Crypto World

Fed to hike? When traders see a rate increase coming

The Federal Reserve logo is seen on the William McChesney Martin Jr. Building in Washington, Sept. 16, 2025.

Kevin Dietsch | Getty Images

While President Donald Trump made his pick for chair of the Federal Reserve with interest rate cuts in mind, his appointee may preside over the first rate hikes since 2023.

That’s according to traders on prediction market platform Kalshi, where there’s a rising likelihood the Fed will move to increase rates in the next year.

Traders place 64% odds on the next interest rate hike coming by July 2027. They also think there’s a 43% chance tighter policy happens as soon as this year.

Odds of a rate hike have jumped in the last 24 hours in reaction to ballooning yields on U.S. Treasurys, concern that inflation will continue to march higher and as oil prices show no signs of materially falling in the midst of the unresolved Iran war. Traders previously assigned just 50-50 odds that a rate hike would come in the first half of 2027.

Incoming Federal Reserve Chair Kevin Warsh during a Senate Banking, Housing, and Urban Affairs Committee confirmation hearing in Washington, April 21, 2026.

Graeme Sloan | Bloomberg | Getty Images

“Who’s actually in the monetary-policy driver’s seat? We’d argue that it’s the Bond Vigilantes,” Yardeni wrote.

But Wolfe Research chief investment strategist Chris Senyek in a Tuesday note said the moves in the bond markets might force a resolution to the war in the Middle East, potentially easing inflation pressures.

“We believe the U.S. Treasury market has been signaling persistent inflation and this week was the final straw,” he said. “Our sense is that there is potential for bond vigilantes to push yields higher in [an] attempt to push the Trump Administration to come to a quick resolution on Iran.”

Traders on Polymarket assign 35% odds that there is a rate hike in 2026.

