Business

BofA raises Pfizer stock price target on first-quarter beat

Workers in southern Scotland can find themselves paying more tax than colleagues who live south of the border.

There is a particular kind of dinner I have, every couple of months, in a particular kind of place, a Soho members’ club that lets you bring more than three people without an interrogation, in this case, with a particular kind of British technology founder.

He is, by his late thirties, on his third successful company. He has, between them, raised something north of £180 million in venture capital. He has, currently, about 220 employees in London, with another fifty due to be hired in the coming twelve months. He has, last week, sold a further $40 million tranche of his Series C to two American funds.

And he has, somewhere between his second and third glass of red, told me that he is moving the company’s headquarters to New York. Not on principle. Not on tax. Not on regulation. Not even, despite the obvious temptation in this column, on the Chancellor. He is moving because the next $200 million he needs, in 18 months, is in New York, and the practical day-to-day life of a CEO in a series of monthly trips to a city eight time zones from his children is, frankly, too painful. So he is moving the family. The London office will remain. It will, over time, get smaller. A version of this conversation has happened, by my count, with at least twelve British founders I know personally in the last two years.

Britain does not, in 2026, have a start-up problem. We start-up exquisitely. We have, by any international comparison, more new technology businesses per capita than nearly any other developed economy. Cambridge is, on its own, one of the great clusters of the world. London’s software and fintech ecosystems are deeper than Berlin’s, deeper than Paris’s, comparable to New York’s on most measures, with a couple of exceptions. We have brilliant universities, a working tax-incentive regime in EIS, a meaningful angel community, and a steady flow of seed and Series A capital.

What we have is a stay-at-home problem.

The numbers are visible if anyone bothers to look. UK technology IPOs, by listed value, are running at less than 12 per cent of US listings adjusted for relative GDP. UK Series C and onwards rounds are dominated, by deal count, by American lead investors. The proportion of UK technology companies founded in 2018 that have, by 2025, relocated their corporate domicile overseas, to the US, to Delaware, to Ireland, to Singapore, is now over 22 per cent. The proportion of all UK-founded unicorns that listed on the New York Stock Exchange or Nasdaq, rather than the London Stock Exchange, is over 80 per cent for the last decade. Eighty.

Why? It is not, despite the City lobbying, primarily a tax problem. American capital gains rates are not, in any meaningful sense, more friendly to founders than British rates. It is not, despite a great deal of Treasury-led discussion, a corporate-tax problem. The US corporate tax rate, when you blend federal and state, is comparable. It is not, despite the political mood music, a regulatory problem in the technology sectors that matter, the FCA, where it counts for fintech, is a notably more friendly regulator than its American equivalent.

It is, primarily, a depth-of-capital-pool problem. The UK pension system, despite the most articulate efforts of the Edinburgh Reforms and the Mansion House Compact and a half-dozen subsequent initiatives, allocates an embarrassingly small proportion of its £3 trillion of assets to growth-stage British equities. Canadian pension funds are, statistically, more invested in British scale-ups than British pension funds. This is the absurdity of the present situation: the world’s ninth-largest pension industry, hosted in Britain, is not investing in British growth, and is being out-deployed, in British growth equity, by Canadians, Australians, and Americans.

Fix the depth, and the rest of the problem largely goes with it. There are about three things to do. First, get UK Defined Contribution pension money, which is, by the way, growing at over £100 billion a year, into a properly structured British scale-up vehicle, at a meaningful target allocation, with a proper governance overlay. Second, restore the pre-2008 status of the London Stock Exchange as a competitive listing venue for technology businesses, by reforming the dual-class share structures and the listing-rules architecture that has kept it stranded in the era of utilities and miners. Third, make the EIS reliefs permanent, generous, and unfussy at the seed stage, so that the early-stage capital remains the easiest tier to raise.

None of this is impossible. None of this is even, in the international context, particularly bold. The Australians did most of it in 2008. The Canadians did most of it in 2014. The Singaporeans built theirs in around six years. We are, in 2026, still pondering it.

