, while it trades at a discount and before the put window opens.

Discover: The Best Token Presales

The post Bitcoin News Today: Saylor Moves to MicroStrategy 2.0 with Treasury Bonds as the Company Stops Buying BTC appeared first on Cryptonews.

The U.S. Senate is moving to unbanned passive stablecoin yield from every regulated platform in the country, as the industry is already engineering its way around it. The CLARITY Act has previously extended a yield prohibition that the earlier Genius Act applied only to issuers and now targets exchanges, brokers, and any custodial intermediary offering APY on idle stablecoin balances.

— Coin Bureau (@coinbureau) May 23, 2026

THE CLARITY ACT COULD UNLOCK “YIELD-AS-A-SERVICE”

THE CLARITY ACT COULD UNLOCK “YIELD-AS-A-SERVICE”

STBL’s Joe Vollono says this may be the bill’s biggest outcome, creating an entirely new crypto market. pic.twitter.com/p94apRj2cn

Joe Vollono, Chief Compliance Officer at STBL, argues that the legislative pressure is not killing yield so much as relocating it. According to him, Yield-as-a-Service becomes the dominant architecture once direct issuer-to-holder yield is prohibited, with AI agents acting as the compliance and execution layer between regulated stablecoins and yield-generating DeFi protocols.

Discover: The Best Crypto to Diversify Your Portfolio

The CLARITY Act and Yield Ban

The current Senate draft retains prior language banning rewards on idle stablecoin balances held in accounts while explicitly permitting yield generated through transactional activity. The critical legal phrase is “functional or economic equivalent” of bank-deposit interest: if a product looks like a savings APY, it is treated as a savings APY, regardless of its label.

The Tillis–Brooks compromise, driving the current bill, explicitly closes that exemption. Under the new text, the prohibition reaches “all intermediaries, any exchange, any platform holding your stablecoins.”

The White House Council of Economic Advisers models the full prohibition as increasing U.S. bank lending by roughly $2.1 billion while imposing a net welfare cost of $800 million, a cost-benefit ratio of 6.6 that reflects the amount of consumer surplus passive yield that was being generated.

As we know, the Banking and credit-union groups are lobbying hard to keep the ban tight, arguing that stablecoin rewards amount to unregulated shadow banking that competes directly with insured deposits.

Yield-as-a-Service: The Technical Stack It Requires

Vollono’s Yield-as-a-Service framework reframes the compliance constraint as a market-structure shift. If the issuer cannot pay yield and the custodian cannot pay yield, the yield must come from somewhere the law does not yet reach, specifically, from active strategy execution rather than passive balance accumulation.

The architecture requires an AI agent layer positioned between the user’s regulated stablecoin balance and the DeFi protocols generating returns. These AI agents monitor chain liquidity in real time, score protocol risk dynamically, and execute trades to capture yield-generating opportunities. They are the operational core of the model.

The agents do not hold the stablecoins; they route them through compliant DeFi pools, collect returns from transactional activity explicitly permitted under the CLARITY Act carve-outs, and return net yield to users as the product of active management.

The Golden Age of simple Earn programs is closing. What replaces it depends on whether AI agents can close the integration gap before regulators close the transactional yield carve-out too.

Discover: The Best Token Presales

The post Clarity Act Chaos? Automating Compliant Crypto Yield with AI appeared first on Cryptonews.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Bitcoin mining enters a new era as Bitmain and AntPool push hash rate financialization and ecosystem integration.

Summary

- Bitcoin mining is shifting toward a broader “BTC Ecosystem” model focused on hash-rate financialization and infrastructure integration.

- BTC Ecosystem uses renewable-powered mining operations across Texas, Canada, and Australia.

- The company positions low-cost renewable energy, ASIC efficiency, and scalable infrastructure as key long-term mining advantages.

