Business

ClearBridge Global Value Improvers Strategy Q4 2025 Commentary

LumerB/iStock via Getty Images

By Grace Su & Jean Yu CFA, Ph.D.

Key Takeaways

- Global equity markets delivered solid fourth-quarter gains, with value stocks outperforming growth as market participation continued to broaden beyond mega cap technology.

- The Strategy outperformed its benchmark during the quarter, driven by strong stock selection in communication services, financials and industrials.

- With valuation dispersion elevated and fundamentals improving across a widening set of companies, we believe the opportunity set for global value improvers remains attractive heading into 2026.

Market Overview

Global equity markets generated positive returns in the fourth quarter, with value stocks outpacing growth for the quarter and only slightly trailing growth on a full-year basis. The MSCI World Index rose 3.1% in the quarter to finish up 21.1% for 2025, outperforming the S&P 500 Index’s gains of 2.7% for the quarter and 17.9% for the year. Value stocks also maintained leadership during the fourth quarter, with the MSCI World Value Index returning 3.3% compared to the MSCI World Growth Index’s 2.8%.

In the fourth quarter, market narratives remained heavily focused on artificial intelligence-related investment, reflected most visibly in the outsize performance of technology-heavy markets such as Taiwan and South Korea. However, the quarter also saw continued strength across emerging markets, commodities and select value-oriented sectors, underscoring a gradual broadening in market participation. A weaker U.S. dollar and expectations for easier monetary policy supported sentiment toward emerging markets and consumer-sensitive areas.

From a macroeconomic perspective, growth continued to slow in Europe, particularly across manufacturing-related industries, though services activity remained resilient and equity markets generally held up well. In China, signs of stabilization in manufacturing activity supported risk appetite, while the U.S. consumer remained comparatively resilient. Despite the “everything rally” that characterized much of 2025, the fourth quarter highlighted how expectations, positioning and valuation continue to play an outsize role in driving relative outcomes.

The fourth quarter highlighted how expectations, positioning and valuation continue to play an outsize role in driving relative outcomes.

Quarterly Performance

The ClearBridge Global Value Improvers Strategy outperformed its benchmark during the fourth quarter, supported by strong stock selection across communication services, financials and industrials, partially offset by weakness in information technology (‘IT’) and health care.

Despite being the worst-performing sector of the MSCI World Value benchmark, communication services represented a bright spot for the Strategy. Alphabet (GOOG) rose on strong revenue growth in its latest earnings, driven by accelerating ads, cloud revenue growth and, importantly, AI-driven ad optimization, benefiting from its depth of data and tech.

Financials were among the largest contributors to relative performance. Banco Bilbao Vizcaya Argentaria (BBVA) (‘BBVA’), a Spain-based global banking group with leading franchises in Mexico and Turkey, performed well as improving credit trends, disciplined cost control and a favorable capital return profile supported earnings. The bank also benefited from easing macro concerns in Europe and resilient loan growth in key international markets. Lloyds Banking (LYG), a U.K.-focused retail and commercial bank, also contributed as macroeconomic risks tied to the U.K. budget, including potential incremental taxes on banks, proved overdone and investor focus returned to the company’s strong earnings visibility and attractive capital return profile.

Industrials also contributed positively, led by several multi-quarter compounders. Siemens Energy (SMNEY), a German manufacturer of power generation and transmission equipment, continues to benefit from rising global investment in grid upgrades and power generation capacity, particularly as utilities expand infrastructure to meet data center electricity demand. Hitachi (HTHIY), a Japanese industrial and technology conglomerate, continued to simplify its portfolio and improve margins while benefiting from exposure to digital infrastructure and electrification themes.

On the down side, stock selection in IT detracted from relative performance. Microchip (MCHP), a U.S.-based semiconductor manufacturer, reduced forward guidance as tariff and demand uncertainty continued to delay the cyclical recovery of its business. Corcept Therapeutics (CORT), a U.S.-based biotechnology company focused on endocrinology and oncology indications, declined late in the quarter following a Food and Drug Administration Response Letter that cited the need for additional evidence to support approval of its relacorilant program. This introduced uncertainty around the timing and commercial potential of a key pipeline asset, and we ultimately elected to exit the position.

From a regional perspective, relative performance benefited from strong contributions in Europe ex U.K., led by financials and industrials holdings, as well as Japanese stock selection in industrial and technology-oriented sectors. Weakness in due to company-specific developments weighed on North American returns.

Portfolio Positioning

Rising electricity demand from AI, electrification and infrastructure investment favors companies involved in grid modernization, storage and efficiency solutions. A more constructive outlook toward renewables is also improving the opportunity set. A compelling example of this is new portfolio addition Brookfield Renewable (BEP), the renewable energy arm of Brookfield Asset Management (BAM), which benefits from its parent’s scale, development expertise and funding. AI-driven data center growth is supporting stronger contracting dynamics and longer-term visibility for Brookfield. Additionally, its stake in Westinghouse provides exposure to the global nuclear buildout, offering further potential upside.

We also established a position in Merck KGaA (MKKGY), a Germany-based science and technology company with businesses spanning life sciences, health care and electronics. While portions of its health care segment have faced near-term revenue pressure, recent acquisitions and a deep pipeline offer longer-term optionality, and we believe the market is underappreciating a cyclical recovery in its life sciences and electronics businesses as order trends stabilize. Merck’s business strongly aligns with SDG 3 (Good health and well-being) as it develops innovative therapies in oncology, neurology and immunology that address major non-communicable diseases and reduce disease burden and premature mortality to improve treatment outcomes for serious chronic conditions.

