Crypto World

BeInCrypto Institutional Research: 8 Neobanks Setting Standards for Digital Asset Accessability

Digital-asset neobanking has moved beyond basic crypto access. The category now covers firms combining bank-account-style services — checking, direct deposit, debit, savings, and banking partnerships or charters — with native crypto products built into the primary financial app.

Best Digital Assets Neobank is a category within the BeInCrypto Institutional 100, under Pillar 1: Retail to Crypto Bridge. The 8 firms below are listed alphabetically and are not ranked. A shortlist will be named in May 2026, with the winner announced at Proof of Talk in Paris on June 2–3, 2026.

Key Facts

- Long list: 8 firms across bank-chartered neobanks and BaaS, EMI, or VASP-licensed fintechs with crypto integrated into the primary banking app

- Initial pool: 18 firms screened; 8 advanced to the long list, with 3 outreach candidates retained

- Order: Listed alphabetically, not ranked

- Scoring: 30% quantitative data · 50% Expert Council · 20% disclosed company data

- Criteria assessed: User base, crypto user count, product depth, regulatory licensure, payments and card integration, geographic reach, financial performance, innovation

- Data sources: OCC, FCA, BaFin, DNB, ACPR, MAS, CSSF, NYDFS, BACEN, CNBV, GFSC, MiCA-CASP, SEC EDGAR, audited filings, reserve attestations, on-chain data, PitchBook, Crunchbase, Tracxn

| Firm | HQ | Reach | Top Licensure / Charter | Representative Work |

|---|---|---|---|---|

| Bunq | Amsterdam, Netherlands | 17M+ users across 30+ EEA countries 2024 net profit of €85.3M, up 65% year over year |

Full Dutch banking licence from De Nederlandsche Bank EU passporting, MiCA-compliant; UK banking and US broker-dealer licences applied for in 2025–26 |

Launched Bunq Crypto through Kraken partnership in Apr 2025 Offers 300+ cryptocurrencies inside a licensed-bank environment; first-year crypto trades passed €100M |

| Cash App | Oakland, USA Block, NYSE: XYZ |

59M monthly active users in Q4 2025 9.3M primary banking actives; $316B total customer inflows in 2025 |

Banking via Sutton Bank partnership FDIC-insured checking, direct deposit, Cash Card, savings; NYDFS-licensed Bitcoin business |

Launched Proof of Reserves dashboard in Apr 2026 covering 8,883 BTC Bitkey self-custody wallet expanded; 5% Bitcoin Back rolled out across Cash App Card |

| KAST | Singapore / New York | 1M+ users across 170–190 countries About $5B annualized transaction volume; 150M+ merchants accepted globally |

Holds MSB Canada, MSB US, VASP EU, TCSP Hong Kong Uses regulated partners including Bridge, Tazapay, Reap, Fireblocks, BitGo, and Privy |

Closed $80M Series A in Mar 2026 at $600M valuation KAST Business beta launched in May 2026; security stack includes Sardine, Elliptic, ChainPatrol, Vanta, and Scanner.dev |

| Mercado Pago | Buenos Aires, Argentina Mercado Libre, NASDAQ: MELI |

100M+ users across Brazil, Mexico, Argentina, Colombia, Chile, Uruguay, and Peru via MELI ecosystem | Jurisdiction-specific fintech and payments licences across Latin America VASP authorisations for MELI Cripto in operating markets |

MELI Cripto expanded to 17 tokens by May 2026 Trading fee cut to 0.2%; Meli Dólar stablecoin available across Brazil, Mexico, and Chile |

| Nomad | São Paulo, Brazil | 1M+ users Brazilian USD-account neobank focused on retail consumers and global investment access |

Brazilian fintech registration Banking issued through Brazilian and US partner banks; CVM-regulated investment platform component |

Pioneered XRP Ledger settlement for Brazilian USD payments Adapting to Brazil BCB Resolution 561, which restricts crypto and stablecoin use in cross-border eFX settlement |

| Nubank | São Paulo, Brazil Nu Holdings, NYSE: NU |

110M+ customers 7M+ NuCripto users; Berkshire Hathaway among significant shareholders |

Full Brazilian banking licence from BACEN OCC US national bank branch conditional approval; Mexico and Colombia authorisations |

Earn Crypto staking launched in Mar 2026 with Solana promotional yield NuCripto now supports 20+ assets; USDC partnership with Circle deepened crypto access |

| Revolut | London, UK | 70M+ customers across 40+ countries as of Jan 2026 2025 revenue of $6B and profit before tax of $2.3B |

Lithuanian EU banking licence UK banking licence, Mexican banking licence, MiCA-CASP authorisation, US charter in progress |

Reached $75B valuation in Nov 2025 capital raise Revolut X offers 230+ digital assets, staking, low-fee trading, and RWA token listings |

| SoFi | San Francisco, USA NASDAQ: SOFI |

12.6M members Q1 2026 revenue of $1.1B with $166.7M net income |

SoFi Bank N.A. OCC-regulated national bank and FDIC-insured depository institution |

Launched retail crypto trading in Nov 2025 Opened 239,509 crypto accounts in Q1 2026; SoFiUSD stablecoin launched in Dec 2025 |

About This List

The BeInCrypto Institutional 100 — Best Digital Assets Neobank (2026 Long List) identifies digital-first consumer and SMB banking platforms that combine bank-account-like services with substantial depth in digital assets.

Two structural models qualify: bank-chartered direct entities such as Bunq, Nubank, Revolut, and SoFi; and BaaS-partnered, EMI-licensed, or VASP-licensed crypto fintechs that integrate crypto into the primary banking app, such as Cash App, KAST, Mercado Pago, and Nomad.

The category does not include crypto exchanges with payment cards added on, self-custody spending cards without banking services, stablecoin issuers, institutional digital asset banks, defunct crypto banking platforms, or chartered neobanks without native crypto products.

Methodology

This category is evaluated under Track B of the BeInCrypto Institutional 100 methodology: 30% quantitative metrics, 50% Expert Council scoring, and 20% disclosed company data.

Assessment spans seven criteria: total user base and crypto user count; crypto and stablecoin product depth; regulatory licensure; payments and card integration; geographic footprint; financial performance and sustainability; and innovation during the award window.

Data was verified using regulatory registers, company filings, SEC EDGAR, audited financial statements, reserve attestations, Proof of Reserves disclosures, relevant on-chain data, private-market sources including PitchBook, Crunchbase, and Tracxn, and mainstream financial press.

The post BeInCrypto Institutional Research: 8 Neobanks Setting Standards for Digital Asset Accessability appeared first on BeInCrypto.

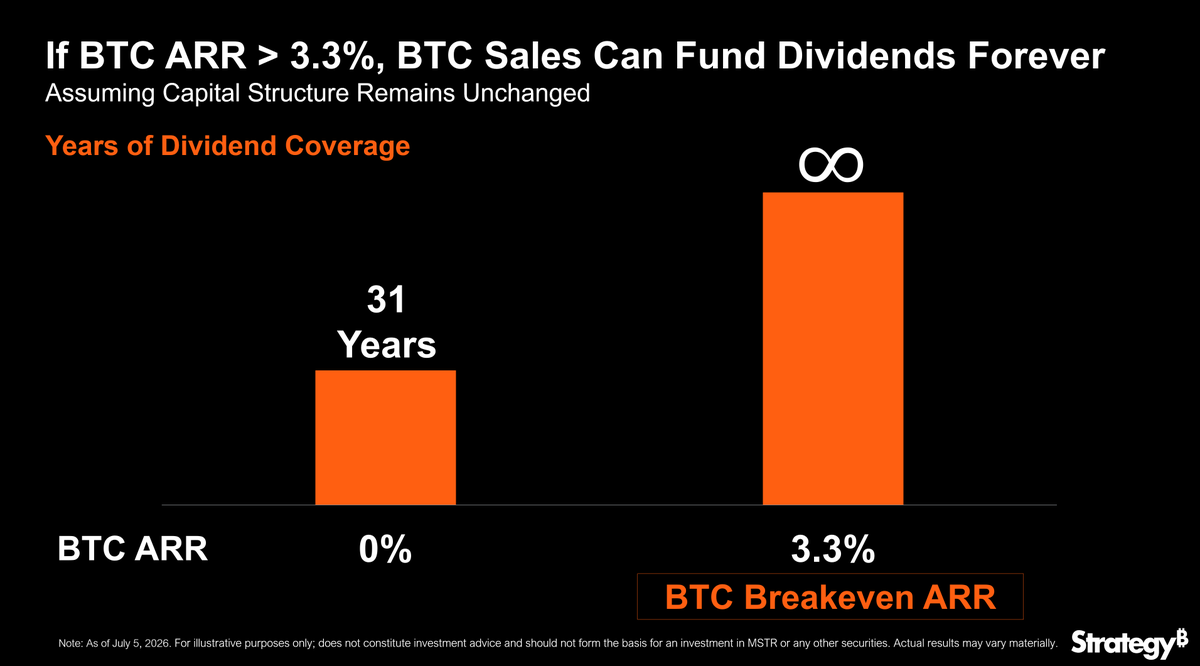

Michael Saylor spotlighted Strategy’s BTC Breakeven ARR on Tuesday, July 7. He argued Bitcoin (BTC) only needs 3.3% yearly growth to fund the firm’s preferred dividends from capital gains indefinitely.

