Crypto World

Are we done Finding Satoshi?

Even after more than a decade and a half, the identity of Bitcoin’s pseudonymous creator, Satoshi Nakamoto, is still an active mystery that provokes discourse and disagreement.

In the last couple weeks, a New York Times piece authored by investigative journalist John Carreyrou suggested that Satoshi is in fact Adam Back, while the recent documentary Finding Satoshi pegged a two-person team, namely Hal Finney and Len Sassaman.

Protos has reviewed the evidence pointing to several of the internet’s favored candidates for this illustrious role and laid out our findings below.

Adam Back

Adam Back, the chief executive officer (CEO) of Blockstream, has often been labeled as a likely candidate for Satoshi.

Among the reasons for this is his identity as a cypherpunk, an online community which believed in the beneficial effects of freedom technology tools developed using cryptography.

Satoshi generally appears to be a cypherpunk, or at the very least to be sympathetic to cypherpunk ideas, regularly citing and conversing with others in the community.

Back was also behind HashCash, another cryptographically based digital cash technology that was cited by Satoshi.

Notably, there exist emails that Back has shared in court cases which seem to show Satoshi reaching out to Back to make sure that he appropriately cites the HashCash paper. This has led Carreyrou to ask us to consider if “Mr. Back…sent those emails to himself as a cover story.”

Carreyrou’s reporting also emphasized the fact that Back shared certain stylistic markers with Satoshi.

Among these similarities were certain phrases like “backup” and “human friendly” as well as inconsistent hyphenation in words like e-mail/email.

Despite these stylistic similarities, there are still differences, with Carreyrou noting, “Mr. Back made a lot of typos and had a rambling style when he posted to mailing lists, while Satoshi’s writing was crisp and mostly typo-free.”

Others, like YouTuber BarelySociable, have also suggested that Back is the most likely Satoshi candidate.

Back strongly denies being Satoshi.

He was also briefly considered as a candidate by Finding Satoshi; however, it concluded he didn’t post at the appropriate times to be Satoshi.

Hal Finney

Hal Finney was a cryptographer who was the first person to receive bitcoin (BTC) from Satoshi.

Like Back, he seems to have many of the necessary skills, even working on a previous digital cash, Reusable Proofs of Work.

Finney was the first person to participate in a BTC transaction with Satoshi.

Read more: Why Hal Finney might not be Satoshi Nakamoto

Multiple previous analyses have pointed to Finney as one of the more likely Satoshi candidates.

Even the stylistic analysis commissioned by Carreyrou initially concluded, “After comparing papers from the 12 suspects to the Bitcoin white paper, Mr. Cafiero’s stylometry program showed Mr. Back as the closest match. But he said it wasn’t a snug fit and that Mr. Finney was a very close second. In fact, the difference between them was barely distinguishable, he said, and he considered the overall result inconclusive.”

In response to this inconclusive result, Carreyrou suggested that Cafiero change the methodology, and “Mr. Cafiero changed the way he computed the distance between the 12 suspects’ texts and Satoshi’s white paper. The result was the opposite of what I’d hoped: Other candidates pulled ahead of Mr. Back. Mr. Cafiero said he considered these results inconclusive too.”

However, there are key stylistic differences between Finney and Satoshi, especially the use of British spellings for many of the words.

Interestingly, Finney at one point proposed creating a protocol called P2Poker that would use his digital cash, RPOW, for poker. Similarly, the original Bitcoin client contained code for a poker client.

Finney was one of the two candidates that Finding Satoshi flags as the likely Satoshi. This was supported by the times of day at which Finney posted.

Additionally, the failure of Satoshi to cite Finney is used as evidence that Finney might be trying to misdirect.

Finney also was apparently quite unproductive in the two months before Bitcoin launched and was coding at that time in C++, the language that the original client used.

Jameson Lopp, a developer in the Bitcoin ecosystem, was interviewed for the documentary due to his post insisting that Finney wasn’t Satoshi.

Lopp focuses on various emails and transactions that were sent by Satoshi while Finney was running a race.

Finney and his wife have both denied that he was Satoshi.

Paul Le Roux

Paul Le Roux created Encryption for the Masses and may be behind TrueCrypt (although denies involvement in the project).

Additionally, Le Roux was behind an international drug cartel, got involved with arms dealing, and was involved in a variety of murders and assassinations.

Besides that illustrious career, some speculate that he may be behind Bitcoin.

Le Roux has been included as a possible Satoshi since 2019 when Evan Ratliff suggested it as a possibility in an article in Wired.

However, Ratliff also noted that there was insufficient evidence at the time to substantiate the idea.

One of the reasons that Le Roux is an attractive candidate is that his arrest corresponds somewhat to some of the late Satoshi posts, suggesting to some viewers that Satoshi’s withdrawal from the public may have been rooted in these legal issues.

Le Roux was arrested in September 2012, after several of his conspirators and associates had been arrested in the months beforehand. Satoshi told Mike Hearn that he’d “moved on to other things” in April 2011.

However, we should note that there are 17 months between these two dates, over a year, for a technology that was only a few years old.

Finding Satoshi considered Le Roux before concluding that he wasn’t the Satoshi candidate, believing he didn’t fit the profile they constructed for him.

Craig Wright

Craig Wright is one of the least likely candidates, despite his prolific claims to being Satoshi.

Wright has spent years in complex legal cases trying to claim various levels of creation, control, or ownership over the Bitcoin system as a whole, eventually committing his reputation to a fork of a fork, Bitcoin Satoshi Vision.

Read more: Craig Wright trial reveals never-before-seen emails from Satoshi Nakamoto

Throughout Wright’s legal battles, judges, lawyers, critics, journalists, and neutral viewers of every sort have regularly observed his willingness to flout reality and invent history.

Eventually courts in the UK ordered Wright to display a notice that made clear that he wasn’t Satoshi, and acknowledge that he had “lied to the Court extensively and repeatedly.”

Dave Kleiman

Dave Kleiman was, largely, pulled posthumously into Satoshi speculation by Wright.

Kleiman was initially suggested as a possible Satoshi candidate when documents suggesting his involvement with Wright to create Bitcoin were distributed to the press in 2015.

Wright would later endorse this theory publicly.

Read more: David Kleiman’s estate appeals Bitcoin verdict, says ‘Wright is wrong’

Kleiman’s family would end up suing Wright, claiming he’d misappropriated Bitcoin-related intellectual property from the partnership between the men.

Wright owes the Kleiman estate substantial amounts in this case.

Len Sassaman

Len Sassaman was a cryptographer and cypherpunk.

Sassaman has been proposed a couple times, often again because he had both the technical skills and desire to build this kind of thing.

There are also some stylistic similarities between the two.

Sassaman died by suicide in July 2011, several months after Satoshi said he had “moved on to other things.”

Read more: Will HBO documentary unveil Bitcoin’s creator, Satoshi Nakamoto?

Sassaman was the other candidate flagged by Finding Satoshi because of the times that he posted.

Additionally, we are told by Sassaman’s widow that Sassaman was very interested in pseudoynyms and avoiding stylometric analysis.

Interestingly, as the documentary observes, Sassaman regularly publicly criticized Bitcoin.

Peter Todd

Peter Todd, a bitcoin developer, was the candidate flagged as Satoshi in the HBO documentary Money Electric.

This theory relied on Todd’s background as a cryptographer, raised by an economist.

Todd denies being Satoshi.

Todd has also been accused of sexual misconduct, allegations he also denies, and he has filed a suit against the person who made the allegations.

Nick Szabo

Nick Szabo is a programmer, cryptographer, and the creator of smart contracts and Bit Gold.

Szabo is one of the forerunners cited in the Bitcoin whitepaper and has been put forward as a Satoshi candidate for years.

Szabo was considered a possible candidate by Finding Satoshi before concluding he didn’t post at the appropriate times to be Satoshi.

Other Satoshi candidates

Dorian Satoshi Nakamoto was originally flagged by Newsweek in a disastrous misdiagnosis.

Wei Dai was considered as a possible Satoshi by Finding Satoshi; however, it concluded he didn’t post at the right times.

Other even less credible candidates have been put forward, including Elon Musk, Ross Ulbricht, and assorted random mathematicians and cryptographers.

Did Finding Satoshi find Finney and Sassaman?

Put simply, the documentary provides effectively zero new insight into the long-standing question: Who is Satoshi Nakamoto?

At one point, Kathleen Puckett, a former behavioral analyst at the FBI, makes the argument that Satoshi is an individual because Satoshi always used “we,” a plural pronoun, just like Theodore Kaczynski, the Unabomber, who she exposed.