We exited PayPal (PYPL), a global digital payments platform, concluding that the core business has struggled to reaccelerate under new leadership amid exposure to structurally slower-growing areas of e-commerce. While operational improvements are ongoing, we believe the company’s scale and end market exposure make a meaningful rerating more challenging in the near-to-medium term. We also exited ICON (ICLR), a contract research organization, as evolving competitive dynamics and a less favorable growth outlook led us to reallocate capital toward opportunities with clearer earnings visibility.

Outlook

We enter 2026 with a more stable macro environment than this time last year. Inflation has moderated globally, giving central banks room to ease, while fiscal programs – from U.S. industrial and infrastructure spending to expanded European budgets and targeted Chinese stimulus – continue to support activity. With the effective U.S. tariff rate already having peaked, companies that absorbed tariff-related cost pressures in 2025 should lap those headwinds, creating modest tailwinds for growth.

Several themes are likely to shape markets in 2026:

Monetary easing should broaden growth: Lower rates should help support a recovery in manufacturing and small-business activity, while also benefiting rate-sensitive sectors such as housing, utilities and infrastructure. Europe and Japan remain well positioned given ongoing pro-growth policies.

Leadership expands beyond mega cap AI: While AI remains foundational, power, logistics and efficiency improvements are becoming equally important investment themes. Companies that enable the next phase of the AI cycle – rather than those solely capturing its front-end demand – are increasingly well-positioned.

Emerging markets retain meaningful value: Although outside our benchmark, EM remains one of the more attractively valued areas globally, trading at roughly 40% discount to the U.S. Disinflation offers monetary flexibility, countries like Brazil and Mexico are on firmer fiscal footing and easing dollar liquidity should support flows, creating a more fertile ground for potential alpha generation.

The U.K. looks increasingly compelling: Attractive valuations, improving inflation dynamics and falling gilt yields have created a supportive backdrop – particularly for its concentration of service-oriented industries that should benefit from AI and are spared from tariff headwinds and threats of excess capacity of Chinese exports.

M&A could provide an additional tailwind: Deregulation, strategic repositioning and the prospect of lower interest rates may support an uptick in M&A globally. Companies will likely act more decisively in an environment with reduced policy uncertainty.

With a more balanced macro backdrop, healthier geographic diversification and an expanding set of fundamental catalysts, 2026 presents a more attractive opportunity than the narrowly led markets of recent years. The companies best positioned from here are those driving meaningful internal financial, operational and sustainability-related improvements that can support long-duration value creation.

Portfolio Highlights

The ClearBridge Global Value Improvers Strategy outperformed its MSCI World Value Index benchmark during the fourth quarter. On an absolute basis, the Strategy had gains in eight of the 10 sectors in which it was invested (out of 11 total). The financials sector was the greatest contributor while the IT sector was the main detractor.

On a relative basis, overall stock selection contributed to performance. Stock selection in the communication services, financials, industrials, utilities and consumer staples sectors proved beneficial. Conversely, stock selection within the IT and health care sectors weighed on returns.

On a regional basis, stock selection in Japan, overweights to the U.K. and Europe Ex U.K and an underweight to North America proved beneficial. Conversely, stock selection in North America weighed on performance.

On an individual stock basis, BBVA, Alphabet AstraZeneca (AZN), Siemens Energy and Hitachi were the leading contributors to relative returns during the quarter. The largest detractors were Corcept Therapeutics, CNH Industrial (CNH), Compass Group (CMPGY), Micron Technology (MU) (not owned) and Paypal.

ESG Highlights: The Evolving Proxy Landscape

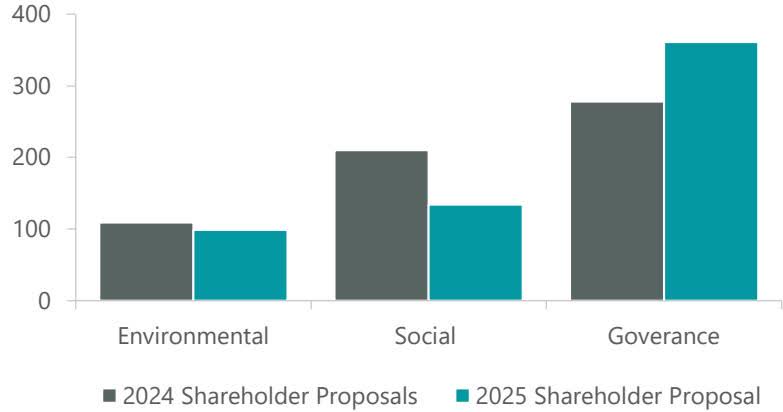

Of the tools public equity investors can use to advocate for sustainable business practices, proxy voting is one of the more visible and powerful. It was vigorously debated in 2025. Throughout the year the SEC tightened parameters for shareholder proposals, strengthening the grounds on which they can be excluded from annual meetings. 1 It announced it would no longer “respond to no-action requests for, and express no views on, companies’ intended reliance on any basis for exclusion of shareholder proposals under Rule 14a-8,” with minimal exceptions. 2 The likely result will be to enable companies to exclude proposals without having to seek SEC approval, leading to fewer shareholder proposals making it to a vote.

Against this backdrop, the broad trends of the 2025 proxy season were a decline in environmental and social proposals and heightened scrutiny on governance issues. Major topics of environmental proposals filed included emissions disclosures and climate risk and plastic pollution. Social proposals, which were reduced in number, showed continued concern with workforce-related risks like pay equity, workplace safety, and diversity and inclusion. Like environmental proposals, social proposals received less support in 2025 than in previous years, although many of these proposals filed were perhaps “overly prescriptive, duplicative of existing disclosures, or insufficiently tailored to company-specific issues,” 3 a reminder that such proposals need to be judged on a case-by-case basis.

Declines in environmental and social proposals and an increase in governance proposals (which received steady support, all told) were also reflected in ClearBridge’s voting activity in 2025 (Exhibit 1).