The metric divides annual preferred dividend obligations, now roughly $1.76 billion by company figures, by the value of the corporate Bitcoin reserve. Saylor called it one of the most misunderstood numbers attached to Strategy (formerly MicroStrategy).

What BTC Breakeven ARR Means for MicroStrategy

Strategy reports holding 843,775 BTC, worth roughly $53.8 billion with Bitcoin trading near $63,603, and the stack keeps growing. The company disclosed 818,334 BTC in its May earnings release, meaning it added over 25,000 coins through a drawdown.

Saylor, the company’s founder and executive chairman, made the case in a Tuesday post on X (Twitter).

“One of the most misunderstood $MSTR metrics is BTC Breakeven ARR. If BTC appreciates faster than 3.3% over time, BTC capital gains can fund $STRC dividends indefinitely.”

A companion chart from Strategy illustrates the trade-off. At zero Bitcoin growth, the reserve plus a $2.55 billion cash buffer covers about 31 years of payments, per the company’s dashboard. The buffer alone funds roughly 17 months.

The pitch leans on a real track record. MicroStrategy has paid 23 consecutive preferred distributions totaling over $693 million since early 2025, per its Q1 release.

Critics Question the Bitcoin Dividend Math

The model assumes obligations stop compounding, and so far, they have not. Preferred dividends hit $229.5 million in the first quarter of 2026, up from $10.6 million a year earlier. Preferred equity outstanding has swelled past $13.5 billion.

Skeptics also doubt the funding side. JPMorgan recently warned that Strategy’s Bitcoin sales policy could add up to $1.25 billion in sell pressure. On-chain data already pointed to a new Bitcoin sale of 491 BTC on July 1, which was later confirmed to be 7x bigger.

Meanwhile, STRC paid an 11.5% annualized rate in May yet trades below its $100 par target. Preferred holders still price in risk despite the low breakeven hurdle.

Whether 3.3% proves a low bar depends on Bitcoin reclaiming its long-term trend, with the price down nearly 49% from its October peak.

However, coming payments may reveal how much of the burden falls on BTC sales rather than capital gains.

The post Michael Saylor Reveals the One Metric Keeping MicroStrategy’s Bitcoin Play Sustainable appeared first on BeInCrypto.

Bitcoin (BTC) circled $63,000 after Tuesday’s Wall Street open as chip companies led a dip in US stocks.

Key points:

- Bitcoin attempts to hold $63,000 after seeing its highest levels in two weeks.

- US stock markets see a correction on the day SpaceX joins the Nasdaq-100.

- Bollinger Bands creator John Bollinger continues to eye a long-term BTC price reversal.

BTC price comes off two-week highs as US stocks fall

Data from TradingView showed BTC price action cooling after a trip to $64,660 — its highest point since June 22.

BTC/USD one-day chart. Source: Cointelegraph/TradingView

BTC/USD surfed a comedown in US equities, with the S&P 500 and Nasdaq 100 down 0.6% and 2.1%, respectively, at the time of writing. Chip stocks led the sell-off, with Micron Technologies, whose earnings were highly anticipated last month, down over 9%.

Micron Technologies stock one-hour chart. Source: Cointelegraph/TradingView

At the same time, Tuesday was due to see SpaceX added to the Nasdaq 100 after its own stock turbulence in late June.

“This marks the fastest inclusion into the Nasdaq 100 in the index’s history,” trading resource The Kobeissi Letter noted in its latest commentary on X.

US spot Bitcoin ETF net flows (screenshot). Source: Farside Investors

Fresh from a second day of net inflows to the US spot Bitcoin exchange-traded funds (ETFs), BTC/USD managed to avoid a major comedown.

“Correlation to the Nasdaq just flipped to +0.72 from -0.87 in the matter of days last week,” trader Daan Crypto Trades reported on X.

“That’s the difference between trading like a complete hedge/inverse and trading like a high beta tech stock. Right now we’re back to the middle on the 4H timeframe.”

BTC/USDT futures (Binance) four-hour chart. Source: Daan Crypto Trades/X

Commentator Exitpump was conservative on low time frames, expecting a “rounding topping structure” and further downside next.

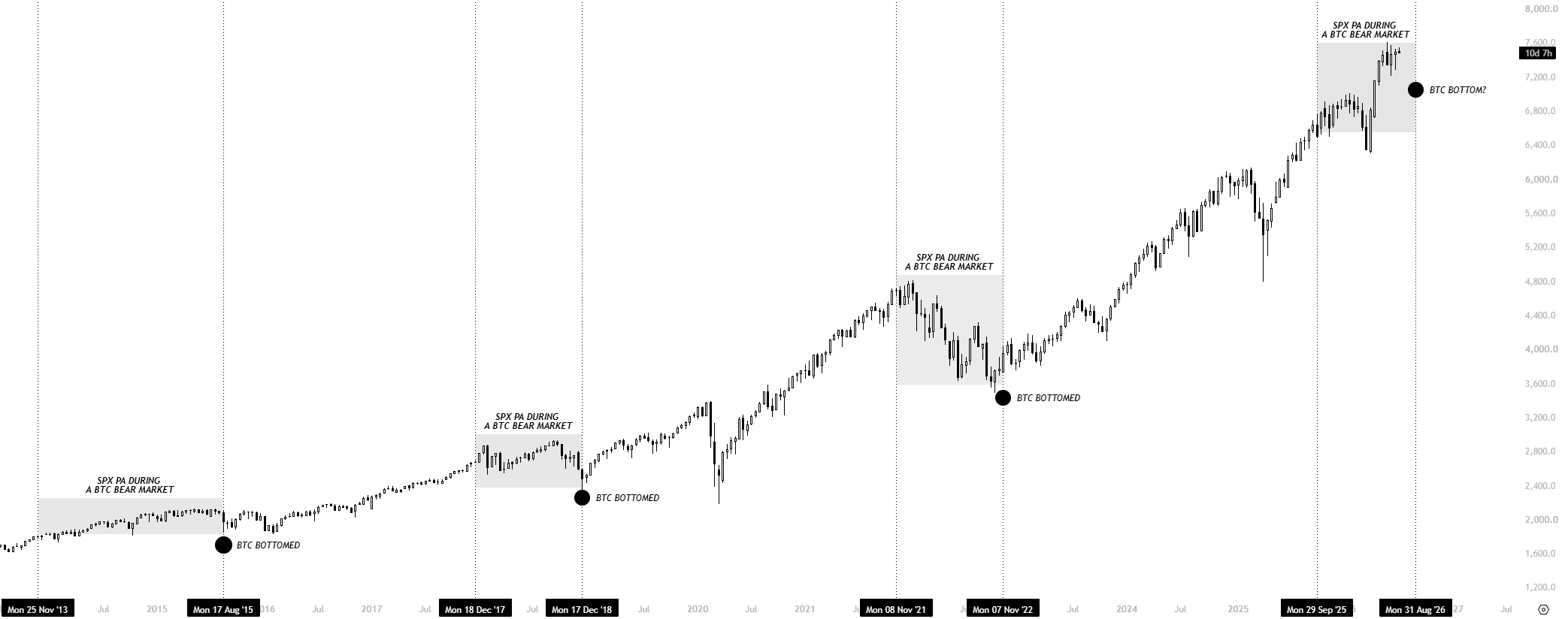

“The next correction on S&P should mark the true $BTC bottom according to history,” trader Killa suggested.

“Lets see if we repeat, 2015, 2018 & 2022.”

S&P 500 chart data. Source: Killa/X

Bollinger: “We are at a critical point”

In recent X discussions, meanwhile, John Bollinger, creator of the Bollinger Bands volatility indicator, had some more positive news for Bitcoin bulls.