That isn’t evidence.

Another piece of “evidence” she cites is the fact that Satoshi cited a book from the 1950s, An Introduction to Probability Theory and Applications, in the whitepaper.

Puckett believes this suggests that Satoshi is either older than we thought or a free thinker.

However, Satoshi cited this paper because he believed that the best way to capture the probability of an attacker catching the honest chain was an example of a “Gambler’s Ruin” problem.

So rather than being evidence about the type of person that Satoshi is, instead it mostly tells us that he knew probability math.

The very fact that every serious investigative journalist, documentarian, and random Twitter personality has their own candidate really suggests that we need to stop trying.

Each and every one uses a different combination of stylistic analysis, a different set of vibes, and a different set of hunches from people who maybe worked with Satoshi; at the end of the day they’re all speculating.

There are quite a few people who have the interest, who have the capability, who were present in these communities at this time.

None of these candidates are willing to sign; none of these candidates are willing to move BTC; none of these candidates (at least the believable ones) claim to be Satoshi.

This is a cryptographic system where every person who investigates it is forced to rely on weak circumstantial evidence, because the cryptography that would provide real evidence will not appear.

Let dead men lie.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Key Insights

- Valuation of TAO depends largely on the actual usage of AI networks and especially on subnets’ expansion.

- Cycles of adoption during 2026-2030 will define the fate of Bittensor – will it become a foundational layer of decentralized AI.

- Utility metrics, such as validator growth and output efficiency, matter more than market speculation at the moment.

Bittensor’s Value Proposition Within the AI Economy

Bittensor has created an interesting niche in the space where blockchain technology meets artificial intelligence and has created a decentralized exchange of machine learning models.

While most cryptocurrencies are based on speculative trading of tokens, the value of the TAO is derived from the network’s utility that involves computing power and performance of AI models running on the network.

Miners, validators, and developers are rewarded through tokens for delivering tangible results, which means that the future prospects for the price of TAO are linked to the network’s efficiency in completing AI tasks. It is precisely this focus on utility that separates Bittensor from other blockchains trying to get into the AI game.

Subnet Expansion as Key Growth Factor

Subnets form a vital part of the Bittensor ecosystem. Every subnet represents a unique AI marketplace that deals with activities like language processing, data indexing, or prediction analysis. Increase in the amount and variety of subnets reflects increasing practical application.

The more AI models enter those subnets, the more network activity there will be. Thus, the demand for TAO tokens will rise as well, because only through using the token can individuals participate in the network and gain incentives. Therefore, the development of subnets is going to be one of the strongest price drivers in the long term.

According to forecasts, the period from 2026 to 2028 will involve the development of mature subnet ecosystems. If this process succeeds, Bittensor will have an opportunity to become an essential component of decentralized AI services.

Adoption Patterns and Market Trends (2026-2030)

The years between 2026 and 2030 can be characterized by specific phases. At the beginning of this period, growth is most likely to depend on roadmap implementation and the stability of current subnets, which involves enhancing scalability, security, and accessibility for developers.

The middle phase (2027-2028) can see the advent of wider adoption because businesses and individual developers will start incorporating decentralized AI applications. At this stage, institutions will pay attention to Bittensor due to cost efficiency compared to centralized AI suppliers.

The latter years (2029 and 2030) can be associated with a mature phase for the project. The value will largely be determined through its relevance within the wider picture of decentralized architecture. Therefore, the value of TAO will no longer depend on hype but on the demand for AI computing.

Utility Metrics Versus Speculative Trends

The first significant change in the TAO valuation paradigm relates to the use of utility metrics. Instead of basing their estimates on the volume of trades, analysts consider the number of validators, the level of computation, and the overall efficiency of the network. These parameters offer a better understanding of the actual demand compared to conventional speculative metrics.

It is possible to assume that the new approach can create a more stable pricing algorithm for Bittensor tokens. The platform will not have the same levels of volatility as pure speculation-based cryptocurrencies. On the other hand, the rate of growth might slow down significantly.

Regulations and Competition

Regulation will be a key consideration for the future of Bittensor. Favorable regulations regarding AI and blockchain technology would contribute to the rapid development of this project. On the other hand, negative regulation would hamper further development and global expansion.

Another aspect to consider in regard to Bittensor’s future is competition. The project faces serious competitive pressure not only from various decentralized AI solutions but also from tech giants, which have a firm grip on the AI market due to the advantage they have in the field of infrastructure.

Nonetheless, the decentralized nature of Bittensor, which makes it an open and incentive-driven platform, allows for collaborative innovation that is not hindered by any central entity.

Risk Factors and Future Prospects

Nevertheless, despite its promise, there are certain risks for Bittensor. For instance, fast evolution in AI technology might leave the network behind. Issues related to security and scalability also need addressing.

Nonetheless, the future prospects of TAO depend on how it succeeds in turning innovation into practical usage. Should the development of subnets continue, and decentralized AI be in higher demand, Bittensor may occupy an important place in the digital world of the future.