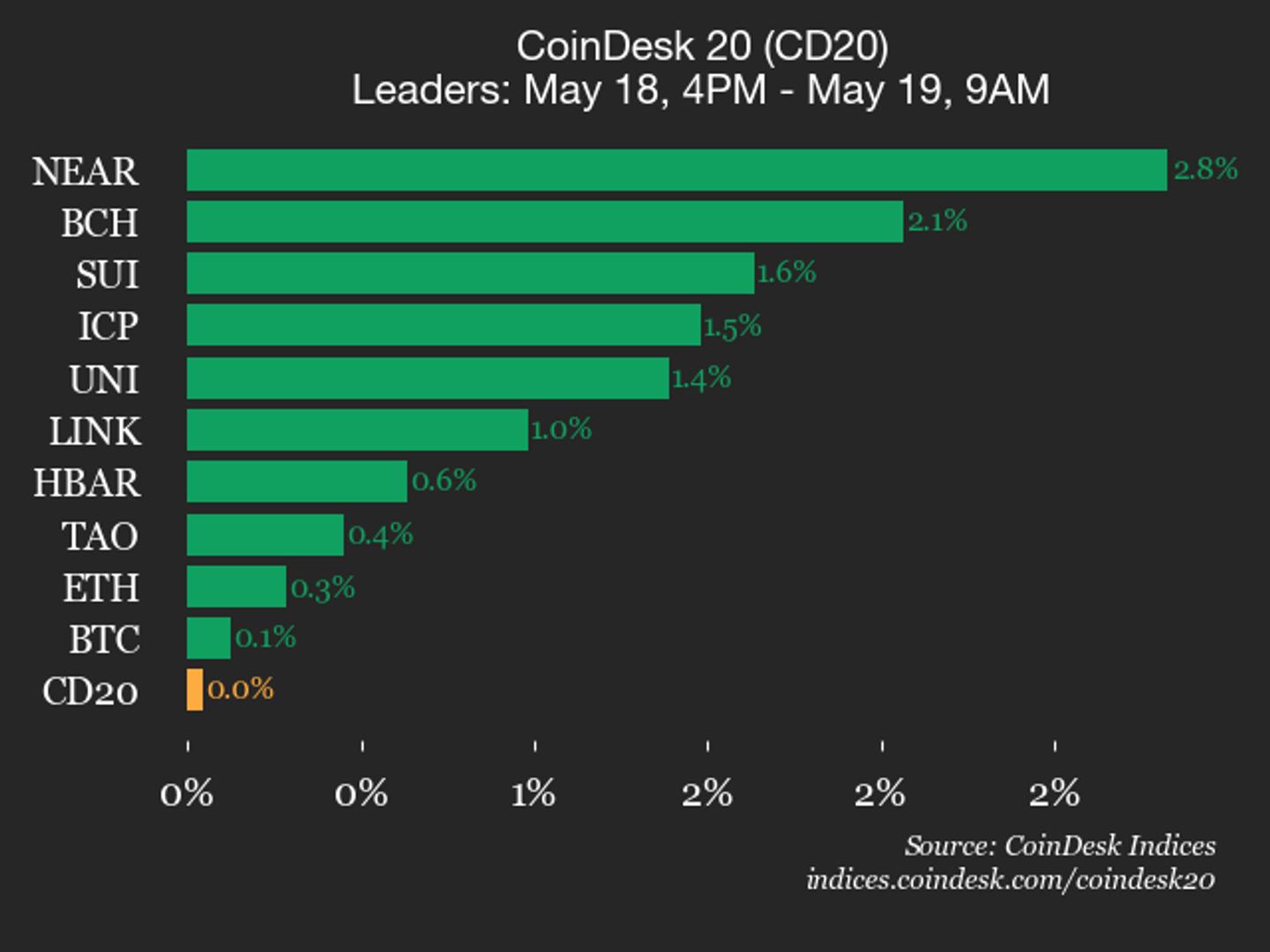

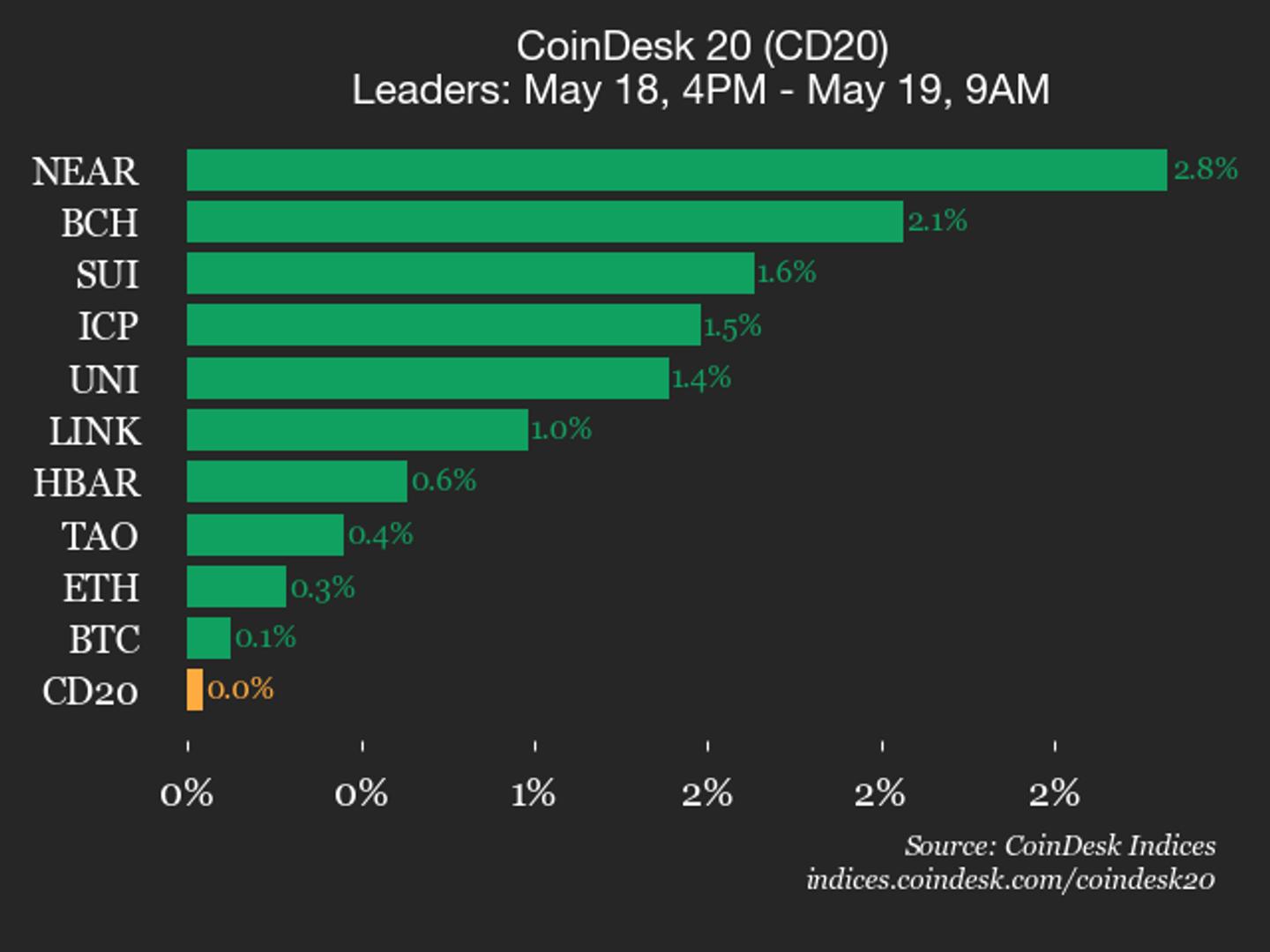

NEAR Protocol (NEAR), up 2.8%, was also a top performer.

TLDR

- The CFTC and the DOJ filed a lawsuit against Minnesota shortly after the state approved a ban on prediction markets.

- Federal regulators argue that prediction markets fall under their exclusive jurisdiction as regulated derivatives products.

- The complaint states that Minnesota’s law unlawfully interferes with federally approved trading platforms.

- The state law bans platforms that allow users to bet on events such as sports outcomes and economic trends.

- The statute also extends liability to banks, media firms, and data providers linked to these platforms.

Federal regulators moved quickly after Minnesota enacted a law banning prediction markets across the state. The Commodity Futures Trading Commission and the Department of Justice filed a lawsuit within one day. They argue that the state law interferes with federally regulated derivatives markets.

Federal lawsuit challenges Minnesota Authority Over Prediction Markets

The CFTC and DOJ filed the complaint against Minnesota and Governor Tim Walz in federal court. They claim the state law violates the agency’s exclusive jurisdiction over derivatives trading and regulated contracts.

Officials stated that prediction markets operate as federally approved financial instruments under existing law.

The complaint reads, “This flagrant and unprecedented incursion must be preliminarily and permanently enjoined.”

The agencies explained that the law classifies prediction markets as illegal gambling within Minnesota borders. However, federal regulators maintain that these platforms trade event-based contracts under national oversight rules.

They also stressed that exchanges offering these contracts must comply with federal standards. Therefore, the agencies argue that state-level bans disrupt a uniform regulatory system.

State Law Targets Platforms and Related Financial Services

Minnesota’s new statute prohibits platforms that allow users to wager on future events and outcomes. The law covers predictions involving sports, weather, economic indicators, and political developments.

The statute also extends liability to banks, payment processors, and media organizations connected to these platforms. It includes entities that advertise, verify, or supply data used by prediction market operators.

The complaint highlights partnerships between prediction platforms and major organizations. These include sports leagues, media companies, and financial data providers that support market activity.

Regulators argue that penalizing these partners creates broader enforcement risks beyond trading platforms. They maintain that federal law already governs these activities under established financial regulations.

Broader Dispute Expands Across Multiple U.S. States

The lawsuit forms part of a wider conflict between federal regulators and state authorities over market classification. Several states have attempted to restrict prediction platforms using local gambling laws.

The CFTC has taken legal action against states such as Illinois, Arizona, and Connecticut in similar disputes. These cases focus on whether states can override federal authority in regulating derivative products.

Meanwhile, Minnesota has introduced mixed policies toward crypto and related services in recent months. Governor Walz approved legislation allowing banks and credit unions to provide crypto custody services.

Earlier this year, the state also banned crypto ATMs, citing concerns about fraud and scams. The new prediction market ban will take effect on Aug. 1, according to the statute.