Throughout the history of cryptocurrency, mining has remained the ironclad foundation safeguarding Bitcoin’s network security and decentralization. Yet with the rapid emergence of the “BTC Ecosystem” narrative, the mining industry is evolving far beyond the traditional model of simply “mining and selling coins.” A new era centered on the financialization of hash rate is now taking shape.

Against this backdrop, the strategic alliance between Bitmain, AntPool, and leading BTC ecosystem projects signals a profound transformation underway across the mining sector. From hardware efficiency and hash rate allocation to capital deployment and ecosystem integration, the industry is entering a new phase of vertical integration — a strategic evolution increasingly favored by Western capital markets.

Core technology: Pushing the limits of computing efficiency

The technological foundation of this collaboration lies in the deep integration of next-generation mining hardware with the rapidly expanding BTC ecosystem infrastructure. At the center of this evolution is Bitmain’s latest Antminer S21 Pro series, delivering an industry-leading energy efficiency ratio below 15J/T. Through deeper protocol-level optimization, miners can achieve more stable firmware upgrades and significantly faster response speeds when processing complex inscriptions and Bitcoin Layer 2 transactions, laying the groundwork for a more efficient and scalable mining ecosystem.

To meet the growing demand for high-frequency computing within the BTC ecosystem, AntPool and its strategic partners are accelerating the large-scale deployment of liquid-cooling infrastructure. Standardized liquid-cooled mining cabinets not only extend the operational lifespan of ASIC chips but also improve heat dissipation efficiency by nearly 40%. This advancement enables industrial-scale mining farms to transition toward a more stable and efficient “high-frequency profitability” model, further enhancing overall operational performance.

At the same time, industry speculation suggests that future Antminer models may integrate dedicated modules designed to accelerate Bitcoin Layer 2 zero-knowledge proof (ZK) computation. If realized, this innovation would fundamentally redefine the role of mining hardware — transforming miners from simple block producers into decentralized computing providers capable of supporting DApps, sidechains, and broader BTC ecosystem infrastructure.

What is the BTC Ecosystem?

The BTC Ecosystem is operated byADAPT ECOSYSTEM PTY LTD, an Australia-registered company regulated under the oversight framework of the Australian Securities and Investments Commission (ASIC). Established in October 2022, the company focuses on building next-generation mining infrastructure powered by renewable energy, positioning itself at the intersection of Bitcoin mining, sustainable energy, and ecosystem expansion.

Its mining operations are strategically distributed across multiple global regions to optimize both energy efficiency and long-term scalability. In Texas, operations benefit from a mature and highly stable power grid capable of supporting large-scale, continuous mining activity. In Canada, abundant hydroelectric resources provide cleaner and more cost-efficient energy solutions, helping improve operational efficiency while maintaining competitive mining costs.

Meanwhile, in Australia, the company is progressively integrating solar and wind energy into its infrastructure strategy to support the sustainable expansion of its mining ecosystem. This multi-regional energy deployment model reflects the broader industry trend toward greener, more resilient, and institutionally scalable Bitcoin mining operations.

Investment potential: From commodities to creating yield-generating contracts

In the eyes of institutional investors in Europe and the United States, simply holding Bitcoin yields Beta returns, while participating in this “mining + ecosystem” collaboration is the key to obtaining Alpha returns

BTC Ecosystem operates data centers sited in regions tied to long-term renewable energy contracts. Geothermal, hydro, and wind power the fleet, and the company reports operating costs roughly 30% below the industry average as a result. Hardware is a current-generation ASIC, with continuous firmware management and redundancy built into the facility layer.

The renewable footprint is not just an ESG talking point. As global mining difficulty continues to climb, marginal cost decides the difference between a profitable operation and a stranded fleet. Siting compute near cheap, contracted renewable power is the structural advantage the company is building around.

Contract tiers and a $15 no-deposit trial

The platform’s contract menu is tiered by capital commitment and duration. Headline tiers include:

- A $15 welcome contract is activated at signup, returning $0.53 per day. This contract is designed to let new users see daily settlement before committing capital of their own.