Related: Bitcoin can fall below $58K if one of its ‘cleanest’ metrics copies history: Analysis

As Cointelegraph reported, Bollinger was eyeing a “W”-shaped reversal pattern currently in the process of confirmation on daily time frames.

Last week, he queried whether its latest iteration could end up canceling the BTC price downtrend altogether.

“We are at a critical point,” he added on Monday.

“In a bear market bullish setups break and in a bull market bearish setups break. So if this W pattern is successful I would see it as a confirmation of a change in trend.”

BTC/USD one-day chart with Bollinger Bands. Source: John Bollinger/X

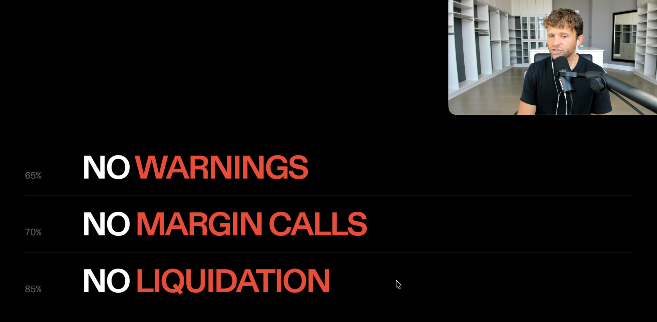

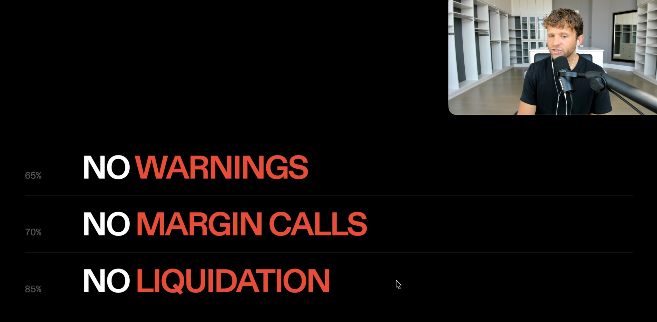

Bitcoin financial services platform Strike has launched a “volatility-proof” Bitcoin-backed loan that eliminates margin calls and forced liquidations amid the depths of a bear market, but only for those who can pay on time and handle a 14% interest rate.

In an announcement on Tuesday, Strike CEO Jack Mallers said the offering came in response to broad customer feedback on Strike’s first Bitcoin loan product, which launched in May 2025 and triggered many liquidations during a timeframe in which Bitcoin (BTC) dropped 54% from peak to trough.

“No margin calls. No price liquidations. No matter how far bitcoin falls, your bitcoin doesn’t move,” Strike CEO Jack Mallers said of the new Bitcoin loan product. The trade-off is an expensive interest rate, a shorter six-month loan term, and an obligation to pay on time to avoid liquidation, Mallers said.

Strike’s Jack Mallers is presenting the new Bitcoin-backed loan product. Source: Jack Mallers

The Bitcoin industry has spent the better part of a decade racing to build financial products that expand Bitcoin’s use case beyond a savings technology. A report in June from crypto lending platform Ledn, however, found that while 88% of surveyed crypto investors said they would consider a crypto-backed loan, only 14% use them.

Ledn said confidence in crypto-lending products and market volatility are among the main reasons for this 6-to-1 “crypto collateral gap” that has slowed adoption.

Volatility has been one of the biggest obstacles behind that push, with Bitcoin dropping 30% or more in 10 of the past 12 years, while also experiencing a 50% or more drawdown four times since 2014, Mallers noted.

Other crypto market participants offering Bitcoin-backed loans are Binance, Coinbase, Nexo and Xapo Bank.

Strike charges double-digit interest

The maximum initial loan-to-value ratio for the volatility-proof loans is 45%, meaning that a customer who puts up $100,000 in Bitcoin as collateral can borrow up to $45,000, while the annual percentage rate (APR) is also 2.95 percentage points higher than Strike’s standard loan product.

“The secret sauce is that we’re taking the extra charge that we’re giving you guys and we’re putting it on extra hedges in the market to protect all of us.”

Strike’s standard Bitcoin loans charge an annual percentage rate between 7.75% and 11.25%, meaning the volatility-proof products could carry interest between 10.7% and 14.2%.

“If you’re OK with a slightly shorter term and a little bit higher of a fee, there is no price move that can liquidate you,” Mallers said.

Over the past year, Bitcoin has fallen 54% from its all-time high of $126,080 in October to $58,190 on June 25.

Bitcoin investor Fred Krueger said the loan product “could eliminate one of Bitcoin’s biggest structural problems: forced selling during market crashes.”

“Instead of volatility causing automatic liquidations, defaults would be driven by borrowers’ inability to service debt rather than by temporary price swings,” he said.

Related: Coinbase rolls out UK crypto-backed loans as FCA shapes rules

“Great product for those who need near-term liquidity and don’t want to risk liquidation,” added Vibes Capital Management executive chairman Rob Topping, though he also acknowledged the 14% APR was expensive.

Customers must pay up or face consequences

If a client misses a payment, they have 10 days to make the payment or contact Strike to explain their financial situation, Mallers said.

Failing to pay after that 10-day period may mean Strike starts liquidating their Bitcoin to cover the overdue amount, Mallers warned.

“If we don’t hear from you for a few weeks, then I may have no choice but to sell off some of the Bitcoin because it seems like you’re doing a hit-and-run.”

“That’s why we call it ‘volatility-proof,’ not ‘liquidation-proof,’” Mallers added.

The Bitcoin loans are offered in most US states and can be taken out in both personal and business names. They can be used for new loans, refinancing or consolidating.

While the minimum loan amount varies from state to state, the minimum loan offered through personal loans is $10,000, while businesses in certain states can access loans as low as $5,000.

Features: Bitcoin miners are pivoting to AI, so why is the hashrate near ATHs?

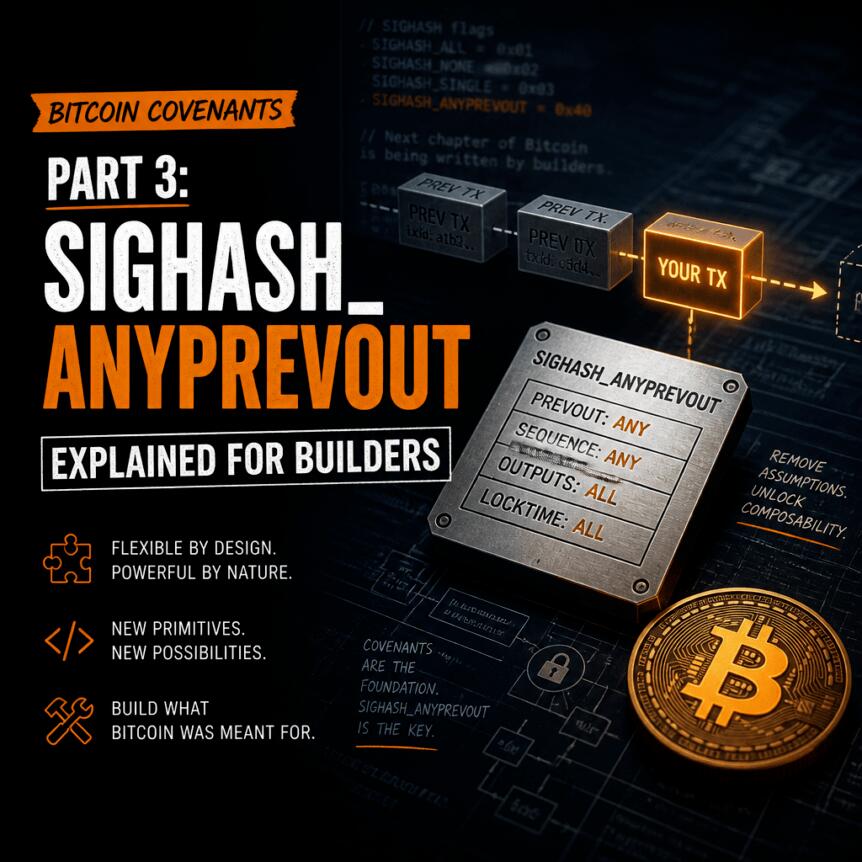

Bitcoin covenants continue to be explored through incremental, deployable changes to the protocol—rather than sweeping new functionality. In Cointelegraph Research’s technical series, the focus shifts to SIGHASH_ANYPREVOUT, a proposed soft-fork upgrade that changes how Bitcoin signatures bind to the transaction they authorize.