And in the meantime, my Soho friend will, in the autumn, leave. He will take the family. He will keep the London office. The American round will close. The next British unicorn, and there will be a next British unicorn, will, on present trajectory, list, again, in New York. The Mayoral candidates will, on the day after, all denounce the loss to “Brand London”. And the bottle of red, in our particular Soho members’ club, will be uncorked, again, by someone else.

We start-up brilliantly, in this country. We just need, finally, to learn how to keep them. The May locals, it turns out, are not the only thing on the ballot.

Richard Alvin

Richard Alvin is a serial entrepreneur, a former advisor to the UK Government about small business and an Honorary Teaching Fellow on Business at Lancaster University.

A winner of the London Chamber of Commerce Business Person of the year and Freeman of the City of London for his services to business and charity. Richard is also Group MD of Capital Business Media and SME business research company Trends Research, regarded as one of the UK’s leading experts in the SME sector and an active angel investor and advisor to new start companies.

Richard is also the host of Save Our Business the U.S. based business advice television show.

MaxLinear director Daniel Artusi sells $825,728 in company stock

Ramil Asadulzada is an experienced executive with more than 20 years of leadership across finance, strategy, and operations. Born in Baku, Azerbaijan, he grew up in a humble family shaped by discipline and education.

His father served in the military and his mother was a teacher. From a young age, Ramil showed strong leadership and analytical skills. He captained his school basketball team and regularly competed in mathematics Olympiads, often earning top awards.

He earned his Bachelor of Science from the Azerbaijan State Oil Academy before building an international career across Azerbaijan, Turkey, Switzerland, and Romania. Over the past 15 years, he held senior finance roles, serving as CFO and most recently as CEO of SOCAR Petroleum SA, where he was promoted to Chief Executive in January 2024.

Ramil is known for his expertise in financial analysis, IFRS, risk management, corporate strategy, M&A, supply chain management, and large-scale project leadership. He combines financial discipline with operational clarity. He holds an MBA with Honours from The University of Chicago Booth School of Business and is a member of ACCA.

Oil and gas remains his professional passion. He is recognised for leading large teams while maintaining strong relationships across all levels of business. Outside of work, he enjoys basketball, travelling, reading professional literature, and following Real Madrid. A lifelong learner, Ramil approaches leadership with humility, precision, and long-term vision.

Q: You were born in Baku and grew up in a military household. How did your early life shape your leadership style?

I was raised in a very simple and humble family. My father was a military serviceman and my mother was a teacher. Discipline and education were part of daily life. There was structure at home. There was respect for learning. That environment shaped how I approach work today.

As a child, I loved mathematics. I competed in Olympiads and often won gold prizes. Mathematics teaches logic and problem solving. It forces you to think clearly. I also played basketball and served as team captain. Sport taught me leadership. You learn quickly that you win as a team or you lose as a team.

Q: What led you into the oil and gas industry?

I studied Economy and Management of Production and Service Fields at the Azerbaijan State Oil Academy. Oil and gas is a key industry in Azerbaijan. It is part of our economic identity. Naturally, I was drawn to it.

Over time, it became more than an industry. It became a passion. The scale of operations, the capital intensity, the global exposure — it is a complex and strategic field. I enjoy that complexity.

Q: You spent more than 11 years at SOCAR and rose from CFO to CEO. How did that journey unfold?

My career has been heavily focused on finance and strategy. For roughly 15 years I held CFO positions, and in January 2024 I was promoted to CEO of SOCAR Petroleum SA.

As CFO, my responsibility was financial discipline. IFRS reporting, risk management, budgeting, forecasting, internal controls, and audit were central to my role. We managed large-scale operations across multiple countries. That required precision.

When I became CEO, the perspective shifted. You still rely on financial rigour, but you must think more broadly. Strategy, people management, commercial positioning, supply chain resilience — all become interconnected.

Q: What was the most challenging transition from CFO to CEO?

As CFO, you evaluate risk and protect the balance sheet. As CEO, you balance risk with growth. You must make decisions that affect thousands of stakeholders.

One challenge is moving from detailed financial analysis to big-picture leadership. I learned to trust the systems and the teams we built. Strong internal controls and governance frameworks allowed me to focus on long-term direction rather than day-to-day issues.