Crypto World

JPMorgan says ether and altcoins won't catch up to bitcoin without a major network boom

The bank said ether and the broader altcoin market continue to trail bitcoin as weak network activity, sluggish DeFi growth and limited real-world adoption weigh on investor demand.

Crypto firms are pausing long-awaited IPO plans as weak trading volumes and macro pressures weigh on valuations despite boom in AI-linked tech listings.

Key takeaways:

- Solana perpetual futures funding rates flipped negative, signaling excess demand for bearish positions.

- Rival networks like Base and Hyperliquid pose direct threats to Solana by aggressively capturing DEX market volume.

Solana’s native token SOL (SOL) faced a 15% correction following a rejection at $98 on May 11. A retest of the $83 level on Tuesday was followed by negative futures funding rates, indicating increased demand for short SOL positions.

While declining network activity contributed to the price drop, competition among rival blockchain networks has picked up.

SOL perpetual futures annualized funding rate. Source: Laevitas

The SOL perpetual futures funding rate stood at -3% on Tuesday, down considerably from the +8% on Saturday. During neutral market conditions, this indicator hovers near +9% to account for the cost of capital and exchange risk. Demand for bullish leverage has been largely absent since Saturday, when SOL price slipped below $90.

Solana DEX activity has declined by 56% since January

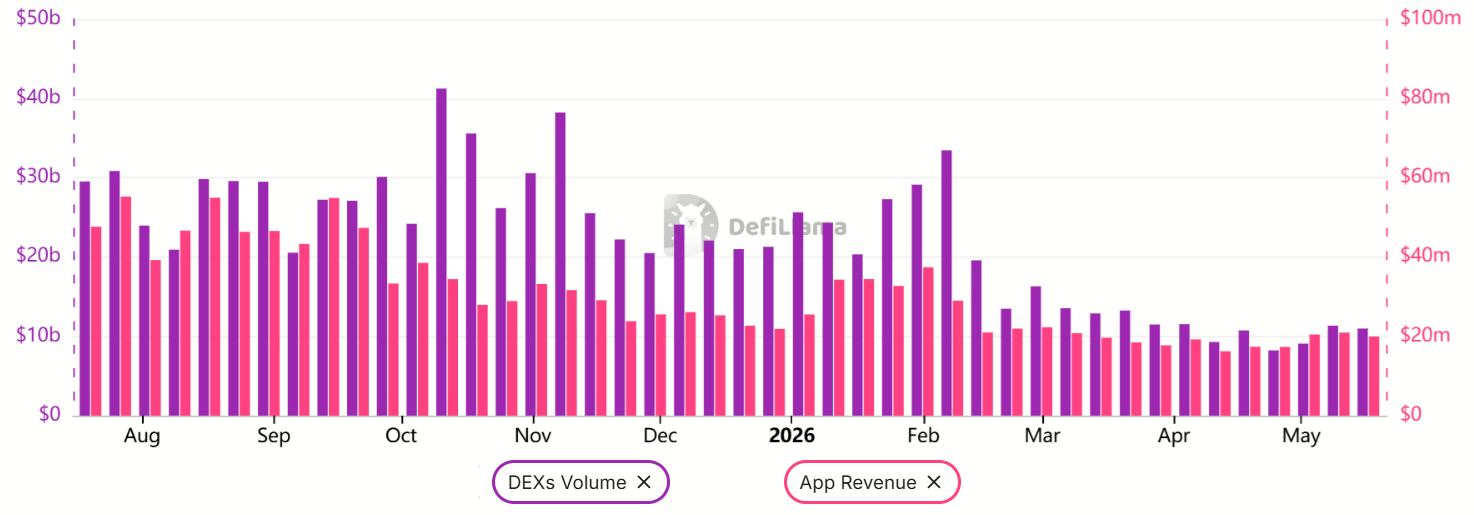

Declining activity on Solana’s decentralized exchanges (DEXs) has reduced ecosystem revenue and demand for SOL. This reduced appetite for decentralized applications (DApps) was not exclusive to Solana, but growing competition poses a major threat, as investors fear that demand for memecoins has faded for good.

Solana weekly DEX volumes, DApps revenue, USD. Source: DefiLlama

Solana DApp revenue stabilized near $20 million per week, down from an average of $35 million in January. This movement closely mirrors the network’s DEX activity trend, which currently stands at $11 billion per week, compared to January’s average of $25 billion. The 30-day DApp revenue leaders on Solana are Pump, Axiom Pro, Phantom, and Jupiter, which command a combined 65% market share.