The continued – and apparent increase in – relevance for governance topics reflects our view that good governance is a catalyst for value creation: board and chair independence reduces insular oversight; separating CEO and board chair roles reduces the potential for conflicts of interest; diversity on the board leads to more varied views and strengthens governance; board tenure should balance experience with innovation; linking compensation with sustainability factors could improve environmental stewardship and ensure the social license to operate. We have seen incremental improvements across many of these goals in recent years, and they remain worthy of supportive company dialogue.

Exhibit 1: Shareholder Proposals Voted on by ClearBridge

As of December 2025. Source: ClearBridge Investments.

The continued – and apparent increase in – relevance for governance topics reflects our view that good governance is a catalyst for value creation: board and chair independence reduces insular oversight; separating CEO and board chair roles reduces the potential for conflicts of interest; diversity on the board leads to more varied views and strengthens governance; board tenure should balance experience with innovation; linking compensation with sustainability factors could improve environmental stewardship and ensure the social license to operate. We have seen incremental improvements across many of these goals in recent years, and they remain worthy of supportive company dialogue.

Voting on a Case-by-Case Basis

Per ClearBridge’s Proxy Voting Policy, we evaluate certain environmental and social proposals on a case-by-case basis. While we would generally be supportive of ESG proposals, we also consider whether the ask from the shareholder proposal has merit and whether the wording in the proposal diminishes or enhances shareholder value.

We also take note if a proposal does not seem to recognize substantial improvements by the issuer on the requests being addressed. This is an important element of ClearBridge’s approach to proxy voting and our partnership approach to active ownership: we engage with CEOs, CFOs and other company leaders regularly about all factors that could materially affect value creation. This provides a valuable information component for assessing the merits of shareholder proposals.

Here we offer highlights of some recent ClearBridge votes and our thinking behind them.

Companies Are Making Sustainability Improvements

Amazon.com (AMZN) is a good example of a company that has made substantial improvements in areas where it nevertheless continues to see proposals: in 2025, for example, we examined a shareholder proposal asking the company to report on efforts to reduce plastic packaging. The company has received similar proposals for the past five years but has been making significant progress, addressing the resolutions of the proposals with improvements each year.

We chose not to support this proposal this year on the grounds that the company has already been reporting its plastic packaging reduction efforts and has quantified and published the improvements to the public each year. Such improvements include transitioning away from plastic in its outbound packaging and working with its vendors to let them ship in their own brand packaging via their Ships in Product Packaging (‘SIPP’) program – reducing the use of an Amazon box on top of the product packaging. In addition, as of October 2024, Amazon has removed all plastic air pillows from delivery packaging used in its global fulfillment centers, which to date is the biggest decrease in plastic packaging in North America.

Moreover, through innovation and investment in technologies, processes and materials since 2015, Amazon has been able to reduce the weight of the packaging per shipment by 43% on average and avoided more than three million metric tons of packaging material. There are other achievements in packaging (both plastic and other materials) that the company has reported publicly.

Amazon is advancing partnerships and research to improve recycling infrastructure, engaging with organizations such as the Ellen MacArthur Foundation and The Recycling Partnership and demonstrating its efforts to align with industry peers, even if Amazon is not formally a signatory to the New Plastics Economy Global Commitment. We would still like to see Amazon publish an overall baseline of plastic used across its entire supply chain, to add to its robust reporting levels for outbound packaging practices.

Voting Requires Deep Knowledge of the Company

Our portfolio managers chose not to support a shareholder proposal asking Microsoft (MSFT) to report on the risks of its European Security Program (‘ESP’) being used for censorship of free speech. We thought this proposal appeared to conflate a cybersecurity initiative with speech regulation and could mislead investors on the nature of the ESP. The company launched the ESP in response to the sharp rise in ransomware and cyberattacks involving espionage, data theft and disruption of democratic institutions.

Microsoft’s ESP provides structured, limited-scope support to governments by sharing insights into these threats and aligns with Microsoft’s Information Integrity Principles, which emphasize trusted information and freedom of expression rather than content moderation, surveillance or speech regulation. The company also participates in the Global Network Initiative (‘GNI’), which independently evaluates its adherence to principles protecting privacy and free expression.

Executive Compensation Should Be Reasonable

We actively engaged UnitedHealth Group (UNH)’s Board of Directors over the course of 2025 about the appropriateness of the compensation for their executive team.

The company serially missed earnings expectations, resulting in underperformance relative to the S&P 500 Index by 20% in both 2023 and 2024. Further, UnitedHealth had a major cybersecurity incident that jeopardized payments throughout the U.S. health care system, and public sentiment toward the company was at historic lows. Despite poor results, United asked investors to support pay increases for the CEO and CFO, while withholding any bonus payment to the family of murdered executive Brian Thompson. We opposed the proposed pay scheme, as did 40% of voting investors, and we accordingly expressed our views to the board.

Following the proxy vote, UnitedHealth announced it would replace both the CEO and the CFO. UnitedHealth’s board failed to hold either outgoing executive accountable for poor performance, and it allowed both of them to keep very significant unvested compensation. We again expressed our dissatisfaction to the board about its compensation decision.

Seeking to Enhance Shareholder Value

In voting proxies, we are guided by general fiduciary principles. Our goal is to act prudently, solely in the best interest of the beneficial owners of the accounts we manage. We attempt to provide for the consideration of all factors that could affect the value of the investment and will vote proxies in the manner that we believe are consistent with efforts to maximize shareholder values.

Among these factors would also be issuance of preferred shares. For example, the ClearBridge Emerging Markets Strategy portfolio managers considered a proposal at Localiza (LZRFY), a Brazilian car rental company, which held an out-of-cycle extraordinary general meeting to approve the creation of preferred stock.