Q: You have worked internationally in Azerbaijan, Turkey, Switzerland and Romania. How has that shaped your executive approach?

International experience teaches adaptability. Regulations differ. Market conditions differ. Cultural expectations differ.

Working in Switzerland strengthened my understanding of governance and financial transparency. Turkey and Romania exposed me to dynamic markets. Azerbaijan grounded me in operational depth.

You learn to listen more. You learn that leadership must adapt without losing consistency.

Q: How did your MBA at Chicago Booth influence your thinking?

The MBA at The University of Chicago Booth School of Business was transformative. The programme is analytical. It challenges assumptions. I graduated with honours, which was important to me personally.

Booth reinforced the importance of data-driven decision making. It sharpened my approach to corporate strategic planning and M&A. It also expanded my global network.

Q: What defines strong leadership in oil and gas today?

Oil and gas remains a highly strategic industry. It requires operational efficiency, strict compliance, and risk awareness.

Strong leadership today means balancing profitability with sustainability. It means maintaining high standards of safety and governance. It means preparing for volatility.

I believe clarity is critical. Teams perform better when objectives are defined. Large-scale projects require strong project management skills. I gained much of that experience managing complex operations and cross-border initiatives.

Q: You led large teams across functions. How do you maintain alignment at scale?

Communication and structure. When you lead large teams, you must create systems that allow transparency and accountability.

I focused on building relationships across all levels of the organisation. Whether with senior management or frontline staff, consistency matters. Respect matters.

Leadership is not only about direction. It is about creating an environment where people can perform at their best.

Q: Outside of work, what keeps you grounded?

Basketball remains important to me. Real Madrid is my favourite football club. Cristiano Ronaldo’s discipline and work ethic inspire me.

I enjoy travelling and reading professional literature. I am a lifelong learner. Oil and gas is my passion, but I believe growth comes from constant education.

I also support charitable initiatives quietly. I believe helping others should not require publicity.

Q: Looking back, what lesson stands out most from your career?

Discipline compounds over time. Whether in mathematics competitions as a child, on the basketball court, or in boardrooms, preparation matters.

Long-term thinking is essential. Short-term decisions can create long-term consequences.

For me, leadership is about responsibility. You must build systems that outlast you. That is the true measure of impact.

Romer Debbas managing partner Pierre Debbas rips the New York City mayor over plans for the Big Apple on ‘Varney & Co.’