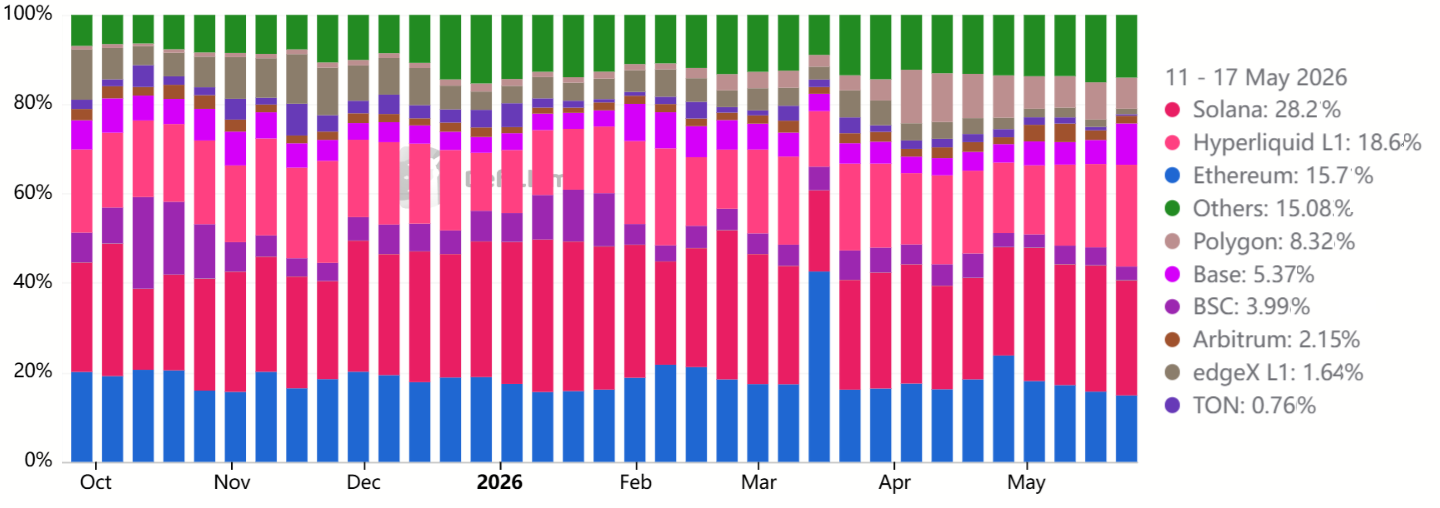

Blockchain ranked by weekly DApps revenue market share. Source: DefiLlama

Solana remained the top blockchain for DApp revenue despite intensifying competition. Hyperliquid created a direct threat due to its dominance in perpetual contracts, offering a high-throughput solution with core trading features built directly into the consensus layer. Meanwhile, the Ethereum layer-2 network Base offered seamless integration into the Coinbase ecosystem.

In terms of total value locked (TVL), Solana secured second place with $5.9 billion, followed by BNB Chain at $5.5 billion and Base at $4.5 billion. DEX platforms and staking DApps like Jupiter, Kamino, Sanctum, and Raydium lead Solana’s TVL. Still, no blockchain threatens Ethereum’s $43.2 billion TVL, which relies heavily on collateralized lending and liquid staking.

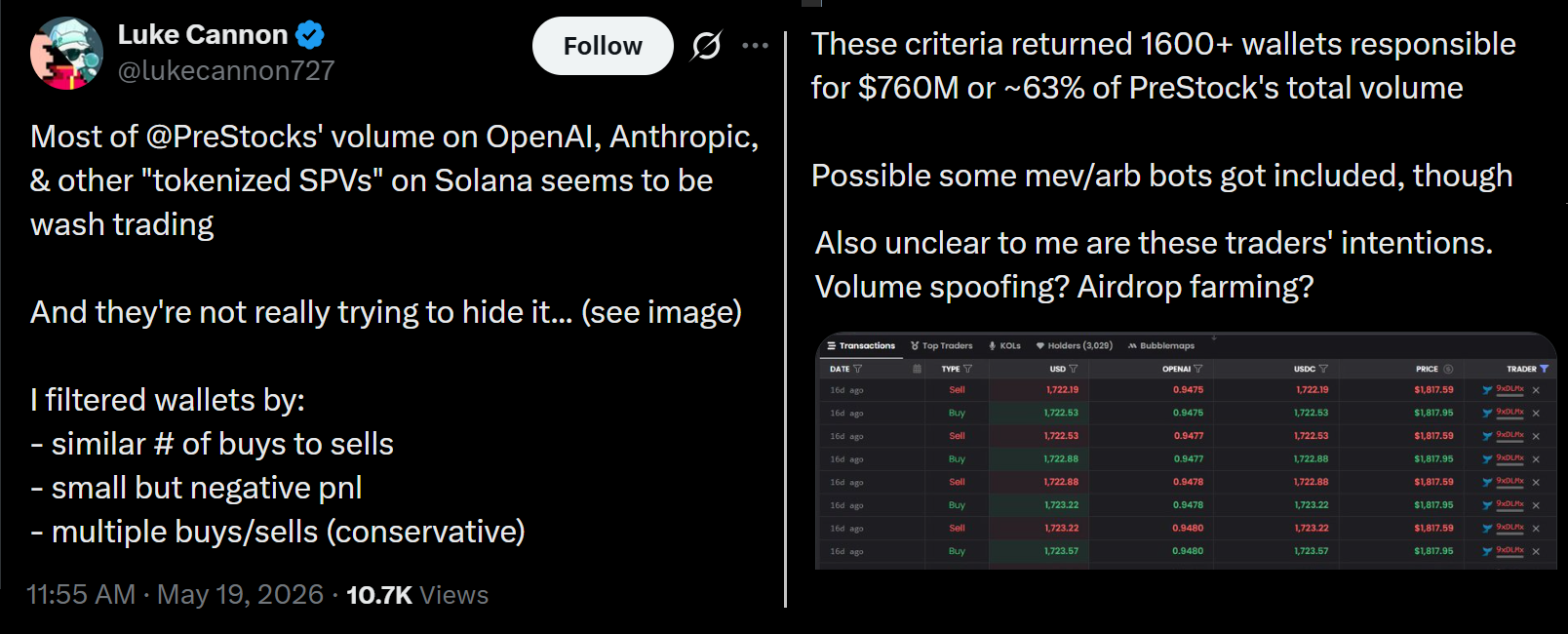

Potential spoofing activity on Solana network DApps

Solana’s footprint in the DApp industry cannot be understated, but the network’s low fees offer a perfect opportunity for maximal extractable value (MEV) botting and inflated activity.

Related: Goldman Sachs exits XRP, Solana ETF exposure in Q1 2026

Source: X/lukecannon727

X user lukecannon727 noted that 1,600 addresses were reportedly responsible for nearly 63% of volumes on PreStocks, a synthetic asset trading platform that runs on the Solana network. According to the analysis, those entities presented balanced trading activity, high execution frequency, and small net losses. These findings are highly consistent with arbitrage activity, but they could also indicate volume spoofing.

Recent weakness in SOL prices can be partially attributed to the broader decline in DApp demand and increased competition, especially from Hyperliquid and Base. An eventual bull run seems highly dependent on a pickup in DEX activity, particularly in memecoin trading. But, at the same time, there is no indication that SOL should retest the $78 level last seen in early April.

Crypto World

Polymarket unlocks $5 trillion private market for retail traders, previously reserved for elites

Polymarket’s new private-company prediction markets let retail traders bet on startup milestones once reserved for Wall Street insiders.