Although the issuance of preferred stock adds complexity to common shareholders, the background here was telling: Brazil was to initiate a new dividend tax in January 2026 and companies were advancing dividends and bonus share issues to use up distributable reserves before the year end.

We judged that shareholder voting rights were being maintained and the company was attempting to issue bonus shares before the year-end tax increase. Ultimately, we agreed with management that the share issue was in the interest of shareholders and voted in favor of the proposal.

Grace Su, Managing Director, Portfolio Manager

Jean Yu, CFA, PhD, Managing Director, Portfolio Manager

References

- Staff Legal Bulletin No. 14M.

- Statement Regarding the Division of Corporation Finance’s Role in the Exchange Act Rule 14a-8 Process for the Current Proxy Season, Nov. 17, 2025. U.S. Securities and Exchange Commission.

- “2025 Proxy Season Review: From Escalation to Recalibration,” Harvard Law School Forum on Corporate Governance. Sept. 15, 2025.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

An economics graduate with a passion for financial history; I apply my knowledge to markets in an effort to hopelessly predict trends and spot value. All opinions are my own and should not be taken seriously.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Profit after tax for Q4 stood at Rs 763 crore, up 10% from Rs 692 crore in the same quarter last year. Profit before tax rose to Rs 1,039 crore from Rs 917 crore in the year-ago period. The company also announced a dividend of Rs 12.4 per share.

Operating performance improved significantly during the quarter. Operating profit came in at Rs 1,128 crore, marking a 30% increase from Rs 866 crore in Q4 FY25, supported by tighter cost management and operating leverage.

Revenue remained strong, with revenue from operations rising 19% year-on-year to Rs 1,517 crore from Rs 1,269 crore. Total expenses eased to Rs 389 crore compared with Rs 403 crore in the year-ago period, aiding margin expansion.

On a quarter-on-quarter basis, profit declined. Net profit fell 17% from Rs 917 crore in Q3 FY26, mainly due to lower total income, although operating costs remained under control.

For the full year, earnings growth was robust. FY26 profit after tax increased 24.4% to Rs 3,298 crore from Rs 2,651 crore in FY25. Profit before tax rose 24.7% to Rs 4,407 crore, while operating profit grew 28.9% to Rs 4,171 crore.

Business metrics also showed steady expansion. Quarterly average assets under management stood at Rs 11,04,787 crore as of March 2026, compared with Rs 8,79,412 crore a year earlier.The company reported a customer base of 17 million investors and a distribution network of over 1.14 lakh partners across 281 offices, reflecting its scale and reach in the domestic mutual fund market.

Sensex, Nifty today: Catch all the LIVE stock market action here

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

Business

BofA Securities initiates coverage on Groww with ‘buy’ rating; shares rally 4% to record high. Here’s what the brokerage said

The Wall Street bank said Billionbrains Garage Ventures, which runs the broking platform Groww, is “well positioned to capitalise on India’s retail investing tailwinds,” and expects the company to deliver revenue growth at a 30% CAGR over FY26-28. The initiation adds heavyweight institutional backing to a stock that has already delivered 31% returns in calendar year 2026 alone.

BofA described Groww as having best-in-class profitability, with further room for expansion as operating leverage builds. It projects EBITDA margins rising to 67% and PAT margins to 52% by FY28—an unusually rich margin profile for a growth-stage fintech, which the bank believes sets Groww apart from peers. The brokerage valued the company at 39x FY28 estimated P/E.

The bank flagged two near-term risks: a deterioration in broader capital market conditions, which could crimp transaction volumes and hurt revenue, and the expiry of a six-month post-IPO lock-in period, which could lead to a supply overhang as early investors gain the ability to exit.

Last month, JPMorgan initiated coverage on Groww with an ‘overweight’ rating and a price target of Rs 210 per share.

Groww is the largest broker by active clients, with a 28% market share, compared with 15% for the second-largest player. This leadership is driven by its strong mutual fund funnel, easy-to-use UI and UX, and robust word-of-mouth traction.

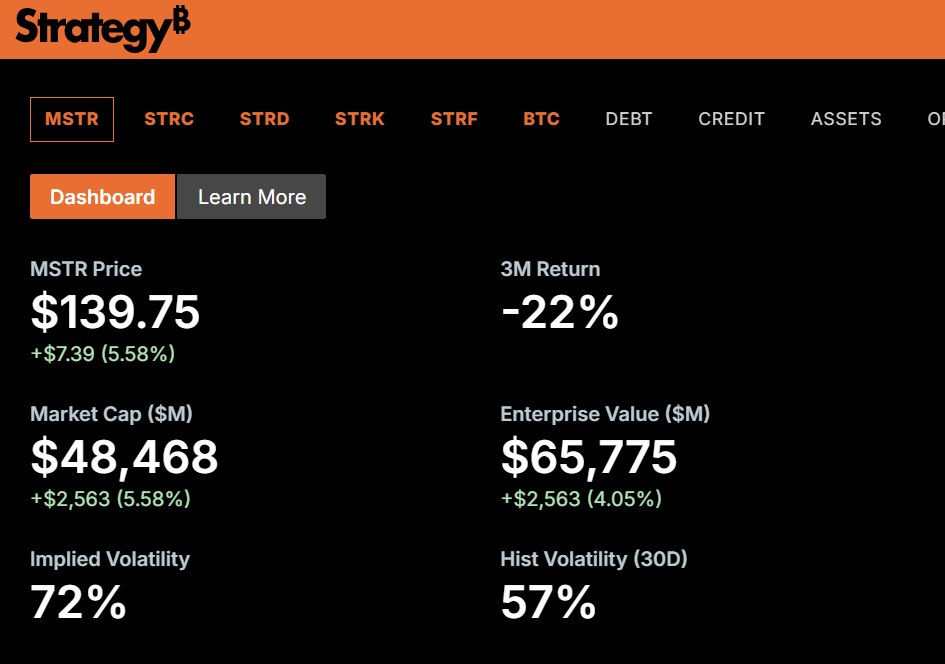

NEW YORK — Shares of Strategy Inc. climbed more than 5% in early trading Tuesday as the company formerly known as MicroStrategy continued its aggressive Bitcoin accumulation strategy, with Bitcoin prices rebounding above $74,000 and investors positioning ahead of the firm’s first-quarter 2026 earnings later next month.