- A $1,500 contract over 10 days, returning approximately $21.75 per day.

- A $9,000 contract over 20 days, returning approximately $142.20 per day.

- A $30,000 contract over 30 days, returning approximately $528 per day.

- Institutional-scale allocations up to $300,000, with daily returns reported in the four-figure range.

Earnings settle to user accounts on a 24-hour cadence. Withdrawals become available once a balance reaches $100. The platform supports BTC, ETH, USDT (ERC20 and TRC20), LTC, BCH, XRP, SOL, and DOGE for both deposits and payouts.

Industry observations and future outlook

This strategic collaboration sends a clear signal to the market: Bitcoin is evolving beyond “digital gold” into a decentralized computing platform. As the BTC ecosystem expands, mining infrastructure is no longer limited to block production, but is becoming a core layer supporting Layer 2 networks, DApps, and on-chain computation.

At the same time, ESG compliance and institutional adoption are accelerating industry transformation. Bitmain’s high-efficiency mining hardware aligns more closely with Western ESG standards, making large-scale mining infrastructure increasingly attractive to institutional capital, including pension funds and insurance investors.

However, as industry giants strengthen collaboration and improve operational efficiency, hashrate decentralization remains a key concern within the crypto community. In response, AntPool and its partners have emphasized more transparent pooling mechanisms and governance models. Ultimately, this shift represents not only an advancement in mining technology, but also a new era of capital efficiency — where transforming “cold computing power” into a thriving ecosystem may define the next crypto cycle.

For more information, visit the official website.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Crypto World

BNB Chain Launches Agent Survival Pack, Bringing Onchain Payments to AI Agents Across 6 Partner Projects

[PRESS RELEASE – Dubai, UAE, May 25th, 2026]

21 May: BNB Chain, one of the most active blockchain ecosystems worldwide, today announced the launch of the Agent Survival Pack, a coordinated initiative bringing together six AI infrastructure partners to give autonomous AI agents the ability to pay for their own operating costs directly on-chain.

Participating projects span the two layers an AI agent needs to operate (LLM access and financial infrastructure), with every transaction settling in BNB or BEP-20 tokens on BNB Smart Chain (BSC).

The initiative addresses a structural gap in current AI agent deployments. Most agents today still rely on human-managed billing infrastructure, including AWS accounts, OpenAI API keys, and SaaS subscriptions tied to individual cards. This forces human intervention whenever payment, top-up, or service changes are required, creating a hard limit on how autonomously an agent can operate.

Participating projects span the two layers an AI agent needs to operate: LLM access and financial infrastructure.

LLM access and compute:

- Alt AI: Access to leading models through a unified interface, with payment settled in BEP-20 tokens.

- Pieverse: An AI gateway built on x402b, its own extension of the x402 HTTP payment standard for BNB Chain. Agents pay for API calls inline using stablecoins, with every payment generating a verifiable on-chain receipt.

- Bankr: OpenAI-compatible access to 30+ models including Claude, GPT, Gemini, Grok, and DeepSeek, with payment metered on-chain per token.

- WorldClaw: A unified router across 300+ AI models with stablecoin settlement on BNB Chain. Active users earn credits and points through ongoing platform activity.

Financial infrastructure:

- B.AI (Bank of AI): A comprehensive financial layer integrating on-chain payments (via x402), on-chain identity (via ERC-8004), and DeFi access including lending, swap, and yield, deployable in a single line of code.

- AEON: A bridge between on-chain agents and the real-world economy, enabling agents to pay via QR code at physical merchants across Southeast Asia, with Visa and Mastercard rails rolling out next.

Each participating project is running its own incentive program alongside the launch, designed to lower the barrier to entry for builders and agents testing the integrations. All programs are tracked on-chain, with no separate signup or claim form required. Specifics vary by project and are detailed in the Agent Survival Pack launch documentation.