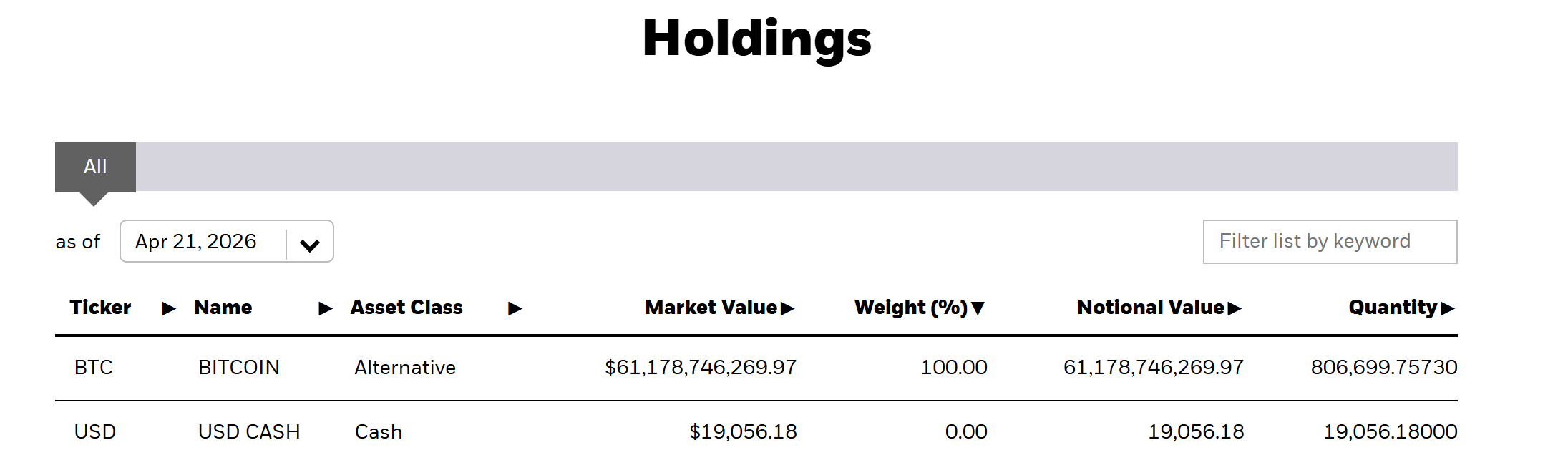

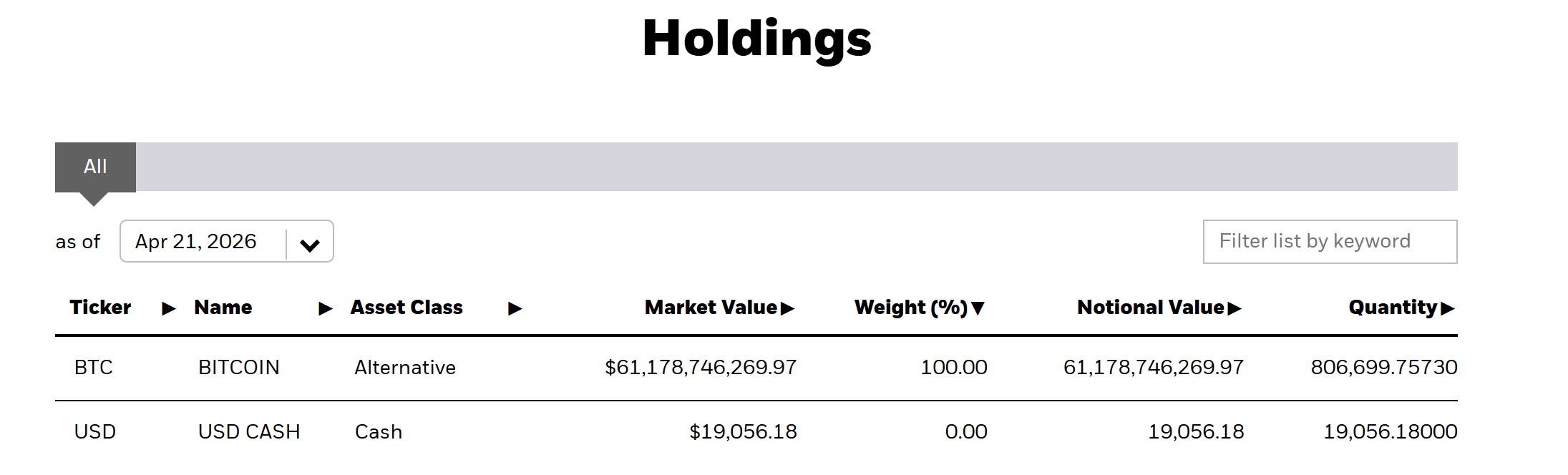

BlackRock’s iShares Bitcoin Trust (IBIT) has accumulated 806,700 Bitcoin (BTC) worth approximately $63.7 billion. The total marks a new all-time high for the world’s largest spot BlackRock Bitcoin ETF.

The record follows nine consecutive trading days of net inflows, during which IBIT added roughly 21,500 BTC. Institutional demand for regulated Bitcoin exposure continues to grow as BTC trades near $78,000.

BlackRock’s IBIT Dominates US Bitcoin ETF Market

BlackRock’s fund now commands roughly 49% of total US spot Bitcoin ETF assets. That puts it well ahead of Fidelity’s FBTC and Grayscale’s GBTC.

The ETF recorded net inflows on 48 of 62 trading days during Q1 2026. Those flows totaled an estimated $8.4 billion for the quarter.

The buying pace picked up in mid-April. IBIT attracted $291.9 million on April 15 and $269.3 million on April 10, according to ETF flow data. That sustained demand pushed total holdings past the 800,000 BTC mark for the first time.

Across the broader market, US spot Bitcoin ETFs have reversed four months of capital flight. The group accumulated roughly $2 billion over four straight weeks of positive net inflows. IBIT contributed approximately $1.7 billion of that total.

MicroStrategy Reclaims Largest Holder Title

Despite the IBIT record, the fund is no longer the single largest corporate Bitcoin holder. MicroStrategy Inc. recently surpassed the ETF with 815,061 BTC on its balance sheet. The firm reclaimed a lead it had lost in Q2 2024.

The Michael Saylor-led firm has bought aggressively this month, adding 13,927 BTC for roughly $1 billion on April 13 alone. The gap between the two now sits at approximately 8,300 BTC.

BlackRock is also broadening its crypto product lineup. The asset manager recently filed an amended S-1 with the SEC for a Bitcoin income ETF under the ticker BITA. The proposed fund would generate yield through a covered call strategy tied to IBIT.

With both IBIT and MicroStrategy continuing to add BTC, the race between the two largest institutional holders may intensify through Q2.

The post BlackRock Bitcoin ETF Holdings Hit Record 806,700 BTC Worth $63.7 Billion appeared first on BeInCrypto.

Russia’s lower house advanced a core digital-currency framework in a first reading on Tuesday, signaling a shift toward a regulated, state-supervised market for crypto activity. The draft law 1194918-8, titled “On Digital Currency and Digital Rights,” would begin to channel crypto trading through licensed intermediaries operating under the Bank of Russia’s oversight, with unlicensed platforms to face a ban in 2027 if enacted. According to official records cited by Cointelegraph, the measure aims to formalize a pathway for crypto commerce while preserving a prohibition on crypto payments within the domestic economy.

Alongside bill 1194918-8, another measure — 1194929-8 — passed its first reading on the same day as part of a broader legislative package aimed at restricting crypto trading to regulated venues. The two drafts together signal Moscow’s intent to move the market toward a licensed, state-supervised structure, even as important enforcement provisions remain unresolved. The Supreme Court weighed in separately on related criminalization efforts, underscoring a recognition that the full regulatory architecture has yet to be adopted.

Key takeaways

- Bill 1194918-8 would legalize crypto purchases and sales through approved intermediaries under Bank of Russia supervision, with the domestic market expected to operate within licensed channels as early as July; unlicensed platforms would be banned starting in July 2027 if the draft becomes law.

- Retail investors would face a framework that restricts access to the most liquid digital currencies defined by the central bank, subject to thresholds on market size, trading history, and a personal investment cap.

- The proposed thresholds require assets to demonstrate an average market capitalization above 5 trillion rubles, an average daily trading volume above 1 trillion rubles, and a trading history of at least five years over the two years preceding listing.

- Retail purchases would be limited to 300,000 rubles per year per intermediary, and a test would be required for retail investors seeking exposure to the restricted set of currencies.

- Residents would be allowed to buy crypto abroad through foreign accounts, provided those transactions are reported to tax authorities; the regime retains a strict prohibition on domestic crypto payments, in line with the 2021 law On Digital Financial Assets.

- Two criminal-penalty proposals, bills 1194944-8 and 1209607-8, seek liability and enforcement measures for unregistered digital-asset services, including registration requirements with the Bank of Russia; the Supreme Court characterized the latter as premature until a broader federal framework is adopted.

Russia’s regulatory architecture: licensing, oversight, and the path to licensure

According to official records cited by Cointelegraph, the core instrument of the package creates a system whereby domestic crypto activity would be funneled through intermediaries that meet regulatory and oversight criteria established by the Bank of Russia. The emphasis on licensing aligns with an overarching policy objective: to reduce unregulated trading and to bring digital-asset activity into a state-supervised framework. The bills explicitly couple the licensing regime with a prohibition on unregistered venues, signaling a centralized approach to market access and participant eligibility.

The two draft measures form part of a broader, multi-bill package described by lawmakers as a comprehensive effort to regulate digital assets in Russia. One companion bill, 1194929-8, passed its first reading concurrently, reinforcing the government’s intent to coordinate licensing, supervision, and compliance across the sector. While the legislative package appears to be advancing in principle, several critical enforcement provisions remain unsettled, raising questions about how the rules would be implemented, monitored, and adjudicated in practice.

Retail investor framework and market implications

The outlined retail framework introduces a calibrated approach to household participation in digital assets. By designating a subset of assets as eligible for retail investment — the “most liquid digital currencies” defined by the Bank of Russia — the regime seeks to balance investor access with risk controls tailored to the domestic market’s maturity. The proposed criteria, including a market-cap threshold, a minimum trading history, and a volumetric requirement, establish a screening mechanism intended to shield participants from assets with insufficient liquidity or longer track records.

From a compliance perspective, the regime implies measurable steps for exchanges and banks that participate in the licensed market. Intermediaries would be responsible for validating asset eligibility, enforcing investment caps, and conducting the investor-test process. A yearly cap of 300,000 rubles per intermediary places a ceiling on retail exposure, potentially affecting demand for certain assets and shaping the speed at which market participants, especially retail investors, can accumulate positions. For residents, the option to purchase crypto via foreign accounts—so long as transactions are reported to tax authorities—introduces a cross-border element that will require robust cross-border AML/KYC controls and tax reporting interoperability with domestic authorities.

Importantly, the regime preserves a strict prohibition on crypto payments within the domestic economy. That clause, anchored in the 2021 law On Digital Financial Assets, remains a core constraint on how digital currencies can function in everyday transactions. Analysts note that while the licensing pathway could usher digital-asset activity into a regulated frame, it could also push a portion of activity into the gray market if participants perceive the compliance burden as onerous or if access to eligible assets is perceived as limited. The enforcement gap highlighted by industry observers underscores a perennial regulatory risk: the balance between formalization and practicable compliance in a shifting market environment.

Enforcement considerations and judicial posture

Beyond the licensing framework, lawmakers introduced two criminal-penalty measures to address violations of the new rules, including unregistered digital-asset services and broader registration mandates with the Bank of Russia. The text of the measures suggests penalties that would carry fines and prison terms for non-compliance. However, the judiciary’s position nuanced the immediate path forward. In a formal review, the Supreme Court stated that the proposed criminal article is premature because it presupposes a federal framework that has not yet been adopted. The court’s language underscored a central regulatory reality: the enforcement architecture depends on the completion and adoption of the broader digital-currency statute that the government is still developing.