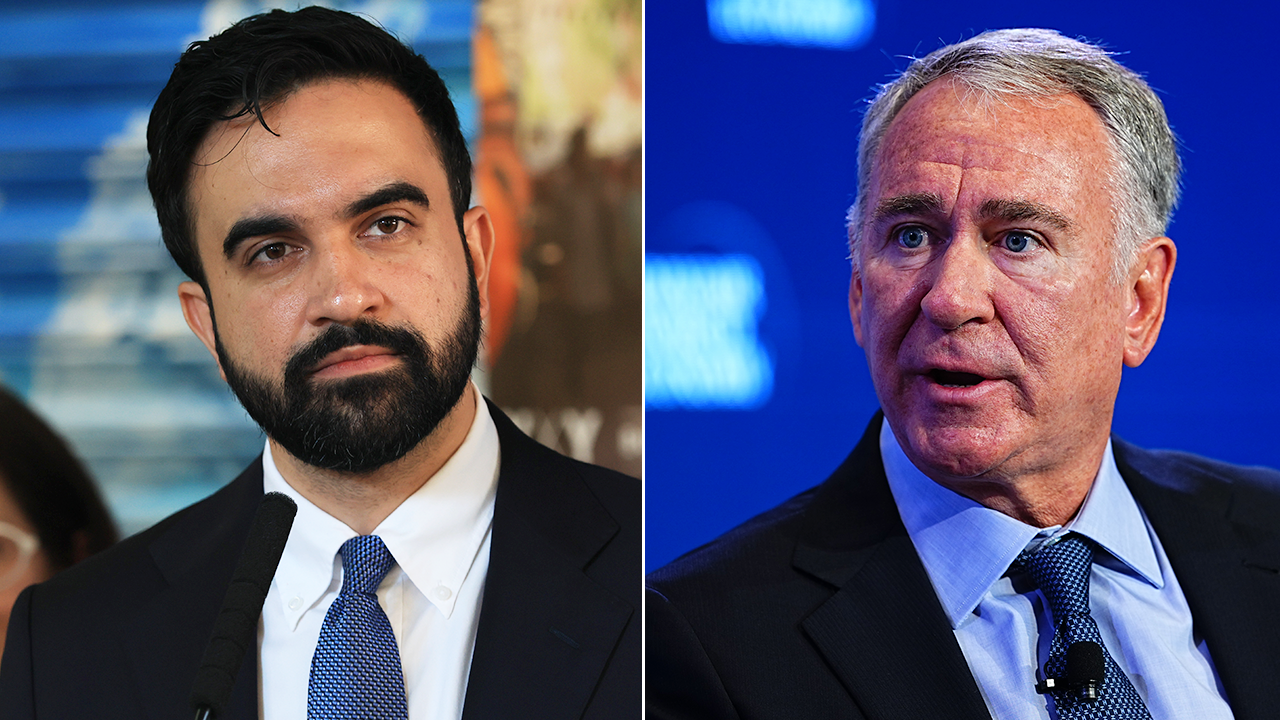

Citadel founder and CEO Ken Griffin described New York City Mayor Zohran Mamdani’s “tax the rich” video targeting him as a “creepy and weird” political advertisement.

Speaking at the Milken Conference in Los Angeles on Tuesday, Griffin said Mamdani’s “frightening” video reaffirmed his decision to “double down” on business in Miami.

“Mamdani has made it very clear—New York does not welcome success,” Griffin said during the panel.

MAMDANI’S CLASH WITH BILLIONAIRE PUTS NYC STREET FOOD VENDORS IN THE CROSSHAIRS

On April 15 (Tax Day), NYC Mayor Zohran Mamdani posted a video outside Ken Griffin’s Manhattan penthouse promoting a new “tax-the-rich” policy. (Spencer Platt/Aaron Schwartz/Bloomberg/Getty Images / Getty Images)

On April 15, Mamdani posted a video highlighting Griffin’s property while announcing a new pied-à-terre tax.

The video shows Mamdani—who has pledged to raise taxes on wealthy New Yorkers—standing outside Griffin’s 24,000-square-foot property. Griffin purchased the home in 2019 for $238 million, the most expensive residential sale in U.S. history.

“This is an annual fee on luxury properties worth more than $5 million whose owners do not live full-time in the city—like this penthouse, which hedge fund CEO Ken Griffin bought for $238 million,” Mamdani said while announcing the proposal.

Following the video, Citadel COO Gerald Beeson suggested that plans for the firm’s skyline project at 350 Park Avenue could be reconsidered.

NEW HAMPSHIRE GOVERNOR RECRUITS NYC BUSINESS OWNERS FLEEING MAMDANI ‘REGIME’

New York City Mayor Zohran Mamdani has previously criticized billionaires, including Ken Griffin, whom he recently thanked for supporting police. (Spencer Platt/Getty Images / Getty Images)

“We are about to commence the redevelopment of 350 Park Avenue, creating 6,000 highly paid construction jobs and supporting more than 15,000 permanent jobs in Midtown New York,” Beeson wrote in an April 23 memo to employees.

“The project—if we move forward—will involve more than $6 billion in spending,” he added.

Griffin said Tuesday that the project’s future remains “a point of discussion” within the company.

Mayor Mamdani’s office did not immediately return Fox Business’ request for comment.

Citadel is currently building a new headquarters in Miami. Griffin told the Milken audience that the tower’s design is being revised to “make it bigger,” adding that Florida’s leadership has demonstrated stronger support for pro-business policies.

Griffin, who founded Citadel and Citadel Securities, previously moved both firms from Chicago to Miami following the COVID-19 pandemic. He has frequently criticized leadership in Chicago and the broader state of Illinois.