The Agent Survival Pack is part of BNB Chain’s broader strategy to position BSC as the operating layer for autonomous AI agents. The launch follows the introduction of the BNBAgent SDK and the chain’s continued growth as a destination for AI agent activity, with BNB Chain currently hosting one of the largest deployed agent populations of any public blockchain.

About BNB Chain

BNB Chain is a community-driven decentralized blockchain ecosystem powering Web3 applications across DeFi, AI, gaming, and consumer use cases. Its multi-chain architecture spans BNB Smart Chain (BSC), opBNB, and BNB Greenfield, providing the infrastructure for builders deploying onchain applications at scale. For more information, visit www.bnbchain.org.

Disclaimer

BNB Chain is not affiliated with or operating any of the projects featured in this article. The Agent Survival Pack is an ecosystem initiative showcasing independent projects building on BNB Chain. This content is for informational purposes only and does not constitute financial or investment advice. Always do your own research and assess potential security risks before interacting with any project mentioned.

The post BNB Chain Launches Agent Survival Pack, Bringing Onchain Payments to AI Agents Across 6 Partner Projects appeared first on CryptoPotato.

Crypto World

Influence360 Launches as the First AI & Data-Driven Web3 KOL Platform with Global KOL Coverage and Real Attribution

Influence360 introduces a campaign engine that enables Web3 projects to discover KOLs globally, execute structured campaigns, and track real performance across regions, languages, and channels.

A benchmark study of 143 Web3 KOLs highlights major gaps in payments, access, and campaign infrastructure, providing context for the platform’s launch.

Influence360 today announced the launch of its platform, introducing a new infrastructure layer for Web3 influencer marketing built around trust, data, and global execution.

Projects can discover web3 KOLs across 10+ languages and key platforms, including X, YouTube, TikTok, and Telegram; launch structured campaigns; and manage execution in one place with AI-powered optimization, smart contract escrow, and real-time performance tracking, enabling transparent payments and clear attribution at a global scale.

“Web3 influencer marketing already moves serious budgets, but the infrastructure around it still feels too basic for the level the market has reached,” said Dejan Horvat, founder & CEO of Influence360. “The biggest issue in the industry is that campaigns don’t compound, as teams aren’t learning what actually drives performance. Influence360 turns every campaign into data, showing which creators deliver value, what content works, and how to optimize spend over time. That’s how we bring trust, structure, and measurable performance to Web3 marketing.”

Influence360 is built by a team with extensive experience in Web3 influencer marketing and campaign execution. Through their previous work at Innovion, the co-founders, Dejan Horvat and Laura Toma, have collaborated with leading blockchain projects and KOL networks across multiple regions over the last 9 years, managing campaigns and partnerships that directly informed the platform’s design and its focus on real-world execution challenges.

Influence360 also extends this infrastructure to Web3 agencies and talent managers. Through a permission-based system, influencers can grant agencies custom access levels covering everything from campaign applications to payment handling, while agencies manage their full roster from a single account. Agencies can apply to campaigns on behalf of creators, set their own pricing on top of influencer rates, and earn a share of platform fees from influencers they bring on, for life. This structure is part of Influence360’s broader referral program, which will expand to include a dedicated affiliate marketing feature focused on performance-based campaigns.

Influence360 is now open to Web3 projects looking to run structured campaigns, KOLs seeking reliable partnerships, agencies managing creator rosters, and affiliate marketing partners focused on performance-driven growth. Learn more and join at influence360.io.

For its launch, Influence360 is releasing The State of Web3 Influencer Marketing 2026, based on survey responses from 143 Web3 KOLs across seven global regions.

The research shows a financially active ecosystem, where more than half of KOLs earn between $1,000 and $5,000 per campaign, with experienced KOLs exceeding that range. The report highlights a persistent trust gap in the market, with only 35% of KOLs reporting that they have been paid by every project they have worked with.