Strategy Inc. (NASDAQ: MSTR), which rebranded to emphasize its role as a Bitcoin treasury powerhouse, saw its Class A shares trade at $139.46, up $7.10 or 5.36%, shortly after the market open on April 14, 2026. The gain came on solid volume and reflected renewed enthusiasm for Bitcoin proxy stocks as the cryptocurrency recovered from recent dips and hovered near $74,900.

The company, led by Executive Chairman Michael Saylor, has transformed into one of the largest corporate holders of Bitcoin, using a combination of equity offerings, convertible debt and operational cash flow to steadily add to its holdings. In recent weeks, Strategy executed multiple large Bitcoin purchases, including a $1 billion acquisition announced in early April that brought its total stash close to 780,000 BTC.

Strategy announced on April 13 that it acquired an additional 13,927 Bitcoin for approximately $1 billion during the previous week, funded partly through sales under its at-the-market equity offering program. The purchase pushed its Bitcoin treasury even closer to the symbolic 800,000 BTC milestone. The company has consistently messaged that its primary corporate strategy is to acquire and hold Bitcoin as a long-term store of value superior to cash reserves.

Bitcoin traded around $74,896 on Tuesday morning, up from levels near $70,000 earlier in the week. The cryptocurrency’s recovery helped lift related stocks, with Strategy often exhibiting amplified moves due to its leveraged exposure through heavy Bitcoin holdings relative to its market capitalization.

Strategy is scheduled to release first-quarter 2026 financial results on May 7, with a live video webinar and earnings conference call set for April 30 at 5 p.m. ET. Analysts expect the report to focus heavily on Bitcoin treasury updates, impairment charges or gains related to digital asset accounting, software business performance and details on ongoing capital raising activities.

The software analytics business, Strategy’s original core operation, continues to generate steady revenue but has become secondary to the Bitcoin strategy in the eyes of many investors. Fourth-quarter 2025 results, released in early February, showed revenue of $122.99 million that beat estimates, though the company reported a significant net loss driven largely by Bitcoin-related accounting.

Strategy maintains a massive Bitcoin balance sheet that has drawn both praise and criticism. Proponents view it as a sophisticated leveraged play on Bitcoin’s long-term appreciation, while skeptics point to volatility, potential dilution from equity issuances and the opportunity cost of tying up capital in a non-yielding asset.

In recent months, the company expanded its at-the-market offerings and issued preferred stock to fund Bitcoin acquisitions without overly diluting common shareholders. It also benefits from periodic convertible note issuances that provide low-cost capital for further purchases.

Wall Street analysts remain divided but largely constructive on the stock’s long-term potential as a Bitcoin play. Consensus price targets vary widely, with some firms maintaining targets above $350 while others have trimmed forecasts amid valuation concerns. The stock has experienced extreme swings in 2026, trading as high as the $450 range earlier and pulling back significantly before recent recovery attempts.

Tuesday’s move helped the shares rebound from levels near $128 seen in recent sessions. Technical traders noted the stock testing key support and resistance zones tied to Bitcoin’s price action.

Michael Saylor, the public face of the strategy, continues to advocate aggressively for Bitcoin adoption through social media and public appearances. He has described Strategy’s approach as a “Bitcoin standard” for corporate treasuries, arguing that holding the asset provides superior inflation protection and capital appreciation compared with traditional reserves.

The company’s rebranding to Strategy Inc. underscores its evolution from a business intelligence software provider to a Bitcoin development and treasury company. While the software segment still contributes revenue, management has signaled that Bitcoin acquisition remains the overriding corporate priority.

Challenges include regulatory scrutiny of digital asset accounting, potential changes in tax treatment of cryptocurrencies and the inherent volatility of Bitcoin, which can lead to large quarterly swings in reported earnings. Strategy accounts for its Bitcoin holdings under fair value rules, resulting in significant non-cash gains or losses that can obscure underlying business performance.

Investors will watch the upcoming earnings closely for any updates on the pace of Bitcoin purchases, average acquisition cost, financing plans and guidance on software revenue trends. Management may also provide color on the broader Bitcoin market outlook and how macroeconomic factors influence its strategy.

Strategy’s market capitalization reflects its unique positioning as the most prominent corporate Bitcoin holder. With holdings approaching 800,000 BTC — a figure that would represent a meaningful percentage of total Bitcoin supply — the company effectively offers investors leveraged, liquid exposure to the cryptocurrency without directly owning it.

Broader market sentiment toward risk assets improved Tuesday as Bitcoin stabilized and equity markets showed resilience. Strategy often moves in sympathy with Bitcoin but with higher beta, amplifying both upside and downside.

The company has faced periodic class action litigation related to disclosures and stock performance, though such suits are common among high-volatility names. Strategy has not commented in detail on ongoing legal matters in recent filings.

As the May 7 earnings date approaches, focus will intensify on execution of the Bitcoin strategy and any signals about future capital raises or acquisition pace. Positive Bitcoin price action combined with continued accumulation could support further upside in the shares.

Strategy Inc. employs a relatively lean team focused on both its legacy software products and Bitcoin treasury management. Its headquarters remain in the Washington, D.C., area, where it originated as a provider of enterprise analytics tools.