As described in BIP 118, SIGHASH_ANYPREVOUT would not introduce a new opcode. Instead, it proposes a new value for the SIGHASH flag so that signatures can omit commitment to the exact outpoint being spent. The key idea: keep important parts of the previous output committed, while relaxing one binding that normally prevents safe signature reuse across compatible UTXOs.

Key takeaways

- SIGHASH_ANYPREVOUT is a proposed SIGHASH-flag value, not a new opcode, intended for soft-fork deployment.

- The proposal excludes the spent outpoint from the signature digest, enabling signature reuse across different but compatible UTXOs.

- SIGHASH_ANYPREVOUT preserves commitments to the previous output’s amount, scriptPubKey, and the input’s nSequence; SIGHASH_ANYPREVOUTANYSCRIPT relaxes the scriptPubKey commitment too.

- Because the signature no longer commits to a specific outpoint, replay risk increases, depending on how the scheme is configured and implemented.

- The “soft-fork upgradability” constraints limit applicability to taproot spends under the proposal’s design.

Why outpoint binding matters in Bitcoin signatures

In Bitcoin, the SIGHASH flag is appended to a signature and determines what parts of a transaction are included in the data that the CHECKSIG opcode verifies. The signer chooses the SIGHASH value; it is not enforced by scriptPubKey. The upshot is that different SIGHASH modes control how tightly a signature is cryptographically bound to the transaction structure.

Cointelegraph Research notes that Bitcoin already has several standard SIGHASH behaviors. For example, with SIGHASH_ALL, the signature must cover all inputs, all outputs, and the specific outpoint (the transaction ID plus output index) being spent—meaning the authorization is locked to that exact UTXO. Variants like SIGHASH_NONE and SIGHASH_SINGLE loosen what outputs are committed to, while ANYONECANPAY allows a single input to be signed independently of other inputs. However, the common thread is that none of these established modes allows the signature to omit commitment to the outpoint itself.

That omission—removing outpoint commitment from the digest—is the central change SIGHASH_ANYPREVOUT introduces.

What BIP 118 proposes: two ANYPREVOUT variants

According to BIP 118, SIGHASH_ANYPREVOUT defines two variants that differ in how much of the previous output remains in the signing digest.

SIGHASH_ANYPREVOUT excludes the outpoint from the digest. But the signature still commits to several other fields: the previous output’s amount and scriptPubKey, along with the input’s nSequence. In other words, the signature is not tied to “which exact UTXO index is spent,” yet it remains tied to the characteristics of the previous output relevant to spending conditions.

SIGHASH_ANYPREVOUTANYSCRIPT goes further by also excluding the previous output’s amount and scriptPubKey. As Cointelegraph Research highlights, this means the signature is not bound to the locking script of the spent output at all. The rest of the signature message construction follows the normal Taproot signature digest rules, depending on the selected base flag (such as SIGHASH_ALL or SIGHASH_SINGLE).

How signature reuse could work—and why it matters for layer-2

The practical effect of leaving the outpoint out of the digest is that the same signature can authorize spending any compatible UTXO that matches the remaining committed fields. Cointelegraph Research provides a concrete example: a transaction pre-signed under ANYPREVOUT | ALL to create a 0.5 BTC output could be reused later if the address receives a different 0.5 BTC UTXO. In that scenario, reuse does not depend on retaining the original signing key.

But reuse is not free of economic consequences. If the new UTXO holds more than the original amount, the extra value may be lost to miners unless the original design included a change output. That means protocol designers still need to account for the possibility that the “next available” compatible UTXO might differ in total value—despite the signature being reusable.

Cointelegraph Research connects this rebinding property to a broader use case: layer-2 protocols. In these systems, it’s common to preconstruct or preauthorize transactions that must later become valid under multiple possible on-chain realities. By allowing the same pre-signed transaction to apply to multiple compatible UTXOs, ANYPREVOUT-style flexibility can reduce the number of times new signatures—and new coordination—are required.

Where covenants fit—and what remains technically missing

For covenant-like applications, the research notes a crucial distinction. SIGHASH_ANYPREVOUT preserves commitment to the previous output’s scriptPubKey, making it more relevant than SIGHASH_ANYPREVOUTANYSCRIPT, which removes that binding entirely. If the goal is to enforce that funds remain governed by a specific locking script across compatible UTXOs, maintaining that commitment is typically important.

The series also clarifies a limitation. While SIGHASH_ANYPREVOUT improves on what pre-signed transactions can already do, it does not by itself enable more advanced covenant mechanisms such as recursive covenants or transaction introspection. Instead, it changes the binding between a signature and a specific UTXO, allowing reuse across compatible candidates—one building block rather than a complete covenant system.

Cointelegraph Research additionally references academic work suggesting another theoretical angle: removing outpoint commitment might enable “recovered-key” constructions where a public key can be derived from a fixed signature and message pair such that the corresponding private key is provably unknown. In principle, that could force spending through a script path rather than a key path, potentially avoiding temporary keys used in some script-path-only designs. However, the piece stresses that this observation appears in research literature rather than representing a BIP-118 design proposal.

The main downside: signature replay risk

The most important concern with SIGHASH_ANYPREVOUT signatures is signature replay. Cointelegraph Research explains that because the signature does not commit to a specific outpoint, the same signature can be used to spend a different UTXO than the one originally intended—so long as the new UTXO satisfies the other committed fields.

The severity depends on configuration and surrounding assumptions. The research highlights situations where replay becomes more pronounced, such as:

- Using ANYPREVOUT | SINGLE when output amounts can be rearranged.

- Having a separate UTXO with the same scriptPubKey and amount in the case of ANYPREVOUT.

- Having compatible script structures that include the same public key in the case of ANYPREVOUTANYSCRIPT.

- Miner influence over transaction ordering and inclusion that could potentially be exploited under certain conditions.

At the same time, Cointelegraph Research emphasizes that these are not unavoidable flaws. They generally require deliberate misuse or failure to account for replay conditions during protocol design and implementation.

Looking ahead, Cointelegraph Research says the next article will move from signature mechanics to “supporting tools”—opcodes that expand what Bitcoin script can express or how data can be handled, but don’t provide covenant behavior on their own. For readers tracking SIGHASH_ANYPREVOUT’s relevance, the open watchpoints are straightforward: how developers plan to mitigate replay risk, which taproot spend patterns emerge in practice, and whether future covenant constructions can leverage the relaxed outpoint binding without introducing new operational fragility.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

EX DeFi is gaining attention as an AI-powered cloud mining platform, offering users access to BTC, DOGE, and LTC mining without owning hardware.

Summary

- EX DeFi launched a cloud mining platform with AI-powered infrastructure and free computing power for new users.

- It has expanded its cloud mining services, highlighting AI optimization, security features, and multi-asset support.

- The platform has introduced AI-driven cloud mining services for BTC, DOGE, LTC, and other major digital assets.

As we enter 2026, mainstream digital assets such as Bitcoin (BTC), Dogecoin (DOGE), and Litecoin (LTC) continue to attract widespread attention from global investors. For many newcomers to cryptocurrencies, how to participate in the digital asset market with a lower barrier to entry and explore long-term profit opportunities has become a key focus. Therefore, free cloud mining platforms are gaining popularity.

Compared to traditional mining models that rely on ASIC miners, cloud mining eliminates the need to purchase expensive equipment and incur electricity costs or complex maintenance. Users simply need to register to participate in the digital asset ecosystem through cloud computing power, starting their digital asset experience in a more convenient way.

Among numerous cloud mining platforms, EX DeFi has gradually become one of the most watched platforms in the market due to its AI-driven computing power optimization technology, automated management system, and transparent operating model. The platform offers a variety of cloud computing power products, helping users participate in the digital asset ecosystem more easily and efficiently, attracting the attention of many novice users and long-term investors.

EX DeFi – A Cloud Mining Platform to Watch in 2026

Register now and receive a $17 reward of computing power for new users!

For those new to cloud mining, EX DeFi offers a low-barrier-to-entry experience. The platform provides new users with $17 worth of free computing power, combined with AI-powered intelligent hosting and computing power optimization technology, making it easier for users to participate in cloud computing services. Whether someone is a cryptocurrency novice or someone looking to learn about long-term cloud computing models, EX DeFi makes it easy to start their digital asset journey.

EX DeFi Platform Advantages

Compliance and Transparency

Headquartered in the UK, EX DeFi is committed to providing digital asset services within a transparent and compliant operating framework, continuously improving its platform operation system to create a more reliable user experience.