The U.S. Commodity Futures Trading Commission (CFTC) has moved to block Minnesota’s new restriction on prediction markets, filing a lawsuit in the District of Minnesota that challenges Senate File (SF) 4760 as an overreach of state authority. The suit centers on the state’s prohibition of advertising, creating, operating, or otherwise facilitating prediction-market platforms, with a specific focus on event contracts tied to sporting events, military conflicts, and weather—essentially banning platforms such as Kalshi and Polymarket from listing these products within Minnesota’s borders.

In its filing, the CFTC argues that Minnesota’s law conflicts with federal regulation of derivatives and event contracts under the Commodity Exchange Act (CEA), asserting exclusive federal jurisdiction over such products. The agency seeks to block the Minnesota statute on both preliminary and permanent grounds, asserting that Minnesota’s law would criminalize exchanges the CFTC has approved and event contracts that have been self-certified to the Commission. The filing frames the state action as prejudicing the federal government’s ability to enforce federal law.

The Minnesota bill was signed into law by Governor Tim Walz and is slated to take effect on August 1. It amended state statutes to ban the advertising, creation, operation, or facilitation of prediction-market platforms, effectively constraining the listing of event contracts on platforms like Kalshi and Polymarket. The law’s text specifies that event contracts tied to various categories, including sports outcomes and other contingencies, would be treated as wagers under Minnesota law.

The CFTC’s position is that it holds “exclusive jurisdiction” to regulate prediction markets under the CEA, and it argues that Minnesota’s ban would interfere with the federal framework for these products. The agency asked the court to issue both a preliminary injunction and a permanent injunction to prevent the law from taking effect, emphasizing that the state action would undermine the federal government’s enforcement of federal law.

According to Cointelegraph, the CFTC has, in recent episodes, aligned with Kalshi in multiple state-level challenges to prediction-market constraints and has pursued similar actions against authorities in states such as Connecticut, Illinois, New York, and Ohio. The current Minnesota case is presented as the first outright state legislative ban in the United States, contrasting with prior regulatory-focused actions at the state level. The Commission’s stance has been supported by statements from the agency’s leadership, who have signaled that state restrictions on prediction markets would be challenged in court. In response to Minnesota’s move, Kalshi described the law as unenforceable and constitutionally and federally unlawful, while Polymarket did not immediately respond to inquiries for comment.

Key takeaways

- Federal overreach argument: The CFTC asserts exclusive federal jurisdiction over event contracts under the Commodity Exchange Act, challenging Minnesota’s outright ban on prediction-market activities.

- State law and effective date: Minnesota’s SF 4760, signed by the governor, will prohibit advertising, creation, operation, or facilitation of prediction-market platforms when it takes effect on August 1.

- Judicial remedy sought: The CFTC requests both preliminary and permanent injunctions to halt the Minnesota law from taking effect and to prevent enforcement actions against exchanges listing event contracts.

- Affected entities and responses: The suit directly implicates platform operators such as Kalshi and Polymarket; Kalshi has argued the law is unenforceable, while Polymarket has not issued an immediate public statement.

- Broader crypto policy context in Minnesota: Separately, Minnesota enacted a crypto custody services bill for banks and credit unions, set to take effect August 1, and also passed a ban on crypto kiosks and ATMs in a bid to curb scams—reflecting a broader regulatory approach to crypto activity within the state.

Legal framework and the Minnesota challenge

The CFTC’s legal argument rests on the premise that event contracts—for example, contractual bets on sports results or other future contingencies—fall under the purview of regulated derivatives and swaps, which the federal regulator oversees. By labeling Minnesota’s prohibition on listing or facilitating these contracts as incompatible with federal law, the CFTC contends that the state cannot criminalize exchanges that have received federal approval or the contracts that have been self-certified under federal oversight. The complaint emphasizes the risk that Minnesota’s statute would interfere with the federal government’s ability to enforce federal law governing these markets.

State action and institutional implications for markets

Minnesota’s SF 4760 marks a notable instance of state lawmakers choosing to curtail prediction-market activity outright, moving beyond regulatory restrictions or licensing frameworks seen in other jurisdictions. The CFTC’s challenge highlights a core tension in the U.S. market structure: whether state capitals may expand restrictions on a federally regulated derivative product, potentially creating a patchwork of compliance requirements for exchanges that aspire to operate nationwide. This legal dynamic has immediate implications for platform operators seeking to serve multiple states and for banks or custodians that may consider exposure to or integration with these markets.

From an enforcement and compliance perspective, the case underscores several practical considerations for exchanges and financial institutions:

- Licensing and registration: If the CFTC prevails on jurisdictional grounds, platforms may need to reassess multi-state listing strategies and ensure alignment with federal registration requirements to avoid inadvertent violations.

- Compliance program design: Firms must ensure KYC/AML controls, contract disclosures, and listing procedures meet federal standards for traded products and that cross-border or cross-state listings do not create legal exposure.

- Cross-state regulatory risk: The Minnesota action illustrates how state-level action can complicate a platform’s risk and compliance posture, even when federal preemption is invoked, potentially affecting regulatory anticipation and capital planning.

- Operational certainty: The outcome could influence the timing of product launches, self-certifications, and listing decisions, particularly for platforms seeking to operate with broad access across the United States.

Commentary from platform representatives indicates divergent views on the enforceability and legality of Minnesota’s approach. Kalshi described the law as unenforceable and a constitutional overstep, while Polymarket did not immediately provide a public reaction to the lawsuit. The CFTC’s broader stance in related cases—where it has supported Kalshi in other state actions—adds a layer of strategic tension between federal and state authorities over the governance of prediction markets. These dynamics are being tracked not only by market participants but also by compliance and legal teams evaluating the risk landscape for regulated financial products tied to real-world outcomes.

Regulatory context and policy implications

The Minnesota dispute arrives amid ongoing national and global debates about how prediction markets should be treated within financial regulatory frameworks. The CFTC’s aggressive posture toward state restrictions aligns with a broader trend of asserting federal authority over novel derivatives markets, especially those that could intersect with commodities and securities laws. The case also sits within a larger policy dialogue about how such markets should be regulated in light of anti-fraud, consumer protection, and risk-management concerns.