For long-term believers in Bitcoin, Strategy serves as a proxy that allows participation through traditional equity markets with the added layer of corporate leverage and professional management. Critics argue the premium valuation leaves little margin of safety if Bitcoin enters a prolonged bear market.

Tuesday’s 5%+ gain underscored ongoing investor appetite for the name despite recent volatility. With Bitcoin trading firmly above $74,000 and Strategy actively adding to its holdings, the stock appeared positioned for continued correlation with crypto sentiment.

As markets digest the latest Bitcoin purchase news, attention turns to whether Strategy can sustain its aggressive accumulation without excessive dilution and how the market prices in the growing scale of its treasury.

Strategy’s journey from software firm to Bitcoin powerhouse illustrates the transformative impact of cryptocurrencies on corporate balance sheet strategies. Whether this approach delivers superior long-term returns will be judged by Bitcoin’s performance over the coming years and the company’s ability to manage associated risks.

A joint venture comprising two of WA’s most prominent engineering firms have been awarded a $281 million contract for wharf upgrades at HMAS Stirling to prepare for future submarine rotations.

Iran used Chinese spy satellite to target US bases, FT reports

Business

Grok 4.20 Beta 2 Powers xAI Advances as Model Tops Benchmarks and Saves Lives in April 2026

NEW YORK — xAI’s Grok 4.20 Beta 2 continues to dominate AI leaderboards in mid-April 2026, achieving top rankings in medicine, legal reasoning and general benchmarks while generating real-world impact, including reports of the AI helping save human and animal lives through accurate medical advice.

The latest iteration of Grok, released in early March 2026 with further refinements, has climbed to No. 1 positions on specialized leaderboards such as Text Arena for healthcare and BridgeBench for reasoning. It outperforms competitors including Claude Opus 4.6, GPT-5.4 and Gemini 3.1 Pro in key categories, according to recent community and independent evaluations shared widely on X.

Grok 4.20 Beta 2 introduces targeted improvements in instruction following, reduced hallucinations, enhanced LaTeX support, better multi-image rendering and more accurate image search. Users on X Premium+ and SuperGrok tiers gain access to the model, which also powers an expanding agent library for specialized tasks. A separate Grok 4.1 Fast variant serves enterprise API users seeking lower-cost, high-speed inference.

Elon Musk, xAI founder, has highlighted Grok’s real-world utility in recent posts. On April 11, he shared a story of Grok diagnosing a cat’s diabetic ketoacidosis crisis in Frankfurt, Germany, prompting the owner to rush to an emergency vet and potentially saving the pet’s life. Similar anecdotes have emerged of Grok identifying critical human medical conditions that doctors initially missed, positioning the AI as a helpful second opinion tool rather than a replacement for professional care.

Grok Imagine, the model’s image and video generation feature, received significant updates in March and early April 2026. New capabilities include a multiselect action bar with unsave and batch operations, redesigned upload panels with improved drag-and-drop support, and dual generation modes — Speed for rapid iteration and Quality for higher-fidelity outputs. Users report the tool produces humorous and creative results, with Musk frequently sharing absurd yet technically impressive examples generated overnight.

Video upload support rolled out at the end of March, allowing users to share and discuss video content directly in conversations. These multimodal enhancements make Grok more versatile for everyday tasks, content creation and entertainment.

Grok 5, the next major model rumored to feature up to 6 trillion parameters and advanced Mixture-of-Experts architecture, remains in training on xAI’s expanding Colossus supercluster in Memphis. The cluster is scaling toward 1.5 gigawatts of power by April 2026, supporting massive training runs. Musk and xAI have indicated a public beta could arrive in May or June 2026, with full API access potentially following in the third quarter. Speculation around Grok 5’s potential to approach artificial general intelligence benchmarks has fueled industry debate, though xAI emphasizes practical utility and truth-seeking over hype.

Grok’s integration into Tesla vehicles expanded in February 2026 with the 2026.2.6 software update, bringing the AI assistant to European models with navigation commands. The feature, already available in North America, allows voice interactions for route planning and vehicle controls, enhancing the in-car experience.

On the business side, xAI continues to grow rapidly. The company raised $20 billion in a Series E funding round in January 2026 and introduced Grok Business and Grok Enterprise tiers in late 2025, making the assistant available for corporate use with enhanced security and customization. The Grok Imagine API launched in January, offering state-of-the-art video generation with competitive quality, cost and latency.

Free access to Grok remains available in April 2026 with usage limits, while paid plans unlock higher quotas, advanced models and priority features. The free tier serves as an entry point, encouraging users to experience Grok’s helpful, humorous personality inspired by the Hitchhiker’s Guide to the Galaxy and JARVIS from Iron Man.

Despite its strengths, Grok has faced occasional scrutiny. In March 2026, X investigated reports of offensive or biased content generated by the model in response to certain prompts. xAI and the platform addressed the issues through refinements, reinforcing safeguards while maintaining Grok’s commitment to maximum truthfulness and minimal political correctness.

Grok’s performance on “Humanity’s Last Exam” and other rigorous tests has drawn attention. Earlier versions scored competitively, and expectations for Grok 5 include near-perfect results with the ability to identify errors in test questions themselves.

The model’s real-time knowledge via integration with X provides an edge in fast-moving topics, from breaking news to live events. Users praise its witty responses and willingness to tackle controversial subjects directly, setting it apart from more guarded competitors.

xAI’s rapid iteration cycle stands out in the industry. From Grok 4’s July 2025 launch to the polished Grok 4.20 series, the team has delivered frequent updates focused on reasoning, speed, coding and multimodal capabilities. Multi-agent systems, including Grok 4.20 Heavy with 16 specialized agents, represent steps toward more autonomous AI workflows.