Citadel Founder and CEO Ken Griffin called New York City Mayor Zohran Mamdani’s viral video singling out his Manhattan penthouse while announcing a new tax a “personal attack” and a “profound lack of judgment.” (Denis Balibouse/Reuters / Reuters)

On Tuesday, Griffin said his dispute with Mamdani is “triggering the trauma” he “experienced in Chicago.”

MAHER DEFENDS CAPITALISM AS BETTER THAN ‘REVERSE,’ CALLS OUT MAMDANI’S SOCIALIST BELIEFS

With an estimated net worth of $51 billion, Griffin ranks among the world’s 35 richest people. He has also said Mamdani’s video reflects a “profound lack of judgment.”

Speaking at the Norges Bank Investment Management 2026 Investment Conference in Oslo, Griffin criticized what he described as the “demonizing” of business leaders.

New York Mayor Zohran Mamdani speaks during a press conference at Staten Island University Hospital Community Park on April 27, 2026, in New York City. (Michael M. Santiago/Getty Images / Getty Images)

GET FOX BUSINESS ON THE GO BY CLICKING HERE

“What upset me was the personal attack,” Griffin said. “You were at the White House Correspondents’ Dinner on Saturday, where they tried to assassinate the president. Not far from where I live in New York is where the CEO of UnitedHealthcare was assassinated.”

FOX Business’ Louis Casiano contributed to this report.

Meta director Peggy Alford sells $251,342 in stock

Business

GlobalFoundries Stock Is Upgraded Ahead of Earnings. It’s a Big Week for the Chip Manufacturer.

GlobalFoundries Stock Is Upgraded Ahead of Earnings. It’s a Big Week for the Chip Manufacturer.

A ‘Mornings with Maria’ panel assesses the oil markets amid the conflict with Iran, Jamie Dimon’s warning of risks in the credit and debt markets and earnings season.

U.S. financial regulators are proposing to switch required filings for publicly traded companies from quarterly reporting to semiannual.

The Securities and Exchange Commission on Tuesday released its amended proposal for optional semiannual reporting for companies on Wall Street. SEC officials say the change in frequency of reporting won’t impact the type of information disclosed publicly. Companies will be expected to file a new form called Form 10-S in lieu of the traditional Form 10-Q if they choose to report twice a year.

SEC Chairman Paul Atkins says this proposal will allow for more freedom between companies and investors.

BAY AREA BANKER WANTS TO SWAP HIS $8M ESTATE FOR AI COMPANY STOCK

SEC Chairman Paul Atkins says this proposal will allow for more freedom between companies and investors. (Michael Nagle/Bloomberg via Getty Images)

“The rigidity of the SEC’s rules has prevented companies and their investors from determining for themselves the interim reporting frequency that best serves their business needs and investors,” Atkins said in a statement. “Today’s proposed amendments, if ultimately adopted, would provide companies with increased regulatory flexibility in this regard.”

The SEC attempted to ease the concerns of investors, saying corporations can still hold quarterly earnings calls even if they choose semiannual reporting. (iStock)

However, some investors are skeptical about how this benefits anyone other than the companies.

Gary Kaltbaum, president of Kaltbaum Capital Management and a FOX Business contributor, said this will pave the way for less clarity for investors to make decisions on Wall Street.

COULD S&P 500 ETFS ALONE FUND YOUR ENTIRE RETIREMENT?

“The No. 1 reason why stocks do well is because of their earnings reports,” Kaltbaum said. “And now that you’re going to separate it by six months, that’s tough going for investors to try and figure out what’s going on with a company when you’re not going to hear from them in six months.”

Under the current proposal, companies will be given the opportunity to opt-in for semiannual reporting at the start of every fiscal year. (Michael Nagle/Bloomberg via Getty Images)

The SEC attempted to ease the concerns of investors, saying corporations can still hold quarterly earnings calls even if they choose semiannual reporting. The Wall Street regulator says they’re not mutually exclusive, but critics are skeptical that companies would bother with quarterly earnings calls since they don’t have to make public disclosures as frequently.