Security Protection

The platform employs an offline cold wallet storage solution, combined with the McAfee® cloud security system and Cloudflare® enterprise-grade network protection, providing multi-layered protection for user accounts, assets, and data security.

Supports Multiple Mainstream Digital Assets

The platform supports multiple mainstream digital assets, including BTC, ETH, XRP, USDC, DOGE, SOL, LTC, and USDT, meeting the asset management needs of different users.

Daily Earnings Settlement

Cloud computing power earnings are settled daily according to platform rules. Users can flexibly manage their assets according to platform regulations, providing a more convenient experience for long-term participation in the digital asset ecosystem.

Green Energy Data Center

EX DeFi’s data center uses clean and renewable energy to provide stable support for cloud computing power services, while actively practicing green and sustainable development concepts.

Affiliate Program

The platform launches an affiliate program, where eligible users have the opportunity to receive rewards of up to $50,000, providing more incentives for long-term participation in the platform ecosystem.

How to Start Earning Passive Income?

1. Register

Visit the EX DeFi official website and create an account on the platform using an email address. Upon successful registration, users will receive a $17 newcomer bonus.

2. Choose a Smart Contract Plan

Choose a popular mining contract that matches a particular budget and contract term, and start automatic mining with one click.

3. After purchasing the contract,

The system will automatically contribute computing power to the mining pool, and the rewards will be automatically credited to the account within 24 hours. No action is required; the principal will be automatically returned upon contract expiration.

Popular DeFi Yield Plans

BTC (Beginner Trial Contract): Investment: $100 | Term: 2 days | Daily Yield: $4 | Total Yield: $100 + $8

DOGE (Goldshell-Mini-Doge-Pro): Investment: $500 | Term: 6 days | Daily Yield: $6.5 | Total Yield: $500 + $39

BTC (Canaan-Avalon-A1466): Investment: $1,000 | Term: 10 days | Daily Yield: $13.4 | Total Yield: $1,000 + $134

BTC (Bitmain-S19): Investment: $7,000 | Term: 25 days | Daily Yield: $107.8 | Total Yield: $7,000 + $2,695

BTC (Whats-M56) Investment Amount: $30,000 | Term: 33 days | Daily Yield: $501 | Total Earnings: $30,000 + $16,533

Click here to learn more about EX DeFi mining contract options.

Conclusion: Why EX DeFi is one of the mining platforms to watch in 2026

As the digital asset industry continues to develop, cloud computing power is gradually becoming a convenient way for more and more users to participate in the cryptocurrency ecosystem. Among many platforms, EX DeFi has attracted the attention of more and more new users with its transparent operating model, intelligent computing power management, and simplified usage process, providing users with a more relaxed digital asset participation experience.

For office workers, freelancers, and digital asset novices who want to understand the cloud mining model with a lower barrier to entry, EX DeFi provides a more convenient way to get started. Users do not need to purchase complicated hardware equipment to participate in the digital asset ecosystem through cloud computing power, and further understand and experience how to create more income using computing power.

Ready to start the cryptocurrency journey? Register for EX DeFi now and start the intelligent passive income journey.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

EDX Markets, a cryptocurrency exchange focused on institutional investors, has raised $76 million in a Series C funding round led by Japan’s SBI Holdings, marking one of the larger funding rounds this year for crypto market infrastructure as institutional adoption continues to expand.

The company said Monday it will use the proceeds to expand its spot trading, clearing and settlement services, develop new products and grow internationally. EDX operates a US-focused institutional spot exchange and a Singapore-based perpetual futures venue for eligible non-US institutional clients.

The latest round builds on previous backing from traditional financial companies, including Citadel Securities, Fidelity Digital Assets, Virtu Financial and Charles Schwab, highlighting continued investor appetite for institutional crypto infrastructure despite a slower venture funding market.

Source: EDX Markets

EDX has quietly expanded its institutional footprint over the past year. In May, Ripple Prime integrated with the exchange, allowing institutional clients to access EDX’s spot and perpetual futures liquidity through Ripple’s prime brokerage platform, with the companies also planning to support RLUSD as a settlement and collateral asset.

The exchange has processed as much as $685 million in daily trading volume, underscoring growing demand for institutional crypto trading venues.

Related: Ripple co-founder backs venture launched by US senator’s son: Report

Crypto infrastructure continues to attract capital despite bear market conditions

The latest funding round reflects continued investor interest in institutional crypto infrastructure, even as digital asset trading volumes have softened and venture funding remains below the industry’s 2021 peak.

Investors have increasingly backed companies building trading, payments and settlement infrastructure, betting that institutional adoption will continue to expand as the US regulatory environment becomes more accommodating.

San Francisco-based Framework Ventures, an early investor in several crypto startups, recently raised $400 million for a new fund targeting frontier technologies, including blockchain networks and decentralized finance, according to Fortune.

Other crypto infrastructure startups have also secured fresh capital. Fomo, a crypto trading startup focused on cross-chain trading, recently raised $75 million at a $550 million valuation. Meanwhile, Trace Finance, a startup building stablecoin-based cross-border payment and settlement infrastructure for businesses, raised $32 million to expand its platform.

Magazine: Bitcoin decouples from tech stocks, Ether eyes ‘selling wave’: Market Moves

A decentralized exchange swap worth $2.01 million ended in a steep loss for one trader after a liquidity router routed the trade through a thin market, enabling an Ethereum block builder to capture profits from a same-block arbitrage. According to GoPlus Security, the order effectively turned into a “backrun extraction” rather than a fair swap outcome—one that left the victim with only about $14,500 in the resulting tokens.

The episode highlights how maximal extractable value (MEV) activity and routing mechanics can combine to produce outsized losses when trades are executed through low-liquidity pools. It also underscores a practical lesson being shared in the community: users should review the transaction route before signing DEX actions, not just confirm the trade.

Key takeaways

- A $2.01 million ETH swap on a DEX resulted in a near-total value drop, landing at roughly $14,500 after execution via a low-liquidity pool.

- GoPlus Security described the event as same-block backrun extraction, not a conventional “sandwich” attack.

- Titan Builder was identified as the largest beneficiary, receiving about $1.8 million as a builder reward from the transaction.

- The victim’s route involved routing into an AVAIL/WETH pool that executed at around 120x the later sell price, enabling an imbalance to be monetized.

- Traders are being urged to verify swap routes before confirming, since clicking through without inspecting routing can lead to irreversible execution outcomes.

A swap that was rerouted into a low-liquidity trap

GoPlus Security said the trader swapped 1,126.44 ETH on Monday at 1:59 am UTC but received only 5,776 Lighter (LIT) tokens. The security firm framed the result as a “textbook case of same-block backrun extraction,” where the trade’s execution path created an exploitable price discrepancy within the same block.

In the assessment, this was not portrayed as a classic sandwich attack. Instead, the core mechanic was that a router directed the swap through a pool with insufficient depth, allowing another actor—working with block-building capabilities—to profit from the temporary mispricing and the order’s same-block lifecycle.

The incident was publicly discussed via on-chain analysis referenced in earlier community posts, including Lookonchain, and GoPlus’s commentary identifying the nature of the extraction.

How the route imbalance drove a ~99% loss

GoPlus Security’s breakdown points to the swap’s intermediate routing. The firm said the victim’s transaction routed roughly 1,117 ETH into a low-liquidity AVAIL/WETH pool on Uniswap v3. Once executed, the swap price was reportedly around 120 times higher than what the received AVAIL tokens could later be sold for.

That pricing mismatch becomes a leverage point when a trade is executed in a way that creates a temporary window for extraction. After the trader received nearly 6.67 million AVAIL tokens at an inflated price, the router involved—identified by GoPlus as “0x router”—reportedly sold a small amount of externally sourced AVAIL back into the same pool. The purpose, according to GoPlus, was to extract approximately 1,072 WETH before paying out 1,018 ETH, worth about $1.8 million, to Titan as a builder reward.

After these internal steps, the AVAIL was swapped for LIT tokens valued at roughly $14,200. That translated to a reported 99.3% loss for the trader, based on the amounts described in GoPlus Security’s analysis.

For users, the key takeaway is that the harm didn’t come from a smart contract “hack” in the typical sense. It came from execution conditions—specifically, routing into a pool where trade size relative to liquidity could severely distort outcomes, while MEV-aware infrastructure could monetize that distortion before the victim can unwind.