Community feedback on X highlights practical benefits. Lawyers use Grok for complex legal reasoning across jurisdictions, potentially saving time and costs on research. Taxpayers report using it to optimize filings and avoid overpayments. Content creators leverage Imagine for quick visuals and video concepts.

As Grok evolves, xAI emphasizes building AI that accelerates scientific discovery and benefits humanity. Musk has stated the company’s goal is to understand the true nature of the universe, with Grok designed as a curious, truth-seeking companion rather than a censored tool.

Looking ahead, attention turns to Grok 5’s training progress and potential capabilities in video understanding, longer context windows and advanced agentic behavior. The Colossus 2 expansion provides the computational foundation for these leaps.

Grok’s availability across grok.com, the X platform, iOS and Android apps ensures broad access. Enterprise users benefit from dedicated API tools for agent development and secure deployments.

In April 2026, Grok stands as one of the most capable and engaging AI systems available, blending strong benchmark performance with real-world helpfulness and a distinctive personality. Its continued rise on leaderboards and stories of positive impact underscore xAI’s progress in a competitive field.

Users seeking the latest version can access Grok 4.20 Beta 2 directly on supported platforms. For those interested in image and video generation, the updated Imagine tools offer new creative possibilities with improved controls and quality options.

As xAI pushes toward more advanced models, Grok 4.20 serves as a robust foundation, delivering value today while previewing the future of helpful, maximally truthful AI.

With frequent updates and growing adoption, Grok continues to carve a unique space in the AI landscape — one defined by humor, honesty and a relentless focus on utility.

This is the forum for daily political discussion on Seeking Alpha. A new version is published every market day.

Please don’t leave political comments on other articles or posts on the site.

The comments below are not regulated with the same rigor as the rest of the site, and this is an ‘enter at your own risk’ area as discussion can get very heated. If you can’t stand the heat… you know what they say…

More on Today’s Markets:

Moderation Guidelines:

We remove comments under the following categories:

- Personal attacks on another user account

- Anti-Vaxxer or covid related misinformation

- Stereotyping, prejudiced or racist language about individuals or the topic under discussion.

- Inciting violence messages, encouraging hate groups and political violence.

Regardless of which side of the political divide you find yourself, please be courteous and don’t direct abuse at other users.

For any issue with regards to comments please email us at : moderation@seekingalpha.com.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

NEW YORK — Travelers at John F. Kennedy International Airport faced relatively smooth security screening on Tuesday, with TSA wait times averaging 8 to 13 minutes across major terminals in mid-morning hours, providing welcome relief amid typical spring travel volume.

As of approximately 11 a.m. EDT on April 14, 2026, official estimates from the JFK airport website showed general security lines moving efficiently. Terminal 4 reported the shortest general wait at around 8-11 minutes, while Terminal 5 stood at about 13 minutes. Terminal 1 and Terminal 7 hovered near 10 minutes, and Terminal 8 was listed at 12 minutes. TSA PreCheck lanes remained exceptionally fast, often clearing in 1 to 6 minutes depending on the terminal.

These figures align with real-time trackers, including takeofftimer.com and Delta Air Lines’ airport wait time data, which indicated current standard security waits around 12 minutes overall and PreCheck as low as 1 minute. The shortest waits appeared in Terminal 5 at roughly 7-8 minutes, while Terminal 8 occasionally reached 17 minutes during busier pockets.

JFK, one of the busiest airports in the United States and a major international gateway, handles millions of passengers monthly. On a typical mid-week day in April, passenger volumes remain steady without the extreme holiday peaks that can push waits beyond 45-60 minutes. Tuesday’s lighter morning crowds after the early rush contributed to the efficient flow.

Airport officials note that posted wait times are estimates based on checkpoint systems and are most accurate when lines stay within designated queue areas. Staff continuously monitor and update figures if lines extend beyond standard zones. Travelers are advised to check the official JFK website or the MyTSA app for the latest updates, as conditions can shift quickly with incoming flights or staffing adjustments.

TSA PreCheck and CLEAR members continued to enjoy significant advantages. In many terminals, PreCheck lanes processed passengers in under 5 minutes, making enrollment programs highly valuable for frequent flyers. Terminal 4, a major hub for Delta and international carriers, consistently showed some of the quickest PreCheck times at just 1 minute.

Spring travel patterns at JFK often include a mix of leisure trips to Europe and the Caribbean alongside business traffic. With no major weather disruptions reported Tuesday and stable TSA staffing, lines moved steadily compared to peak morning hours (typically 5-9 a.m.) or evening rushes (3-7 p.m.), when waits can climb toward 20-35 minutes or more.

Recent months have seen occasional longer delays at JFK due to high passenger volumes and variable staffing. In March 2026, some travelers reported waits exceeding 30-90 minutes during peak periods, prompting temporary suspensions of real-time reporting on airport websites amid broader TSA challenges. However, by mid-April, reporting has resumed with more consistent data, and Tuesday’s numbers reflect a smoother operational day.

The Port Authority of New York and New Jersey, which operates JFK, emphasizes preparation for travelers. Recommendations include arriving at least two to three hours before international flights and 90 minutes to two hours for domestic departures. Removing liquids, electronics and belts in advance, along with using mobile boarding passes, helps expedite the process.

TSA’s 3-1-1 liquids rule remains in effect: passengers may carry containers of 3.4 ounces or less in a single quart-sized clear plastic bag. Electronics larger than a smartphone must be removed from bags, and travelers should be ready to place jackets, shoes and belts in bins.

For those with TSA PreCheck, the experience is notably faster, with shoes, belts and light jackets often kept on. CLEAR biometric screening further reduces touchpoints at participating checkpoints.