The court’s assessment—that “the proposed article is drafted as a blanket provision, the application of which is not possible in isolation from rules directly established by regulatory acts”—highlights the interdependence of legal instruments within Russia’s evolving framework. In practice, this means that while the lower chamber’s first-reading votes indicate political appetite for constraint and oversight, the concrete enforcement pathways will crystallize only as the federal law matures and corresponding regulatory acts are issued. As noted by observers, this sequencing can create transitional risks for licensed intermediaries and for institutions seeking to align operations with anticipated standards.

Context, risks, and policy implications

Russia’s direction mirrors a broader global shift toward centralized oversight of digital-asset markets, but the approach remains distinctly domestic in its design and implementation. The move to restrict trading to regulated intermediaries, the emphasis on BoR-defined asset liquidity, and the cross-border reporting provisions together create a regulatory skeleton that would govern market access, investor participation, and supervisory responsibilities. While advancing the policy objective of reducing illicit or unregistered activity, the package raises questions about its practical effects on market liquidity, innovation, and cross-border activity, as well as on the sector’s recovery trajectory from prior shocks and hacks that have affected confidence in domestic platforms.

From a compliance and institutional perspective, the bills’ framework could necessitate significant adjustments by exchanges, custodians, banks, and financial-service providers that facilitate crypto activity. Licensing criteria, ongoing reporting obligations, and the proposed investor-protection tests would require robust onboarding controls, audit trails, and regulatory coordination with the Bank of Russia and tax authorities. In a broader policy context, the measures sit alongside ongoing international dialogue about crypto regulation, including contrasting approaches with global frameworks such as the European Union’s MiCA, and with U.S. authorities’ enforcement regimes coordinated by agencies like the SEC, CFTC, and DOJ. While direct interoperability with MiCA is not implied in the Russian texts, the emphasis on licensing, supervision, and compliance structures situates Russia within a growing cohort of jurisdictions pursuing formalized market governance for digital assets.

Experts have cautioned that overly stringent limits or a slow legislative process could incentivize activity to migrate underground or to unregulated actors, potentially undermining the stated objective of protection and oversight. The current readings illustrate a cautious, staged approach: formalizing licensed venues, clarifying investor eligibility, and reserving the question of enforcement for a subsequent phase as the federal framework materializes. The practical implication for market participants is the need to monitor not only the bills’ text but also the regulatory guidance and licensing criteria that will define who qualifies as an intermediary and how asset eligibility will be operationalized in real markets.

Closing perspective

Tuesday’s first-reading votes mark an important milestone in Russia’s ongoing attempt to structure its digital-asset market around licensed, state-supervised channels, while acknowledging that the legal architecture remains incomplete. The coming sessions will determine whether these measures solidify into law and how enforcement rules will be harmonized with the evolving federal framework. For institutions, exchanges, and banks, the immediate implication is heightened attention to licensing pathways, compliance readiness, and cross-border reporting obligations as Russia charts a course toward a regulated but evolving digital-currency environment.

Crypto World

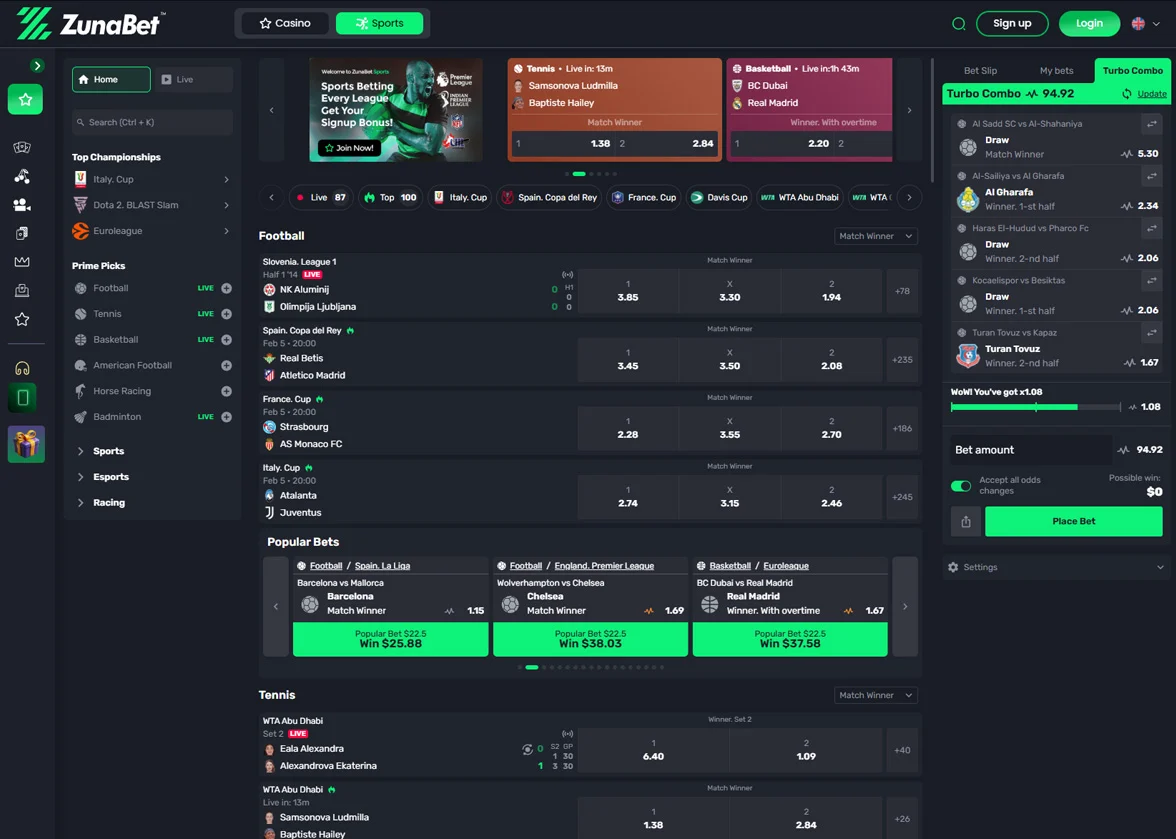

BetMGM Alternative Searches Are Climbing Steadily and ZunaBet Is Leading the Conversation

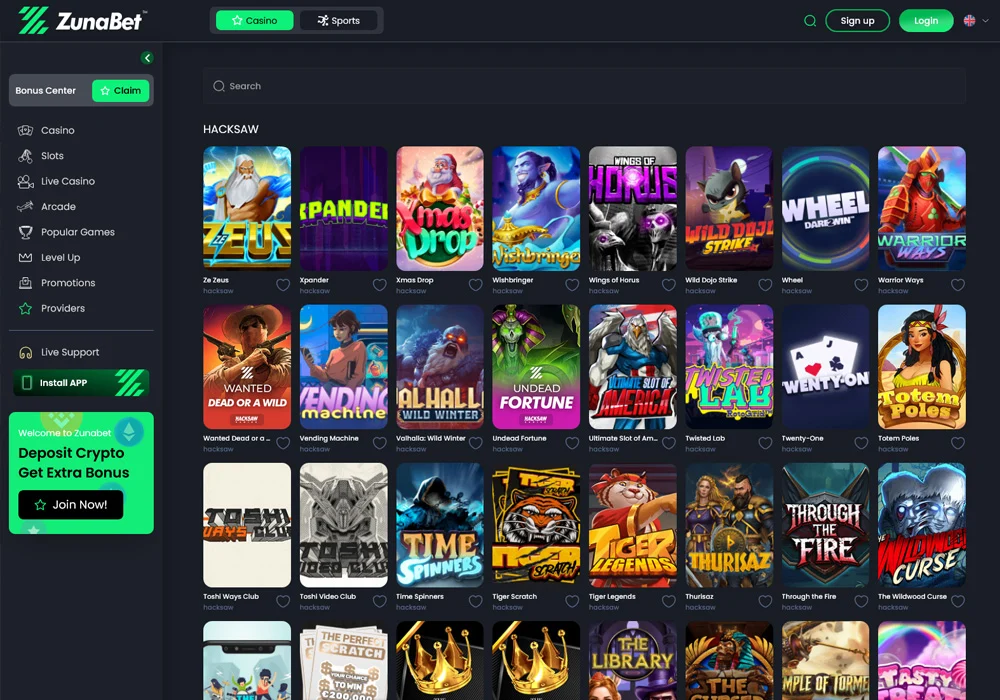

The online gambling industry is watching its audience evolve in real time. Players who once gravitated toward the biggest brand in the room and stayed without questioning the choice are behaving differently now. They compare. They research. They ask whether the platform they are using is genuinely the best available option or simply the most visible one. BetMGM, carrying one of the most storied names in casino history, has become a frequent reference point in that comparison process. The platform remains a major force in the market. But the steady growth in searches for BetMGM alternatives reveals that a meaningful and expanding portion of players believes the market now offers something that the traditional giants were not built to provide. The platform appearing most consistently in those searches is ZunaBet — a crypto-native casino and sportsbook that launched in 2026 and immediately demonstrated what online gambling looks like when it is designed for the audience that is arriving rather than the audience that came before.