Why this is more than “just a bad swap”: MEV and routing mechanics

The episode fits a broader pattern in decentralized trading: as long as block builders can influence transaction ordering and routing can route through multiple liquidity venues, the same block can contain both the victim’s swap and the counter-trade needed to extract advantage from temporary imbalances.

The article’s framing also connects the event to ongoing concerns about MEV bots and liquidity routers atop a landscape that already faces risks from scams and exploits. While the details here are specific, the implication is general—traders may believe they are placing a straightforward order, but routing behavior and transaction ordering can turn the execution into a target.

From an investor or trader perspective, this means diligence has to extend beyond token and protocol selection. Execution parameters—including route, intermediary hops, and whether a swap is likely to interact with thin liquidity—can determine whether the trade results in the expected price or in an unfavorable extraction scenario.

Community warning: read the route before you click confirm

In response to incidents like this, crypto trader Ruslan Khairullin advised that traders should read the transaction route before signing the transaction. He described the event as what happens when someone “clicked confirm faster than you read the route,” calling it a “painful lesson” after the fact.

This kind of guidance is practical because it targets the behavioral failure mode: users often focus on the expected output shown by interfaces while ignoring what the route actually does under the hood. In low-liquidity conditions, the route’s intermediate steps can matter as much as—if not more than—the end pair.

Where the mechanics are especially risky is when routing can pull a large trade into a pool with limited depth, because the price impact can be severe enough to create an exploitable imbalance. If the resulting swap path lets MEV-capable actors profit within the same block, victims may not have a straightforward opportunity to recover at a reasonable price.

Titan Builder’s role and what to watch next

GoPlus Security identified Titan Builder as the biggest beneficiary, stating it received about $1.8 million from the transaction as a builder reward. Cointelegraph reported that it reached out to Titan but did not receive an immediate response. Separately, DefiLlama data shows Titan has made $112.6 million in revenue from block building services this year.

The firm’s profitability is not limited to this case. Cointelegraph noted that Titan’s biggest day this year came in March, when it extracted around $34 million in arbitrage profit from a MEV bot incident involving the CoW Protocol.

For market participants, the immediate question is not whether these mechanics exist—they do—but how often they are triggered by routing into low-liquidity pools and whether future tooling will make route inspection easier for ordinary users. The next developments to watch are whether DEX interfaces or aggregators tighten route transparency by default and whether users get better warnings when a trade path passes through thin liquidity that could be targeted by same-block extraction.

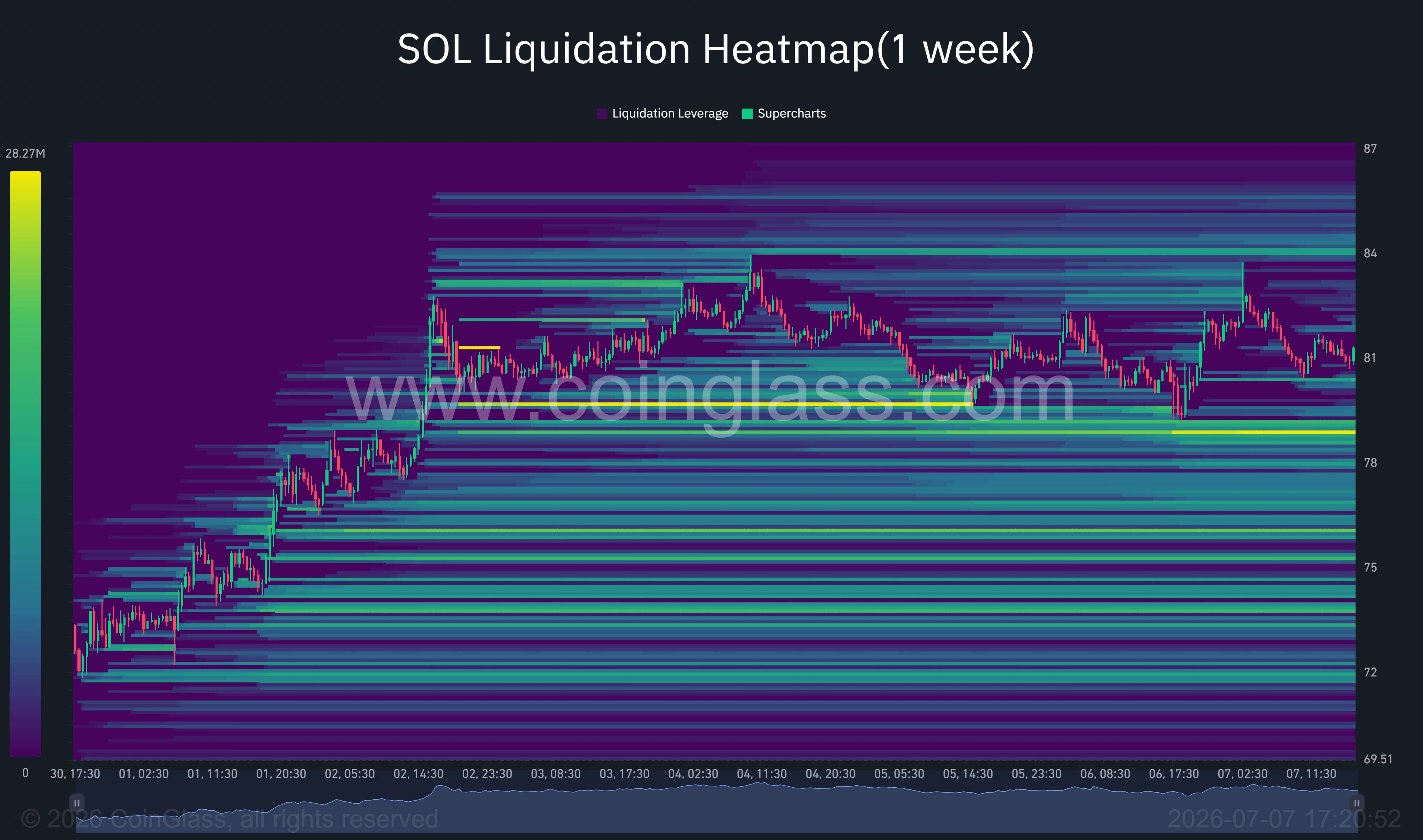

Solana has extended its July rally after record on-chain activity, tokenized stock issuance, and steady ETF inflows revived bullish sentiment.

Summary

- Solana climbed above $81 after tokenized stock issuance and record network activity boosted buying interest.

- Technical charts show bulls defending $80 support while traders watch $83 and $90 as the next resistance levels.

- Analysts remain optimistic on long-term upside, though macro risks and liquidity could limit near-term gains.

According to data from crypto.news, Solana (SOL) extended its recovery this week, gaining roughly 11% over several sessions to trade around $81 after briefly reclaiming the $82 level. The rally accelerated as institutional adoption on the network continued to expand, led by Securitize tokenizing $295 million worth of New York Stock Exchange-listed common stock on Solana following its SPAC debut.

The development arrived alongside the launch of the Solana Foundation’s Governance Proposals framework, introducing formal on-chain validator voting and adding another utility milestone for the ecosystem.

Network activity has expanded at the same time. Solana processed more than one billion weekly non-vote transactions for the first time, while tokenized asset spot volume reached an all-time quarterly high of $5.77 billion, reinforcing the network’s growing role in real-world asset issuance.

Institutional demand also remained positive, with spot Solana ETFs recording approximately $5.75 million in net inflows even as several other crypto investment products experienced persistent capital outflows.

Technical structure has shifted back in favor of buyers

The daily chart shows Solana recovering from its June selloff after buyers defended the long-term support zone near $73, close to the 0.786 Fibonacci retracement level referenced by many traders during last month’s decline. Price has now reclaimed the previous breakdown area around $80.14 and is attempting to convert it into support while approaching horizontal resistance near $83.13.

Momentum indicators have improved alongside the rebound. The daily RSI has climbed above 62 after recovering from oversold conditions in June, while the Supertrend indicator has remained bullish with dynamic support near $69.6. A successful close above $83 could expose the next resistance around $90, whereas failure to hold above $80 may invite another test of the $75.4 support region.

Shorter-term charts also favor bulls. On the 4-hour timeframe, SOL continues trading above its 20-, 50-, 100- and 200-period moving averages, with the 20 SMA near $81.4 providing immediate dynamic support. The moving average alignment remains constructive even as price has entered a brief consolidation after last week’s sharp advance. The Aroon indicator still favors buyers, although the slight decline in Aroon Up suggests momentum has slowed while the market waits for another catalyst.