US ETF ASSETS UNDER MANAGEMENT TO MORE THAN DOUBLE TO $25T BY 2030, CITIGROUP SAYS

Under the current proposal, companies will be given the opportunity to opt-in for semiannual reporting at the start of every fiscal year. If companies don’t like the new reporting practices, then they can opt back into quarterly reporting the following fiscal year.

The SEC says the public comment period will be open for the next 60 days after publishing the proposal in the Federal Register.

Fast moving industries are make it or break it. Worse, they are constantly shifting. Who the biggest player is in the market can change from one day to the next.

A new tech, a new tool, a new game, all of this can shake up who is successful and who is not. More importantly for industries that are regulated, like the gaming industry, new regulations can immediately drop the biggest fish off the map, while those who put player satisfaction and safety at the forefront rise to the top.

Longevity is difficult to maintain in a fast-moving industry, especially a digital industry where updates can roll out instantly. You don’t need to restructure your supply chain or wait for a product or service to reach your customers. The only problem with this instant delivery is that your competitors also have access to that same level of quick-fire delivery.

That’s why longevity is all about standing out and delivering on a specific experience again and again:

The Importance of Theme and Niche in a Fast-Moving Market

Digital industries shift fast, and not only on the platforms themselves. Sometimes the biggest challenge is both how many competitors there are, and also how many newcomers are arriving on the scene. This is a challenge both for the existing providers and the newcomers themselves.

That’s why one of the top ways that platforms are working to maintain the long-term interest of their players is by building their platform around a visual niche. This is particularly important in industries like iGaming, where platforms can look nearly identical from one provider to the next.

In this sort of environment, brands like River Belle, which have been built around a specific visual niche (in this case, a luxury vintage steamer ship), are leading the way. Not only have they built a memorable, striking, and engaging niche, but they have also followed it up by putting their live casino game experiences at the forefront.

New Games, New Experiences

Digital platforms have the benefit of being able to see the numbers in detail. They know exactly where their audience is spending their time, what games they’re playing, for how long, and what’s most popular.

That’s why they can easily keep the top playing games, restructure those that have potential, and still release new games and variations that keep players coming back. More importantly, those analytics can actually be used to predict future game success by understanding current appetites. This approach keeps the platform fresh while also avoiding the alienation that can come from taking down a top-performing game by mistake.

Safety, Safety, Safety

When there are so many competitors and the industry moves fast, being reliable is the easiest way for platforms to ensure their longevity. Using the latest security features to both reduce friction in the sign-up and deposit process, while also delivering secure and timely withdrawals, boosts trust and the overall experience. When competitors are screaming at the top of their lungs for attention, the options may seem endless, but customers will still ultimately go where they know they are safe. Being scammed and fooled is every digital customer’s top fear, so providing that safety and assurance is one of the last top ways digital platforms are maintaining their long-term success.

Restaurant owners have spent years refining the customer journey through booking tools, POS platforms, kitchen display systems, loyalty apps and payment technology.

Yet many hospitality businesses are now looking beyond the dining room for inspiration, and a practical PMS system guide for hotels can be surprisingly useful for understanding how accommodation-led businesses connect reservations, payments, guest profiles, and daily operations into a clearer commercial picture.

That matters because restaurants are no longer judged only on food and service. Guests expect accuracy, speed, personalisation and consistency across every touchpoint. The same customer who books a boutique hotel online also expects a restaurant to remember dietary preferences, process payments smoothly and handle last-minute changes without confusion.

Why Restaurant Operators Should Care About PMS Thinking

A Property Management System, or PMS, is traditionally associated with hotels. It helps manage room bookings, guest records, housekeeping, billing and availability. At first glance, that may seem far removed from a restaurant POS system. But the underlying business logic is very familiar.

Both restaurants and hotels depend on:

- Accurate availability

- Fast service delivery

- Clean customer data

- Efficient staff workflows

- Clear reporting

- Reliable payment handling

For restaurant owners, the lesson is not that they need to run hotel software. It is that the best hospitality systems are built around the full guest journey rather than isolated transactions.

A modern PMS system in a hotel environment gives managers a joined-up view of guests, bookings, charges, and service requirements. Restaurants can apply the same principle by connecting table reservations, POS data, stock usage, marketing preferences and customer history.