BetMGM: Legacy Power in a Digital World

BetMGM operates with advantages that most competitors cannot replicate. The MGM brand has been a pillar of casino culture for generations. BetMGM translates that legacy into the digital space through a joint venture backed by MGM Resorts International and Entain, combining physical casino expertise with online gambling technology. The platform holds licenses across a substantial number of US states and ranks among the most prominent online gambling operators in the American market.

The product reflects the investment behind it. The casino section features a curated collection of slots, table games, and live dealer rooms from reputable providers. The sportsbook delivers broad coverage of NFL, NBA, MLB, NHL, college athletics, international football, tennis, golf, motorsports, and combat sports. The mobile app is well engineered and benefits from regular updates. BetMGM also connects its online loyalty program to the wider MGM Rewards ecosystem, allowing players to accumulate points redeemable for hotel stays, dining experiences, entertainment, and other perks at physical MGM properties across the country.

Payment infrastructure follows the established model. Bank accounts, debit and credit cards, PayPal, and similar traditional services manage the flow of funds. These methods provide the kind of universal accessibility that a mainstream-oriented platform requires to minimize barriers for the widest possible audience.

BetMGM delivers a polished and professional experience within the boundaries it was designed to operate in. The issue driving alternative searches is not product failure but product scope. The game library is focused but modest compared to what newer global platforms now deliver at launch. The payment system processes transactions through intermediary networks that impose delays and fees inherent to traditional banking. And while the connection to physical MGM properties is a genuine differentiator for a specific audience, it holds limited relevance for the growing population of players whose gambling activity is entirely digital and whose financial lives increasingly run on cryptocurrency. BetMGM was built to bring the MGM experience online. The market is now asking for something that goes beyond translating a legacy experience into digital form.

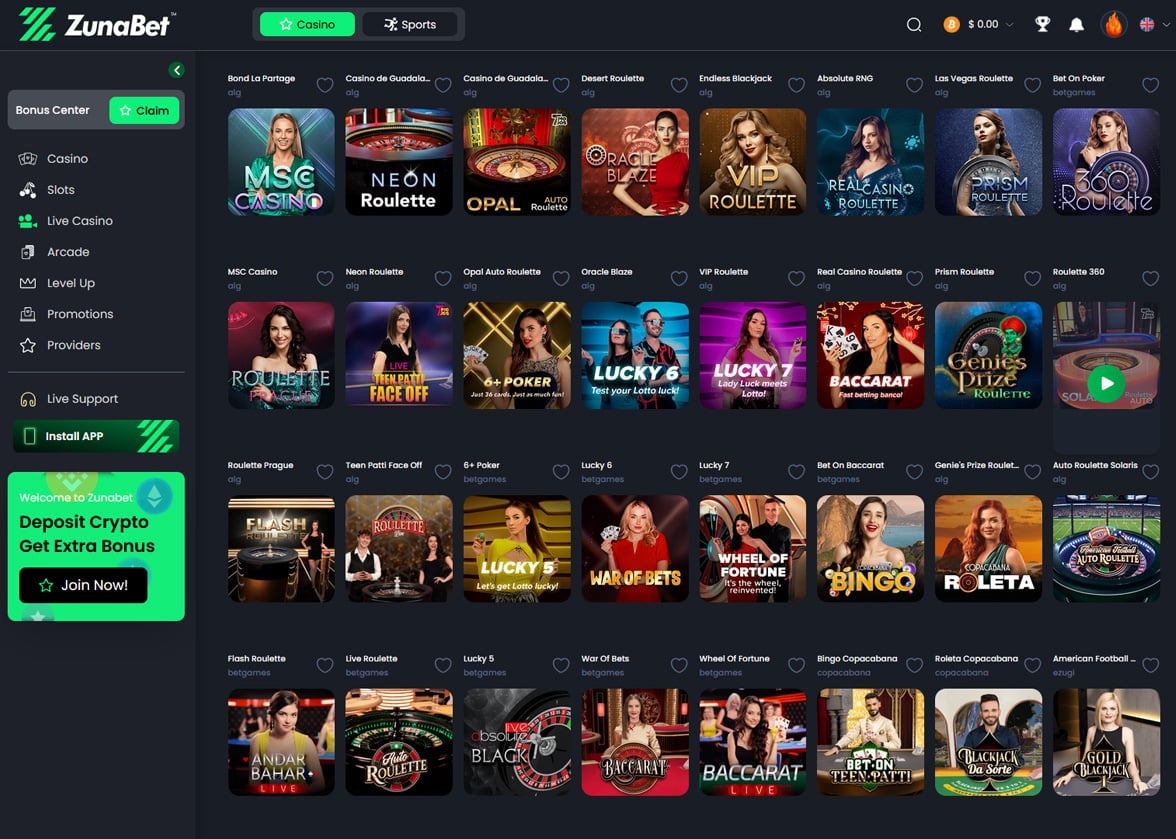

ZunaBet: Built From Scratch for a Digital-First Audience

ZunaBet was not designed to digitize an existing brand. It was designed to build something new for an audience that traditional operators were never equipped to serve. Launched in 2026 by Strathvale Group Ltd, the platform is guided by a management team with more than 20 years of combined gambling industry experience. It operates under an Anjouan gaming license and is registered in Belize. Cryptocurrency serves as the foundational infrastructure — the core architectural principle from which every feature and system extends.

The game library delivers the first and most powerful statement of intent. ZunaBet launched with 11,294 games from 63 separate providers. That volume exceeds what many established operators have built across years or even decades of continuous operation. The provider roster is headlined by studios that set the quality standard across the industry — Pragmatic Play, Evolution, Hacksaw Gaming, Yggdrasil, and BGaming — supported by dozens of additional developers whose collective output ensures comprehensive coverage across every game category and style.

Slots constitute the largest portion of the catalog, as they do at every online casino worldwide. ZunaBet’s strength lies in the depth beyond slots. RNG table games span blackjack, roulette, baccarat, poker across multiple variants, and specialty titles that add unexpected range to the non-slot categories. The live dealer section features high-definition real-time streaming from premium production studios, creating immersive interactive experiences that capture the atmosphere of a physical casino within a digital interface. With 63 providers contributing distinct design philosophies and mechanics, the catalog offers the kind of genuine diversity that sustains a sense of discovery across months of regular play rather than weeks.

That sustained discovery changes how players relate to the platform. On sites with smaller libraries, content fatigue arrives quickly and drives players to look elsewhere. On ZunaBet, the sheer volume and variety of available content means that months of regular activity leave the majority of the catalog still unexplored. The experience of finding something genuinely new does not fade after the first few sessions. It remains a constant feature of the platform, creating organic retention that no promotional campaign can substitute for.

The sportsbook functions as a fully developed product alongside the casino, sharing the same player account and wallet. Traditional sports coverage extends across football, basketball, tennis, NHL, combat sports, and virtual sports. Esports receives dedicated comprehensive treatment with complete betting markets on CS2, Dota 2, League of Legends, and Valorant. This commitment reflects a strategic understanding of the modern gambling audience. Competitive gaming draws hundreds of millions of viewers globally, and the overlap between esports fans and crypto-native users is substantial. ZunaBet built for that intersection from day one, giving it immediate credibility with a demographic that traditional operators have repeatedly underestimated.