Derivatives positioning presents a similar picture. CoinGlass liquidation heatmaps show one of the largest nearby short liquidation clusters sitting around the $84 level. A decisive move through that zone could trigger forced short covering and accelerate upside toward the upper liquidity pocket near $87. On the downside, dense long liquidation levels have accumulated between $78 and $79, making that area an important support if profit-taking intensifies.

Analysts target triple-digit prices while key resistance remains intact

Market participants have also become more optimistic after Solana strengthened against Bitcoin. Commenting on the latest structure, analyst Michaël van de Poppe wrote that SOL “is still in an uptrend here,” adding that it has broken its year-long downtrend versus Bitcoin.

“I don’t think that we’ll stall, I do think that we’ll continue to see strength happening here,” he wrote, adding that he would buy lower levels if a deeper correction develops before concluding that “it’s a matter of time until $SOL regains the $100+ levels.”

Despite the improving technical backdrop, Solana remains roughly 74% below its all-time high near $293 and more than 40% lower year to date. Macro uncertainty surrounding future Federal Reserve policy, geopolitical risks, and relatively thin crypto spot liquidity continues to limit aggressive positioning. Until bulls establish sustained closes above the $90 and $100 resistance zones, the current recovery is likely to remain vulnerable to renewed selling pressure despite the network’s strengthening institutional fundamentals.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

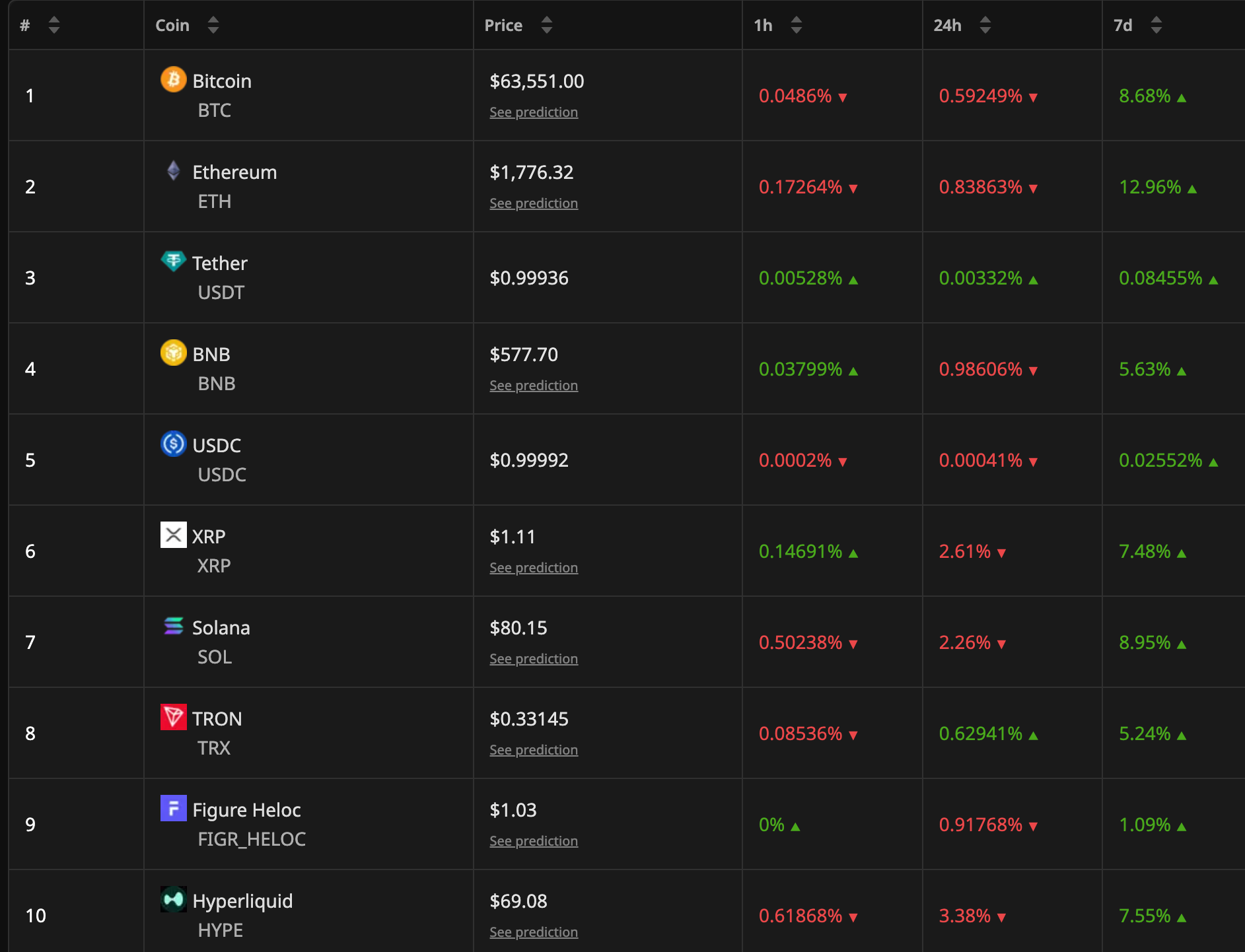

The total cryptocurrency market fell 1.24% on Wednesday after the United States launched military strikes against Iran, lifting oil prices and pushing investors out of risk assets.

Bitcoin (BTC), Ethereum (ETH), and most large tokens traded lower over the past 24 hours, though the majors held onto strong gains built over the past week.

Oil Price Jumps as US Strikes Hit Iran

CENTCOM said its forces struck Iran, revealing they hit more than 80 targets with precision munitions on July 7. The actions followed reports of Iranian attacks on three vessels in the Strait of Hormuz.

The latest attacks tested a fragile ceasefire reached between Washington and Tehran last month. The military described the operation in a statement posted to social media.

“The unwarranted aggression by Iranian forces is a clear and dangerous violation of the ceasefire and undermines freedom of navigation,” CENTCOM wrote.

Follow us on X to get the latest news as it happens

At the same time, Washington re-imposed sanctions on Iranian oil. The Ministry of Foreign Affairs of the Islamic Republic called it a “clear and material breach of Article 10 of the Memorandum of Understanding on the Cessation of War.”

Following the escalation, oil prices jumped. Brent crude rose 2.05% to $75.68 a barrel, according to Trading Economics data. US West Texas Intermediate (WTI) gained 2.07% to $71.90.

Crypto Retreats in Risk-Off Move

Meanwhile, crypto markets moved in the opposite direction, with the total market cap down 1.24%. Bitcoin traded near $63,551, down 0.59% over 24 hours. Ethereum slipped 0.84% to about $1,776.

Hyperliquid (HYPE) led losses among the top 10 assets, falling 3.38% to $69.08. XRP (XRP) dropped 2.61%, and Solana (SOL) fell 2.26%.

The pullback came after a strong week for digital assets. Higher oil prices tend to fuel inflation worries. Those concerns can push expectations of interest rate cuts further out, weighing on risk assets.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Crypto Market Slips 1.24% as US Strikes on Iran Lift Oil appeared first on BeInCrypto.

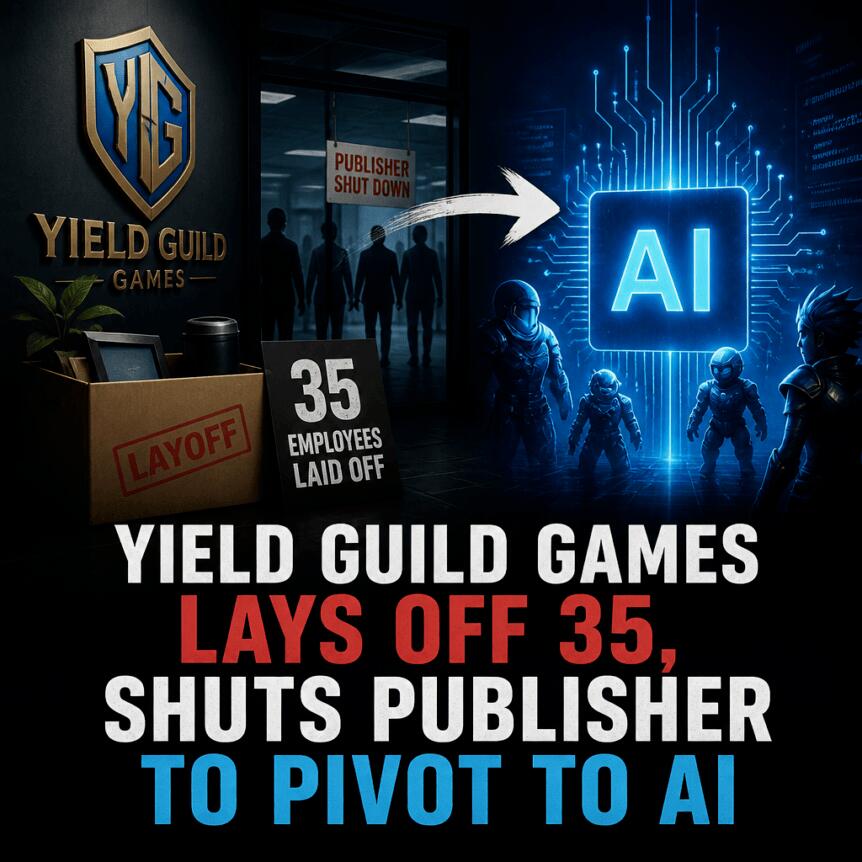

Yield Guild Games (YGG) has moved to shut down its crypto game publishing arm, YGG Play, while cutting 35 employees and redirecting resources toward AI-focused datasets. The restructuring comes as the company cites a prolonged downturn in crypto markets alongside a difficult environment for video game publishing.