The Shift from Transactional Systems to Guest-Centred Operations

Many restaurants still think of software in separate boxes. The POS handles sales. The booking platform manages reservations. The stock system monitors ingredients. The loyalty tool sends offers. Each product may work well on its own, but the business can still feel fragmented.

Hotels faced this problem years ago. A guest might book online, request an early check-in, order room service, visit the bar and pay at reception. Without connected systems, the experience becomes clumsy for both staff and guests.

Restaurants face similar challenges when:

- A regular guest books online but is not recognised by the front-of-house staff

- A POS system records spend but does not inform marketing

- A kitchen runs out of an item that is still available on digital menus

- A private dining enquiry is managed outside normal reporting

- A loyalty reward is missed because customer data is incomplete

The value of PMS-style thinking is that it encourages operators to view software as an operational ecosystem rather than a collection of tools.

Lessons from Hotels That Restaurants Can Apply

1. Treat customer data as an operational asset

Hotels depend on guest profiles. Preferences, previous stays, spending patterns and special requests all influence service quality. Restaurants can benefit from the same mindset.

A guest who regularly orders vegetarian dishes, prefers a quiet table, or books for business lunches is giving the business useful information. When handled responsibly, this data can improve service without feeling intrusive.

The goal is not to over-personalise. It is to help staff make better decisions.

2. Make availability visible and accurate

Hotel teams live and die by availability. Rooms cannot be sold twice, and poor availability management damages revenue. Restaurants deal with the same issue through table capacity, kitchen load, staff coverage and event space.

The discipline used in PMS systems for small hotels can be useful here. Smaller hotels often need lean, practical systems that prevent overbooking without creating unnecessary administration. Restaurants, especially independents and small groups, need similar clarity around covers, sittings and peak-time capacity.

3. Connect payments to the customer journey

In hotels, charges may come from the room, restaurant, spa, minibar or event space. A good PMS keeps billing coherent. Restaurants can learn from that approach, particularly those offering deposits, delivery, catering, events, memberships or gift cards.

Payment should not be treated as the final step only. It is part of the experience. A slow bill split, a missing deposit, or an unclear service charge can weaken an otherwise excellent meal.

Why This Matters for B2B Restaurant Software Buyers

Restaurant software buyers are becoming more commercially mature. They are not simply asking, “Does this POS take payments?” They are asking whether technology can reduce labour pressure, improve margins and support better decision-making.

For B2B restaurant software clients, the bigger questions are:

- Does the system reduce duplication of work?

- Can managers see useful reporting without exporting spreadsheets?

- Does it integrate with booking and payment platforms?

- Can staff learn it quickly?

- Does it improve the guest experience?

- Will it scale as the business grows?

These are the same questions that hotel operators ask when assessing PMS for small hotels. The scale may differ, but the buying logic is similar: the software must make the business easier to run.

Small Hospitality Businesses Need Practical, Not Overbuilt, Systems

There is a temptation in hospitality technology to add features because they sound impressive. In reality, many operators need fewer features that work better together.

PMS systems for small hotels are often judged on usability, affordability and operational clarity. The same should apply to restaurant technology. A small restaurant group does not need enterprise complexity if the team cannot use it confidently during service.

The most valuable software usually supports everyday work:

- Taking bookings accurately

- Managing walk-ins fairly

- Processing orders quickly

- Updating menus easily

- Tracking stock sensibly

- Reporting sales clearly

- Supporting repeat customers

- Reducing manual admin

Technology should remove friction. It should not become another operational burden.

The POS Is Still Central, But It Should Not Stand Alone

For restaurants, the POS remains the heart of daily operations. It captures revenue, drives kitchen communication, supports payments and provides sales reporting. But the POS becomes far more powerful when it sits within a connected hospitality stack.

A standalone POS can tell you what sold yesterday. A connected system can help explain why it sold, who bought it, whether the margin was strong and what action should follow.

That is where PMS thinking becomes useful. Hotels have long understood that operational data is only valuable when it supports decisions. Restaurants can use that same approach to improve rota planning, menu engineering, customer retention and event sales.