On the international side, policy makers frequently contrast U.S. approaches with evolving European frameworks, such as MiCA, to illustrate different model outcomes for market integrity, licensing, and cross-border service provision. While MiCA governs crypto-asset service providers within the European Union, cases like Minnesota’s SF 4760 serve as a reminder that cross-jurisdictional coherence remains a critical objective for global market participants seeking to minimize legal and operational risk. For U.S. market participants, the current litigation could influence legislative debates about preemption, federal licensing norms, and the boundaries of state intervention in federally regulated product categories.

Overall, the dispute signals potential near-term attention for exchanges, banks, and investors as courts weigh the balance between state policy experimentation and federal regulatory prerogatives. The court’s ruling will have immediate relevance for the status of prediction-market platforms in Minnesota and could set a precedent for similar challenges in other states that may consider restrictive measures or outright bans. Analysts and compliance teams will be watching for how the court addresses the CFTC’s allegations of exclusive jurisdiction and what that implies for the governance of event contracts in a federated regulatory environment.

Looking ahead, the August 1 effective date of Minnesota’s law remains a critical milestone. The court’s decision on the CFTC’s injunction request will shape the practical viability of prediction-market platforms within Minnesota’s borders and illuminate the broader legal framework governing the intersection of federal derivatives regulation and state policy. As enforcement actions unfold, a clearer picture should emerge on how the federal government will enforce preemptive authority in this space and how state legislators might approach similar issues in the future.

As coverage continues, observers should monitor filings for any narrowing of claims, potential settlements, or interim court orders that could affect product listings, platform operations, or custody arrangements tied to prediction-market activities. In the near term, the Minnesota development reinforces the need for robust regulatory reporting, comprehensive compliance controls, and strategic risk assessments for entities operating or considering entry into federally regulated prediction markets.

Source notes: The CFTC’s press materials and related regulatory filings are publicly accessible, and Minnesotan legislative text can be reviewed through the state’s official repository. For context on related rulings and positions, Cointelegraph has reported on the CFTC’s stance in other state actions, including Kalshi-related matters referenced in this coverage.

Crypto World

$100/Month in Bitcoin Since 2015 Would Have Turned $13,700 Into $632,000, Coinbird Analysis Shows

[PRESS RELEASE – Nuremberg, Germany, May 19th, 2026]

Based on Coinbird DCA Calculator data: monthly Bitcoin buying since 2015 returned +4,515%, while investors would still have endured a 76.72% drawdown, and DCA underperformed lump-sum investing in Coinbird’s tested shorter-term scenarios

New analysis from independent crypto comparison platform Coinbird shows what disciplined monthly Bitcoin buying since 2015 would have actually produced, while also showing where the popular narrative of “just DCA into Bitcoin” oversimplifies the reality.

The findings are based on Coinbird’s Bitcoin DCA Calculator, which uses historical Bitcoin price data from CoinGecko and lets users model recurring investment scenarios going back to 2013.

To run the backtest or explore alternative scenarios, users can visit:

https://www.coinbird.com/cryptocurrencies/bitcoin/dca-calculator

Key findings

- An investor who began a $100/month Bitcoin DCA plan in January 2015 would have made 137 monthly purchases through May 2026, investing a total of $13,700. As of May 19, 2026, the resulting portfolio of 8.219 BTC would be worth approximately $632,315, representing a total return of +4,515% on invested capital. The strategy accumulated Bitcoin at an average acquisition cost of roughly $1,667 per BTC, because early purchases acquired significantly more Bitcoin before prices rose.

- For investors who started later, near the May 2021 market peak before the 2022 crash, a $100/month DCA plan still returned +84.34% in the May 2021–May 2026 scenario — turning $6,100 invested across 61 monthly purchases into approximately $11,244. Over the same period, a lump-sum investment of the full amount made upfront in May 2021 returned approximately +43%. In this specific scenario, DCA outperformed because the strategy automatically accumulated more Bitcoin during the 2022 bear market.

- Importantly, lump-sum investing beat DCA at the 1-, 2-, 3- and 4-year horizons in Coinbird’s tested scenarios. The five-year DCA advantage emerged only after a full crash-and-recovery cycle. The conclusion that “DCA beats lump-sum” is not universal — it depends heavily on start date and market regime.

- DCA investors across the full period still experienced a maximum drawdown of -76.72% during the 2022 bear market, underscoring that recurring purchases do not eliminate volatility or the psychological difficulty of holding through severe declines.

“The interesting finding is not simply that Bitcoin went up since 2015,” said Philipp, Founder of Coinbird. “The interesting finding is that, in this historical scenario, automatic monthly buying through crashes, all-time highs and regulatory uncertainty still produced extraordinary long-term results. At the same time, the drawdowns show why this strategy is much harder to live through than it looks on a chart in hindsight.”

Coinbird’s Bitcoin DCA Calculator is available free of charge and allows users to test different investment amounts, purchase intervals and start dates going back to 2013.

Methodology

The analysis simulates recurring Bitcoin purchases at the selected monthly interval using historical CoinGecko price data. Lump-sum comparisons assume the full planned contribution amount is invested upfront at the start of the selected period. Calculations exclude taxes and trading fees. Past performance does not guarantee future results.

About Coinbird

Coinbird is an independent crypto comparison and market intelligence platform helping retail investors compare cryptocurrencies, exchanges and wallets with clearer data. On coinbird.com, users can explore live market data, compare providers, use crypto calculators and follow market indicators such as the Bitcoin Rainbow Chart, Bitcoin Dominance and Altcoin Season Index.

Coinbird is operated by Coinbird GmbH and is the international platform of kryptovergleich.de, one of Germany’s leading crypto comparison portals, serving more than two million users annually. Across both platforms, Coinbird combines transparent data, practical tools and educational guides for new and experienced crypto investors alike.

The post $100/Month in Bitcoin Since 2015 Would Have Turned $13,700 Into $632,000, Coinbird Analysis Shows appeared first on CryptoPotato.

Bitcoin miners are increasingly positioning themselves as pivotal players in the AI infrastructure supply chain, leveraging their control of sizable power capacity and data-center real estate to support surging demand for AI workloads. A fresh Bernstein analysis shows publicly traded miners collectively plan more than 27 gigawatts of power capacity and have disclosed AI-related agreements totaling over $90 billion, covering about 3.7 gigawatts with hyperscalers, neocloud providers and chipmakers. The finding adds a new dimension to the industry’s post-halving trajectory, suggesting energy and site access could become the true bottlenecks in scaling AI computing, even as crypto mining undergoes a notable pivot toward AI-focused data centers and high-performance computing facilities.