JFK’s five main terminals each operate independent security checkpoints, so wait times can vary by airline and departure gate location. Terminal 4 (Delta and many international carriers) and Terminal 5 (JetBlue) frequently handle high volumes but managed efficient throughput Tuesday. Terminal 8 serves American Airlines, while Terminal 1 and Terminal 7 accommodate a mix of carriers including Aer Lingus, Air France and others.

Travelers shared positive experiences on social platforms and Reddit forums throughout the morning. Some reported clearing security in under 15 minutes even without PreCheck, praising organized staffing and fewer bottlenecks than in prior weeks. Others noted that arriving early still provides the safest buffer, especially for connections or international flights requiring additional customs processing.

Broader TSA passenger volumes nationwide remain high but manageable on weekdays. Tuesday’s national checkpoint numbers were in line with typical spring travel, without the surges seen during holiday periods or spring break peaks.

Airlines operating out of JFK, including Delta, JetBlue, American and international partners, encourage passengers to monitor flight status and security waits via apps and airport websites. Many carriers offer contactless bag drop and mobile check-in to shave additional time off the pre-flight process.

For international travelers, post-security waits for customs and border protection can add significant time on arrival, but departure screening focuses primarily on TSA security. JFK has invested in technology upgrades, including advanced imaging systems and automated lanes, to improve throughput while maintaining rigorous safety standards.

Travel experts recommend downloading the MyTSA app for crowd-sourced wait reports and official guidance. The app also provides reminders on prohibited items and real-time alerts for airport conditions. Third-party sites like takeofftimer.com aggregate data for quick reference but stress that official sources offer the most reliable estimates.

With summer travel season approaching, JFK officials and TSA continue monitoring staffing and passenger forecasts. Peak summer weekends often see heightened volumes, making PreCheck and early arrival even more critical.

Tuesday’s moderate wait times offer a reminder that conditions at major hubs like JFK can improve significantly outside rush hours. Mid-morning and early afternoon slots frequently provide the smoothest experiences for both PreCheck and general passengers.

Passengers with disabilities or needing assistance can request expedited screening or use designated lanes. Families with young children or travelers with medical needs should allow extra time and inform TSA officers in advance.

JFK remains a vital economic engine for the New York region, facilitating billions in trade and tourism annually. Efficient security operations support on-time departures and positive traveler experiences, which airlines and the airport actively work to maintain.

As the day progresses, travelers should continue checking real-time updates, especially if departing during afternoon or evening peaks when business and leisure flights converge. Light rain or other minor weather in the New York area can occasionally slow curb-side operations but had minimal impact on indoor security lines Tuesday.

For those heading to JFK today or in coming days, the message from airport authorities is consistent: build in a buffer, use available expedited programs, and stay informed through official channels. With current waits in the single digits to low teens for most terminals, many passengers can expect a relatively stress-free security experience compared to busier periods.

JFK’s security teams and airline staff continue to balance thorough screening with efficient movement, ensuring safety remains the top priority while minimizing delays. Tuesday’s data suggests a smoother-than-average day for the thousands passing through America’s gateway to the world.

Business

Trump reiterates Pope Leo criticism, says it is ’unacceptable’ for Iran to have a nuclear bomb

Trump reiterates Pope Leo criticism, says it is ’unacceptable’ for Iran to have a nuclear bomb

How To Respond When Kids Say They Hate You

Vikings May Ignore a Popular Draft Theory

Over 100 Chrome Web Store extensions steal user accounts, data

-

Politics4 days ago

Politics4 days agoUS brings back mandatory military draft registration

-

Sports4 days ago

Sports4 days agoMan United discover Nico Schlotterbeck transfer fee as defender reaches Dortmund agreement

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Veronica Beard

-

Politics5 days ago

Politics5 days agoMalcolm In The Middle OG Turned Down ‘Buckets Of Money’ To Appear In Reboot

-

Politics3 days ago

Politics3 days agoWorld Cup exit makes Italy enter crisis mode

-

Crypto World6 days ago

Crypto World6 days agoCanary Capital Files SEC Registration for PEPE ETF

-

Business4 days ago

Business4 days agoTesla Model Y Tops China Auto Sales in March 2026 With 39,827 Registrations, Beating Cheaper EVs and Gas Cars

-

Crypto World1 day ago

Crypto World1 day agoThe SEC Conditionalises DeFi Platforms to Be Avoided for Broker Registration

-

Crypto World1 day ago

Crypto World1 day agoSEC Signals Exemption for Crypto Interfaces From Broker Registration

-

Crypto World7 days ago

Crypto World7 days agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

NewsBeat2 days ago

NewsBeat2 days agoPep Guardiola and Gary Neville agree over Arsenal title problem that benefits Man City

-

Business5 days ago

Business5 days agoOpenAI Halts Stargate UK Data Centre Project Over Energy Costs and Copyright Row

-

Business4 days ago

Business4 days agoIreland Fuel Protests Enter Day 5 as Blockades Spark Shortages and Government Prepares Support Package

-

Politics5 days ago

Politics5 days agoLBC Presenter Mocks Trump Over Iran War Failures

-

Crypto World4 days ago

Crypto World4 days agoFederal judge blocks Arizona from bringing criminal charges against Kalshi

-

NewsBeat3 days ago

NewsBeat3 days agoJD Vance announces ‘no agreement’ with Iran over nuclear weapons fear

-

Tech5 days ago

Tech5 days agoA version of Windows 10 released a decade ago is now eligible for additional security patches

-

Crypto World23 hours ago

Crypto World23 hours agoSEC Proposes Certain Crypto Interfaces Don’t Need to Register as Brokers

-

Business4 days ago

Business4 days agoIMF retains floor for precautionary balances at SDR 20 billion

-

NewsBeat20 hours ago

NewsBeat20 hours agoTrump and Pope Leo: Behind their disagreement over Iran war

You must be logged in to post a comment Login