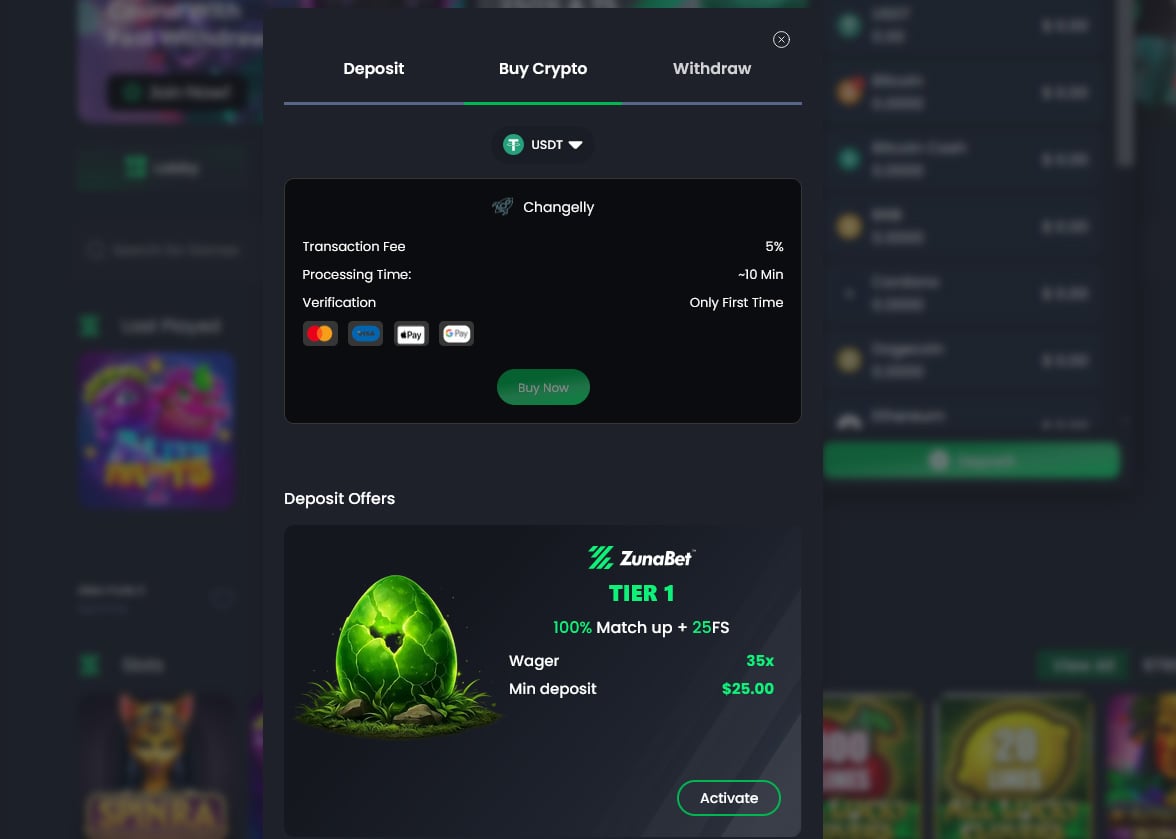

Over 20 cryptocurrencies power the payment infrastructure — Bitcoin, Ethereum, USDT across multiple blockchain networks, Solana, Dogecoin, Cardano, XRP, and additional options. Platform processing fees do not exist. Withdrawals settle on blockchain networks that operate without interruption, returning funds to player wallets in minutes regardless of when the request is submitted. The crypto-only architecture means no traditional fiat system operates beneath the surface to introduce delays or inconsistency. Every transaction follows the same seamless path.

New players access a welcome package worth up to $5,000 plus 75 free spins over three deposits. First deposit receives a 100% match up to $2,000 with 25 free spins. Second deposit earns a 50% match up to $1,500 with 25 spins. Third deposit completes the offer with a 100% match up to $1,500 and 25 final spins. The three-deposit structure sustains engagement across multiple sessions rather than concentrating all value at the point of entry.

The platform runs on HTML5 with a dark-themed responsive interface and fast performance across every device type. Native apps cover iOS, Android, Windows, and MacOS. Live chat support is available at every hour of every day.

Why Crypto Infrastructure Outperforms Traditional Payment Systems

The payment gap between crypto-native and traditional platforms is not a matter of minor convenience. It is a structural difference that produces measurably different outcomes across every transaction a player makes.

Traditional platforms route financial transactions through layered networks of banks, card companies, and payment processors. Each layer adds processing time. Many add cost. Withdrawals are particularly affected — platform review stages, banking processing queues, business-day limitations, and weekend and holiday pauses stack on top of each other to create timelines stretching from one to five business days. Fees charged at various points along the chain erode the total reaching the player.

On ZunaBet, every transaction is a single blockchain event. Player initiates. Network confirms. Funds arrive. Minutes from start to finish. No platform fees. No institutional queues. No calendar dependencies. The experience works identically at any hour because blockchain networks never stop operating.

Over a year of regular use, the accumulated savings in time and money are significant. These savings are not promotional. They are the permanent product of a more efficient infrastructure applied uniformly to every transaction. A player on ZunaBet does not need to strategize around withdrawal timing or payment method selection. The system delivers speed and cost efficiency by default because it was built to do nothing else.

ZunaBet maintains this consistency through pure crypto architecture. No traditional payment layer runs alongside it. No hybrid system creates variability. One foundation produces one consistently excellent outcome for every player on every transaction.

Physical Rewards vs Digital Progression

BetMGM’s loyalty program holds a distinctive advantage through its integration with MGM Rewards. Players earn points that translate to tangible benefits at physical MGM properties — hotel rooms, restaurant reservations, show tickets, and resort experiences. For players who visit MGM destinations, this bridge between digital gambling and physical luxury creates genuine added value.

For the expanding segment of players whose gambling lives exist entirely in the digital realm, however, those physical perks carry limited weight. This is the space where ZunaBet’s loyalty approach resonates most powerfully.

The dragon evolution system structures progression across six tiers — Squire at 1% rakeback, Warden at 2%, Champion at 4%, Divine at 5%, Knight at 10%, and Ultimate at 20%. Each tier delivers escalating digital rewards — free spins building to 1,000 at the highest level, VIP club access, and double wheel spins. A dragon mascot called Zuno evolves visually as the player advances through each stage, creating a personal progression narrative.

The design draws directly from video game mechanics. Defined levels with clear requirements. Meaningfully escalating rewards at each stage. Visual evolution that makes progress observable and personal. Achievement dynamics that give milestones emotional weight. These principles have sustained engagement in gaming for decades, and they connect powerfully with the demographic most likely to use a crypto-native gambling platform — players raised on progression systems, achievement unlocks, and visual feedback loops.

ZunaBet players interact with their loyalty tier actively rather than passively. They track progress. They strategize around milestones. They feel authentic accomplishment when they advance. That behavioral pattern represents a fundamentally different relationship with loyalty than what points-based systems produce, even those connected to physical resort experiences. For the digital-first audience, progression that lives within the platform they use daily carries more personal resonance than perks they may never redeem at a property they may never visit.

What the Search Data Means

The consistent growth in BetMGM alternative searches tells a straightforward story about a market in transition. BetMGM will continue to hold significant ground. The MGM brand, regulatory licenses, Entain partnership, physical property integration, and financial resources provide a foundation that ensures long-term relevance. The platform serves its audience well and will keep doing so.

But the audience itself is diversifying beyond what BetMGM was constructed to address. The fastest-growing player segment wants crypto-native payments that are instant and free. It wants game catalogs so vast that boredom becomes structurally impossible. It wants esports treated as a serious betting vertical. It wants loyalty programs designed for digital engagement rather than physical redemption. It wants platforms built for the world it currently inhabits.

ZunaBet was engineered from a blank page to satisfy every one of those demands. Its game library ranks among the deepest anywhere. Its payment infrastructure delivers speed and cost efficiency beyond what traditional systems can approach. Its esports offering serves a massive audience with genuine commitment. And its loyalty system turned the industry’s most neglected convention into something players actively enjoy. That is why ZunaBet keeps appearing when players search for something beyond BetMGM. They are looking for what online gambling should be for a new generation, and ZunaBet already built it.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

The American Bankers Association (ABA) has asked US government agencies responsible for regulations related to a stablecoin bill for more time to comment, potentially delaying implementation by as much as two months.

In a Tuesday letter to the US Treasury Department, Federal Deposit Insurance Corporation (FDIC), Financial Crimes Enforcement Network (FinCEN) and Treasury’s Office of Foreign Assets Control, the ABA requested the agencies extend the deadline for public comment on rules for the GENIUS Act, a stablecoin payments bill signed into law in July 2025.

The banking group asked for 60 additional days to comment on rulemaking after the issuance of a final rule by the Office of the Comptroller of the Currency (OCC), saying the rules by the other agencies were “substantially dependent” on the outcome of the OCC’s.

“The FDIC has stated explicitly in its [notice] that it ‘has endeavored, in many areas, to align this proposed rule with the OCC’s proposed rule, to the extent relevant,’ and specifically invites comment ‘on the extent to which the primary Federal payment stablecoin regulators should further align in their final rules to promote consistency of regulations applicable to all PPSIs subject to the GENIUS Act,’” said the letter. “Meaningful comment on that question is impossible without knowing the final content of the OCC’s rule.”

Since being signed into law by US President Donald Trump in July, implementation of the stablecoin bill has moved to agencies like the FDIC and Treasury, which need to finalize regulations. According to the law, the legislation can be enacted 120 days after final regulations are issued or 18 months after enactment, whichever comes first.