In an update posted Monday, YGG said it is sunsetting the web-based publishing activities under YGG Play because it no longer expects consumer demand in crypto gaming or the broader Web3 publishing market to recover “sufficiently” in the near term. The company also attributed the shift to how a major market crash on Oct. 10 “fundamentally altered retail market psychology.”

Key takeaways

- Yield Guild Games is sunsetting YGG Play, ending its publishing website, web app experience, and community rewards support.

- The company will lay off 35 employees, pointing to weak crypto consumer conditions and an unsustainable publishing market.

- YGG says the restructure extends its operating runway to four years, citing $20.6 million in treasury funds as of the end of the first quarter.

- Instead of publishing games, YGG plans to build “AI data economy” pipelines using behavioral datasets generated by its global community through gameplay.

Sunsetting YGG Play amid market stress

According to YGG’s announcement, the decision is driven less by product performance and more by the economics of Web3 game publishing under current conditions. The company said YGG Play “cannot be commercially sustainable,” blaming both a continued crypto market slump and what it called a “similarly brutal” video game publishing landscape.

In a brief statement included with the update, YGG co-founder Gabby Dizon framed the move as a response to market realities. She said sunsetting YGG Play is a “market decision, not a product decision,” adding that she was “proud of what this team achieved under such tough conditions.”

As part of the shutdown, YGG said it will close the YGG Play website, discontinue its web app used to launch games, and end marketing support for third-party titles. That includes taking down specific games listed as browser-based offerings, while other Web3 versions are set to remain accessible.

What ends—and what stays live

YGG said it will remove LOL Land, a browser game described as a “game in the style of a board game,” and also take down the puzzle game Waifu Sweeper.

However, YGG indicated that Web3 versions of two other titles would continue as normal. Those are the baseball game GIGACHADBAT and the battle game Ragnarok Breaker. The company’s update suggests that it will focus on maintaining certain blockchain-based game experiences while stopping the publishing and support layer that sits behind YGG Play’s broader web infrastructure.

The company also said it would end marketing support for third-party games distributed through YGG Play, signaling that the restructure is not limited to internal game development but also affects the broader publishing and promotion function.

From publishing to AI training data pipelines

While sunsetting YGG Play, Yield Guild Games says it is pivoting toward “the AI data economy.” The company’s plan is to use its community to create datasets designed to help train AI systems.

YGG stated it will initially build a pipeline for gaming datasets and that its global community “can generate these behavioral datasets just by playing.” In other words, rather than monetizing publishing as a standalone activity, YGG is positioning gameplay behavior as a raw input for AI model training.

The company also argued that games create complex, real-time decision-making environments. In YGG’s framing, video game players continually make split-second choices, often involving “human irrationality and emergent behavior,” which it says AI networks could benefit from learning.

This shift reframes YGG’s role in the Web3 ecosystem: from distributing and promoting games to contributing structured behavioral information that can support AI development.

Runway extended, layoffs align with broader crypto job cuts

YGG said the sunsetting of YGG Play and the associated restructuring will extend its operating runway to four years. The company added that it held $20.6 million in treasury as of the end of the first quarter.

The layoffs at YGG are part of a wider wave of workforce reductions across the crypto sector. Data cited in the reporting shows that crypto companies have cut more than 5,000 jobs this year, with many employers citing difficult market conditions and a redirection of budgets toward artificial intelligence initiatives.

Examples highlighted include Block Inc.’s large February layoff round in which it cut 4,000 staff, roughly half its workforce at the time, according to earlier coverage from Cointelegraph. BitGo later laid off about 15% of staff (estimated at 90 people), while Robinhood reportedly reduced its workforce by 10%. Earlier in the year, Kraken said it cut 150 roles and Coinbase reduced 700 employees, with Gemini also cutting 200 employees in February and Crypto.com reducing about 180 staff the following month—again citing the role of AI in shaping staffing priorities.

For investors and builders, the pattern suggests companies are not only tightening costs, but also changing what they view as the most durable growth lever. In YGG’s case, that lever is shifting from Web3 entertainment publishing toward data production tied to AI training—an approach that may be less dependent on immediate consumer spending on new crypto game launches.

What remains to be seen is how YGG will translate community gameplay into usable datasets in practice, and whether its AI data direction can generate sustainable revenue or partnerships at scale. Readers should watch for details on the pipeline, how YGG measures dataset quality and value, and which of its current game experiences remain central to that data strategy as the YGG Play transition continues.

Ex-FBI Agent Says Nancy Guthrie’s Kidnapper Was ‘an Amateur’ as Savannah Publicly Marks Five Months of Agony

Michael Saylor Reveals the One Metric Keeping MicroStrategy’s Bitcoin Play Sustainable

“X-Factor” for 2026 Vikings Has Been Identified

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: High Hopes

-

NewsBeat3 days ago

NewsBeat3 days agoTaylor Swift and Travis Kelce wedding staffer hilariously struggles to keep her cool while checking in megastars

-

Fashion1 day ago

Fashion1 day agoOpen Thread: What Great Books Have You Read Recently?

-

Crypto World7 days ago

Crypto World7 days agoAirdrop Registration Becomes Key Focus For Remittix As RTX Launch Updates Approach

-

Politics5 days ago

Politics5 days agoThe House | “Reframing the debate from a binary discussion of winners and losers”: Yuan Yang reviews ‘We Are Not Machines’

-

Crypto World4 days ago

Crypto World4 days agoStandard Chartered Secures MiCA License as ESMA Adds 37 New Crypto Firms

-

Business1 day ago

Business1 day agoAXT Shares Jump Nearly 14% as Semiconductor Materials Maker Rebounds on AI-Linked Indium Phosphide Demand

-

Sports7 days ago

Sports7 days agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Crypto World6 days ago

Crypto World6 days agoBinance stock trading tops $1B in first month after launch

-

Crypto World1 day ago

SK hynix (000660.KS) Stock Dips as $28B Nasdaq ADR Offering Drives AI Memory Expansion

-

Crypto World6 days ago

Crypto World6 days agoAlibaba-affiliate Ant Group enters the humanoid robot market with 12 deals

-

Crypto World3 days ago

Crypto World3 days agoSouth Africa proposes crypto tax guidance under existing rules

-

News Videos1 day ago

News Videos1 day agoBest Time to Enter Small Caps Right Now? Another Bull Run? | Financially Free

-

Tech3 days ago

Tech3 days agoLenovo laptops are now shipping with YMTC SSDs, a sign of Chinese NAND entering the mainstream

-

News Videos23 hours ago

News Videos23 hours agoWhats Hidden Inside This Cash Register? #treasure #reselling #money

-

Business6 days ago

Business6 days agoMeta Platforms Stock Jumps 7% Today as Bloomberg Reports Company Plans to Enter the Cloud Business

-

NewsBeat6 days ago

NewsBeat6 days agoNew exhibition reflects five decades of movement between island of Ireland and GB

-

Business5 days ago

Business5 days agoWhat a 10 Percent Drop Means for Buyers, Sellers and Renters

-

Crypto World5 days ago

Crypto World5 days agoBinance Re-Enters Philippines As EU MiCA Rules Restrict Access

-

News Videos2 days ago

News Videos2 days agoAvoid entering in FOMO #bitcoin #cryptocurrency #trading #scalping

You must be logged in to post a comment Login