What Restaurant Owners Should Look For Next

Restaurant operators do not need to copy hotels directly. A restaurant is not a bedroom inventory business, and the service rhythm is different. But the best hospitality technology shares common qualities.

Owners should look for systems that are:

- Simple enough for staff to use under pressure

- Flexible enough to support different revenue streams

- Clear enough to inform management decisions

- Open enough to integrate with other tools

- Secure enough to protect customer and payment data

- Scalable enough to grow with the business

The strongest technology choices are rarely the flashiest. They are the ones that fit the operation, improve consistency and help the team serve guests better.

Final Thoughts: Hospitality Software Is Moving Towards One Guest View

The future of restaurant technology is not about replacing people with systems. It is about giving people better information at the right moment.

Hotels, especially those using modern PMS platforms, have already shown the value of joined-up guest management. Restaurants can take the same strategic lesson and apply it to tables, orders, payments, loyalty and events.

For restaurant owners, POS buyers and B2B software clients, the opportunity is clear: stop thinking only in terms of transactions and start thinking in terms of relationships. A better-connected system does not just make reporting cleaner. It helps create smoother service, smarter decisions and more resilient hospitality businesses.

Forward Industries, RockawayX Invest in OnRe Reinsurance

Met Gala AI-Generated Photos Sparks Reactions

the strong emotions and memories around these meals reflect their social, economical and cultural importance

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

NewsBeat2 days ago

NewsBeat2 days agoChannel 5 – All Creatures Great and Small series 7 new post

-

Tech4 days ago

Tech4 days agoTrump’s 25% EU auto tariff breaches Turnberry Agreement that also covers semiconductors and digital trade

-

Sports4 days ago

Sports4 days agoPaul Scholes issues Marcus Rashford reality check as agreement emerges over Man United star

-

Business6 days ago

Business6 days agoTesla Officially Registers Elon Musk’s Stock: What Investors Need to Know

-

Business7 days ago

Business7 days agoBarclay Brothers Avoid Bankruptcy: HSBC Drops High Court Petitions After IVA Deal

-

Entertainment6 days ago

Entertainment6 days agoCelebrities Who Are Attending the 2026 Met Gala Event

-

Entertainment4 days ago

Entertainment4 days agoMet Gala 2026 Rumored Guest List Is Turning Heads

-

Entertainment6 days ago

Entertainment6 days agoInsider Claims Reason Behind Key & Peele Split

-

Tech6 days ago

Tech6 days agoTexas Instruments made a new flagship graphing calculator: the TI-84 Evo

-

Business5 days ago

Business5 days agoTwo Powerball Tickets Split $143 Million Jackpot in Indiana and Kansas

-

Business6 days ago

Business6 days agoStrait of Hormuz Remains Heavily Restricted on April 29 Amid Iran Conflict

-

Crypto World6 days ago

Crypto World6 days agoMeta (META) starts stablecoin payout to creators in Circle’s USDC on Polygon, Solana via Stripe

-

Business2 days ago

Winning Numbers Drawn as Jackpot Resets to $20 Million

-

Crypto World5 days ago

Crypto World5 days agoCoreWeave (CRWV) Stock Climbs 8% Despite $45M Insider Share Dump

-

Business5 days ago

Strait of Hormuz Blockade Persists Amid US-Iran Standoff, Sending Oil Prices Soaring

-

Entertainment4 days ago

Entertainment4 days agoKylie Jenner Hit With Second Lawsuit From Ex-Housekeeper

-

Crypto World6 days ago

Crypto World6 days agoSecuritize and Computershare Enable Tokenized Equity Issuance for Over 25,000 U.S.-Listed Stocks

-

Sports6 days ago

Sports6 days agoSaudi Arabia set to withdraw LIV Golf funding after 2026 season, per reports

-

Sports4 days ago

Sports4 days agoDavid Benavidez responds to team Canelo saying the fight will never happen

-

Crypto World6 days ago

Crypto World6 days agoGibraltar Proposes Tokenized Funds Regulation to Bolster Compliance

You must be logged in to post a comment Login