Related: UK cracks down on illegal peer-to-peer crypto trading in nationwide raids

In addition to its request related to the GENIUS Act, the ABA is a party to policy debates concerning a crypto market structure bill, which could potentially affect the legal status of stablecoin yield. Last week, the association challenged a report from the White House that claimed banning stablecoin yields would only have a negligible impact on banks.

Stablecoin yield debate continues as Senate considers CLARITY Act

As of Wednesday, lawmakers in the US Senate had not announced a deal which could allow a separate crypto market structure bill, called the CLARITY Act when it passed the US House of Representatives in July, to move forward.

North Carolina Senator Thom Tillis reportedly said on Monday that he recommended Senate Banking Committee leader Tim Scott schedule a markup on the bill in May, potentially pushing back a vote in the full chamber.

Magazine: How to fix insider trading on platforms like Polymarket and Kalshi

Rekomendasyon: Live casino siteleri deneyimlerinize canlı ve etkileyici bir katman ekleyin. En güvenilir slot casino siteleri arasında seçebileceğiniz yeni casino siteleri ve casino bahis siteleri arasında seçim yapın.

Slot Casino Siteleri: En iyi slot siteleri, çeşitli oyunlar ve yüksek kazanç olasılıkları sunar. Güvenilir slot siteleri, güvenli ödeme sistemleri ve profesyonel müşteri hizmetleri ile öne çıkmaktadır.

Canlı Casino Siteleri: Canlı casino siteleri, canlı croupierlerle oynanabilecek reallikli oyunlar sunar. Bu siteler, kullanıcıların gerçek zamanlı bir deneyim yaşamasına olanak tanır ve profesyonel bir atmosfer sunar.

Yeni Casino Siteleri: Yeni casino siteleri, en güncel ve popüler oyunlarla kullanıcıları etkiler. Bu siteler, kullanıcı dostu arayüzler ve geniş oyun sunumları ile öne çıkmaktadır.

Casino Bahis Siteleri: Casino bahis siteleri, çeşitli bahis oyunları ve yüksek kazanç olasılıkları ile bilinen slot oyunları dışında, farklı bahis seçenekleri sunar. Güvenilir casino bahis siteleri, güvenli ve hızlı ödeme sistemleri ile öne çıkmaktadır.

Seçiminiz: En iyi slot siteleri ve canlı casino siteleri arasında seçim yaparken, güvenilirlik, güvenli ödeme sistemleri ve profesyonel müşteri hizmetleri gibi faktörleri göz önünde bulundurun. Yeni ve casino bahis siteleri de, kullanıcı dostu arayüzler ve geniş oyun sunumlarıyla ilgi çekicidir.

En İyi Slot Casino Sitelerini Keşfedin

2026 yılında güvenilir casino siteleri arasında “Yeni Casino Siteleri” adlı platforma göz atmanızı öneririm. Bu platform, slot casino siteleri ve casino bahis siteleri arasında en iyi seçenekleri sizin için sıralar. Platformda deneme bonusu veren casino siteleri de bulunuyor, bu sayede deneyimden memnuniyet duyabilirsiniz. Ayrıca, en güvenilir casino siteleri arasında yer alan sitelerin listesini bulabilirsiniz. Bu siteler, güvenilirlik ve güvenilir ödeme sistemleriyle bilinir, bu nedenle kaynaklarınızı güvenle kullanabilirsiniz.

En iyi slot siteleri arasında “Güvenilir Casino Siteleri” adlı bir platform da yer alıyor. Bu platform, slot oyunları için en iyi siteleri ve en yüksek kazançları sunuyor. Platformda bulunan siteler, kullanıcı dostu arayüzler, çeşitli oyun seçenekleri ve profesyonel müşteri hizmetleri ile öne çıkmaktadır. Ayrıca, bu sitelerde güvenilirlik ve güvenliği en üst düzeyde ön planda tutuyorlar, bu nedenle kaynaklarınızı güvenle kullanabilirsiniz. En iyi slot sitelerini keşfetmek için bu platformu kullanmanızı öneririm.

En İyi Güvenilir Kasino Sitelerinin Seçimi

En güvenilir slot casino siteleri arasında Deneme Bonusu Veren Casino Siteleri yer alıyor. Bu siteler, yeni kullanıcıların deneme oyunları ile tanışmasını sağlar, böylece riski azaltan bir deneyim sunarlar. Örneğin, Slot Casino Siteleri arasında Evraç Casino ve Fortuna Casino bu konuda öne çıkmaktadır. Bu siteler, kullanıcıların güvenli bir ortamda oynayabilecekleri çeşitli slot oyunlarını sunarlar.

Canlı Casino Siteleri de güvenilirliği açısından önemli bir rol oynar. Bu siteler, canlı cüzzamlı dealerlerle oynanabilecek oyunları sunar. Örneğin, Live Casino House ve LeoVegas Casino bu tür siteler arasında öne çıkmaktadır. Bu siteler, kullanıcıların gerçek zamanlı bir deneyim yaşayabilecekleri güvenli bir ortam sağlarlar.

Yeni Casino Siteleri de güvenilirliği açısından dikkat etmeniz gereken bir nokta. Bu siteler, güvenilirlik açısından daha yeni olup, belki de daha az bilinen markalar olabilir. Ancak, bazı siteler, güvenilirliği ve güvenliğini sağlamak için çeşitli güvenlik standartlarını takip ederler. Örneğin, Novomatic Casino ve NetEnt Casino bu tür siteler arasında güvenilirliği açısından öne çıkmaktadır.

Casino Bahis Siteleri de güvenilirliği açısından dikkat etmeniz gereken bir nokta. Bu siteler, çeşitli bahis oyunları sunarlar. Örneğin, Unibet Casino ve Bet365 Casino bu tür siteler arasında güvenilirliği açısından öne çıkmaktadır. Bu siteler, kullanıcıların güvenli bir ortamda oynayabilecekleri çeşitli bahis oyunlarını sunarlar.

Güvenilir Casino Siteleri arasında Unibet Casino ve LeoVegas Casino yer alıyor. Bu siteler, kullanıcıların güvenli bir ortamda oynayabilecekleri çeşitli slot ve bahis oyunlarını sunarlar. Ayrıca, bu siteler, kullanıcıların para yatırma ve çekme işlemlerini kolaylaştıran çeşitli ödeme yöntemlerini desteklerler.

En Güvenilir Casino Siteleri arasında Evraç Casino ve Fortuna Casino yer alıyor. Bu siteler, kullanıcıların güvenli bir ortamda oynayabilecekleri çeşitli slot oyunlarını sunarlar. Ayrıca, bu siteler, kullanıcıların güvenli bir ortamda oynayabilecekleri canlı cüzzamlı dealerlerle oynanabilecek oyunları sunarlar. Bu siteler, kullanıcıların güvenliği ve güvenilirliği açısından öne çıkmaktadır.

Stablecoin issuer argues Aave’s interest rate curve is failing to clear the $1.89B pool after four days at full utilization.

Circle has proposed an emergency overhaul of the interest rate parameters on Aave V3 Ethereum Core’s USDC pool, which has been pinned at 99.87% utilization for four days in the wake of the April 18 KelpDAO exploit.

In a governance post published Tuesday, Circle Chief Economist Gordon Liao argued Aave’s current interest rate mechanism is failing to clear the market. The pool holds $1.89 billion in supply against $1.89 billion in borrows, with less than $3 million in available liquidity. Borrow rates are flat at the post-kink ceiling of roughly 14%, and the pool has contracted about $60 million in the last 24 hours as repayments are matched dollar-for-dollar by queued withdrawals.

Liao’s proposal would raise the pool’s Slope 2 parameter for USDC deposits interest rate, from roughly 10% to 40% immediately, via a Risk Steward action. That would be followed by governance ratification of a 50% target within five to seven days.

Optimal utilization would fall from 92% to 87% on an interim basis and 85% on ratification. Under the target parameters, the maximum supply rate at 100% utilization would climb from roughly 12.6% to 48.2%.

Liao’s diagnosis is that current borrowers are using USDC borrowing as a queue-bypass mechanism to exit trapped positions and are insensitive to rates at current levels. The active lever, he argued, is supply attraction: yields in the 40–50% range should pull USDC from allocators within hours, restoring healthy utilization.

The proposal also recommends pausing Aave’s Slope 2 Risk Oracle for USDC, citing its documented underperformance during a February WETH spike and the April 6 offboarding of its maintainer, Chaos Labs.