Meanwhile, a RAND research brief released last week estimates the United States could add roughly 82 gigawatts of net available capacity by 2030, underscoring a broader backdrop of expanding demand for data-center-grade power. Bernstein emphasizes that the real constraint now is electricity access—grid interconnections and approvals can take years, complicating plans to scale AI infrastructure at pace. In practice, the wait times for securing a gigawatt of power can stretch to about 50 months across states, with even growth-friendly jurisdictions such as Texas applying batch-review processes to manage interconnection queues and resource loads. The combination of regulatory scrutiny and local opposition to large-scale data centers further compounds these delays, in Bernstein’s view giving miners an edge due to their existing, grid-connected sites and experience running high-density computing facilities.

With AI demand rising, the report frames Bitcoin miners as potential accelerants for AI infrastructure rather than mere participants in a crypto cycle. The authors note that the bottleneck has shifted from silicon to electricity, a change that could reshape strategies across the crypto and broader tech infrastructure sectors.

The analysis arrives amid a broader narrative that the so-called AI supercycle is not only about chip technology or cloud-scale compute, but also about who can reliably provide the energy and real estate required to run demanding AI workloads at scale. The piece links to prior coverage on how miners are moving beyond traditional Bitcoin production to build data-center ecosystems capable of hosting AI-related infrastructure and computing workloads.

Key takeaways

- Miners control a planned power portfolio exceeding 27 GW and have disclosed more than $90 billion in AI-related agreements covering about 3.7 GW with hyperscalers, neocloud providers and chipmakers, according to Bernstein.

- Access to electricity has become the primary scaling constraint for AI data centers, with grid interconnection queues and permitting delays stretching into multi-year timelines in several states.

- RAND projects a significant growth path for US capacity, estimating around 82 GW of net available capacity could be added by 2030, highlighting a larger macro backdrop for AI infrastructure expansion.

- The regulatory environment and local opposition to large data centers are contributing to delays, reinforcing the advantage for miners already operating grid-connected facilities.

- Miner economics are evolving: after the 2024 halving reduced mining rewards, several players are expanding into AI data centers and high-performance computing, with Soluna Holdings reporting a substantial rise in data-center hosting earnings, while IREN is cited as a prime pivot candidate thanks to Microsoft-backed AI agreements.

AI infrastructure takes the lead, while electricity remains the hurdle

Bernstein’s analysis paints a picture of miner-turned-AI infrastructure players extending beyond their core Bitcoin mining activities. After the 2024 halving compressed mining margins, the sector has increasingly pursued revenue diversification through AI data centers and high-performance computing facilities. The emphasis is shifting from raw hashing power to the ability to secure reliable power and proximity to robust data-center ecosystems—assets that miners already command through long-standing grid connections and experience managing complex, dense computing environments.

The practical implication for investors and builders is clear: the value proposition for miners hinges less on the price of Bitcoin and more on their capacity to unlock and monetize AI-ready energy and real estate. The interconnection bottleneck is no longer a theoretical risk but a real choke point that can slow or derail expansion plans. In this context, utility providers’ approval processes, capacity queues and the pace of grid upgrades become material factors shaping the pace of AI infrastructure deployment. This dynamic helps explain why miners with established infrastructure networks may enjoy a structural advantage as AI workloads proliferate across industries.

Real-world pivots: from mining to AI clouds and data centers

The Bernstein study spotlights concrete examples of diversification beyond traditional crypto mining. Soluna Holdings, for instance, reported a meaningful uptick in first-quarter revenue, driven largely by its data-center hosting business rather than crypto mining. The shift mirrors a broader pattern among miners seeking recurring, sizable revenue streams tied to AI-ready facilities rather than volatile mining rewards alone.

Another prominent example cited by Bernstein is IREN, which is viewed as well-positioned to pivot toward AI infrastructure following multibillion-dollar agreements with Microsoft. The premise is simple: if miners can leverage existing sites and operational expertise to house AI compute and related services, they may unlock new growth channels that complement, or even supplant, traditional mining economics over time.

These moves are not merely opportunistic. They reflect a strategic recalibration in response to both market pressures and regulatory realities. By leveraging grid-connected sites and building AI-capable data centers, miners could become essential partners in AI value chains—providing power, cooling, and space for AI cloud services, while also contributing to the resilience and redundancy of AI compute ecosystems.

For investors, the takeaway is that AI infrastructure demand is not a standalone trend but a potential economic expansion path for miners with the scale and site access to support large, power-intensive deployments. It also underscores a broader market shift: the traditional crypto cycle may increasingly ride on AI-driven demand for compute and data-center capacity, rather than price dynamics alone.

What remains uncertain, however, are the policy and regulatory trajectories across different geographies and how quickly grid operators can modernize the interconnection process. The RAND projection of 82 GW of additional capacity by 2030 provides a bullish backdrop, but the pace at which administrators authorize new connections will be crucial. The coming years could determine whether the mining-to-AI infrastructure pivot achieves its intended scale or encounters persistent friction in the form of permitting delays and local opposition.

Beyond the headline figures, the evolving economic model invites a closer look at how specific players balance energy costs, capital expenditure for data-center facilities, and revenue from AI-related services. The Soluna and IREN cases illustrate how diversified revenue streams—from hosting to cloud-style AI offerings—may become a backbone for miner profitability, particularly as traditional block rewards continue to adjust post-halving cycles.

Additionally, the broader AI hardware supply chain remains a critical factor. As miners court partnerships with hyperscalers, cloud providers and chipmakers, the question becomes not only who can secure the most power but who can integrate seamlessly with AI platforms and meet reliability standards essential for enterprise-grade compute workloads. In this sense, the Bernstein analysis casts miners as potential accelerants for AI infrastructure growth, provided they can navigate energy and regulatory complexities with the same efficiency they apply to data-center management.