The findings also confirm that Web3 influencer marketing is already a repeat-driven and increasingly professionalized channel. 97% of the KOLs surveyed have worked with the same projects multiple times, while most evaluate factors such as team transparency, investor backing, and project credibility before accepting collaborations. However, the lack of structured tooling, reliable payments, and performance attribution continues to limit efficiency and scale.

Influence360 is built to close this gap by combining campaign execution, real attribution, and a growing data layer that will power AI-driven campaign benchmarking and optimization. With a roadmap that expands into advanced analytics, UGC campaign infrastructure, and automation, the platform is positioning itself as a long-term growth engine for Web3 marketing, where campaigns are continuously measured and improved.

About Influence360

Influence360 is a Web3 creator marketing platform designed to make influencer campaigns transparent, fairly compensated, and measurable at scale. The platform enables global creator discovery across regions, languages, and niches; structured campaign execution; smart-contract escrow payments; performance tracking linked to real outcomes; and AI-powered campaign strategy and optimization. Visit influence360.io.

The post Influence360 Launches as the First AI & Data-Driven Web3 KOL Platform with Global KOL Coverage and Real Attribution appeared first on BeInCrypto.

Tom Gordon praises facilities during visit to Thistle Hill

Partnership boosting access to collagen, gelatin ingredients

On-Chain Demand Falls to 2026 Lows; Bitcoin Could Test $72K

-

Crypto World4 days ago

Crypto World4 days agoBlockchain.com files with SEC for U.S. IPO

-

Fashion3 days ago

Fashion3 days agoHoliday Weekend Open Thread – Corporette.com

-

Crypto World3 days ago

Crypto World3 days agoBitcoin Accumulation Weakens as BTC Realized Losses Hit $600M

-

Business3 days ago

Business3 days agoDell Technologies DELL Stock Surges 15% on AI Server Momentum and Analyst Upgrades in 2026

-

Crypto World3 days ago

Crypto World3 days agoSpace X IPO Is ‘Bad News’ for Tech Stocks: But What About Bitcoin?

-

Politics3 days ago

Politics3 days agoMakerfield: a tale of two social-media histories

-

Crypto World2 days ago

Crypto World2 days agoRobinhood crypto COO Tanya Denisova exits

-

Crypto World3 days ago

Crypto World3 days agoMicroStrategy’s Saylor Says Miners No Longer Set Bitcoin Price, Another Force Has Taken Over

-

Business20 hours ago

Business20 hours agoNYT Strands Answers May 24 2026 Revealed for Puzzle No. 812 Theme Summer Essentials

-

Crypto World3 days ago

Crypto World3 days agoAI infrastructure race heats up as IREN pitches full-stack strategy, WhiteFiber lands $160M deal

-

Tech3 days ago

Tech3 days agoA 0.12% parameter add-on gives AI agents the working memory RAG can’t

-

Tech4 days ago

Tech4 days agoWhatsApp ads could make Irish debut after discussions with DPC

-

Tech3 days ago

Tech3 days agoYou Can Now Add ChatGPT To PowerPoint

-

Business3 days ago

Business3 days agoTrump Invests $1M-$5M in Kura Sushi USA Chain With 27 California Locations

-

Crypto World7 days ago

Crypto World7 days agoRevolut Launches Dogecoin Debit Card Across UK and EU

-

NewsBeat4 days ago

NewsBeat4 days agoCharity run by Reform leader Malcolm Offord accused of ‘law breaking’ over Scottish registration

-

Sports4 days ago

Sports4 days ago2026 CJ Cup Byron Nelson leaderboard: Brooks Koepka finds putting stroke in Round 1

-

Crypto World3 days ago

Crypto World3 days agoTrump Media’s Bitcoin Stash Shrinks Again as 2,650 BTC Lands on Crypto.com

-

Business3 days ago

Goldman Sachs reinstates Ageas stock coverage with neutral rating

-

Crypto World5 days ago

Crypto World5 days agoExa Labs raises $250 million in funding led by a16z

You must be logged in to post a comment Login