Circle’s intervention is unusual: the stablecoin issuer is formally telling Aave that the market for its asset is broken.

Elon Musk’s Tesla’s (TSLA) bitcoin holdings were unchanged in the first quarter of 2026, with the company continuing to hold its 11,509 BTC stockpile.

The company booked an after-tax impairment loss of $173 million on its digital asset holdings, according to its first quarter earnings report.

The value of that stash declined as bitcoin fell from around $90,000 at the start of the year to roughly $68,000 by the end of March.

Tesla reported better-than-expected earnings but missed on revenue. For the first quarter, the firm reported revenue of $22.39 billion, slightly below than analyst estimates of $22.71 billion. Earnings per share came in at $0.41, higher than consensus forecast of $0.37.

TSLA stock was trading 4% higher in after-hours trading.

Tesla’s bitcoin journey

Tesla initially bought bitcoin in February 2021, acquiring 43,200 BTC for roughly $1.5 billion. About a month later, the company sold around 4,320 BTC, roughly 10% of its position, to test market liquidity.

By July 2022, amid the bear market, Tesla had cut its position to 9,720 BTC. A small increase in January 2025 brought holdings to 11,509 BTC, where they have remained since.

Oracle network Pyth Network has been selected as the resolution data source for Kalshi’s expansion into commodities markets, underscoring the growing focus on reliable pricing infrastructure in event-based trading.

Kalshi said on Wednesday that Pyth will supply real-time pricing data for its newly launched commodities hub, which debuted in April. The data will be used to determine how event contracts tied to commodity prices are settled.

The move reflects a broader push among prediction market platforms to strengthen backend infrastructure as they expand into more complex asset classes. Accurate, tamper-resistant data feeds are critical for ensuring fair and transparent contract resolution, particularly in markets tied to real-world financial benchmarks.

Kalshi’s commodities hub allows users to trade event contracts linked to physical assets, including gold, silver, oil, copper and key agricultural products. Pyth’s price feeds will serve as the source of truth for determining contract outcomes.

Pyth has also been selected by rival prediction market Polymarket to provide price feeds for equities and commodities.

Pyth Network is a decentralized oracle that delivers real-time market data to blockchain applications. As Cointelegraph recently reported, Pyth has also recently deployed infrastructure that enables institutions to publish and monetize proprietary data across multiple networks.

Related: Kalshi mulls crypto expansion with perpetual futures launch: Report

Kalshi’s federal status faces state pushback

Kalshi is rolling out these changes as it seeks to bring more structure to the fast-growing prediction market sector. The company is regulated by the US Commodity Futures Trading Commission as a designated contract market, meaning it is approved to offer trading in derivatives contracts under federal oversight, similar to a traditional exchange.

State regulators have pushed back on Kalshi and other prediction platforms, arguing that some contracts resemble unlicensed gambling or fall outside existing derivatives rules.

However, the US Department of Justice and the CFTC recently asked a federal court to block Arizona from enforcing state gambling laws against Kalshi’s contracts, signaling support for federal jurisdiction in this area.

The dispute comes as prediction market activity has grown sharply over the past two years, drawing in new entrants from both traditional finance and the crypto sector.

Related: After Kalshi appeal, prediction markets fight could head to US Supreme Court

Two CIA officers were killed in a car crash in the Mexican state of Chihuahua on April 20 while returning from a counternarcotics operation to destroy a clandestine drug lab, igniting a sovereignty dispute between Washington and Mexico City.

Summary

- Two CIA officers and two Mexican law enforcement agents died when their vehicle crashed in rugged mountain terrain in Chihuahua state.

- The crash occurred after an operation to dismantle what authorities described as one of the largest clandestine drug labs found in Mexico.

- Mexican President Claudia Sheinbaum has launched an investigation into whether US agents violated Mexican law by operating without federal authorization.

Two CIA officers were killed alongside two Mexican law enforcement officials in a vehicle crash in Mexico’s Chihuahua state, following an operation targeting a large clandestine drug processing lab, multiple sources briefed on the matter confirmed to CBS News and CNN. The CIA declined to comment on the identities of the officers. Their truck crashed in rugged mountain terrain connecting Chihuahua to Sinaloa state while traveling in the middle of the night after the operation.

CIA Agents Killed in Mexico as Sovereignty Row Erupts

The crash occurred following what Chihuahua Attorney General César Jáuregui described as an operation to dismantle one of the largest clandestine chemical drug production sites ever found in the country. CBS News reported that the vehicle appears to have skidded on a mountain road and fallen into a ravine, causing it to explode. Mexican President Claudia Sheinbaum confirmed on April 21 that federal prosecutors have launched an investigation to determine whether any laws were violated, specifically whether US agents participated in operations on Mexican territory without authorization from the federal government.

Mexico Questions Legality of US Presence

Sheinbaum was pointed in her public response, stating that any joint operations between local governments and the US without federal authorization would constitute a violation of Mexican law and of the constitution. CNN reported that the CIA has significantly expanded its operations inside Mexico under Director John Ratcliffe, including covertly flying MQ-9 Reaper drones over Mexican territory to monitor cartel activity, and has undertaken a review of its authorities to use lethal force against drug cartels. Sheinbaum has previously insisted that there are “no joint operations on land or in the air” in Mexico, describing US involvement as limited to information sharing within an established legal framework.

The Broader Stakes for US-Mexico Relations

The deaths come at a highly sensitive moment in US-Mexico relations. The Trump administration has designated several Mexican cartels as foreign terrorist organizations, a classification that Mexico’s government has pushed back against strongly, viewing it as a potential pretext for direct US military action on Mexican soil. The incident adds fresh pressure to a bilateral relationship already strained by tariffs, immigration enforcement, and the extent of American intelligence activity inside Mexico. How both governments respond to the investigation’s findings is likely to shape the trajectory of counternarcotics cooperation between the two countries for the near term.

The CIA has not confirmed the identities of the two officers or commented on the nature of their role in the operation that preceded the crash.

AI Integration, Growth in Subnets, and Decentralized Intelligence’s Future

NFL fans react to Justin Fields’ comments about Patrick Mahomes after joining Chiefs

Android finally gets a fitting answer to the iPad mini, and it looks stunning

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

US brings back mandatory military draft registration

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Theodora Dress

-

Sports6 days ago

Sports6 days agoNWFL Suspends Two Players Over Post-Match Clash in Ado-Ekiti

-

Politics5 days ago

Politics5 days agoPalestine barred from entering Canada for FIFA Congress

-

Entertainment3 days ago

NBA Analyst Charles Barkley Chimes in on Ice Spice McDonald’s Fiasco

-

Business3 days ago

Business3 days agoPowerball Result April 18, 2026: No Jackpot Winner in Powerball Draw: $75 Million Rolls Over

-

Tech4 days ago

Tech4 days agoAuto Enthusiast Scores Running Tesla Model 3 for Two Grand and Turns It Into Bare-Bones Go-Kart

-

Politics3 days ago

Politics3 days agoZack Polanski demands ‘council homes not luxury flats for foreign investors’

-

Crypto World5 days ago

Crypto World5 days agoRussia Pushes Bill to Criminalize Unregistered Crypto Services

-

Politics2 days ago

Politics2 days agoGary Stevenson delivers timely reminder to register to vote as deadline TODAY

-

Tech7 days ago

Tech7 days ago‘Avatar: Aang, The Last Airbender’ Leaked Online. Some Fans Say Paramount Deserves the Fallout

-

Business6 days ago

Business6 days agoCreo Medical agree sale of its manufacturing operation

-

Business12 hours ago

Business12 hours agoRolls-Royce Voted UK’s Most Iconic Trade Mark as IPO Register Hits 150

-

Politics3 hours ago

Politics3 hours agoDisabled people challenge government SEND proposals over segregation concerns

-

Crypto World5 days ago

Crypto World5 days agoRussia Introduces Bill To Criminalize Unregistered Crypto Services

-

Politics3 hours ago

Politics3 hours agoMaking troops accountable for war crimes threatens US alliance, ex-SAS colonel warns

-

Politics4 hours ago

Politics4 hours agoStarmer handler McSweeney to be dragged from shadows by Foreign Affairs Committee

-

Politics4 hours ago

Politics4 hours agoZack Polanski responds to home secretary’s taser threat

-

Politics5 hours ago

Wings Over Scotland | How To Get Away With Crimes

-

Crypto World4 days ago

Crypto World4 days agoKelp DAO rsETH Bridge Hack Drains $292M as DeFi Losses Top $600M in Two Weeks

-

Tech7 days ago

Tech7 days agoFord EV and tech chief leaving automaker

You must be logged in to post a comment Login