In short, the convergence of Bitcoin mining and AI infrastructure signals a meaningful shift in how digital asset infrastructure assets are valued. It points to a future where energy access, site strategy and long-term power commitments may determine which players lead in AI-enabled compute—and which ones struggle to scale in the face of interconnection bottlenecks and policy headwinds.

Readers should watch how grid operators, regulators and utility providers respond to this evolving landscape, as well as how mining firms optimize their asset portfolios to capitalize on growing AI demand while managing the risk profile that comes with long interconnection timelines and the complex economics of data-center deployments.

TLDR

- BlackRock transferred 5,847 Bitcoin worth about $450 million to Coinbase Prime through 20 separate transactions.

- The transfer occurred as Bitcoin prices fluctuated near $77,000 after a recent dip earlier in the week.

- Coinbase Prime serves as the custody and trading platform for BlackRock’s iShares Bitcoin Trust ETF.

- The movement likely reflects ETF operations such as redemptions, rebalancing, or internal fund management.

- IBIT has grown to nearly $63 billion in assets since its launch in January 2024.

BlackRock transferred 5,847 Bitcoin worth about $450 million to Coinbase Prime on Tuesday through multiple transactions. The movement occurred as Bitcoin prices fluctuated near $77,000 after a recent dip. Market data shows institutional activity continues alongside shifting price trends.

BlackRock Shifts Bitcoin to Coinbase Prime Accounts

BlackRock executed 20 separate transactions to move 5,847 Bitcoin into Coinbase Prime custody accounts. The transfers drew attention from traders tracking institutional wallet activity.

Coinbase Prime serves as the custody and trading platform for BlackRock’s iShares Bitcoin Trust, known as IBIT. The platform handles asset storage and transaction processing for institutional clients.

The asset manager uses Coinbase Prime to manage Bitcoin, backing its exchange-traded fund holdings. Therefore, such transfers often relate to fund operations rather than direct market sales.

Market participants observed the timing as Bitcoin hovered near $77,000 after dropping to $76,000 earlier. Price data from CoinGecko confirmed the short-term fluctuation.

Analysts stated that transfers to Coinbase Prime may signal ETF redemptions or internal portfolio adjustments. Others added that operational needs also drive these transactions.

One market analyst said, “Movements like these often reflect fund mechanics rather than immediate selling pressure.” The statement reflects common interpretations of institutional transfers.

IBIT launched in January 2024 after regulatory approval for spot Bitcoin ETFs in the United States. The fund has since grown to nearly $63 billion in assets.

Bitcoin Whale Wallets Rise as Accumulation Continues

Data from Santiment shows wallets holding at least 100 Bitcoin increased to 20,229 over the past year. The figure rose from 18,191 wallets recorded during the same period.

These wallets typically belong to institutional investors, large holders, and high-net-worth individuals. Each wallet holds Bitcoin valued at roughly $7.7 million based on current prices.

The steady rise occurred despite price volatility across the past year. Bitcoin experienced several swings, yet large wallet counts continued to grow.

Santiment reported that the increase represents an 11% rise in whale wallet numbers. The data highlights continued accumulation by larger holders.

Smaller traders showed mixed sentiment during recent market movements. However, large holders maintained consistent accumulation patterns.

A market observer said, “Large wallets tend to expand holdings during uncertain periods.” The comment reflects ongoing accumulation trends.

Bitcoin’s price remained close to $77,000 at the time of reporting. Market data showed recovery following the brief dip earlier in the week.

Global Market Today: Asian shares decline, Treasury yields hold gains

CoinDesk 20 performance update: Bitcoin Cash (BCH) rises 2.1%

Ciara Miller Unloads In ‘Summer House’ Reunion Trailer

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Crypto World4 days ago

Crypto World4 days agoBloFin War of Whales 2026 Grand Prix opens registration for $5M trading championship

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Theory – Corporette.com

-

Crypto World4 days ago

Crypto World4 days agoE-Estate Announces 1 Year Live: Washington DC Summit as Real Estate Tokenization Enters Its Next Phase

-

Crypto World7 days ago

Bitcoin Suisse expands with Digital Asset License and Investment Business Act Registration Approval in Bermuda

-

Tech5 days ago

Tech5 days agoTech Moves: Microsoft AI leader jumps to OpenAI; former AI2 exec joins Meta; and more

-

Crypto World6 days ago

Crypto World6 days agoGoogle’s Gemini AI Predicts Incredible Solana Price by the End of 2026

-

Tech4 days ago

Tech4 days agoGoogle reimburses Register sources who were victims of API fraud

-

Business4 days ago

Business4 days agoH&R Real Estate Investment Trust (HR.UN:CA) Q1 2026 Earnings Call Transcript

-

Sports4 days ago

Sports4 days agoNapoleonic enters 2026 Doomben 10,000 field via Abounding withdrawal

-

Entertainment5 days ago

Entertainment5 days agoZara Larsson Has Blunt Response To Chris Brown Diss

-

Crypto World6 days ago

Crypto World6 days agoTwo AI Tokens Lead May Rally, But Risks Are Rising

-

Crypto World4 days ago

Crypto World4 days agoBeInCrypto 100 Institutional Awards Nomination: KAST for Best Digital Assets Neobank and Best Digital Assets Fintech

-

Fashion3 days ago

Fashion3 days agoOn the Scene at Gucci’s Cruise Show in New York City: Mariah Carey, Kim Kardashian, Lindsay Lohan, Iman, and More!

-

Tech7 days ago

Tech7 days agoWhy AI is making typography a boardroom conversation

-

Crypto World4 days ago

Crypto World4 days agoWall Street’s Boldest Gold Prediction Has Russians Rushing to Buy

-

Crypto World4 days ago

Crypto World4 days agoBitcoin Battles US Bond Nerves With BTC Price Dip Toward New May Lows

-

Fashion4 days ago

Fashion4 days agoTrending Western Style Vests Perfect for Summer

-

Politics7 days ago

Politics7 days agoBrad Raffensperger targeted by threat as he runs for governor

-

Entertainment4 days ago

Entertainment4 days agoDavid Letterman Returns to Late Show, Blasts Cancellation

-

Crypto World7 days ago

Crypto World7 days agoGarrett Jin Ethereum whale moves $1.35B to Binance

You must be logged in to post a comment Login